Chapter 7

Global Bond Investing

Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous

editions. We adopted the convention that the first currency is the quoted currency in terms of units

of the second currency.

For example, €:$ = 1.4 indicates that one euro is priced at 1.4 dollars. In previous editions we used

the reversed convention $/€ = 1.4, meaning 1.4 dollars per euro.

All problems in this test bank still use the old convention and have not been adapted to reflect the

new quotation symbols used in the 6th edition.

◼ Questions and Problems

1. What is the difference between a foreign bond and a Eurobond?

2. List three differences between dollar Eurobonds and Yankee bonds.

3. Why did U.S. commercial banks have an interest in the development of the Eurobond market?

56 Solnik/McLeavey • Global Investments, Sixth Edition

4. Give at least two reasons why Eurobonds are issued in bearer form.

5. To provide full protection against unexpected tax imposition, all Eurobond contracts have a covenant

stating that the issuer will increase the interest payments to make up for any tax imposed. Assume

that Paf Inc. has issued a Eurobond with a coupon of $10 per $100 bond. For some reason, Paf Inc. is

forced by its government to transfer 15% of the coupon as withholding tax, so that the net coupon

paid to the bondholder is only $8.50. What should Paf Inc. do, according to the bond covenant?

11.7647%.

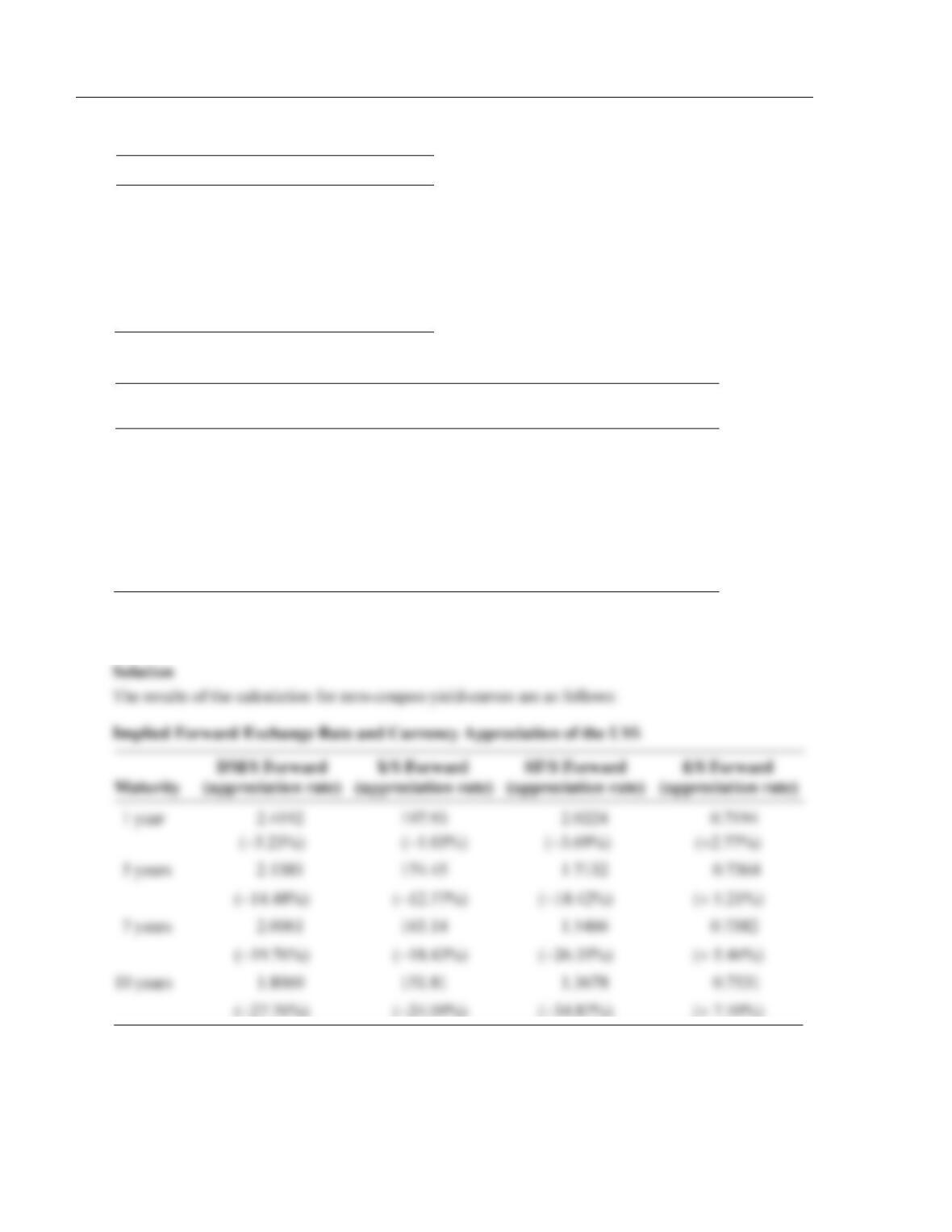

r

=

6. Let’s consider the NKK dual-currency bond shown in Exhibit 7.3. It is a bond quoted in yen at 101%.

What would happen to the market price if the following scenarios took place?

a. The market interest rate on (newly issued) yen bonds drops significantly.

b. The dollar drops in value relative to the yen.

c. The market interest rate on (newly issued) dollar bonds drops significantly.

d. Would you give the same answers if the same bonds were quoted in dollars?

7. Two bond indexes of the same market tend to give the similar total return indications even if their

composition is quite different. Why?

8. Assume that you are an international bank that has lent money to some Latin American countries.

Because of the nonpayment of interest due, you have already taken substantial reserves against these

nonperforming loans. Why would you be willing to exchange these loans for Brady bonds?

9. Discuss the differences between a par and a discount Brady bond.

a. Take the viewpoint of the emerging country.

b. Take the viewpoint of the bondholder.

58 Solnik/McLeavey • Global Investments, Sixth Edition

10. You purchase a Eurobond in euros, at a quoted price of 101.5%. The annual coupon on the bond is

6%, and we are exactly one month after the past coupon date. You buy €100,000 of nominal value of

this bond. What is your total expense?

11. What are the potential biases of the simple yield calculation? Take the example of two straight yen

Eurobonds with the same maturity of five years. Bond A has a coupon of 12% and Bond B, a coupon

of 8%. The current market yield on yen bonds is 10%. These two bonds have the same yield-to–

maturity of 10% and are correctly priced at 107.58% for Bond A and 92.42% for Bond B. What

would be the yield-to-maturity indicated by the simple yield calculation?

Solution

12. Take the example of two straight yen Eurobonds with the same maturity of five years. Bond A has a

coupon of 12% and Bond B a coupon of 8%. The current market interest rate on yen bonds is 9%.

These two bonds have the same yield-to-maturity of 10% and are correctly priced at 111.67% for

Bond A and 96.11% for Bond B. What would be the yield-to-maturity indicated by the simple yield

calculation?

Chapter 7 Global Bond Investing 59

Solution

13. A zero-coupon bond with a five-year maturity is worth 68.06% of its final reimbursement value.

a. Verify that its actuarial yield-to-maturity is equal to 8% by compounding 8% over five years.

b. What is the simple yield of this bond, and why is it so different from the actuarial yield?

Solution

14. What are the annual yield-to-maturity and duration for the following bonds:

a. A zero-coupon bond reimbursed at $100 in ten years and currently selling at $38.

b. A straight bond reimbursed at $100 in ten years, with an annual coupon of 10% and selling

at $110.

c. A perpetual bond with an annual coupon of $8 and currently selling at $110.

Solution

60 Solnik/McLeavey • Global Investments, Sixth Edition

15. The market price of a two-year bond is 105% of its nominal value. The annual coupon to be paid in

exactly one year is 7%. Its yield-to-maturity (European method) is 4.336%.

a. Calculate its duration.

b. Calculate its simple yield.

c. Calculate its semiannual yield (U.S. method).

Solution

Chapter 7 Global Bond Investing 61

16. A bond has been issued in euros with an annual coupon rate of 10%. The previous coupon has just

been paid. This bond has a sinking fund provision: Half of the issue is reimbursed in two years and

half in three years. You hold €10 million of nominal value of this bond.

a. Write the three future annual cash flows in euros, assuming that the previous coupon has just

been paid.

b. The yield curve is currently flat at 9%. What is the value of the bond, its yield–to–maturity, its

duration, and its modified duration?

c. How much do you stand to lose if the yield curve moves uniformly from 9% to 9.1% within

one day?

Solution

17. A straight bond with an annual coupon of 9% will be reimbursed 100% in three years. The previous

coupon has just been paid and this bond currently trades at 105.25%. Its European yield-to-maturity

is 7%.

a. What is its modified duration?

b. What is its semiannual yield-to-maturity?

c. What is its simple yield?

62 Solnik/McLeavey • Global Investments, Sixth Edition

18. You hold a bond with a duration of 17. Its yield is 6% while the cash (one-year) rate is 4%. You

expect yields to move down by 10 basis points over the year.

a. Give a rough estimate of your expected return.

b. What is the risk premium on this bond?

19. A one-year bond is issued by a corporation with a 5% probability of default by year-end. In case of

default, the investor will recover nothing. The one-year yield for default-free bonds is 10%.

a. What yield should be required by investors on these corporate bonds if they are risk neutral?

b. What should the credit spread be?

Chapter 7 Global Bond Investing 63

20. There is a 0.5% probability of default by the year-end on a one-year bond issued at par by a particular

corporation. If the corporation defaults, the investor will not get anything. Assuming that a default-

free bond exists with identical cash flows and liquidity, and the one-year yield on this bond is 4%.

a. What yield should be required by risk-neutral investors on the corporate bond?

b. What should the credit spread be?

21. Several years ago, when the Deutsche mark and French franc still existed, the yield curves were as

follows:

Maturity

US$%

DM%

FF%

1 month

2.10

8.00

7.00

6 months

2.50

7.75

7.15

1 year

3.00

7.00

7.30

2 years

3.50

6.90

7.50

5 years

4.00

6.80

7.60

10 years

4.25

6.75

7.70

Spot Exchange

Rate (per US$)

1.80

5.50

Calculate the implied forward exchange rates, assuming that the interest rates are international money

rates (linear convention) for maturities of less than a year and yields on zero-coupon bonds (European

convention) for maturities of more than one year.

Solution

64 Solnik/McLeavey • Global Investments, Sixth Edition

Forward Rates

Maturity

DM/$

FF/$

1 month

1.8088

5.5224

6 months

1.8467

5.6263

1 year

1.8699

5.7296

2 years

1.9202

5.9333

5 years

2.0557

6.5201

10 years

2.2813

7.6166

22. Back in 1985, when the Deutsche mark still existed, the yield curves were as follows:

Maturity

U.S.

Dollar

Deutsche

Mark

Japanese

Yen

Swiss

Franc

British

Pound

12 months

8.31

4.81

7.19

4.31

11.31

5 years

9.78

6.40

6.82

5.40

10.90

7 years

10.16

6.75

7.00

5.45

11.00

10 years

10.33

6.80

7.33

5.70

11.14

Spot Exchange

Rate (per US$)

2.50

200.00

2.10

0.70

Calculate the implied forward exchange rates, assuming that yields on zero-coupon bonds (European

convention) for maturities of more than one year.

¥/$ Forward

£/$ Forward

Chapter 7 Global Bond Investing 65

23. A young investment banker considers issuing a DM/$ currency option bond for a AAA client and

wonders about its pricing. He knows that currency options are available on the market and that they

could help set the conditions on the bond issue. As a first step, he decides to study a simple case: a

one-year bond. The current market conditions are as follows:

• One-year dollar interest rate: 10%.

• One-year Deutsche mark interest rate: 7%.

• Spot DM/$ exchange rate: $1 = DM 2.

The banker could issue a bond in dollars at 10%, a bond in DM at 7%, or a currency option bond at

an interest rate to be determined. One-year currency options are negotiated on the over-the-counter

market. A one-year currency option to exchange one dollar for two Deutsche marks is quoted at 4%,

that is, four cents per dollar. This is a European option, which can be exercised only at maturity. The

one-year forward exchange rate is:

1 7%

2.

1 10%

F+

=+

a. Given these data, what should the interest rate be on a one-year DM/$ bond?

b. How would you determine how to set the interest rate on an n–year currency bond?

Solution

66 Solnik/McLeavey • Global Investments, Sixth Edition

24. The yields on zero-coupon bonds are as follows:

US$%

Yen%

1 year

3.00

5.00

2 years

3.50

6.00

A young investment banker considers issuing a $/yen dual-currency bond for ¥100 million. It is a

bond with interest paid in yen and principal repaid in dollars. The current spot exchange rate is

$1 = ¥100. The bond will be reimbursed for $1 million in two years. The interest is paid on year

one and year two. What should the interest paid in yen be?

Solution

25. A company is deciding whether to issue a one-year dual-currency bond or a one-year currency option

bond.

• The dual-currency bond would be issued in CHF (Swiss francs) with a principal of 100 CHF per

bond, with interest payable in CHF and principal repaid in U.S. dollars ($50). Denote x the interest

at which this bond is issued.

• The currency option bond is issued in CHF (100 CHF), and the interest and principal are repaid in

CHF or $ at the option of the bondholder. The principal repaid is either 100 CHF or $50, and the

interest rate is either y CHF or 1/2y dollars.

Chapter 7 Global Bond Investing 67

As you guessed, the current spot exchange rate is 2 CHF/$. The current one-year market interest rates

are 6% in CHF and 10% in $. One-year currency options are quoted in Chicago. A put CHF is quoted

at 1.2 U.S. cents per CHF; this option premium is for one CHF, with a strike price of 50 U.S. cents.

a. What is the fair interest rate x on the dual-currency bond?

b. What is the fair interest rate y on the currency option bond?

Solution

68 Solnik/McLeavey • Global Investments, Sixth Edition

26. A young investment banker meets one of its clients, SOSO Inc. that is based in Sydney, Australia.

Current market conditions are the following:

FX Spot rate: AU$/$ = 2.

Interest rate (zero-coupon):

AU$

$

1 year

10%

6%

2 year

11%

7%

Quote in U.S.$ cents for options (strike price: 50 cents per AU$).

PUT AU$

CALL AU$

1 year

2.5

2

2 year

3.5

3

For example a PUT AU$, traded in Chicago, gives the right to sell 1 Australian dollar (AU$) at

50 cents in a year. Its current price is 2.5 cents per AU$.

SOSO would like to issue a bond paying a fixed annual coupon of 6 AU$ and to be reimbursed in a

year 100 AU$ or 50$ at the bearer’s choice.

a. Assuming that the bond is actually issued at 105 AU$, what is the implicit price of the option

linked to that bond? Would you recommend that bond to an investor?

b. If the market was efficient, what is the normal issue price for such a bond?

After many thoughts, SOSO agrees to issue instead a dual-currency bond with an annual coupon in

AU$ and a nominal to be reimbursed in US$ with the following characteristics:

— Issue Price: 100 AU$.

— Reimbursement Price: 50$

— Maturity: 2 years.

— Annual Coupon: C AU$.

c. Under current market conditions, at what level should Coupon C on the dual-currency

bond be set?

Solution

Chapter 7 Global Bond Investing 69

27. Bank PAPOUF decides to issue two bonds and wonders what should be the fair interest rate on these

bonds:

— Bond A: A two-year €/$ dual-currency bond with interest in € and principal in $. The bond is

issued for 100 € and pays an interest rate of i €, each year for two years. The principal is

reimbursed at $50.

— Bond B: A two-year currency option bond. The bond is issued in $ with a face value of $ 100.

The bondholder can choose to have the coupons and principal paid in dollars or in €, at a

specified exchange rate of €/$ = 2, that is, receive either $100 or €200 as principal repayment, or

receive either $C or €2C as interest if C is the coupon set in dollars.

Current market conditions are as follows:

Interest Rate

1-Year

2-Year

US$

8%

8%

€

4%

4%

Currency Options

1-Year Maturity

2-Year Maturity

€ call

2 US cents

5 US cents per €

€ put

1 US cent

3 US cents per €

Spot exchange rate: S = €/$ = 2.

a. What should be the coupon i set on Bond A consistent with current market conditions?

b. What should be the coupon C set on Bond B consistent with current market conditions?

70 Solnik/McLeavey • Global Investments, Sixth Edition

Solution

Chapter 7 Global Bond Investing 71

28. The yield curves in U.S. dollars and Swiss francs are as follows:

U.S. Dollar%

Swiss Franc%

1 Year

10

6

2 Years

12

7

These are yields for zero-coupon bonds of one- and two-year maturities. The spot exchange rate is

SF/$ = 1.5.

a. What are the implied one-year and two-year forward exchange rates?

b. You contemplate issuing a dual-currency bond. You could issue zero-coupon bonds in both

currencies at the interest rates above. Instead, you wish to issue bonds of SF 150 with a coupon C

in Swiss francs, paid each year for two years, and reimbursed for $100 at the end of two years.

What is the interest rate c% (c = C/150) on the bond that would be consistent with the yield

curves above?

c. You contemplate issuing a two-year currency option bond. The bond is issued for $100 and gives

the option to receive the coupons and principal payment in either dollars or Swiss francs at a

fixed exchange rate of SF/$51.5. A bank gives you quotes on the premiums for SF calls with a

strike price of 1/1.5 = 0.66666 US$. The premium for a one-year call is 4 U.S. cents (per Swiss

franc) and for a two-year call is 7 U.S. cents. What coupon rate should you set on your currency

option bond?

Solution

72 Solnik/McLeavey • Global Investments, Sixth Edition

29. Titi, a Japanese company, issued a six-year Eurobond in dollars convertible to shares of the Japanese

company. At time of issue, the long-term bond yield on straight dollar bonds was 10% for such an

issuer. Instead, Titi issued bonds at 8%. Each $1,000 par bond is convertible into 100 shares of Titi.

At time of issue, the stock price of Titi is 1,600 yen and the exchange rate is 100 yen = 0.5 dollar

($/Y = 0.005).

a. Why can the bond be issued with a yield of only 8%?

b. What would happen if:

• The stock price of Titi increases?

• The yen appreciates?

• The market interest rate of dollar bonds drops?

c. A year later, the new market conditions are as follows:

• The yield on straight dollar bonds of similar quality has risen from 10% to 11%.

• Titi stock price has moved up to Y 2000.

• The exchange rate is $/Y = 0.006.

• What would be a minimum price for the Titi convertible bond?

d. Could you try to assess the theoretical value of this convertible bond as a package of other

securities such as a straight bond issued by Titi, options or warrants on the yen value of Titi

stock, an futures and options on the dollar/yen exchange rate?