4. Barr Inc., manufactures a product that passes through two processes: mixing and packaging. All

manufacturing costs are added uniformly in the mixing department.

Information for the mixing department for June follows:

Work in process, June 1

Units (60% complete)

5,000

Direct materials

$20,000

Direct labor

$24,000

Overhead

$ 4,000

During June, 80,000 units were completed and transferred to packaging.

The following costs were incurred by the mixing department during June:

Direct materials

$180,000

Direct labor

200,000

Overhead

59,200

At June 30, 12,000 units that were 10% complete remained in the mixing department.

Use the weighted average method and round unit costs to two decimal places.

Required:

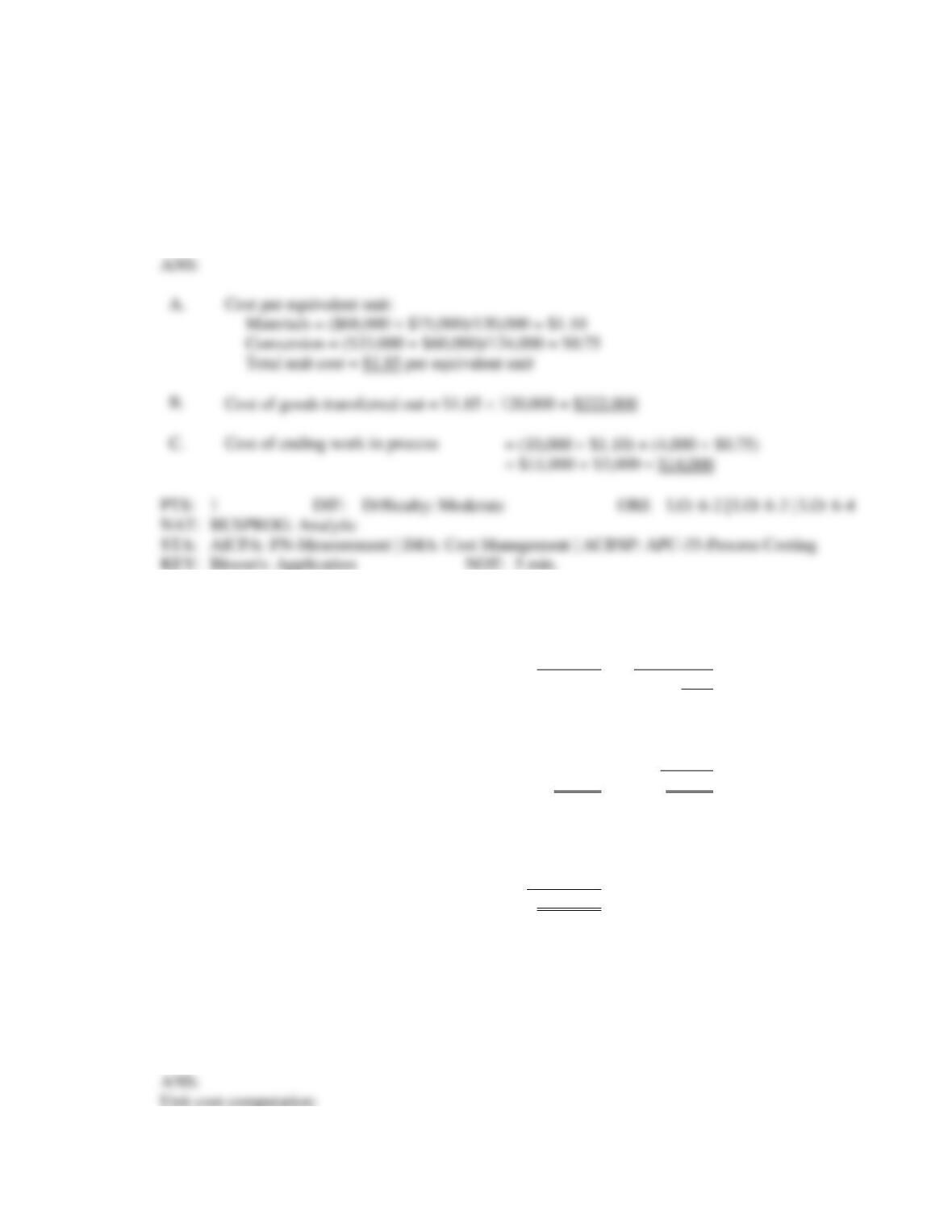

A.

Determine equivalent units of production for June.

B.

Determine June’s total costs to account for.

C.

Determine total cost per equivalent unit of production.

D.

Determine the cost of goods transferred to the packaging department.

E.

Determine the cost of June’s ending work in process for the mixing department.

5. Star Inc., manufactures a product that passes through two processes: mixing and packaging. All

manufacturing costs are added uniformly in the mixing department.

Information for the mixing department for June follows:

Work in process, June 1:

Units (30% complete)

15,000

Direct materials

$ 4,000

Direct labor

$ 3,000

Overhead

$ 2,376

During June, 100,000 units were completed and transferred to packaging.

The following costs were incurred by the mixing department during June:

Direct materials

$50,000

Direct labor

30,000

Overhead

12,000

At June 30, 8,000 units that were 70% complete remained in the mixing department.

Use the weighted average method, and round unit costs to two decimal places.

Required:

A.

Determine equivalent units of production for June.

B.

Determine June’s total costs to account for.

C.

Determine total cost per equivalent unit of production.

D.

Determine the cost of goods transferred to the packaging department.

E.

Determine the cost of June’s ending work in process for the mixing department.

F.

Determine the equivalent units of production for June if ending inventory had been

80% complete.

Figure 6-8.

Department A had the following data for October:

Units in beginning work in process

0

Units Completed

2,000

Units in ending work in process (30% complete)

1,200

Total manufacturing cost

$6,608

6. Refer to Figure 6-8.

A.

Calculate the equivalent units of production in ending work-in-process inventory.

B.

Calculate total equivalent units of production for Department A for October.

Units

7. Refer to Figure 6-8. What is the unit manufacturing cost for Department A for October?

8. Refer to Figure 6-8.

A.

What is the cost of goods transferred out?

B.

What is the cost of ending work-in–process inventory?

$2.80 2,000

9. Harley Company manufactures a product that passes through two processes. The following

information is available for the first department for October.

All materials are added at the beginning of the process.

Beginning work in process consisted of 25,000 units that were 80% complete with respect to

conversion.

Ending work in process consisted of 15,000 units that were 40% complete with respect to conversion.

During the month, 90,000 units were started in process.

Required:

A.

Prepare a physical flow schedule.

B.

Compute equivalent units using the weighted average method.

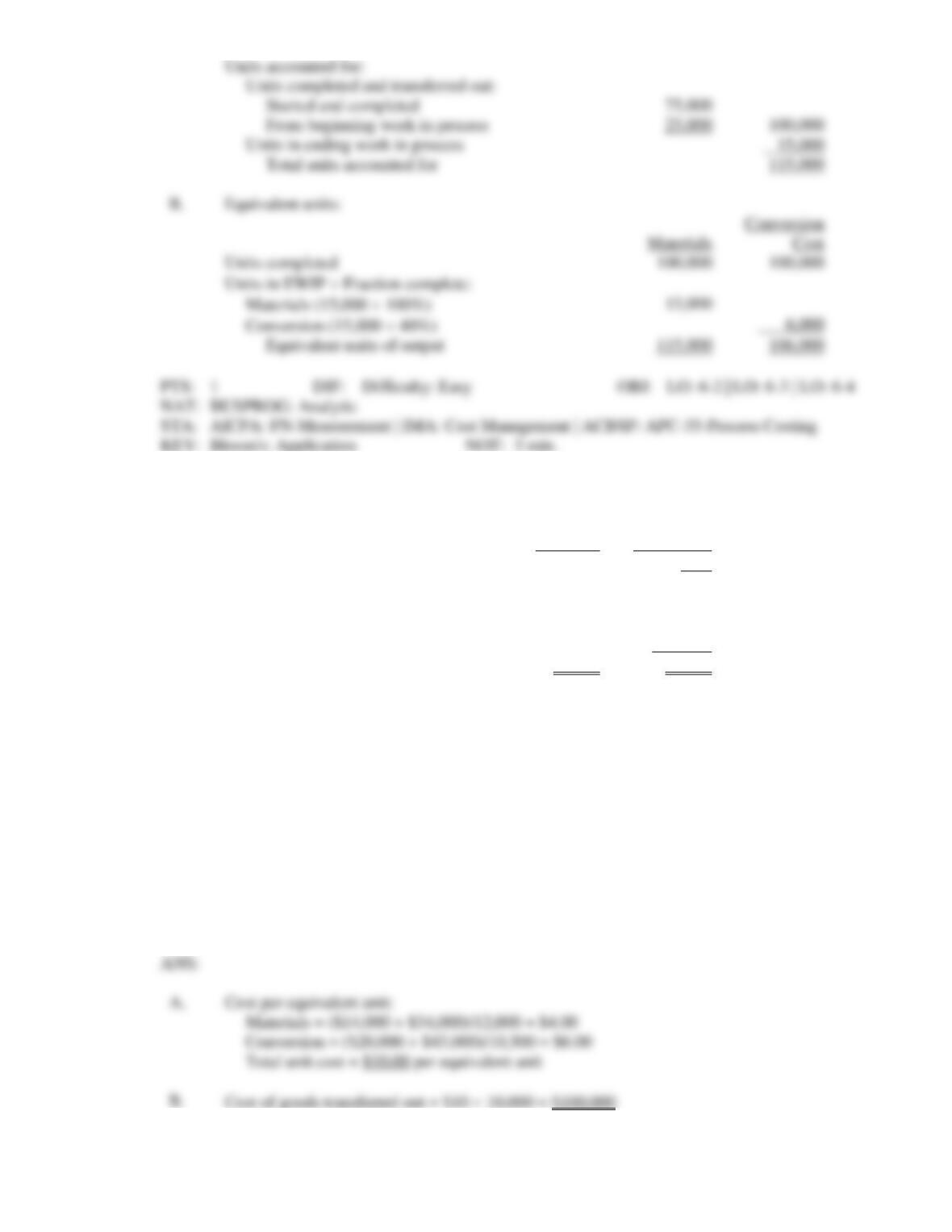

Units accounted for:

Started and completed

75,000

25,000

100,000

Units in ending work in process

Total units accounted for

115,000

Equivalent units:

Conversion

Cost

Units completed

100,000

100,000

Units in EWIP Fraction complete:

Materials (15,000 100%)

Conversion (15,000 40%)

115,000

106,000

10. King Corporation produces a product that passes through two departments. For December, the

following equivalent unit schedule was prepared for the first department:

Materials

Conversion

Cost

Units completed

10,000

10,000

Units in EWIP Fraction complete:

Materials (2,000 100%)

2,000

Conversion (2,000 25%)

500

Equivalent units of output

12,000

10,500

Costs assigned to beginning work in process:

Materials:

$14,000

Conversion:

$20,000

Manufacturing costs incurred during the month:

Materials:

$34,000

Conversion:

$43,000

Required:

A.

Compute the unit cost for December using the weighted average method.

B.

Determine the cost of goods transferred out.

C.

Determine the cost of ending work in process.

Cost per equivalent unit:

Materials = ($14,000 + $34,000)/12,000 = $4.00

Total unit cost = $10.00 per equivalent unit

Cost of goods transferred out = $10 10,000 = $100,000

= $8,000 + $3,000 = $11,000

11. Royal, Inc., manufactures products that pass through two or more processes. The company uses the

weighted average method to compute unit costs. During April, equivalent units were computed as

follows:

Materials

Conversion

Cost

Units completed

90,000

90,000

Units in EWIP Fraction complete:

Materials (4,000 100%)

4,000

Conversion (4,000 30%)

1,200

Equivalent units of output

94,000

91,200

The unit cost was computed as follows:

Materials

$5.00

Conversion cost

3.00

Total cost per unit

$8.00

Required:

A.

Determine the cost of the goods transferred out.

B.

Determine the cost of ending work in process.

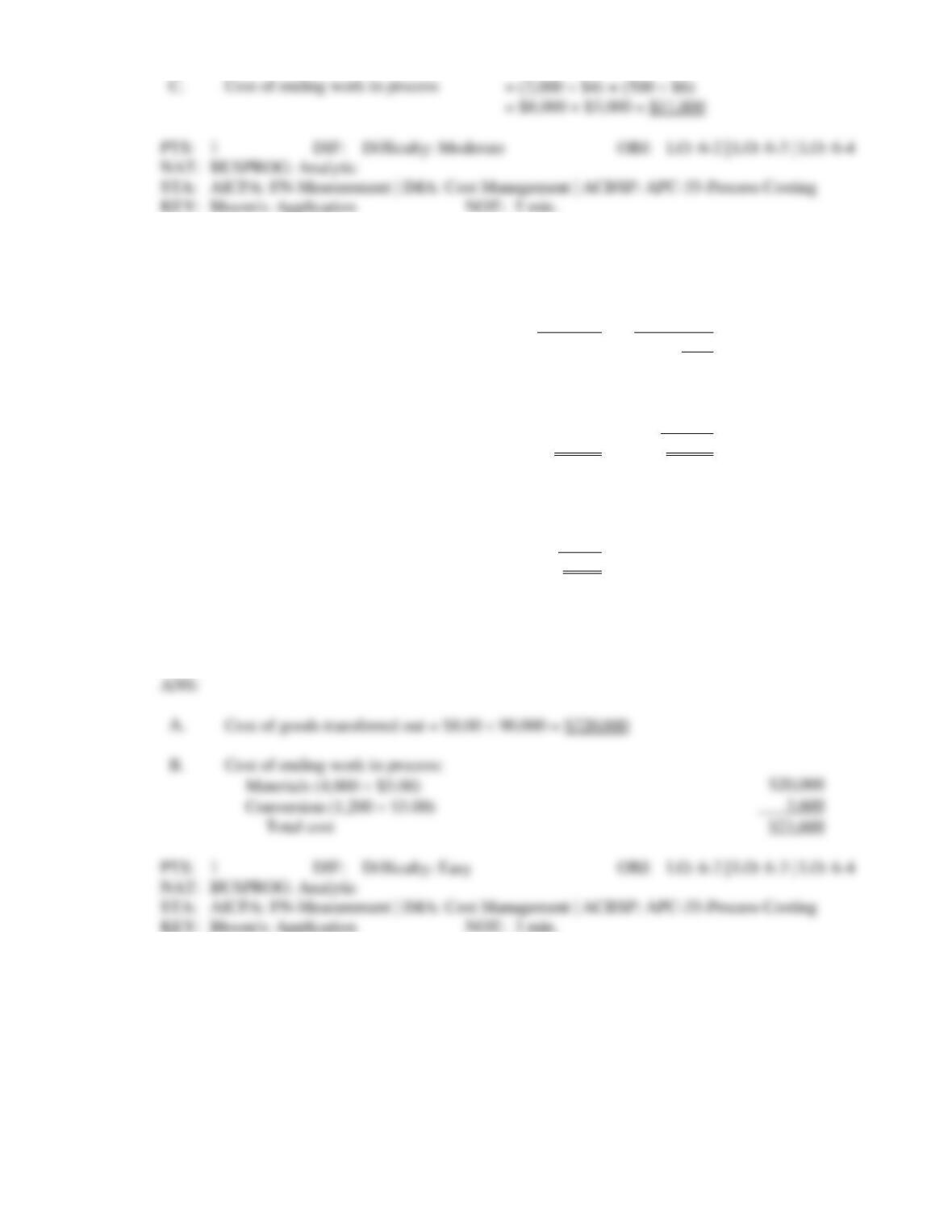

Cost of goods transferred out = $8.00 90,000 = $720,000

Cost of ending work in process:

12. Indigo Inc., manufactures a product that passes through two processes. The following information is

available for the first department for September.

All materials are added at the beginning of the process.

Beginning work in process consisted of 200 units that were 60% complete with respect to conversion.

Ending work in process consisted of 500 units that were 10% complete with respect to conversion.

During the month, 3,000 units were started in process.

Required:

A.

Prepare a physical flow schedule.

B.

Compute equivalent units using the weighted average method.

C.

How would your answer change in part B if the beginning work in process consisted of

200 units that were 80% complete with respect to conversion?

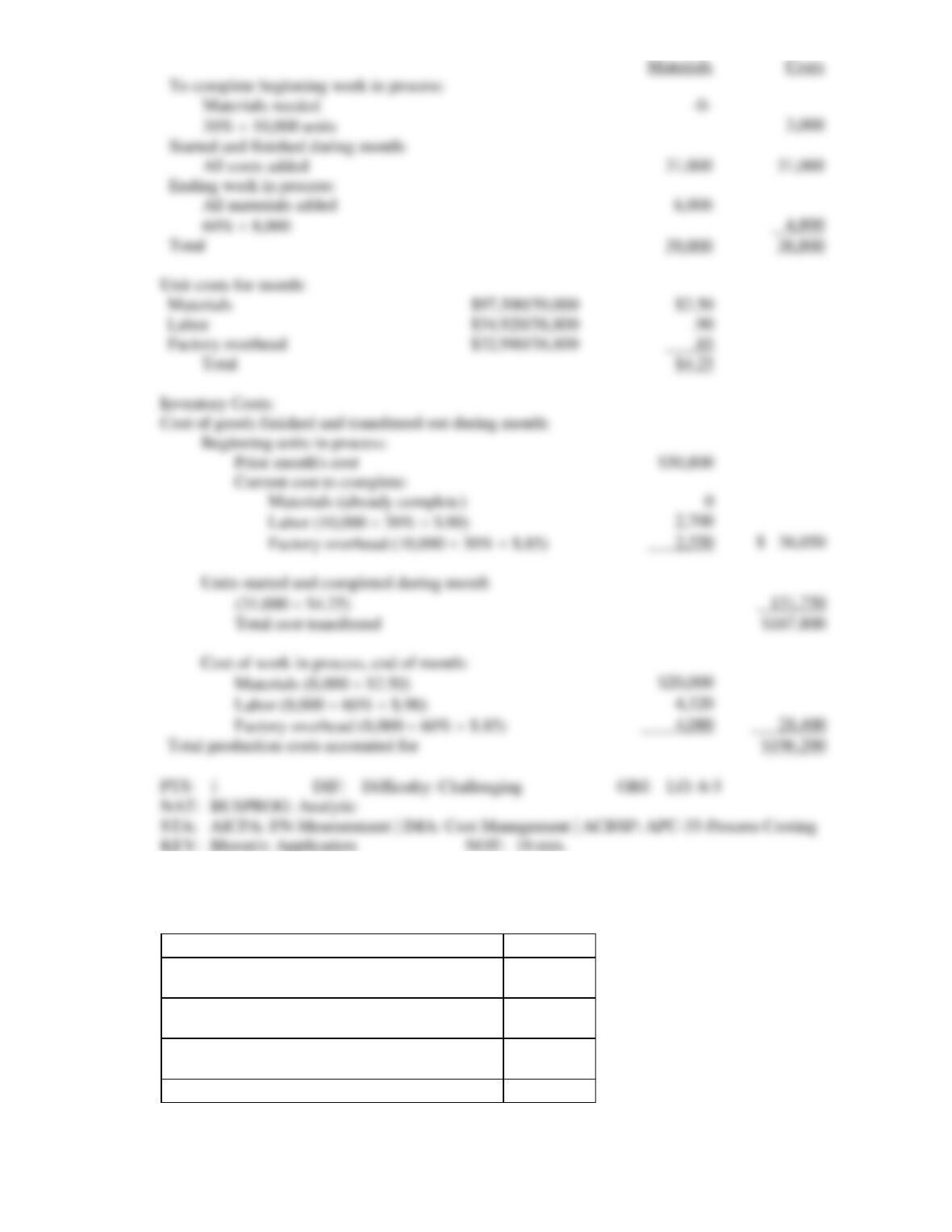

13. Delilah, Incorporated, manufactures quality hair care products. The ingredients are combined in the

mixing department and put in 16-ounce containers in the packaging department.

The following information pertains to the mixing department for the month of May:

Units

(Gallons)

Work in process, May 1

(100% complete materials,

75% labor and overhead)

10,000

Started during May

50,000

Work in process, May 31

(100% complete materials,

50% labor and overhead)

8,000

The costs in work in process at May 1 in the mixing department were as follows:

Mixing

Department

Work in process, May 1:

Materials

$15,000

Direct labor

20,000

Manufacturing overhead

17,600

Total costs

$52,600

The costs added by the mixing department during the month of May were as follows:

Mixing

Department

Materials

$ 90,000

Direct labor

120,000

Manufacturing overhead

100,000

Total costs added

$310,000

Round unit costs to two decimal places.

Required:

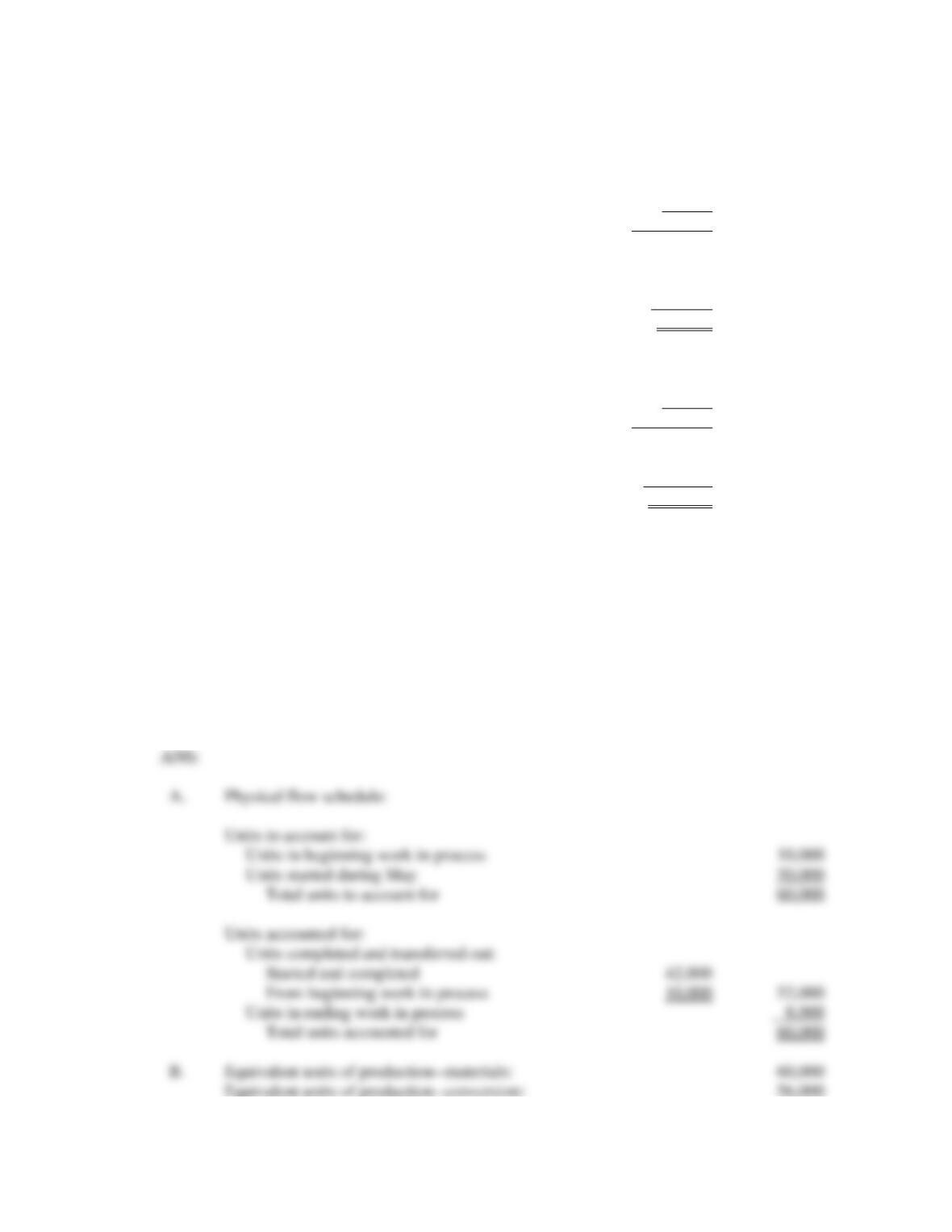

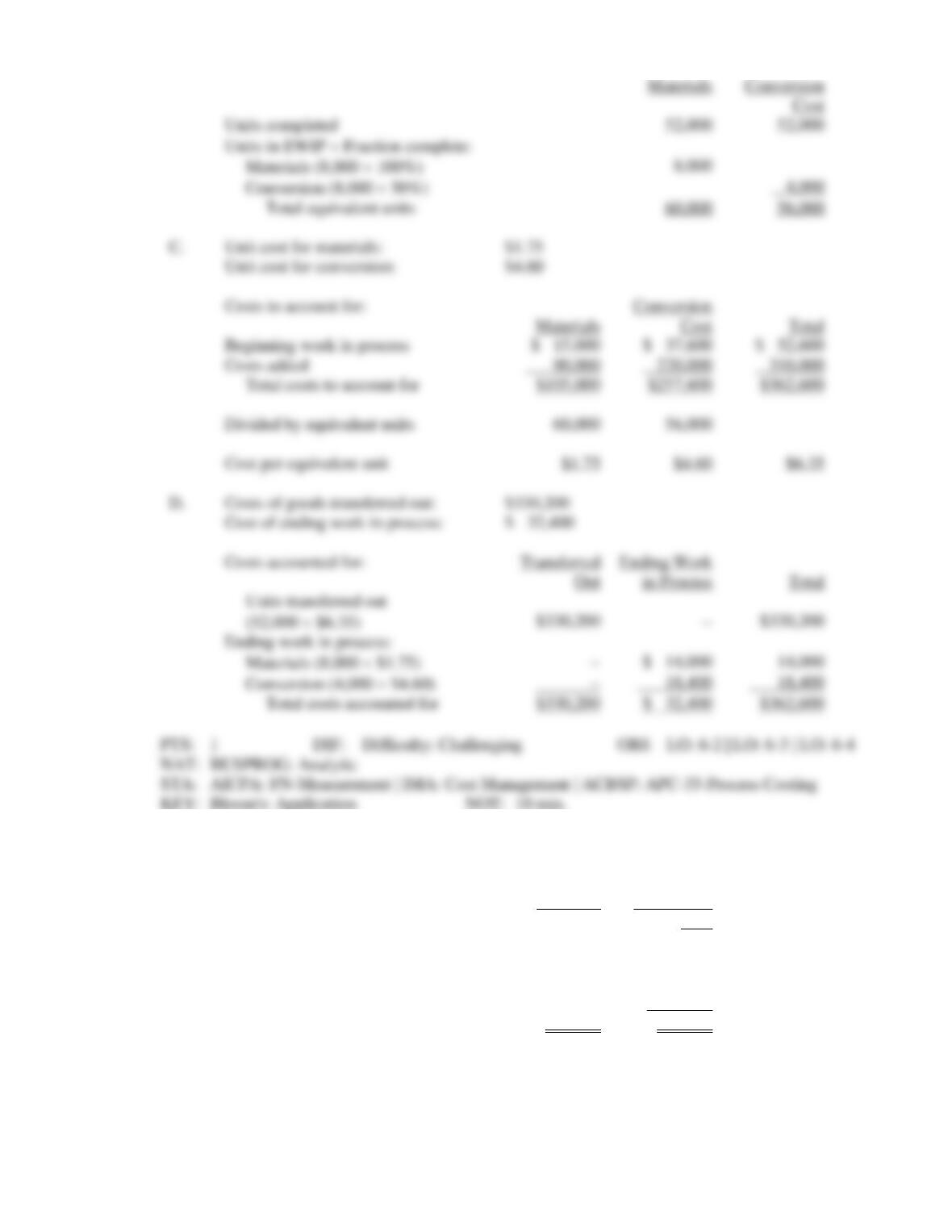

A.

Prepare a physical flow schedule for the mixing department for May.

B.

Using the weighted average method, determine the equivalent units of production for

materials and conversion for the mixing department for May.

C.

Using the weighted average method, determine the cost per equivalent unit of

production for materials and conversion for the mixing department for May.

D.

Using the weighted average method, determine the cost of goods transferred out and

the cost of ending work in process for the mixing department.

Units in EWIP Fraction complete:

Unit cost for conversion:

$4.60

Costs to account for:

Costs added

Divided by equivalent units

Cost per equivalent unit

Costs of goods transferred out:

$330,200

Cost of ending work in process:

$ 32,400

Costs accounted for:

14. AL Corporation produces a product that passes through two departments. For January, the following

equivalent unit schedule was prepared for the first department:

Materials

Conversion

Cost

Units completed

120,000

120,000

Units in EWIP Fraction complete:

Materials (10,000 100%)

10,000

Conversion (10,000 40%)

4,000

Equivalent units of output

130,000

124,000

Costs assigned to beginning work in process:

Materials:

$68,000

Conversion:

$33,000

Manufacturing costs incurred during the month:

Materials:

$75,000

Conversion:

$60,000

Required:

A.

Compute the unit cost for January using the weighted average method.

B.

Determine the cost of goods transferred out.

C.

Determine the cost of ending work in process.

15. Mermain Inc., manufactures products that pass through two processes. The company uses the weighted

average method to compute unit costs. During March, equivalent units were computed as follows:

Materials

Conversion

Cost

Units completed

50,000

50,000

Units in EWIP Fraction complete:

Materials (9,000 100%)

9,000

Conversion (9,000 80%)

7,200

Equivalent units of output

59,000

57,200

Cost was added as follows:

Materials

$ 73,750

Conversion cost

57,200

Total cost

$130,950

Required:

A.

Determine the cost of the goods transferred out.

B.

Determine the cost of ending work in process.

C.

Determine the cost of the goods transferred out if materials in ending work in process

had been 90% complete and conversion in ending work in process had been 70%

complete. Round costs per unit to 2 decimals if necessary.

Cost per equivalent unit:

Cost of goods transferred out = $1.85 120,000 = $222,000

= (10,000 $1.10) + (4,000 $0.75)

= $11,000 + $3,000 = $14,000

16. Davidson Company manufactures a product that passes through two processes. The following

information is available for the first department for October.

All materials are added at the beginning of the process.

Beginning work in process consisted of 20,000 units that were 80% complete with respect to

conversion.

Ending work in process consisted of 15,000 units that were 40% complete with respect to conversion.

During the month, 90,000 units were started in process.

Required:

A.

Prepare a physical flow schedule.

B.

Compute equivalent units using the FIFO method.

Units to account for:

Units started

Units completed and transferred out:

Started and completed

Units in ending work in process

Cost of ending work in process:

Materials equivalent units = 50,000 + (9,000 .9) = 58,100

Conversion equivalent units = 50,000 + (9,000 .7) = 56,300

Conversion cost per unit = $57,200/56,300 = $1.02

Cost of units transferred out = 50,000 ($1.27 + $1.02) = $114,500

17. List the five steps in preparing a production report.

18. Titan Manufacturing uses a process cost system. The following information pertains to operations for

the month of December.

Units

Beginning work-in-process inventory, December 1

7,000

Started in production during December

185,000

Completed production during December

93,500

Ending work-in–process inventory, March 31

98,500

The beginning inventory was 80% complete for materials and 40% complete for conversion costs. The

ending inventory was 85% complete for materials and 30% complete for conversion costs.

Costs pertaining to the month of December are as follows:

Beginning inventory costs are: materials, $38,200; conversion cost $41,400.

Costs incurred during December are: materials used, $462,300; conversion cost $602,700.

Required:

A. Using the weighted average method calculate the total equivalent units of production for direct

materials and conversion cost.

B. Using the weighted average method, calculate the unit cost of materials and conversion for

December.

C. Using the weighted average method, calculate the total cost of the units in the ending work-in–

process inventory at December 31.

19. Plemmon Company adds materials at the beginning of the process in the forming department, which is

the first of two stages of its production cycle. Information concerning the materials used in the forming

department in April follows:

Materials

Units

Costs

Work in process at April 1

15,000

$ 8,000

Units started during April

60,000

$38,500

Units completed and transferred to next department

during April

65,000

Using the FIFO method, what is the materials cost of the work in process at April 30 (round unit

calculations to the nearest cent)?

20. The Roberto Company had computed the flow of units for Department A for the month of May as

follows:

Work in process, May 1:

10,000

Started into production during May

39,000

Units to be accounted for

49,000

Beginning

Added during the

work in process

current month

Materials

$20,800

$ 97,500

Labor

5,200

34,920

Factory overhead

4,800

32,980

Total

$30,800

$165,400

Materials are added at the beginning of the process. There were 8,000 units of work in process at

May 31. The work in process at May 1 was 70% complete as to direct labor and factory overhead costs

and the work in process at May 31 was 60% complete as to direct labor and factory overhead costs.

What was the cost of the goods transferred out and in ending work in process using the FIFO method?

Beginning work in process

Started

Total

Less completed

Ending work in process (complete as to material)

Unit cost (See calculation below)

Materials cost in ending work in process

To complete beginning in process units (materials all 100%)

Units started and finished during month

(60,000 started − 10,000 in ending WIP)

Units in process, April 30 with all materials

Equivalent production for materials

Materials cost:

Total materials cost for period

$38,500/60,000 units = cost per equivalent unit

21. Garrison Inc. manufactures product where all manufacturing inputs are applied uniformly. The

company produced the following physical flow schedule for July:

Units to account for:

Units in BWIP (60% complete)

17,000

Units started

46,000

Total units to account for

63,000

Units accounted for:

Units completed:

From BWIP

17,000

Started and completed

38,000

55,000

Units, EWIP (65% completed)

8,000

Total units accounted for

63,000

Required: Prepare a schedule of equivalent units using the FIFO method.

ESSAY

1. Describe the differences between process costing and job-order costing.

2. Describe how process costing for services differs from process costing for manufactured goods.

Units started and completed

Equivalent units of output

3. Explain the role of the departmental production report in process costing and name the five steps for

completing the departmental production report.

4. Explain how nonuniform inputs and multiple departments affect process costing.

5. Describe the differences in the ways that prior-period costs and output are treated under the weighted

average method and the FIFO method?

6. The controller has asked you do determine what method you think would be the best approach to

dealing with beginning work-in–process; weighted average costing method or FIFO costing method.

Explain the differences between the two methods. Which method would you recommend?