Chapter 6: Accounting for Merchandising Businesses

212.

Using the following data taken from Connor Inc., determine the gross profit to be reported on the income

statement

for the year ended May 31.

Merchandise inventory, June 1

$ 393,250

Merchandise inventory, May 31

380,100

Purchases

1,579,600

Purchases returns and allowances

81,200

Purchases discounts

16,500

Sales

2,060,000

Freight in

59,250

Chapter 6: Accounting for Merchandising Businesses

213.

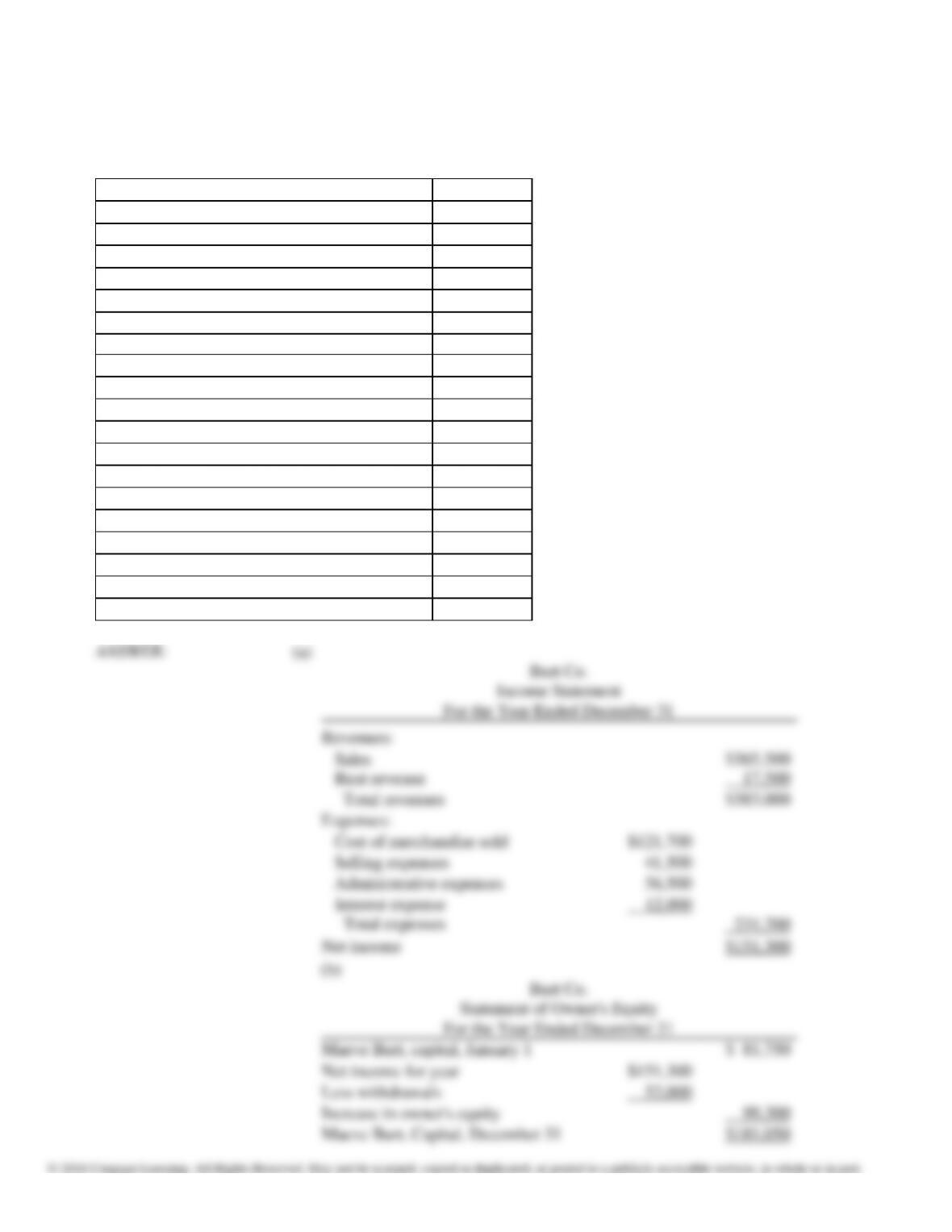

Prepare (a) a single-step income statement, (b) a statement of owner’s equity, and (c) a balance sheet in report

form from the following data for Burt Co., taken from the ledger after adjustments on December 31, the end of the

fiscal year.

Accounts Payable

$ 97,200

Accounts Receivable

64,300

Accumulated Depreciation—Office Equipment

72,750

Accumulated Depreciation—Store Equipment

162,100

Administrative Expenses

56,500

Maeve Burt, Capital

81,750

Cash

53,000

Cost of Merchandise Sold

121,700

Maeve Burt, Drawing

52,000

Interest Expense

12,000

Merchandise Inventory

93,250

Note Payable, Due in two years

154,000

Office Equipment

149,750

Prepaid Insurance

6,500

Rent Revenue

17,500

Salaries Payable

28,700

Sales

365,500

Selling Expenses

41,500

Store Equipment

325,000

Supplies

4,000

Chapter 6: Accounting for Merchandising Businesses

Chapter 6: Accounting for Merchandising Businesses

214.

The following data were extracted from the accounting records of Dana Designs for the year ended March 31.

Merchandise inventory, April 1

$530,000

Merchandise inventory, March 31

375,000

Purchases

270,000

Purchase returns and allowances

25,000

Purchase discounts

10,000

Sales

770,000

Freight in

3,000

Prepare the cost of merchandise sold section of the income statement for the year ended March 31, using the

periodic method.

Chapter 6: Accounting for Merchandising Businesses

215.

Prepare a multiple-step income statement for Armstrong Co. from the following data for the year ended December

31.

Sales, $755,000; cost of merchandise sold, $330,000; administrative expenses, $35,000; interest expense,

$30,000;

rent revenue, $25,000; selling expenses, $50,000.

Chapter 6: Accounting for Merchandising Businesses

216.

Selected data from the ledger of Burt Co., after adjustments, on September 30, the end of the fiscal year, are listed

as follows:

Accounts Receivable

$ 39,120

Office Equipment

$ 82,700

Accumulated Depreciation

60,540

Prepaid Insurance

4,680

Administrative Expenses

90,000

Note Payable

77,750

Bob Burt, Capital

85,000

Salaries Payable

3,060

Cost of Merchandise Sold

550,000

Sales

950,000

Bob Burt, Drawing

65,000

Selling Expenses

102,000

Interest Revenue

10,000

Supplies

3,125

Prepare a single-step income statement and a statement of owner’s equity.

Chapter 6: Accounting for Merchandising Businesses

217.

The following data for the current year ended June 30 are from the accounting records of Zanadu Co.:

Administrative expenses

$ 28,750

Cost of merchandise sold

181,440

Interest expense

3,600

Rent revenue

1,500

Sales

534,440

Selling expenses

65,000

Prepare a multiple-step income statement for the year ended June 30.

218.

Madison Company’s perpetual inventory records indicate that $875,300 of merchandise should be on hand on

October 31. The physical inventory indicates that $781,900 is actually on hand. Journalize the adjusting entry

for

the inventory shrinkage for Madison Company for the year ended October 31.

Chapter 6: Accounting for Merchandising Businesses

219.

Selected accounts and amounts appear below. Journalize the closing entry, assuming a perpetual inventory system.

Merchandise Inventory $ 45,500

Cost of Merchandise Sold 652,500

220.

The records of Penny Co. indicated that $415,000 of merchandise should be on hand on December 31. The

physical inventory indicates that $370,000 of merchandise is actually on hand. Journalize the adjusting entry for

the

inventory shrinkage for the year ended December 31.

Journal

Date

Description

Post.

Ref.

Debit

Credit

Chapter 6: Accounting for Merchandising Businesses

221.

Based upon the following data for a business with a periodic inventory system, determine the cost of

merchandise

sold for August.

Merchandise inventory, August 1

$ 75,560

Merchandise inventory, August 31

96,330

Purchases

373,880

Purchases returns & allowances

14,760

Purchases discounts

10,900

Freight in

4,135

Chapter 6: Accounting for Merchandising Businesses

Match each of the following items (a–h) with the appropriate definition below.

a.

Freight

b.

Delivery Expense

c.

Merchandise Inventory

d.

Sales discount

e.

Purchase Returns and Allowances

f.

Debit memo

g.

Purchase discount

h.

Trade discount

DIFFICULTY: Easy

Bloom’s: Remembering

LEARNING OBJECTIVES: ACCT.WARD.16.06-02 – 06–02

ACCT.WARD.16.06-APP – 06-APP

ACCREDITING STANDARDS: ACCT.ACBSP.APC.04 – Cash vs. Accrual

ACCT.ACBSP.APC.06 – Recording Transactions

ACCT.ACBSP.APC.07 – Adjusting Entries

ACCT.ACBSP.APC.17 – Inventories Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG:

Analytic

222.

Discount taken by the buyer for early payment of invoice.

223.

Account used to record merchandise on hand under a perpetual inventory system.

224.

Early payment discount offered to customers by the seller.

225.

Expense account for recording shipping costs paid by the seller.

226.

Discount to government agencies or customers who purchase large quantities of merchandise.

227.

Account where returned merchandise or price adjustments are recorded by the buyer under the periodic inventory

system.

Chapter 6: Accounting for Merchandising Businesses

228.

The cost associated with delivery of merchandise to the customer.

229.

Informs the seller of the reasons for the return of merchandise or the request for a price allowance.

Match each of the following terms (a–h) with the correct definition below.

a.

Credit terms

b.

FOB destination

c.

FOB shipping point

d.

Periodic inventory system

e.

Perpetual inventory system

f.

Inventory shrinkage

g.

Single-step income statement

h.

Multiple-step income statement

DIFFICULTY: Easy

Bloom’s: Remembering

LEARNING OBJECTIVES: ACCT.WARD.16.06-02 – 06–02

ACCT.WARD.16.06-04 – 06–04

ACCT.WARD.16.06-APP – 06-APP

ACCTWARD.16.06–03 – 06–03

ACCREDITING STANDARDS: ACCT.ACBSP.APC.04 – Cash vs. Accrual

ACCT.ACBSP.APC.09 – Financial Statements

ACCT.ACBSP.APC.17 – Inventories Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

230.

Shipping terms where the ownership of merchandise passes to the buyer when the buyer receives the merchandise.

231.

Losses of inventory due to theft, damage, spoilage, etc. that cause the actual inventory on hand to be less than that

on record.

232.

Statement where net income is determined by deducting all expenses from all revenues.

Chapter 6: Accounting for Merchandising Businesses

233.

Payment arrangements determined by the seller as to when invoices are due and whether early payment discount is

offered.

234.

Inventory system that updates the merchandise inventory account for every purchase and sale transaction.

235.

Inventory system that updates the merchandise inventory account only at the end of the accounting period based

on

a physical count of merchandise on hand.

236.

Statement that includes subtotals for net sales, gross profit, and net operating income in determining net income.

237.

Shipping terms where the ownership of merchandise passes to the buyer when the seller delivers the

merchandise

to the freight carrier.