3. Assume that you are currently negotiating a lease transaction in the role of the lessee. Discuss whether

you would rather structure the lease as an operating lease or a capital lease and why. In addition,

provide the conditions that would require that the lease be accounted for as a capital lease.

4. Discuss the method of accounting for employee stock options. In your answer discuss the how the

accounting has changed during recent years.

PROBLEM

1. In the chart below, assign the directional effect (I = increase, D = decrease, or NE = no effect) of each

of the following six transactions on the components of the book value of common shareholders’

equity.

a. Issuance of $1 par value common stock at par value.

b.Stock repurchased and placed in the treasury

c. Cash dividend declared.

d. Shareholders identified for dividend distribution on the date of record

e. Property dividend declared and paid.

f. Large stock dividend declared and issued.

Item

Common

Stock

Additional

Paid-In

Capital

Deferred

Compensation

Retained

Earnings

Treasury

Stock at

Cost

Total Common

Shareholders’

Equity

a.

b.

c.

d.

e.

f.

Item

Common

Stock

Additional

Paid-In

Capital

Deferred

Compensation

Retained

Earnings

Treasury

Stock at

Cost

Total Common

Shareholders’

Equity

a.

I

c.

e.

f.

I

6-14

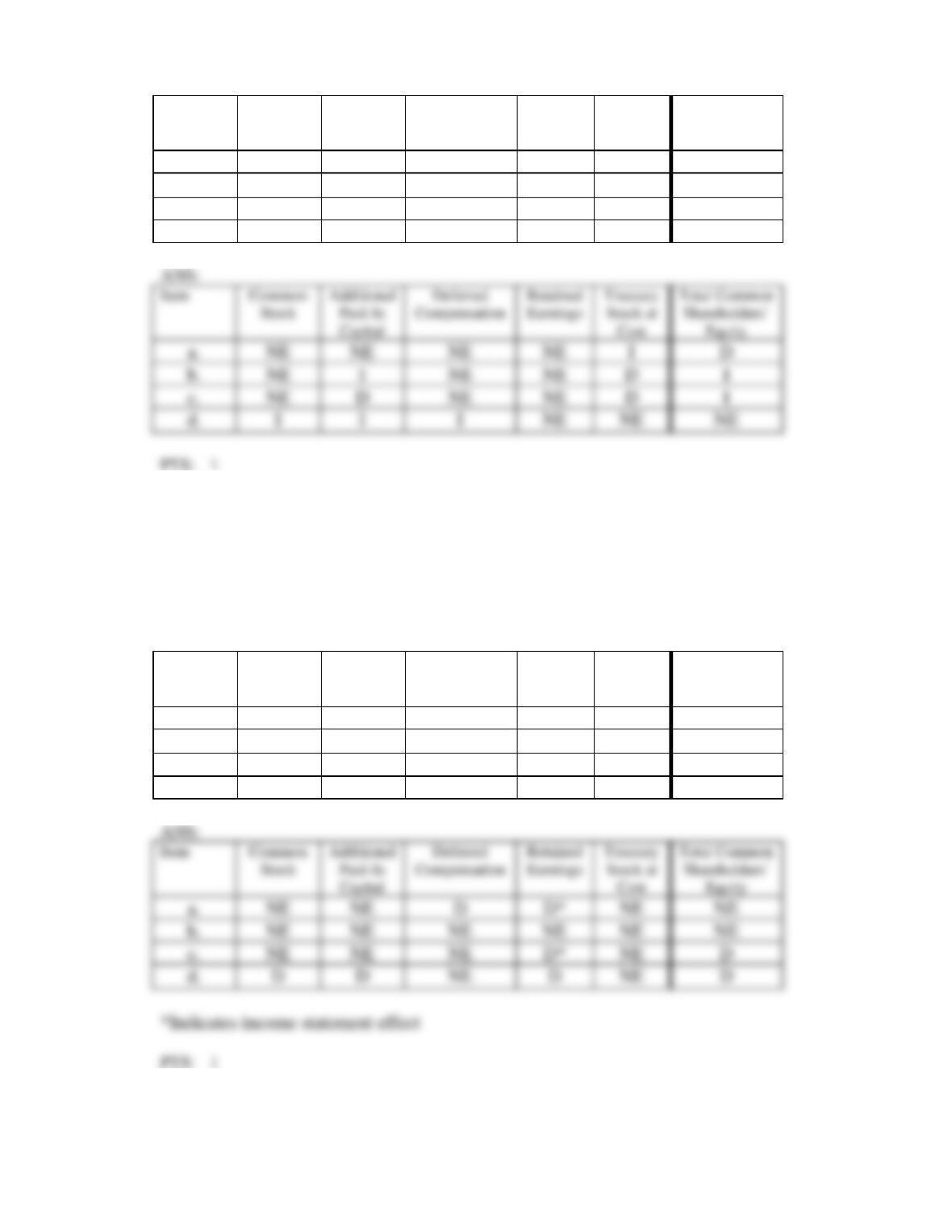

2. In the chart below, assign the directional effect (I = increase, D = decrease, or NE = no effect) of each

of the following six transactions on the components of the book value of common shareholders’

equity.

a. Small stock dividend declared and issued.

b. 2-for-1 stock split announced and issued.

c. Stock options granted.

d. Recognition of compensation expense on stock options.

e. Stock options exercised.

f. Stock options expired.

Item

Common

Stock

Additional

Paid-In

Capital

Deferred

Compensation

Retained

Earnings

Treasury

Stock at

Cost

Total Common

Shareholders’

Equity

a.

b.

c.

d.

e.

f.

a.

I

I

c.

I

e.

I

I

3. In the chart below, assign the directional effect (I = increase, D = decrease, or NE = no effect) of each

of the following four transactions on the components of the book value of common shareholders’

equity.

a. Treasury stock acquired (company uses the cost method).

b. Treasury stock in transaction a. reissued at an amount greater than original acquisition

price.

c. Treasury stock in transaction a. reissued at an amount less than the original acquisition

price.

6-15

d. Restricted stock issued (grant date).

Item

Common

Stock

Additional

Paid-In

Capital

Deferred

Compensation

Retained

Earnings

Treasury

Stock at

Cost

Total Common

Shareholders’

Equity

a.

b.

c.

d.

4. In the chart below, assign the directional effect (I = increase, D = decrease, or NE = no effect) of each

of the following four transactions on the components of the book value of common shareholders’

equity.

a. Recognition of compensation expense related to restricted stock.

b. Granting of stock appreciation rights to be settled with cash.

c. Recognition of compensation expense on stock appreciation rights.

d. Reacquisition and retirement of common stock at an amount greater than original issue price.

Item

Common

Stock

Additional

Paid-In

Capital

Deferred

Compensation

Retained

Earnings

Treasury

Stock at

Cost

Total Common

Shareholders’

Equity

a.

b.

c.

d.

a.

c.

5. Assume that a start-up manufacturing company raises capital through a series of equity issues.

a.

I

c.

I

I

6-16

Required:

a. Using the financial statement template below, summarize the financial statement effects of the

following transactions.

(1) Issues 85,000 shares of $1 par value common stock for $15.00 per share.

(2) Receives land in exchange for 8,500 shares of $1 par common stock when the common stock is

trading in the market at $25 per share. The land has no readily determinable market value.

(3) (a) Receives subscriptions for the issue of 28,000 shares of $1 par value common. The share issue

price is $15 of which 30 percent is received as a down payment.

(3) (b) Subsequently, the remaining 70 percent is received from the transaction in 3(a).

Shareholders’ Equity

Entry

Assets

=

Liabilities

+

CC

+

AOCI

+

RE

1

2

3(a)

3(b)

Journal entry (optional):

b. In each case, how does the company measure the transaction? What measurement

attribute is used?

Shareholders’ Equity

6-17

6. Following is the shareholders’ equity section of Morgan Supplies on a day its common stock is trading

at $77 per share.

Common stock ($2 par value, 30,000 shares issued and outstanding)

$ 60,000

Additional paid-in capital on common stock

1,200,000

Retained earnings

3,000,000

Required:

a. Use the financial statement template below to show the financial statement effects of

the following dividend events. (Assume that the events are independent.)

(1) Cash dividend declaration and payment of $1 per share

(2) Property dividend declaration and payment of shares representing a short-term

investment in Screen Products, Ltd., with a fair value of $15,000

(3) 10 percent stock dividend

(4) 100 percent stock dividend

(5) 3-for-1 stock split

(6) 1-for-2 reverse stock split

Shareholders’ Equity

Entry

Assets

=

Liabilities

+

CC

+

AOCI

+

RE

1

2

3

4

5

6

Journal entry (optional):

b. Which events changed the book value of common equity?

c. Under what conditions will these events lead to future increases and decreases in ROE?

6-19

7. NOTE: This problem requires present value information.

Charter Corp. manufactures office equipment and supplies throughout the U.S. The company owns

property, plant, and equipment and also enters into operating leases for certain facilities. The

company’s tax rate is 35%. Listed below is selected financial data for Charter and the company’s

operating lease disclosure.

2012

2011

2010

Property, Plant, & Equipment (net)

$178,454

$162,369

$155,388

Total Assets

515,685

424,545

410,256

Common Shareholders’ Equity

302,754

298,564

289,455

Sales

$986,258

$888,965

Cost of Goods Sold

693,857

588,920

Depreciation Expense

Interest Expense

84,253

75,689

Net Income

124,581

91,025

Charter Corp.

Operating Lease Disclosure

(amounts in thousands)

Operating Lease Commitments

at the end of 2012

Year

Reported Lease Commitments

2013

$ 25,239

2014

$ 52,800

2015

$ 78,924

2016

$ 48,760

2017

$ 45,678

6-20

Beyond 2017

$212,000

As an analyst you wish to restate Charter’s operating leases into capital leases.

Required:

a.

Using the information in the operating lease disclosure, and assuming that Charter has an

incremental borrowing rate for secured debt of 8%, restate the operating leases into capital

leases.

b.

Estimate the average life of the operating leases.

c.

Calculate Charter’s fixed asset turnover ratio as reported.

d.

Would Charter’s fixed asset turnover ratio increase or decrease, assuming that the

operating leases were capitalized?

8. NOTE: The following problem requires present value information.

Calculate the present value of the operating leases. This is the amount that would be

capitalized.

c.

Calculate Charter’s fixed asset turnover ratio as reported.

d.

Would Charter’s fixed asset turnover ratio increase or decrease assuming that the operating

6-21

On January 1, 2012, Porter Corporation signed a five-year non-cancelable lease for certain machinery.

The terms of the lease called for:

A)

Porter to make annual payments of $60,000 at the end of each year (starting on Dec.

31, 2012) for five years. Porter must return the equipment to the lessor end of this

period.

B)

The machinery has an estimated useful life of 6 years and no expected salvage value.

C)

Porter uses the straight-line method of depreciation for all of its fixed assets.

D)

Porter’s incremental borrowing rate is 8%.

E)

The fair value of the asset at January 1, 2012 is $275,000.

Required:

1.

Discuss whether Porter should account for the lease as an operating or capital lease and

why.

2.

Using the above information determine how the lease would affect Porter’s financial

statements in 2013. Use the balance sheet equation below to show the effects.

C

+

N$A

=

L

+

CC

+

AOCI

+

RE

9. Summarize how the following information about Crank Corp.’s restructuring would affect the balance

sheet and income statement summary chart below. Crank Corp.’s restructuring will take approximately

18 months and was announced on March 15, 2010:

(1)

On March 15, 2010 Crank Corp. announced its restructuring and recognized a

restructuring charge of $845,000.

(2)

The tax effect of the restructuring charge was estimated to be $230,000.

(3)

Crank determined that the cost of disposing and removing facilities and equipment

during 2010 $312,000.

(4)

The tax effect associated with the disposal and removal of facilities and equipment

are $95,000.

(5)

Crank Corp. made cash payments to severed employees and lessors for lease

terminations in 2010 equal to $78,000.

(6)

The tax effect of the severance payments and lease cancellations was $19,000.

Shareholders’ Equity

The lease should be accounted for as a capital lease given that it meets the 75% criteria.

2.

C

NCA

L

+CC

AOCI

RE

239,562

239,562

-47,912

-47,912

Entry

Assets

=

Liabilities

+

CC

+

AOCI

+

RE

1

2

3

4

5

6

1

2