164. Albemarle, Inc., has two producing departments. Each producing department is held responsible for a share

of the costs of a support department.

Actual and budgeted data are as follows:

2011

Support department hours used:

Department X

8,000

Department Y

16,000

Total hours

24,000

Support department costs:

Actual support department costs

$72,000

Budgeted fixed service center costs

$24,000

Budgeted variable rate per hour

$3.00

Normal support department usage is 12,000 hours each for Department X and Department Y.

Required:

a.

Assuming the purpose is product costing, allocate the costs of the support department using the direct method.

b.

Assuming the purpose is to evaluate performance, allocate the costs of the support department.

Department X

Department Y

Variable costs allocated:

($3.00 ´ 12,000)

$36,000

($3.00 ´ 12,000)

$36,000

Fixed costs allocated:

[$24,000 ´ (12,000/24,000)]

12,000

12,000

$48,000

$48,000

b.

Department X

Department Y

Variable costs allocated:

($3.00 ´ 8,000)

$24,000

($3.00 ´ 16,000)

$48,000

Fixed costs allocated:

[$24,000 ´ (12,000/24,000)]

12,000

12,000

$36,000

$60,000

165. Chrome Enterprises has two support departments (S1 and S2) and two producing departments (A and B).

The distribution of services by the support departments is as follows:

Services Provided to

Services Provided from

S1

S2

A

B

S1

–

8%

74%

18%

S2

21%

–

47%

32%

Total department costs for the support and producing departments are as follows:

S1

$ 58,000

S2

124,000

A

712,000

B

568,000

Required:

Find the amount of total costs for A and B using the reciprocal method.

S1

S2

A

B

Direct costs

$58,000

$124,000

$712,000

$568,000

Allocate S1

(85,476)

6,838

63,252

15,386

Allocate S2

27,476

(130,838)

61,494

41,868

$ -0-

$ -0-

$836,746

$625,254

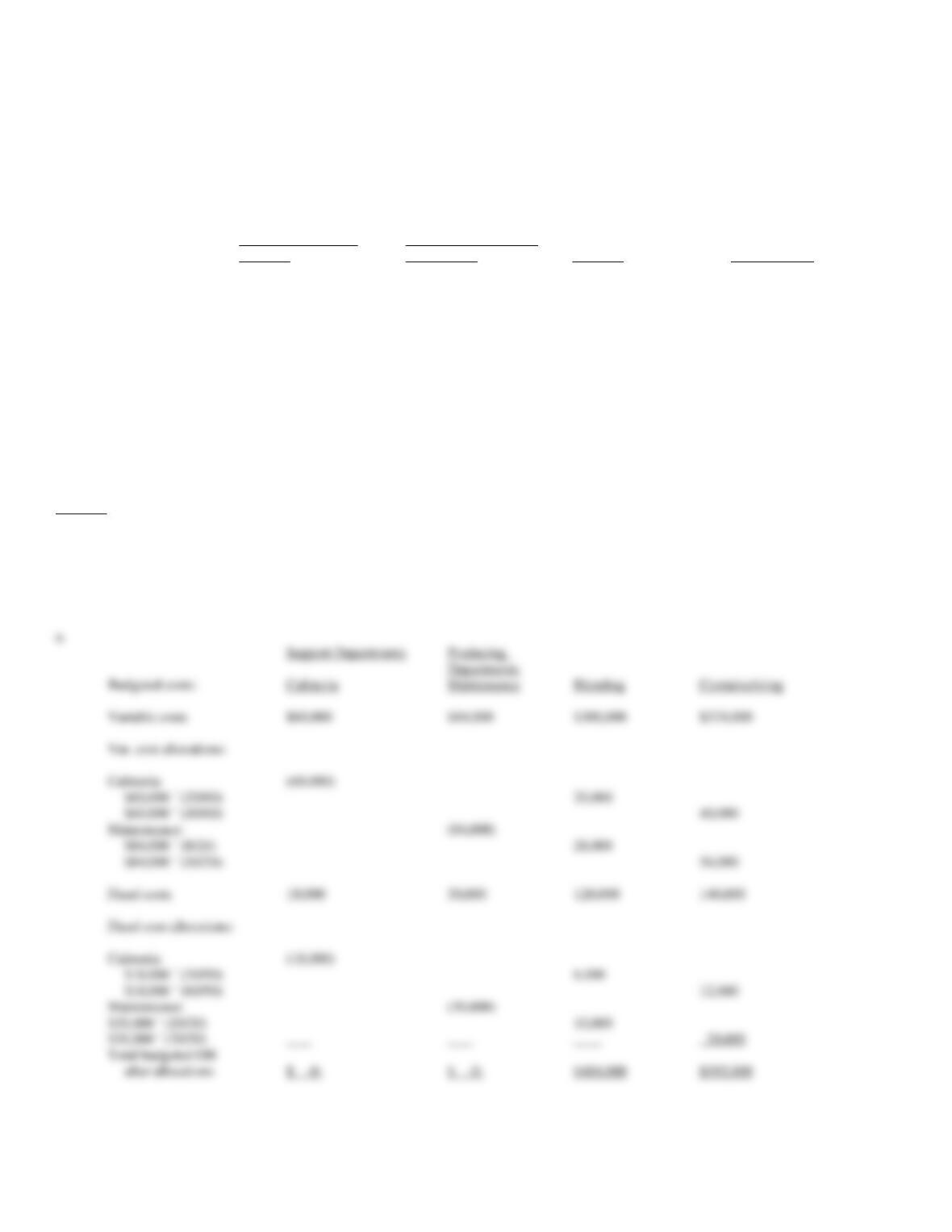

166. Eagle Company applies factory overhead in its two producing departments using a predetermined rate

based on budgeted machine hours in the Blending Department and based on budgeted labor hours in the

Containerizing Department. Variable cafeteria costs are allocated to the producing departments based on

budgeted number of employees, and fixed costs are allocated based on the capacity number of employees.

Variable maintenance costs are allocated on the budgeted number of direct labor hours, and fixed costs are

allocated on labor hour capacity. The data concerning next year’s operations are as follows:

Support Departments

Producing Departments

Budgeted costs:

Cafeteria

Maintenance

Blending

Containerizing

Variable costs

$60,000

$84,000

$300,000

$324,000

Fixed costs

18,000

30,000

120,000

140,000

Other data:

Direct labor hours (capacity)

10,000

20,000

Direct labor hours (budgeted)

8,000

16,000

Number of employees (capacity)

30

60

Number of employees (budgeted)

20

40

Machine hours (capacity)

33,000

66,000

Machine hours (budgeted)

20,000

60,000

Required:

a.

Prepare a schedule showing the allocation of budgeted support department costs to producing departments.

b.

Determine the predetermined overhead rate for the producing departments.

a.

Departments

Budgeted costs:

Cafeteria

Maintenance

Blending

Containerizing

Variable costs

$60,000

$84,000

$300,000

$324,000

Var. cost allocations:

Cafeteria:

(60,000)

$60,000 ´ (20/60)

20,000

$60,000 ´ (40/60)

40,000

Maintenance:

(84,000)

$84,000 ´ (8/24)

28,000

$84,000 ´ (16/24)

56,000

Fixed costs

18,000

30,000

120,000

140,000

Fixed cost allocations:

Cafeteria:

(18,000)

$18,000 ´ (30/90)

6,000

$18,000 ´ (60/90)

12,000

Maintenance:

(30,000)

$30,000 ´ (10/30)

10,000

$30,000 ´ (20/30)

20,000

Total budgeted OH

167. McDuff Company uses a job-order costing system to compute product costs. There are two producing

departments (P1 and P2) and two support departments (S1 and S2). The costs incurred in S1 and S2 are

allocated to Departments A and B and included in their factory overhead rates for costing products. S1 costs are

allocated based on the number of employees, S2 costs are allocated based on direct labor hours, and the

production departmental overhead rates are also based on direct labor hours. The following data are available

for a recent period:

S1

S2

P1

P2

Direct department costs

$12,000

$18,000

$70,000

$117,500

Number of employees

8

12

48

72

Direct labor hours

450

325

2,250

1,800

Required:

a.

Prepare a schedule allocating the support department costs to the producing departments using the sequential allocation method. The

department with the greatest percentage of interdepartmental services should be allocated first.

b.

Determine the overhead rates per direct labor hour for P1 and P2.

c.

Job A2 was completed during the period at a cost of $26,000 for direct materials and direct labor costs. This job required 21 direct labor

hours in Department P1 and 15 direct labor hours in Department P2. What was the total cost of Job A2?

Determination of order of allocation:

S1 = 12/(12 + 48 + 72) = 9.09%

S2 = 450/(450 + 2,250 + 1,800) = 10%

S2 is allocated first.

S2 allocation:

Total

Allocation base (DLH)

4,500

450

2,250

1,800

Percent of total base

100%

10%

50%

40%

Cost allocation

$18,000

$1,800

$9,000

$7,200

S1 allocation:

Percent of total base

100%

40%

60%

Cost allocation

$13,800

$5,520

$8,280

Cost allocation summary:

Total

Dept. costs

$12,000

$18,000

$70,000

$117,500

$217,500

Cost allocations:

S2

1,800

(18,000)

9,000

7,200

–

S1

(13,800)

–

5,520

8,280

–

Department costs

after allocation

$ -0-

$ -0-

$84,520

$132,980

$217,500

168. Mainstream Corporation manufactures two products, I and II, from a joint process. A production run costs

$20,000 and results in 500 units of I and 2,000 units of II. Both products must be processed past the split-off

point, incurring separable costs of $5 per unit for I and $10 per unit for II. The market price is $25 for I and $20

for II.

Required:

a.

Allocate joint production costs to each product using the physical units method.

b.

Allocate joint production costs to each product using the net realizable value method.

c.

Allocate joint production costs to each product using the constant gross margin percentage method.

I

500

5/25 ´ $20,000 =

$ 4,000

2,000

20/25 ´ $20,000 =

$16,000

2,500

$13,333

Costs (500 ´ $5) + (2,000 ´ $10) + $20,000 = $42,500

COGS Percentage = $42,500/$52,500 = 80.9524%

I: (500 ´ $25 ´ 80.9524%) – $2,500 = $7,619.05

II: (2,000 ´ $20 ´ 80.9524%) – $20,000 = $12,380.96

b.

Total (1)

$84,520

$132,980

Factory overhead per DLH ((1)/(2))

$ 37.56

$ 73.88

c.

Direct materials and direct labor

$26,000.00

Department A factory overhead (21 hours ´ $37.56)

788.76

Department B factory overhead (15 hours ´ $73.88)

1,108.20

169. Soy Products produces two products, Soyburgers and Soy steaks, in a single process. In 2014, the joint

costs of this process were $36,000. In addition, 20,000 pounds of soyburgers and 10,000 pounds of soy steaks

were produced. Separable processing costs beyond the split-off point were: soyburgers, $7,500; soy steaks,

$4,500. Soyburgers sells for $2 per pound; Soy steaks sells for $4 per pound.

Required:

a.

Allocate the joint costs using the net realizable value method.

b.

Allocate the joint costs using the physical units method.

Soyburgers

$40,000

$7,500

$32,500

$32,500/$680,000

Soy Steaks

$40,000

$4,500

35,500

$35,500/$680,000

$68,000

b.

Units

Fraction

Allocation

30,000

170. Henderson Company pays a flat fee of $500 for the right to retrieve stray golf balls from lakes and ponds at

golf and country clubs. The recovered balls are then cleaned, graded as to quality (birdie, bogey, or duffer), and

sold to sporting goods stores at the following prices per dozen: birdie quality, $5; bogey quality, $4; and duffer

quality, $3. Last month $8,000 of cost was incurred retrieving the following quantities of golf balls: birdie

quality, 1,000 dozen; bogey quality, 3,000 dozen; and duffer quality, 2,000 dozen.

Required: (Calculate relative quantity to three decimal points.)

a.

Determine the cost and gross profit percent for each type of golf ball using the physical units method of joint cost allocation.

b.

Repeat part (a) using the sales-value-at-split-off method of joint cost allocation.

c.

The company has an opportunity to sell bogey quality balls for $4.50 per dozen to a company that operates golf driving ranges; however,

the balls will have to be painted and striped. The company estimates that the cost of painting and striping will be 60 cents per dozen.

Assuming the physical unit method is used to allocate joint costs, should the offer be accepted?

a.

Quantity

Relative

Birdies

1,000

0.167 ´

$8,000 =

$1,336

Bogeys

3,000

0.500 ´

$8,000 =

4,000

Duffers

2,000

0.333 ´

$8,000 =

2,664

Total

6,000

1.000

$8,000

Birdies

Bogeys

Duffers

Total

Unit sales (dozens)

1,000

3,000

2,000

6,000

Sales

$5,000

$12,000

$6,000

$23,000

Joint costs

1,336

4,000

2,664

8,000

Gross profit %

73.28%

66.67%

55.60%

65.22%

b.

Relative

Product

Sales Value

Sales Value

Joint Cost

Allocation

Birdies

$ 5,000

0.22 ´

$8,000 =

$1,760

Duffers

6,000

0.26 ´

$8,000 =

2,080

$23,000

1.00

$8,000

Sales

$5,000

$12,000

$6,000

$23,000

Joint costs

1,760

4,160

2,080

8,000

Gross profit

$3,240

$ 7,840

$3,920

$15,000

Gross profit %

64.800%

65.333%

65.333%

65.217%

c.

The decision to accept the offer is not affected by the allocation of joint costs, only the relevant revenues and costs after split-off. Since the

171. Compare and contrast the various methods of accounting for joint product costs.

172. Saturn Company manufactures products X, Y, and Z in a joint process. The following information is

available:

Products

X

Y

Z

Total

Units produced

12,000

?

?

24,000

Sales value

at split-off

?

?

$50,000

$200,000

Joint costs

$48,000

?

?

$150,000

Sales value if

processed further

$110,000

$90,000

$60,000

$260,000

Additional cost if

processed further

$18,000

$14,000

$10,000

$42,000

Joint product costs are allocated using the sales value at split-off approach.

Required:

a.

What is the sales-value-at-split-off for Product X?

b.

What is the amount of joint costs allocated to Product Y using the sales-value-at-split-off method?

c.

If the company used the physical units method to allocate joint cost, how much joint cost would be allocated to Product X?

a.

$48,000/$150,000 ´ $200,000 = $64,000

b.

{$150,000 – $48,000 – [($50,000/$200,000) ´ $150,000]} = $64,500

c.

12,000/24,000 ´ $150,000 = $75,000

173. Vladimir, Inc. began the current period with no inventories. During the period, it processed 50,000 pounds

of materials costing $450,000. Conversion costs incurred during the period amounted to $660,000. The firm

ended the period with no work-in-process. During the period, the firm produced 16,000, 24,000, and 10,000

units of X, Y, and Z, respectively. All costs are considered joint costs. The firm sold 12,000 units of X, 16,000

units of Y, and 9,000 units of Z. X sells for $30 per unit, Y for $44 per unit, and Z for $4 per unit. The firm uses

the net realizable value method for cost allocation. Z is considered a by-product.

Required:

a.

Discuss the following methods to account for by-products:

• other income

• replacement cost

• joint cost proration

b.

Give three examples of by-products.

Joint cost proration is when one of the joint cost allocation methods is used to allocate a portion of joint costs to the by-product.

174. Mandala Inc. obtains two products and a by-product from its production process. By-product revenues are

treated as other income and a noncost approach is used to assign costs to them. During the period, 1,200 units

were processed at a cost of $12,000 for materials and conversion costs, resulting in the following:

Sales Value

Costs after

Final

Product

Units

at Separation

Separation

Value

X

200

$4,000

$2,000

$10,000

Y

400

5,000

6,000

12,000

By-product

150

500

500

1,500

Required:

a.

Account for all costs using a physical basis for allocation.

b.

Account for all costs using net realizable value as the basis for allocation.

c.

Account for all costs using final sales value as the basis for allocation.

d.

How much joint costs should be allocated to the by-product?

a.

Product

Units

Fraction

Allocation

X

200

2/6

$ 4,000

Y

400

4/6

8,000

Product

Allocation

Sep. Costs

Total

X

$ 4,000

$2,000

$ 6,000

Y

8,000

6,000

14,000

$12,000

$20,000

b.

Product

Sales

Sep. Costs

NRV

Fraction

X

$10,000

$2,000

$ 8,000

8/14

Y

12,000

6,000

6,000

6/14

Product

Allocation

Sep. Costs

Total

X

$ 6,857

$2,000

$ 8,857

Y

5,143

6,000

11,143

$12,000

$8,000

$20,000

c.

Product

Sales

Fraction

Allocation

X

$10,000

10/22

$5,455

Y

$12,000

12/22

6,545

Product

Allocation

Sep. Costs

Total

X

$ 5,455

$2,000

$ 7,455

B

6,545

6,000

12,545

$12,000

$20,000

d.

None of the cost of the joint costs should be assigned to the by-product.