Chapter 7 – Internal Control and Cash

125. The following procedures were recently implemented at the Pampered Pets, Inc. For each procedure, indicate

whether the internal control over cash represents (1) a strength or (2) a weakness. If it is a weakness, please explain why.

(a) At the end of the day, cash register clerks are required to use their own funds to make up any cash shortages

in their registers.

(b) At the end of the day, an accounting clerk compares the duplicate copy of the daily cash deposit slip with the

deposit receipt obtained from the bank.

(c) After necessary approvals have been obtained for the payment of a voucher, the treasurer signs and mails the

check. The treasurer then stamps the voucher and supporting documentation as paid and returns the voucher

and supporting documentation to the accounts payable clerk for filing.

(d) Along with the petty cash receipts for postage, office supplies, etc., several postdated employee

checks are in the petty cash fund.

Chapter 7 – Internal Control and Cash

126. The following selected transactions relate to cash collections for a firm that maintains a $100 change fund at all

times. Present entries to record the transactions for each of the two days of cash receipts from sales.

(a)

Actual cash in cash register, $5,412.36; cash receipts per cash register tally, $5,413.07.

(b)

Actual cash in cash register, $3,712.95; cash receipts per cash register tally, $3,712.16.

Cash

Cash Short and Over

Cash

127. The actual cash received during the week ended June 6 for cash sales was $8,276 and the amount indicated by the

cash register total was $8,262. Journalize the entry to record the cash receipts and cash sales.

Journal

Date

Description

Post. Ref.

Debit

Credit

June 16

Cash

Chapter 7 – Internal Control and Cash

128. The actual cash received during the week ended October 31 for cash sales was $23,447 and the amount indicated by

the cash register total was $23,457. Journalize the entry to record the cash receipts and cash sales.

Journal

Date

Description

Post. Ref.

Debit

Credit

Date

Credit

Oct. 31

Cash

Cash Short and Over

129. Consider the following information from the cash account. Assume cash payments were 84% of collections.

Cash

??

Beg. balance

$245,000

Collections

??

Disbursements

$80,275

End balance

How much was the beginning balance of the cash account?

Chapter 7 – Internal Control and Cash

130. Describe the features of a voucher system and list typical supporting documents for a voucher.

131. The actual cash received during the week ended June 7 for cash sales was $18,632, and the amount indicated by the

cash register total was $18,628. Journalize the entry to record the cash receipts and cash sales.

Journal

Date

Description

Post.

Ref.

Debit

Credit

Chapter 7 – Internal Control and Cash

132. Consider the following journal entry made by Jones Company for one day’s sales of a single cashier. Upon

investigation, what might you find happened to create this amount of Cash Over/Short account difference? Give three

possible reasons for this difference.

Cash

2,235.00

Cash Short and Over

100.00

Sales

2,135.00

133. List the principal advantages of electronic funds transfers.

Chapter 7 – Internal Control and Cash

134. You are trying to explain debit and credit memos that appear on bank statements and whether these will increase or

decrease your company’s bank account balance. Complete the following table to help your new staff understand.

ITEM

Debit

or

Credit

Memo

Increases or Decreases

the Company’s Bank

Account Balance

EFT payment

Bank correction of an error due to posting another

customer’s check to your account

Service charge

Note and interest collected for our company

NSF check

Bank correction of an error recording a $250

deposit as $520

EFT deposit

EFT payment

Bank correction of an error due to posting

Service Charge

Note and interest collected for our company

NSF check

EFT deposit

135. The following items may appear on a bank statement:

1.

NSF check

2.

EFT deposit

3.

Service charge

4.

Bank correction of an error from recording a $300 check as $30.

Chapter 7 – Internal Control and Cash

Indicate whether the item would appear as debit or credit memo on the bank statement and whether the item would

increase or decrease the balance of your account. Use the following format:

Appears on the

Bank Statement as a

Increases (Decreases) the

a Debit or Credit

Balance of the Company’s

Item No.

Memo

Bank Account

Bank Statement as a

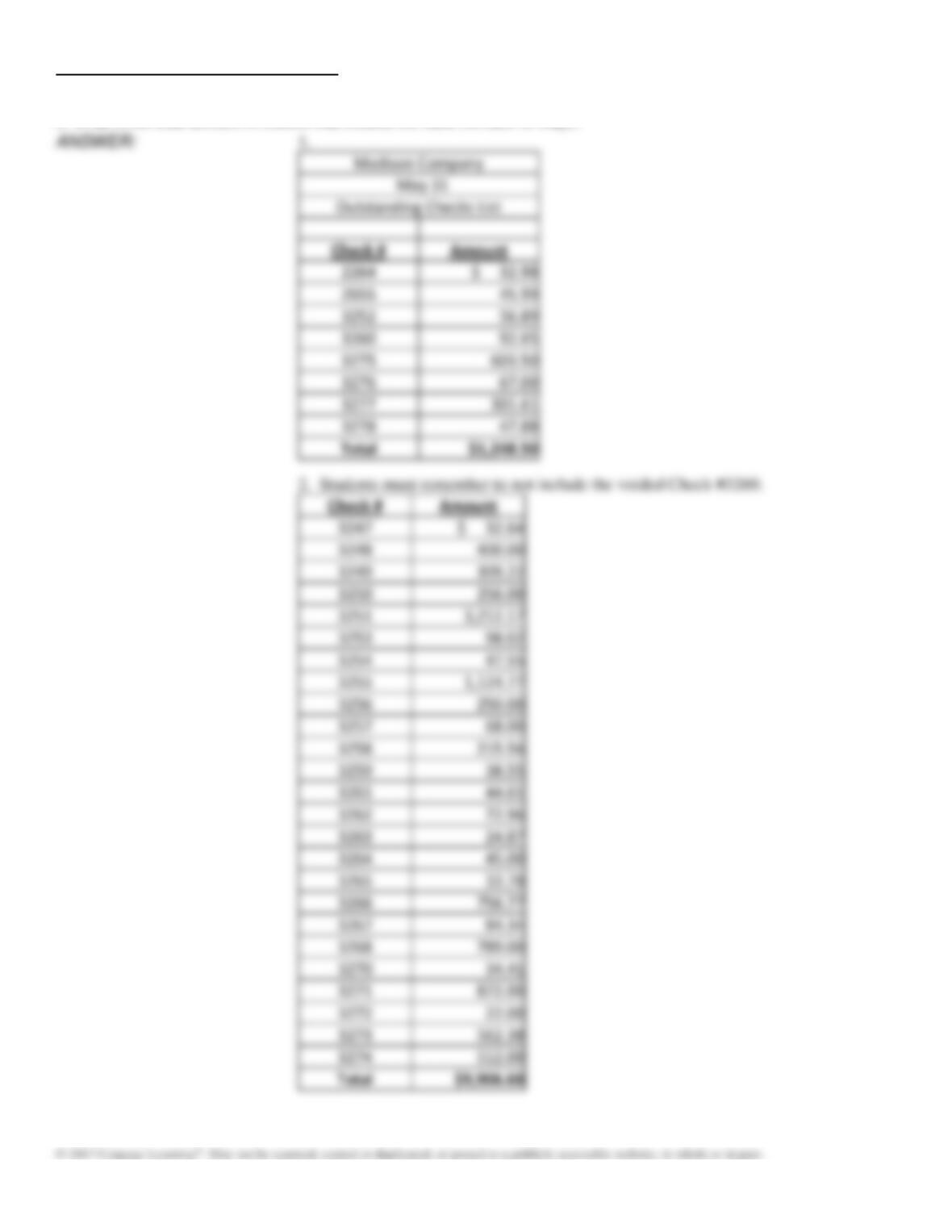

136. The following information is from Madison Corporation’s accounting records for May. Check #3269 was returned

as a double payment and voided. Checks that have not cleared the bank include #3252, #3260, and series #3275–3278.

Check #

Amount

Check #

Amount

3247

$ 32.64

3263

$ 24.87

3248

400.00

3264

45.00

3249

309.22

3265

33.78

3250

256.00

3266

756.77

3251

3,212.17

3267

84.34

3252

56.89

3268

789.00

3253

98.02

3269

48.90

3254

47.55

3270

34.41

3255

1,124.77

3271

872.00

3256

250.00

3272

22.00

3257

68.00

3273

562.38

3258

215.56

3274

512.00

3259

38.55

3275

603.50

3260

92.65

3276

67.00

3261

44.61

3277

301.61

3262

72.96

3278

47.88

In addition to the above list of the checks, Madison had check #2264 for $32.98 and check #2655 for $45.99 outstanding

previously that have not cleared.

Chapter 7 – Internal Control and Cash

1. Create an outstanding checks list for Madison at the end of May.

2. What is the total amount of checks that cleared the bank (written in May)?

Chapter 7 – Internal Control and Cash

137. The Scharf Company is a retailer located in a state without sales tax. The following data was given to you to

complete the transactions for the day’s sales to be recorded. All cash drawers start with $100 in change.

Reg. #1

Reg. #2

Reg. #3

Reg. #4

Cash in drawer

$974.50

$1,383.66

$939.46

$1,137.91

Sales reading

$879.50

$1,298.16

$839.46

$1,030.33

Difference

Record the journal entries for EACH cash register to determine the cashier’s accuracy.

Account

Debit

Credit

Chapter 7 – Internal Control and Cash

138. Jackson Industries has collected the following information but needs assistance completing the table. The cash

payments were 90% of collections.

Cash

??

Beg. balance

$511,770

Collections

??

Payments

$102,275

End balance

How much was the beginning balance of the cash account?

Cash

Beg. balance

$511,770

Collections

$460,593

Payments

$102,275

End balance

139. Identify each of the following reconciling items as (a) an addition to the cash balance according to the bank

statement, (b) deduction from the cash balance according to the bank statement, (c) an addition to the cash balance

according to the company’s records, or (d) a deduction from the cash balance according to the company’s

records. Assume that none of the transactions reported by bank debit and credit memos have been recorded by the

company. Also, indicate by writing “entry” by those items that will require a journal entry in the company’s accounts.

1.

Deposits in transit.

2.

Bank service charges.

3.

NSF check.

4.

Outstanding checks.

5.

Check for $690 incorrectly recorded by the company as $960.

6.

Check for $420 incorrectly recorded by the company as $240.

Chapter 7 – Internal Control and Cash

140. Using the following information, prepare a bank reconciliation for Miller Co. for August 31:

(a)

The bank statement balance is $4,690

(b)

The cash account balance is $5,080.

(c)

Outstanding checks amounted to $715.

(d)

Deposits in transit are $1,020.

(e)

The bank service charge is $40.

(f)

A check for $72 for supplies was recorded as $27 in the ledger.

Cash balance according to bank statement

Adjustments:

Adjusted balance

Cash balance according to company’s records

Adjustments:

Adjusted balance

Chapter 7 – Internal Control and Cash

141. Using the following information, prepare a bank reconciliation for Candace Co. for May 31:

(a)

The bank statement balance is $2,936.

(b)

The cash account balance is $3,194.

(c)

Outstanding checks amounted to $465.

(d)

Deposits in transit are $655.

(e)

The bank service charge is $50.

(f)

A check for $97 for supplies was recorded as $79 in the ledger.

Cash balance according to bank statement

Adjustments:

Adjusted balance

Cash balance according to company’s records

Adjustments:

Adjusted balance

142. Bank reconciliation information for Kaden Co. for May 31 is as follows:

(a)

The bank statement balance is $2,936.

(b)

The cash account balance is $3,194.

(c)

Outstanding checks amounted to $465.

(d)

Deposits in transit are $655.

(e)

The bank service charge is $50.

(f)

A check for $97 for supplies was recorded as $79 in the ledger.

Record the appropriate journal entry for Kaden Co.

Miscellaneous Expense

Supplies

Chapter 7 – Internal Control and Cash

143. The bank statement for Farmer Co. indicates a balance of $7,735.00 on June 30. After the journal entries for June

had been posted, the cash account had a balance of $4,098.00. Prepare a bank reconciliation on the basis of the following

reconciling items:

(a)

Cash sales of $742 had been erroneously recorded in the cash receipts journal as $724.

(b)

Deposits in transit not recorded by bank, $425.

(c)

Bank debit memo for service charges, $35.

(d)

Bank credit memo for note collected by bank, $2,475 including $75 interest.

(e)

Bank debit memo for $256 NSF (not sufficient funds) check from Janice Smith, a customer.

(f)

Checks outstanding, $1,860.

Cash balance according to bank statement

Adjustments:

Adjusted balance

Cash balance according to company’s records

Adjustments:

Bank service charges

Total adjustments

Adjusted balance

144. Accompanying a bank statement for Marsh Land Properties is a credit memo for payment on a $15,000 1-year note

receivable and $900 of interest collected by the bank. Marsh Land Properties had been notified by the bank at the time of

collection, but had made no entries. Journalize the entry that should be made by Marsh Land to bring the accounting

records up to date.

Chapter 7 – Internal Control and Cash

145. For each of the following, explain whether the issue would require you to prepare a journal entry for your company,

assuming any original entry is correct. If an entry is required, please include it as part of your answer.

(1) The bank recorded your deposit as $91 rather than the actual amount of $191.

(2) Two outstanding checks amounted to $450.

(3) Company check number 538 for postage was recorded incorrectly by the company bookkeeper as $50 instead

of $59.

(4) The bank paid a check for $500 after the company had issued a stop payment and voided the check.

(5) An EFT deposit was made by one of the company’s customers, Atlas Design, for merchandise received. The

sale had previously been recorded when shipped and was equal to the payment amount of $125.

146. The following data were gathered to use in reconciling the bank account of Savannah Company:

Balance per bank

$16,750

Balance per company records

16,125

Bank service charges

80

Deposit in transit

2,195

NSF check

950

Outstanding checks

3,850

What is the adjusted balance on the bank reconciliation?

$15,095 ($16,750 + $2,195 – $3,850) or ($16,125 – $80 – $950)

Chapter 7 – Internal Control and Cash

147. The following data were gathered to use in reconciling the bank statement of Build-A-Lot:

Balance per bank

$14,355

Balance per company records

14,010

Bank service charges

80

Deposits in transit

4,100

NSF checks

775

Outstanding checks

5,300

(1) What is the adjusted balance on the bank reconciliation?

(2) Journalize any necessary entries for Build-A-Lot based on the bank reconciliation.

Accounts Receivable

Miscellaneous Expense

148. Roper Electronics received its bank statement for the month of August with an ending balance of $11,740. Roper

determined that check #613 for $155 and check #601 for $420 were both outstanding. Also, a $6,900 deposit for August

30 was in transit as of the end of the month. Northern Regional Bank also collected a $5,000 note receivable on August 1

that was issued March 1. Accrued interest is $250. Northern Regional Bank charged a $35 fee for the collection

service. The bank statement reveals a bank service charge of $20. A customer check for $68 was returned with the bank

statement marked “NSF.” The ending balance of the Roper cash account is $12,938.

Prepare a bank/account reconciliation and any necessary journal entries for the reconciliation.