7-1: Cost Allocation and Contingency Fees

A lawyer allocates overhead costs based on his hours working with different clients. The

lawyer expects to have $200,000 in overhead during the year and expects to work on clients’ cases

2,000 hours during the year. In addition he wants to pay himself $50 per hour for working with

clients. The lawyer, however, does not bill all of his clients based on covering overhead costs and

his own salary. Some clients pay her on contingency fees. If the lawyer works with a client on a

contingency fee basis, the lawyer receives half of any settlement for his client. During the year

the lawyer works 1,200 hours that are billable to clients. The remaining hours are worked on a

contingency basis. The lawyer wins $300,000 in settlements for his clients of which he receives

half. Actual overhead was $210,000,

What does the lawyer earn during the year after expenses?

7-2: 7-1: Solution to Cost Allocation and Contingency Fees (10 minutes)

Fixed Costs and Allocated Costs

The maintenance department’s costs are allocated to other departments based on the

number of hours of maintenance use by each department. The maintenance department has fixed

costs of $500,000 and variable costs of $30 per hour of maintenance provided. The variable costs

include the salaries of the maintenance workers. More maintenance workers can be added if

greater maintenance is demanded by the other departments without affecting the fixed costs of the

maintenance department. The maintenance department expects to provide 10,000 hours of

maintenance.

Required:

a. What is the application rate for the maintenance department?

b. What is the additional cost to the maintenance department of providing another hour of

maintenance?

c. What problem exists if the managers of other departments can choose how much

maintenance to be performed?

d. What problem exists if the other departments are allowed to go outside the organization to

buy maintenance services?

7-2: Solution to Fixed Costs and Allocated Costs (15 minutes)

7-3: Choosing Allocation Bases For Levying Taxes

The town of Seaside has decided to construct a new sea aquarium to attract tourist. The

cost of the measure is to be paid by a special tax. Although most of the townspeople believe the

sea aquarium is a good idea, there is disagreement about how the tax should be levied.

Required:

Suggest three different methods of levying the tax and the advantages and disadvantages

of each.

7-3: Solution to Choosing Allocation Bases for Levying Taxes (15 minutes)

7-4: Outsourcing and Overhead

Peluso Company, a manufacturer of snowmobiles, is operating at 70 percent of plant

capacity. Peluso’s plant manager is considering manufacturing headlights, which are now being

purchased for $11 each (a price that is not expected to change in the near future). The Peluso plant

has the equipment and labor force required to manufacture the headlights. The design engineer

estimates that each headlight requires $4 of direct materials and $3 of direct labor. Peluso’s plant

overhead rate is 200 percent of direct labor dollars, and 40 percent of the overhead is fixed cost.

If Peluso Co. manufactures the headlights, how much of a gain (loss) for each headlight will result?

Source: CMA adapted

7–4: Solution to Outsourcing and Overhead (CMA adapted) (10 minutes)

7-5: Incentive Effects of Cost Allocations

Eastern University prides itself on providing faculty and staff a competitive compensation

package. One aspect of this package is a faculty and staff child tuition benefit of $4,000 per child

per year for up to four years to offset the cost of a college education. The faculty or staff member’s

child can attend any college or university, including Eastern University, and receive the tuition

benefit. If a staff member has three children in college one year, the staff member receives a

$12,000 tuition benefit. This money is not taxed to the individual staff or faculty member.

Eastern University pays the benefit directly to the university where the staff/faculty

member’s child is enrolled or if the student is attending Eastern, it reduces the amount of tuition

owed by the faculty/staff member. The university then charges this payment to a benefits account.

This benefits account is then allocated back to the various colleges and departments based on total

salaries in the college or department.

Evaluate the pros and cons of the present university accounting for tuition benefits. What

changes would you recommend making?

7–5: Solution to Incentive Effects of Cost Allocations (20 minutes)

7-6: Allocating Overhead versus Direct Tracing

Nixon & Ross, a law firm, is about to install a new accounting system that will allow the

firm to track more of the overhead costs to individual cases. Overheads are currently allocated to

individual client cases based on billable professional staff salaries. Attorneys working on client

cases charge their time to “billable professional staff salaries.” Attorney time spent in training,

law firm administrative meetings, and the like is charged to an overhead account titled “unbilled

staff salaries.”

The following is a summary of the costs for the current year:

Billable professional staff salaries

$ 4,000,000

Overhead

8,000,000

Total costs

$12,000,000

The overhead costs were as follows:

Secretarial costs

$1,500,000

Staff benefits

2,750,000

Office rent

1,250,000

Telephone and mailing costs

1,500,000

Unbilled staff salaries

1,000,000

Total costs

$8,000,000

Under the new accounting system, the firm will be able to trace secretarial costs, staff

benefits, and telephone and mailing costs to specific clients.

The following are the costs incurred on the Lawson Company case:

Billable professional staff salaries

$150,000

Secretarial costs

25,000

Staff benefits

13,500

Telephone and mailing costs

8,000

Total costs

$196,500

Required:

a. Calculate the current year’s overhead application rate under the old cost accounting system.

b. How would this application rate change if the secretarial costs, staff benefits, and telephone

and mailing costs were reclassified as direct costs instead of overhead, and overhead was

assigned based on direct costs (instead of staff salaries)? Direct costs are defined as billable

staff salaries plus secretarial costs, staff benefits, and telephone and mailing costs.

c. Use the overhead application rates from (a) and (b) to compute the cost of the Lawson case.

d. Nixon & Ross bills clients 150 percent of the total costs of the job. What will be the total

billings to the Lawson Co. if the old overhead application scheme is replaced with the new

overhead scheme?

e. Steve Nixon, managing partner, has commented that replacing the old allocation system

with the direct charge method of the new accounting system will result in more accurate

costing and pricing of cases. Evaluate the new system.

7–6: Solution to Allocating Overhead versus Direct Tracing (40 minutes)

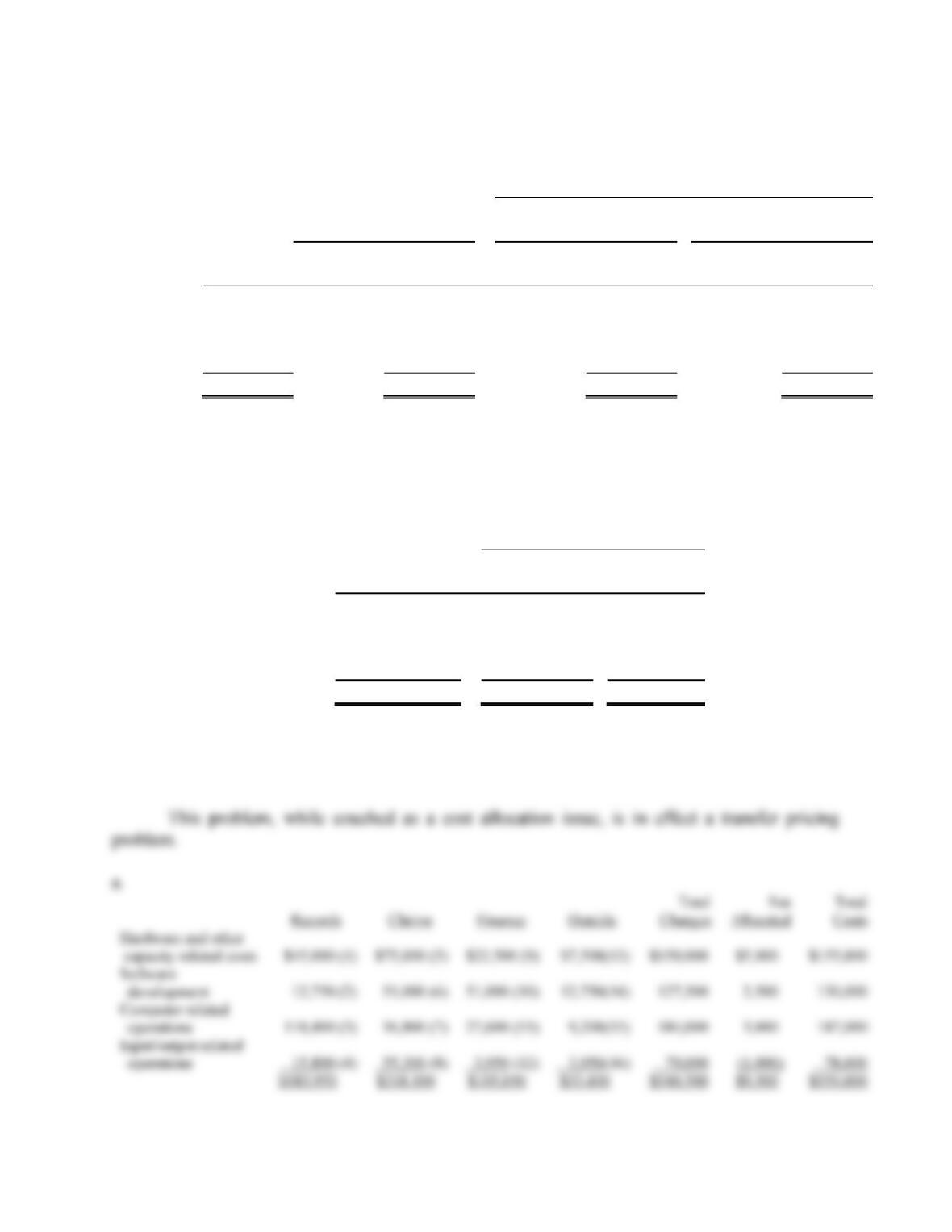

7-7: Allocating Computer Costs

The Independent Underwriters Insurance Co. (IUI) established a systems department two

years ago to implement and operate its information technology system. IUI believed that its own

system would be more cost-effective than the service bureau it had been using.

IUI’s three departments −claims, records, and finance − have different requirements with

respect to hardware and other capacity-related resources and operating resources. The system was

designed to recognize these differing demands. It was also designed to meet IUI’s long-term

capacity. The excess capacity designed into the system is being sold to outside users until IUI

needs it. The estimated resource requirements used to design and implement the system are shown

in the following schedule.

Hardware and

Other Capacity-

Related Resources

Operating

Resources

Records

30%

60%

Claims

50

20

Finance

15

15

Expansion (outside use)

5

5

Total

100%

100%

IUI currently sells the equivalent of its expansion capacity to a few outside clients.

When the system became operational, management decided to redistribute total expenses

of the systems department to the user departments based upon actual computer time used. The

actual costs for the first quarter of the current fiscal year were distributed to the user departments

as follows:

Department

Percentage

Utilization

Amount

Records

60%

$330,000

Claims

20

110,00

Finance

15

82,500

Outside

5

27,500

Total

100%

$550,000

The three user departments have complained about the cost distribution since the systems

department was established. The records department’s monthly costs have been as much as three

times the costs experienced with the service bureau. The finance department is concerned about

the costs distributed to the outside user category, because these allocated costs form the basis for

the fees billed to outside clients.

James Dale, IUI‘s controller, decided to review the distribution method by which the

systems department’s costs have been allocated for the past two years. The additional information

he gathered for his review is reported in Tables 1, 2, and 3. Dale has concluded that the method

of cost distribution should be changed to reflect more directly the actual benefits received by the

departments. He believes that hardware and capacity-related costs should be allocated to the user

departments in proportion to their planned, long-term needs. Any difference between actual and

budgeted hardware costs should remain with the systems department.

The remaining costs for software development and operations would be charged to the user

departments based upon actual hours used. A predetermined hourly rate based upon the annual

budget data would be used. The hourly rates proposed for the current fiscal year are as follows:

Function

Hourly Rate

Software development

$30

Operations

Computer related

$200

Input/output related

$10

Dale plans to use first-quarter activity and cost data to illustrate his recommendations. The

recommendations will be presented to the systems department and the user departments for their

comments and reactions. He then expects to present his recommendations to management for

approval.

Required:

a. Prepare a schedule to show how the actual first-quarter costs of the systems department

will be charged to the users if James Dale’s recommended method is adopted.

b. Explain whether James Dale’s recommended system for charging costs to the user

departments will

(i) Improve cost control in the systems department.

(ii) Improve planning and cost control in the user departments.

(iii) Be a more equitable basis for charging costs to user departments.

Table 1

Systems Department Costs and Activity Levels

First Quarter

Annual Budget

Budget

Actual

Hours

Dollars

Hours

Dollars

Hours

Dollars

Hardware and other

capacity-related costs

−−

$600,000

−−

$150,000

−−

$155,000

Software development

18,750

562,500

4,725

141,750

4,250

130,000

Operations

Computer related

3,750

750,000

945

189,000

920

187,000

Input/output related

30,000

300,000

7,560

75,600

7,900

78,000

$2,212,500

$556,350

$550,000

Table 2

Historical Utilization by Users

Operations

Hardware

and Other

Software

Development

Computer

Input/Output

Capacity

Needs

Range

Average

Range

Average

Range

Average

Records

30%

0-30%

12%

55-65%

60%

10-30%

20%

Claims

50

15-60

35

10-25

20

60-80

70

Finance

15

25-75

45

10-25

15

3-10

6

Outside

5

0-25

8

3-8

5

3-10

4

100%

100%

100%

100%

Table 3

Utilization of Systems Department’s Services for First Quarter

(in Hours)

Operations

Software

Development

Computer

Related

Input/

Output

Records

425

552

1,580

Claims

1,700

184

5,530

Finance

1,700

138

395

Outside

425

46

395

Total

4,250

920

7,900

Source: CMA adapted.

7–7: Solution to Allocating Computer Costs (CMA adapted) (45 minutes)

7–8: Cost Allocations Can Distort Pricing Decisions

Eastman Kodak used to sponsor a car in the NASCAR races. Like other major corporations

that sponsor sports events, Kodak believes that the public’s awareness of its products is enhanced

by sponsoring a NASCAR. For the right to have the car painted yellow with “Kodak” displayed

prominently over the automobile, Eastman Kodak pays the racing team an annual fee in the

millions of dollars.

Kodak is organized around about 25 business units that are profit centers. All Kodak

products are sold by the business units. Senior management at Kodak believes that since the

various business units at Kodak receive the benefits of the NASCAR exposure through greater

name recognition, and hence greater sales, the costs of the program should be allocated back to the

business units and ultimately to all Kodak products. The cost of the NASCAR program is allocated

back to the Kodak business units based on sales revenue. Suppose the allocation is 10 percent of

revenues. That is, for every $1 of revenue, the business unit is allocated $0.10 of cost from the

NASCAR car.

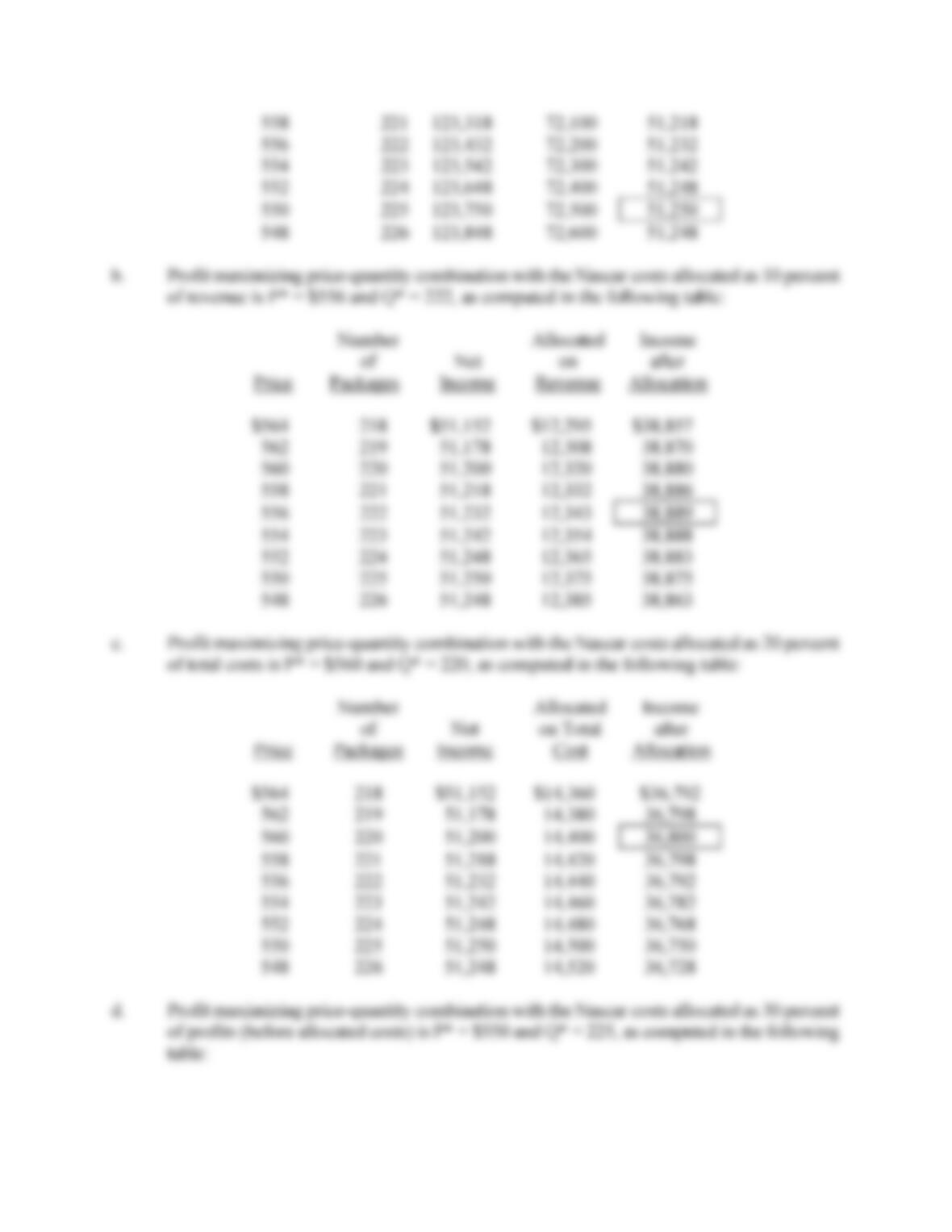

One of Kodak’s business units sells X-ray film in 100-sheet packages. The following table

summarizes possible pricing levels, packages sold at that price, and costs for the various number

of packages.

Price

Number of

Packages Sold

Total Cost

$564

218

$71,800

562

219

71,900

560

220

72,000

558

221

72,100

556

222

72,200

554

223

72,300

552

224

72,400

550

225

72,500

548

226

72,600

Required:

a. What price-quantity combination maximizes the profits of the X-ray film, ignoring the

allocation of NASCAR?

b. If $0.10 of the NASCAR is allocated for every dollar of X-ray revenue, what price-quantity

combination of X-ray film maximizes profits after allocating NASCAR costs?

c. What price-quantity combination of X-ray film maximizes profits after allocating

NASCAR costs using total costs (instead of revenues), where for every dollar of total costs,

$0.20 of NASCAR costs are allocated?

d. Instead of allocating the NASCAR based on revenues, it is allocated based on profits before

allocated costs. For every $1.00 of profits before allocated costs, $0.30 of NASCAR costs

are allocated. Now what price-quantity combination maximizes X-ray profits after

allocating NASCAR costs?

e. Should NASCAR costs be allocated to the business units, and if so, what allocation scheme

should be used (revenues, costs, or profits)?

7–8: Solution to Cost Allocations can Distort Pricing Decisions (45 minutes)