22) The amount that the price of bond “D” will change if its yield to maturity increases from 8%

to 9% is closest to:

A) -$36

B) -$39

C) $36

D) $9

23) Which of the four bonds is the most sensitive to a one percent increase in the YTM?

A) Bond A

B) Bond B

C) Bond C

D) Bond D

24) Which of the four bonds is the least sensitive to a one percent increase in the YTM?

A) Bond A

B) Bond B

C) Bond C

D) Bond D

25) Consider a corporate bond with a $1000 face value, 8% coupon with semiannual coupon

payments, 7 years until maturity, and a YTM of 9%. It has been 57 days since the last coupon

payment was made and there are 182 days in the current coupon period. The dirty (cash) price

for this bond is closest to:

A) $949.70

B) $961.40

C) $936.40

D) $948.90

26) Consider a corporate bond with a $1000 face value, 10% coupon with semiannual coupon

payments, 5 years until maturity, and currently is selling for (has a cash price of) $1,113.80. The

next coupon payment will be made in 63 days and there are 182 days in the current coupon

period. The clean price for this bond is closest to:

A) $1146.50

B) $1065.70

C) $1113.80

D) $1081.10

27) If its YTM does not change, how does a bond’s cash price change between coupon

payments?

Use the table for the question(s) below.

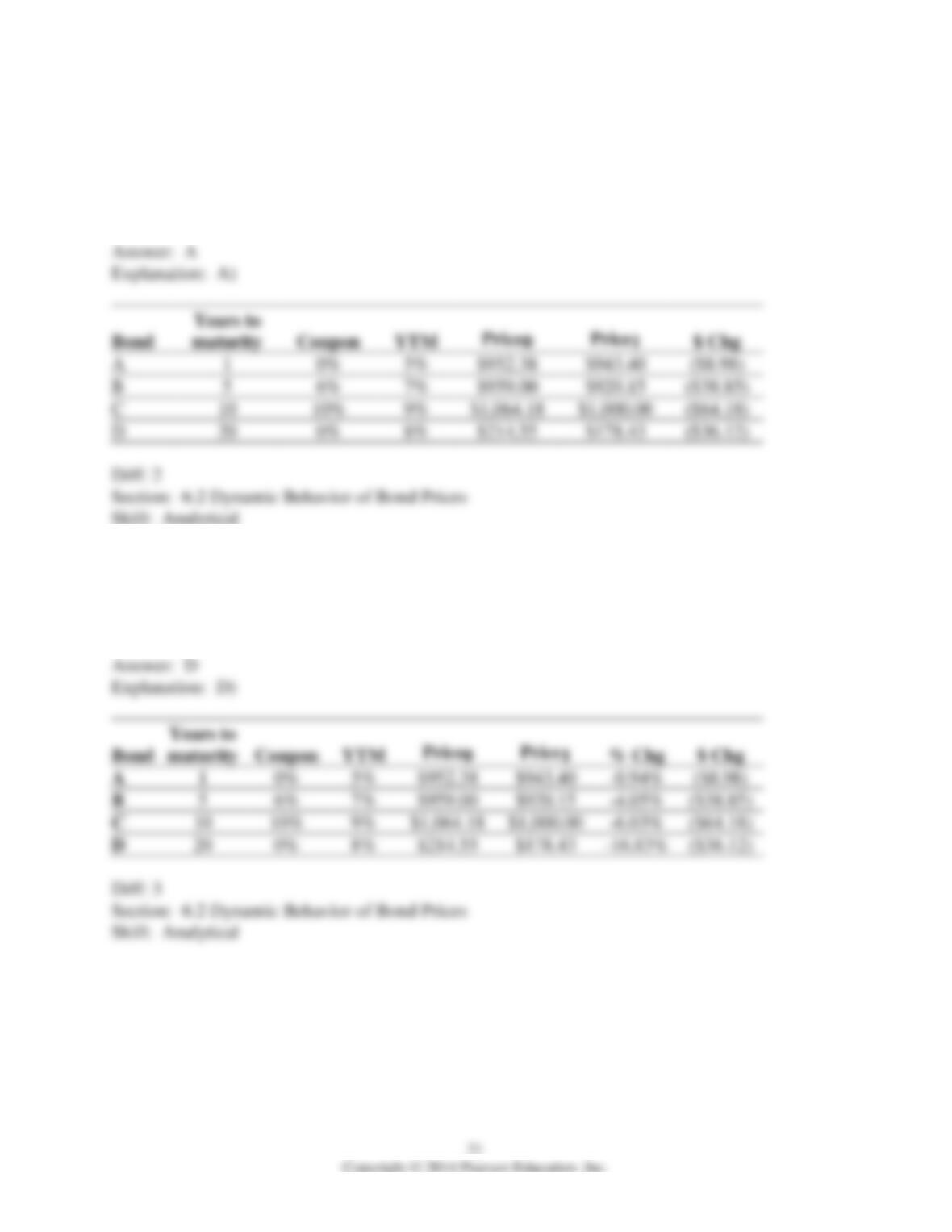

Consider the following four bonds that pay annual coupons:

Bond

Years to

maturity

Coupon

YTM

A

1

0%

5%

B

5

6%

7%

C

10

10%

9%

D

20

0%

8%

28) Assume that the YTM increases by 1% for each of the four bonds listed. Rank the bonds

based upon the sensitivity of their prices from least to most sensitive.

A

B

C

D

6.3 The Yield Curve and Bond Arbitrage

1) Which of the following statements is FALSE?

A) Given the spot interest rates, we can determine the price and yield of any other default-free

bond.

B) As the coupon increases, earlier cash flows become relatively less important than later cash

flows in the calculation of the present value.

C) When the yield curve is flat, all zero-coupon and coupon-paying bonds will have the same

yield, independent of their maturities and coupon rates.

D) When U.S. bond traders refer to “the yield curve,” they are often referring to the coupon–

paying Treasury yield curve.

2) Which of the following statements is FALSE?

A) We can use the law of one price to compute the price of a coupon bond from the prices of

zero-coupon bonds.

B) The plot of the yields of coupon bonds of different maturities is called the coupon-paying

yield curve.

C) It is possible to replicate the cash flows of a coupon bond using zero-coupon bonds.

D) Because the coupon bond provides cash flows at different points in time, the yield to maturity

of a coupon bond is the simple average of the yields of the zero-coupon bonds of equal and

shorter maturities.

3) Which of the following statements is FALSE?

A) By convention, practitioners always plot the yield of the most senior issued bonds, termed the

on-the-run-bonds.

B) We can determine the no-arbitrage price of a coupon bond by discounting its cash flows using

the zero-coupon yields.

C) If the zero coupon yield curve is upward sloping, the resulting yield to maturity decreases

with the coupon rate of the bond.

D) The yield to maturity of a coupon bond is a weighted average of the yields on the zero-

coupon bonds.

4) Which of the following statements is FALSE?

A) The yield to maturity of a coupon bond is a weighted average of the yields on the zero-

coupon bonds.

B) If the zero-coupon yield curve is downward sloping, the yield to maturity will decrease with

the coupon rate.

C) The information in the zero-coupon yield curve is sufficient to price all other risk-free bonds.

D) When the yield curve is flat, all zero-coupon and coupon-paying bonds will have the same

yield, independent of their maturities and coupon rates.

Use the following information to answer the question(s) below.

Maturity (years)

1

2

3

4

5

Zero-Coupon

YTM

3.25%

3.50%

3.90%

4.25%

4.40%

5) The price today of a two-year default-free security with a face value of $1000 and an annual

coupon rate of 5% is closest to:

A) $1002.78

B) $1003.31

C) $1028.50

D) $1028.61

6) The price today of a three-year default-free security with a face value of $1000 and an annual

coupon rate of 4% is closest to:

A) $1002.78

B) $1003.31

C) $1028.50

D) $1028.61

7) A default-free security has an annual coupon rate of 3.25% and sells for par. This bond will

mature in:

A) 1 year

B) 2 years

C) 3 years

D) 4 years

8) Consider a five-year, default-free bond with an annual coupon rate of 5% and a face value of

$1000. The YTM on this bond is closest to:

A) 3.85%

B) 4.20%

C) 4.35%

D) 4.40%

9) Consider a four-year, default-free bond with an annual coupon rate of 4.5% and a face value

of $1000. The YTM on this bond is closest to:

A) 3.85%

B) 4.20%

C) 4.35%

D) 4.40%

Use the table for the question(s) below.

Consider the following zero-coupon yields on default free securities:

Maturity (years)

1

2

3

4

5

Zero-Coupon YTM

5.80%

5.50%

5.20%

5.00%

4.80%

10) The price today of a 3 year default free security with a face value of $1000 and an annual

coupon rate of 6% is closest to:

A) $1000

B) $1021

C) $1013

D) $1005

11) A 3 year default free security with a face value of $1000 and an annual coupon rate of 6%

will trade

A) at a discount.

B) at a premium.

C) at par.

D) There is insufficient information provided to answer this question.

12) The YTM of a 3 year default free security with a face value of $1000 and an annual coupon

rate of 6% is closest to:

A) 5.5%

B) 5.8%

C) 5.7%

D) 5.2%

13) The price of a five-year, zero-coupon, default-free security with a face value of $1000 is

closest to:

A) $754

B) $772

C) $776

D) $791

14) The price today of a 4 year default free security with a face value of $1000 and an annual

coupon rate of 5.25% is closest to:

A) $1000

B) $1003

C) $1008

D) $987

15) A 4 year default free security with a face value of $1000 and an annual coupon rate of 5.25%

will trade

A) at a premium.

B) at par.

C) at a discount.

D) There is insufficient information provided to answer this question.

16) The YTM of a 4 year default free security with a face value of $1000 and an annual coupon

rate of 5.25% is closest to:

A) 5.2%

B) 5.0%

C) 4.9%

D) 5.25%

17) What is the price today of a two-year, default-free security with a face value of $1000 and an

annual coupon rate of 5.75%? Does this bond trade at a discount, premium, or at par?

6.4 Corporate Bonds

1) A corporate bond which receives a BBB rating from Standard and Poor’s is considered

A) a junk bond.

B) an investment grade bond.

C) a defaulted bond.

D) a high-yield bond.

2) Which of the following statements is FALSE?

A) Investors pay less for bonds with credit risk than they would for an otherwise identical

default-free bond.

B) The yield to maturity of a defaultable bond is equal to the expected return of investing in the

bond.

C) The risk of default, which is known as the credit risk of the bond, means that the bond’s cash

flows are not known with certainty.

D) For corporate bonds, the issuer may default—that is, it might not pay back the full amount

promised in the bond certificate.

3) Which of the following statements is FALSE?

A) Because the cash flows promised by the bond are the most that bondholders can hope to

receive, the cash flows that a purchaser of a bond with credit risk expects to receive may be less

than that amount.

B) By consulting bond ratings, investors can assess the credit-worthiness of a particular bond

issue.

C) Because the yield to maturity for a bond is calculated using the promised cash flows, the yield

of bond’s with credit risk will be lower than that of otherwise identical default-free bonds.

D) A higher yield to maturity does not necessarily imply that a bond’s expected return is higher.