Chapter 7 – Internal Control and Cash

149. Green Valley Bank sent Comstock Industries its end-of-month bank statement for July. The end of month balance by

the bank is $11,237. The statement shows that a deposit for $4,250 is in transit at the end of the statement period. The

statement also revealed that checks for $87, $105, and $95 are outstanding. Green Valley collected a $4,000 note

receivable plus $120 of interest revenue. The bank charges $20 for the collection service. The bank charges a monthly

account fee of $35. The end-of-month balance per company books is $11,135.

Prepare a bank/account reconciliation and write any necessary journal entries for the reconciliation.

Chapter 7 – Internal Control and Cash

Cash balance according to bank statement

Adjusted balance

Cash balance according to Comstock Industries

Adjusted balance

Jul. 31

Miscellaneous Expense

Miscellaneous Expense

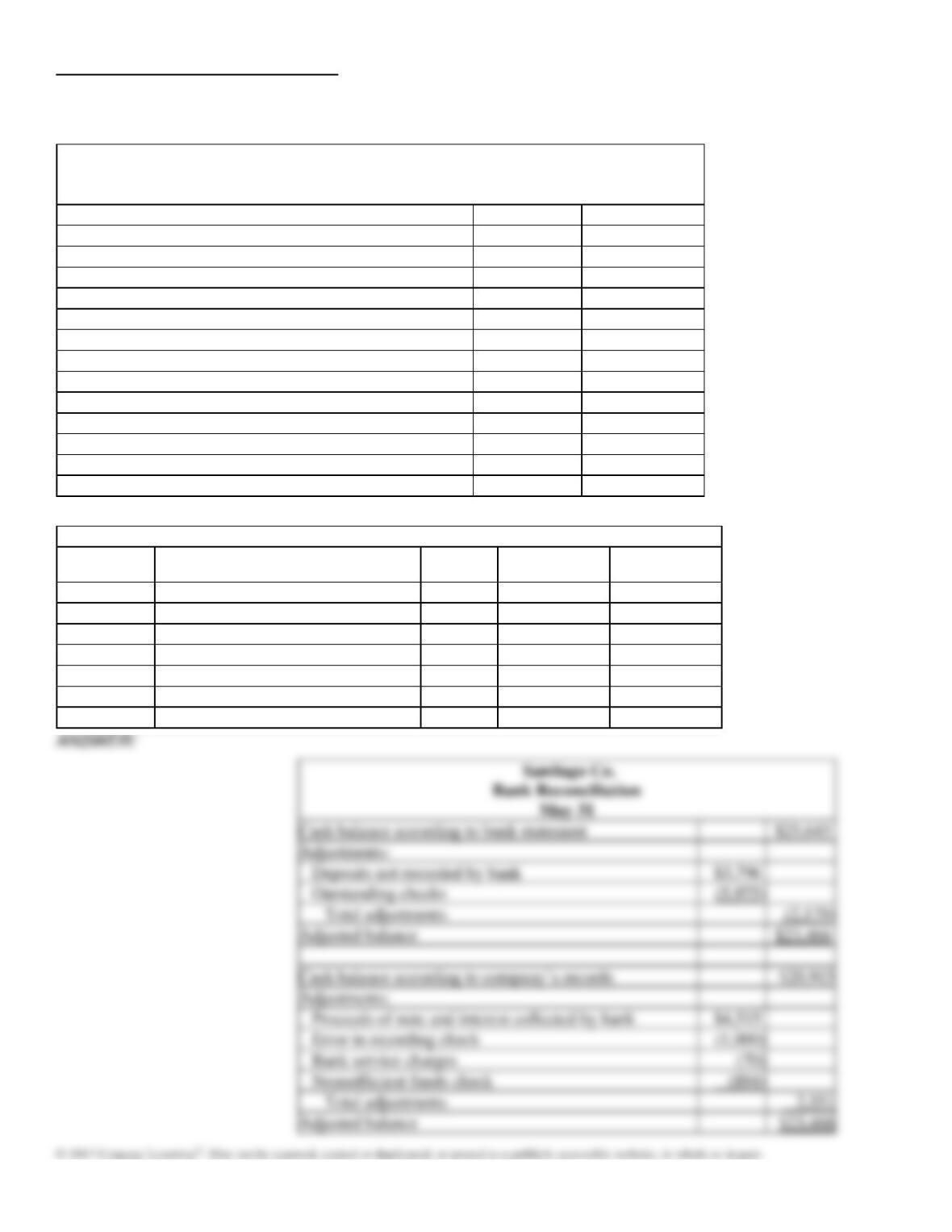

150. The cash account for Santiago Co. on May 31 indicated a balance of $20,915. The March bank statement indicated

an ending balance of $25,645. Comparing the bank statement, the canceled checks, and the accompanying memos with

the records revealed the following reconciling items:

a.

Checks outstanding totaled $5,975.

b.

A deposit of $3,796 had been made too late to appear on the bank statement.

c.

A check for $1,482 returned with the statement had been incorrectly recorded by the

company as $482. The check was originally issued to pay on account.

d.

The bank collected $4,515 on a note left for collection of which $515 was interest revenue.

e.

Bank service charges for May amounted to $70.

f.

A check for $894 was returned by the bank because of insufficient funds.

Prepare a bank reconciliation as of May 31. Journalize the necessary entries.

Chapter 7 – Internal Control and Cash

Santiago Co.

Bank Reconciliation

May 31

Journal

Date

Description

Post. Ref.

Debit

Credit

Chapter 7 – Internal Control and Cash

May 31

Cash

31

Accounts Payable

Miscellaneous Expense

Accounts Receivable

151. The bank statement for Jeffrey Co. indicates a balance of $8,785 on October 31. After the journal entries for October

had been posted, the cash account had a balance of $8,998.

(a)

Cash sales of $945 had been erroneously recorded in the cash receipts journal as $495.

(b)

Deposits in transit not recorded by bank, $778.

(c)

Bank debit memo for service charges, $40.

(d)

Bank credit memo for note collected by bank, $23,985 plus $885 interest.

(e)

Bank debit memo for $756 NSF (not sufficient funds) check from Calin Sams, a customer.

(f)

Checks outstanding, $1,860.

Record the appropriate journal entries that would be necessary for Jeffrey Co.

Cash

Accounts Receivable—Calin Sams

Miscellaneous Expense

Chapter 7 – Internal Control and Cash

152. The bank statement for Gatlin Co. indicates a balance of $7,735 on June 30. After the journal entries for June had

been posted, the cash account had a balance of $4,098.

(a)

Cash sales of $742 had been erroneously recorded in the cash receipts journal as $724.

(b)

Deposits in transit not recorded by bank, $425.

(c)

Bank debit memo for service charges, $35.

(d)

Bank credit memo for note collected by bank, $2,475 including $75 interest.

(e)

Bank debit memo for $256 NSF (not sufficient funds) check from Janice Smith, a customer.

(f)

Checks outstanding, $1,860.

Record the appropriate journal entries that would be necessary for Gatlin Co.

Cash

Accounts Receivable—Janice Smith

Miscellaneous Expense

153. Journalize the entries to record the following:

March 1

Established a petty cash fund of $300.

March 31

The amount of cash in the petty cash fund is now $64. The fund is replenished based

on the following receipts: office supplies, $137; selling expenses, $112.

Record any discrepancy in the cash short and over account.

Journal

Date

Description

Post.

Ref.

Debit

Credit

Chapter 7 – Internal Control and Cash

154. On April 2, Granger Sales decides to establish a $125.00 petty cash fund to relieve the burden on Accounting.

(a) Journalize the establishment of the fund.

(b) On April 10, the petty cash fund has receipts for mail and postage of $43.50, contributions and donations of

$29.50, meals and entertainment of $38.25, and $13.55 in cash. Journalize the replenishment of the fund.

(c) On April 11, Granger Sales decides to increase petty cash to $200.00. Journalize this event.

Chapter 7 – Internal Control and Cash

155. The last custodian of the petty cash fund was hospitalized and you have been asked to take stock of the fund and

replenish it. When you receive the fund, it has $299 in cash and receipts as follows:

Office supplies

$295

Advertising

120

Transportation by Taxi

75

The petty cash fund was established to have $800 in it.

Based on what you have found, what journal entry should be recorded to replenish the fund?

156. Journalize the entries to record the following:

June 1 Established a petty cash fund of $200.

30 The amount of cash in the petty cash fund is now $57. The fund is replenished based on the following receipts:

postage, $25; entertainment, $100; and miscellaneous, $20.

Journal

Date

Description

Post. Ref.

Debit

Credit

June 1

Petty Cash

Postage Expense

Entertainment Expense

Chapter 7 – Internal Control and Cash

157. On April 3, Snappy Sales decides to establish a $135.00 petty cash fund to relieve the burden on Accounting.

(a) Journalize the establishment of the fund.

(b) On April 11, the petty cash fund has receipts for mail and postage of $32.75, contributions and donations of

$25.25, meals and entertainment of $68.00, and $9.75 in cash. Journalize the replenishment of the fund.

(c) On April 12, Snappy Sales decides to increase petty cash to $175.00. Journalize this transaction.

(a) Apr. 3

Petty Cash

(b) 11

Mail and Postage Expense

Contributions and Donations

Meals and Entertainment

(c) 12

Petty Cash

158. Present entries to record the following transactions:

(a)

Established a petty cash fund of $235.00.

(b)

The petty cash fund now has a balance of $42.80. Replenished the fund, based on the

following disbursements as indicated by a summary of the petty cash receipts: office

supplies, $74.50; miscellaneous administrative expense, $92.75; and miscellaneous selling

expense, $18.60.

(c)

Increased the petty cash fund to $300.00.

Chapter 7 – Internal Control and Cash

159. On August 3, Sonar Sales decides to establish a $275.00 Petty Cash Account to relieve the burden on Accounting.

(a) Journalize the establishment of this fund.

(b) On August 11, the petty cash fund has receipts for mail and postage of $124.75, contributions and donations

of $53.25, meals and entertainment of $63.85, and $32.75 in cash. Journalize the replenishment of the fund.

(c) On August 12, Sonar Sales decides to increase petty cash to $400.00. Journalize this transaction.

Chapter 7 – Internal Control and Cash

160. Stephanie Jo Company established a petty cash fund of $300 on May 1. At the end of the month, the petty cash fund

has $42 in cash and receipts for postage, $39; entertainment, $146; and office supplies of $70.

Prepare the needed journal entries, recording any discrepancy in the cash short and over account.

Journal

Date

Description

Post. Ref.

Debit

Credit

161. Journalize the entries to record the following:

Sept. 1 Established a petty cash fund of $350.

30 The amount of cash in the petty cash fund is now $130. The fund is replenished based on the following receipts:

office supplies, $116; postage, $100.

Chapter 7 – Internal Control and Cash

Journal

Date

Description

Post. Ref.

Debit

Credit

Petty Cash

Office Supplies

Postage Expense

Cash Short & Over

162.

(a)

Where are cash equivalents disclosed in the financial statements?

(b)

List three examples of cash equivalents.

(a)

Cash account on the balance sheet

Treasury bills

Chapter 7 – Internal Control and Cash

163. You began your new job as the accountant for Morton Company. You were surprised to find that the company had a

$2,000 petty cash fund, which sits in the break room. The president of the company told you: “Our petty cash system here

works quite smoothly. Since everyone is honest here, everyone has access to the fund for incidentals that might pop up in

the course of the business day. Most of these situations don’t have any receipts tied to them, so I just put the money back

in the fund when my secretary tells me that we have run out of petty cash and we debit the amount to Miscellaneous

Expense.”

(a) Should you implement some controls on petty cash? Why?

(b) If so, what controls could be used for petty cash?

practice that would typically be flagged by the independent auditor.

person of the funds on hand and the payments made by an independent person.

164. Why would a bank require a company to maintain a compensating balance?

Usually a compensating balance is part of a loan agreement or line of credit.

165. Gamma Company and Delta Company have compiled the following data as of the end of the current fiscal year:

Gamma

Delta

Cash

$ 65,700

$302,300

Temporary investments

27,700

125,000

Accounts receivable

2,500

87,000

Inventory

52,400

127,500

Accounts payable

4,500

265,000

Operating expenses

153,000

625,000

Depreciation (one of the operating expenses) for Gamma was $35,000, and for Delta was $65,000.

Chapter 7 – Internal Control and Cash

(1) Calculate days’ cash on hand for Gamma Company and for Delta Company. (Round your answer to one decimal

place.)

(2) Which company has the better liquidity position based on your calculation?

DIFFICULTY:

Bloom’s: Understanding

LEARNING OBJECTIVES:

FNMN.WARR.17.07-ADM – LO: ADM

Match the following elements of internal control:

a.

provides reasonable assurance that business goals will be achieved

b.

used by management for guiding operations and ensuring compliance with requirements

c.

overall attitude of management and employees

d.

used to locate weaknesses and improve controls

e.

identify, analyze and assess likeliness of vulnerabilities

DIFFICULTY:

Easy

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.07-02 – LO: 07–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.10 – Internal Control

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

166. control environment

167. risk assessment

168. control procedures

Chapter 7 – Internal Control and Cash

169. monitoring

170. information and communication

Match each item to a bank statement adjustment, a company books adjustment, or either.

a.

bank statement adjustment

b.

company books adjustment

c.

either

DIFFICULTY:

Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.07-05 – LO: 07–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.11 – Bank Reconciliation

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

171. Outstanding checks

172. NSF check

173. Error in recording a check

174. Bank charges

175. Note collected by the bank

176. Interest revenue

177. Deposit in transit

Assign the letter to indicate whether the following items would be added to or subtracted from the company’s books or the

bank statement during the construction of a bank reconciliation.

a.

added to the company’s books

b.

subtracted from the company’s books

c.

added to the bank statement balance

d.

subtracted from the bank statement balance

DIFFICULTY:

Moderate

Difficulty: Moderate

Bloom’s: Remembering

Chapter 7 – Internal Control and Cash

LEARNING OBJECTIVES:

FNMN.WARD.17.07-05 – LO: 07–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.11 – Bank Reconciliation

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

178. outstanding checks

179. bank service charge

180. deposit in transit

181. NSF check

182. EFT deposit from a customer

183. charges for some other company’s safe deposit box were posted to your account

184. a $1,000 note from one of your customers was collected by the bank

185. interest revenue earned by the note above