Consumers, Producers, and the Efficiency of Markets 1953

41. Let P represent price; let QS represent quantity supplied; and assume the equation of the supply

curve is

If 80 units of the good are produced and sold, then producer surplus amounts to $1,200.

a. True

b. False

42. Let P represent price; let QS represent quantity supplied; and assume the equation of the supply

curve is

If 90 units of the good are produced and sold, then producer surplus amounts to $1,350.

a. True

b. False

1954 Consumers, Producers, and the Efficiency of Markets

43. The cost of production plus producer surplus is the price a seller is paid.

a. True

b. False

44. Total surplus in a market is consumer surplus minus producer surplus.

a. True

b. False

45. Total surplus = Value to buyers – Costs to sellers.

a. True

b. False

Consumers, Producers, and the Efficiency of Markets 1955

46. Total surplus in a market can be measured as the area below the supply curve plus the area above

the demand curve, up to the point of equilibrium.

a. True

b. False

47. Producing a soccer ball costs Jake $5. He sells it to Darby for $35. Darby values the soccer ball

at $50. For this transaction, the total surplus in the market is $40.

a. True

b. False

48. The equilibrium of supply and demand in a market maximizes the total benefits to buyers and

sellers of participating in that market.

a. True

b. False

1956 Consumers, Producers, and the Efficiency of Markets

49. Efficiency refers to whether a market outcome is fair, while equality refers to whether the

maximum amount of output was produced from a given number of inputs.

a. True

b. False

50. Efficiency is related to the size of the economic pie, whereas equality is related to how the pie

gets sliced and distributed.

a. True

b. False

51. Free markets allocate (a) the supply of goods to the buyers who value them most highly and (b)

the demand for goods to the sellers who can produce them at least cost.

a. True

b. False

Consumers, Producers, and the Efficiency of Markets 1957

52. Economists generally believe that, although there may be advantages to society from ticket-

scalping, the costs to society of this activity outweigh the benefits.

a. True

b. False

53. Economists argue that restrictions against ticket scalping actually drive up the cost of many

tickets.

a. True

b. False

54. Ticket scalping can increase total surplus in the market for tickets to sporting events.

a. True

b. False

1958 Consumers, Producers, and the Efficiency of Markets

55. If the United States legally allowed for a market in transplant organs, it is estimated that one

kidney would sell for at least $100,000.

a. True

b. False

56. Even though participants in the economy are motivated by self-interest, the “invisible hand” of the

marketplace guides this self–interest into promoting general economic well–being.

a. True

b. False

57. The current policy on kidney donation effectively sets a price ceiling of zero.

a. True

b. False

Consumers, Producers, and the Efficiency of Markets 1959

58. Wendy is willing to pay $50 for a concert ticket and Bruce would like to receive $25. If the

market price is $40 for this transaction, then the total surplus would be $15.

a. True

b. False

59. Suppose you sell a kayak for $600, but you were willing to sell it for $450. The buyer was willing

to pay $650. The total surplus is $200.

a. True

b. False

60. If a market is in equilibrium, then it is impossible for a social planner to raise economic welfare by

increasing or decreasing the quantity of the good.

a. True

b. False

1960 Consumers, Producers, and the Efficiency of Markets

61. Unless markets are perfectly competitive, they may fail to maximize the total benefits to buyers

and sellers.

a. True

b. False

62. In order to conclude that markets are efficient, we assume that they are perfectly competitive.

a. True

b. False

63. Markets will always allocate resources efficiently.

a. True

b. False

Consumers, Producers, and the Efficiency of Markets 1961

64. When markets fail, public policy can potentially remedy the problem and increase economic

efficiency.

a. True

b. False

65. Market power and externalities are examples of market failures.

a. True

b. False

1962 Consumers, Producers, and the Efficiency of Markets

66. Answer each of the following questions about demand and consumer surplus.

a. What is consumer surplus, and how is it measured?

b. What is the relationship between the demand curve and the willingness to pay?

c. Other things equal, what happens to consumer surplus if the price of a good falls? Why?

Illustrate using a demand curve.

d. In what way does the demand curve represent the benefit consumers receive from

participating in a market? In addition to the demand curve, what else must be considered to

determine consumer surplus?

Consumers, Producers, and the Efficiency of Markets 1963

67. Tammy loves donuts. The table shown reflects the value Tammy places on each donut she eats:

Value of first donut

$0.60

Value of second donut

$0.50

Value of third donut

$0.40

Value of fourth donut

$0.30

Value of fifth donut

$0.20

Value of sixth donut

$0.10

a. Use this information to construct Tammy’s demand curve for donuts.

b. If the price of donuts is $0.20, how many donuts will Tammy buy?

c. Show Tammy’s consumer surplus on your graph. How much consumer surplus would she

have at a price of $0.20?

d. If the price of donuts rose to $0.40, how many donuts would she purchase now? What would

happen to Tammy’s consumer surplus? Show this change on your graph.

1964 Consumers, Producers, and the Efficiency of Markets

Consumers, Producers, and the Efficiency of Markets 1965

68. Answer each of the following questions about supply and producer surplus.

a. What is producer surplus, and how is it measured?

b. What is the relationship between the cost to sellers and the supply curve?

c. Other things equal, what happens to producer surplus when the price of a good rises?

Illustrate your answer on a supply curve.

1966 Consumers, Producers, and the Efficiency of Markets

69. Given the following two equations:

1) Total Surplus = Consumer Surplus + Producer Surplus

2) Total Surplus = Value to Buyers – Cost to Sellers

Show how equation (1) can be used to derive equation (2).

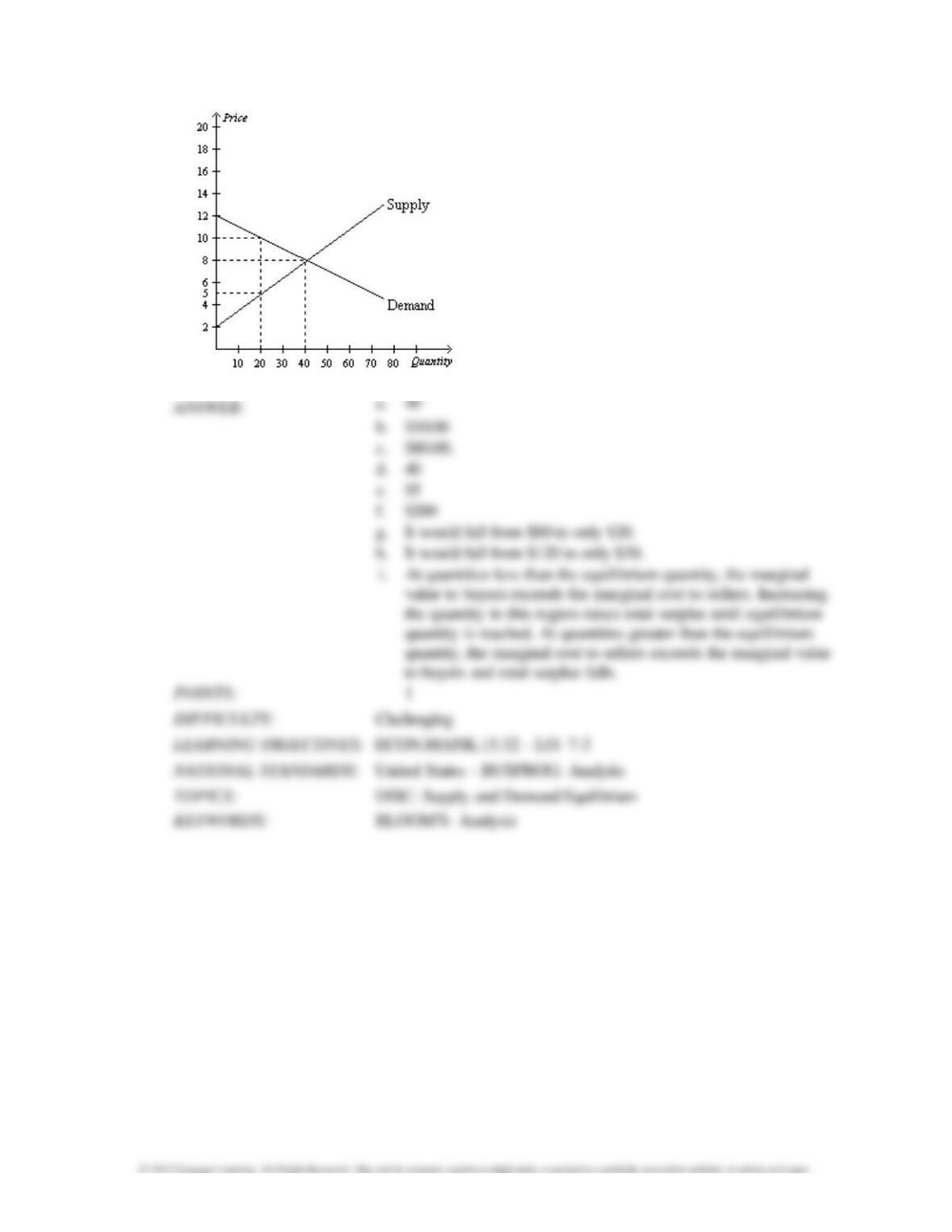

70. Answer the following questions based on the graph that represents J.R.‘s demand for ribs per

week at Judy’s Rib Shack.

a. At the equilibrium price, how many ribs would J.R. be willing to purchase?

b. How much is J.R. willing to pay for 20 ribs?

c. What is the magnitude of J.R.’s consumer surplus at the equilibrium price?

d. At the equilibrium price, how many ribs would Judy be willing to sell?

e. How high must the price of ribs be for Judy to supply 20 ribs to the market?

f. At the equilibrium price, what is the magnitude of total surplus in the market?

g. If the price of ribs rose to $10, what would happen to J.R.’s consumer surplus?

h. If the price of ribs fell to $5, what would happen to Judy’s producer surplus?

i. Explain why the graph that is shown verifies the fact that the market equilibrium (quantity)

maximizes the sum of producer and consumer surplus.

Consumers, Producers, and the Efficiency of Markets 1967

1968 Consumers, Producers, and the Efficiency of Markets

Problems

1. What do economists call the highest amount a consumer will pay to purchase a good?

2. If John’s willingness to pay for a good is $20 and the price of the good is $15, how much is John’s

consumer surplus

from purchasing the good?

Table 7-18

The following table shows the willingness to pay for a good for the only four consumers in a

market.

Consumer

Willingness to Pay

A

$25

B

$40

C

$15

D

$30

3. Refer to Table 7-18. If the price of the good is $20, how many units will be demanded?

Consumers, Producers, and the Efficiency of Markets 1969

4. Refer to Table 7-18. If the price of the good is $20, how much is the total consumer surplus?

Scenario 7-1

Suppose market demand is given by the equation

5. Refer to Scenario 7-1. If the market equilibrium price is $10, how much is total consumer surplus

in this market?

6. Refer to Scenario 7-1. If the market equilibrium price rises from $10 to $15, what is the change

in total consumer surplus in the market?