Chapter 6 – Inventories

Ending inventory

Total goods available

Less ending inventory

Cost of goods sold

Total sales

Less COMS

Gross profit

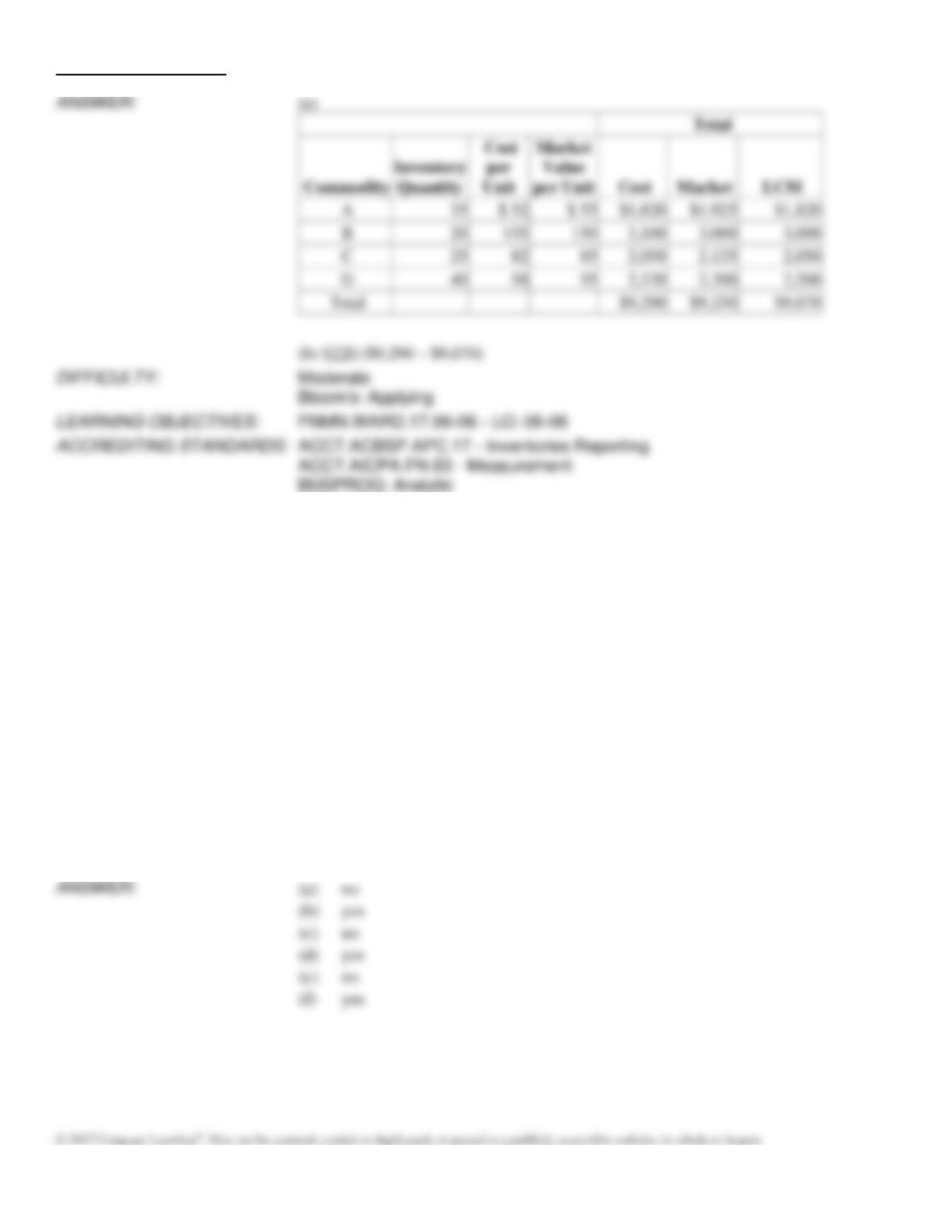

167. Basic inventory data for April 30 are presented below for a business that employs the lower-of-cost-or-market basis

of inventory valuation to each category.

Inventory

Cost per

Market Value

Total

Commodity

Quantity

Unit

per Unit

Cost

Market

LCM

A

35

$ 52

$ 55

_______

_______

_______

B

20

155

150

_______

_______

_______

C

25

82

85

_______

_______

_______

D

40

58

55

_______

_______

_______

(a)

Complete the table.

(b)

Determine the amount of reduction in the inventory at April 30 attributable to market

decline.

Chapter 6 – Inventories

168. Hampton Co. took a physical count of its inventory on December 31. In addition, it had to decide whether or not the

following items should be added to this count.

(a)

Inventory on hand had been sold earlier in the year but had been returned by customers for

various warranty repairs.

(b)

Hampton Co. sent merchandise on a consignment basis on December 31 just prior to the

physical count.

(c)

On December 22, Hampton Co. ordered merchandise on FOB destination terms. The

merchandise was shipped by the supplier on December 30 but had not been received by

December 31.

(d)

On December 27, Hampton Co. ordered merchandise on FOB shipping point terms. The

merchandise was shipped on December 29 but had not been received by December 31.

(e)

Merchandise sold FOB shipping point on December 31 was picked up by the freight

company just before closing on December 31.

(f)

Merchandise shipped to a customer FOB destination was picked up by the freight company

on December 28 but had not arrived at its destination as of December 31.

Answer “yes” or “no” to indicate which items should and should not be added to the December 31 inventory count.

Chapter 6 – Inventories

169. 1. Explain the effect of the following on the financial statements:

Goods held on consignment were included in the ending inventory count.

Goods purchased FOB shipping point were in transit on the last day of the year.

The goods were not counted as part of ending inventory.

Goods sold FOB shipping point were in transit on the last day of the year.

These goods were not counted as part of ending inventory.

2. What happens if inventory errors are not found and corrected?

Chapter 6 – Inventories

170. On the basis of the following data for Sanford Industries as of December 31, determine the value of the inventory at

the lower of cost or market. Also, show how the inventory would appear on the balance sheet (assume that the cost was

determined by the FIFO method). Apply lower of cost or market to each inventory item.

Commodity

Inventory Quantity

Cost per Unit

Market Value per Unit

Size 4

9

$17

$19

Size 5

10

17

14

Size 6

14

20

22

Size 7

12

13

15

Chapter 6 – Inventories

171. Based on the following information: compute (a) inventory turnover; (b) average daily cost of goods sold; and (c)

number of days’ sales in inventory for the current year. Use a 365-day year. (d) If an inventory turnover of 12 is average

for the industry, how is this company doing?

Item

Prior Year

Current Year

Cost of goods sold

$172,900

$215,000

Inventory

18,000

12,000

(a)

$215,000 ÷ [($18,000 + $12,000)/2] =

$215,000 ÷ $15,000 = 14.33 times

(b)

$215,000 ÷ 365 = $589.04

(c)

$15,000 ÷ $589.04 = 24.5 days

(d)

This company is doing worse than the overall industry.

172. The following data were taken from Castle, Inc.

Cost of goods sold

$894,000

Inventory, end of year

78,000

Inventory, beginning of the year

92,000

Determine the inventory turnover ratio and the number of days’ sales in inventory for Castle Inc. Round to two decimal

places.

Chapter 6 – Inventories

173. Based on the following information, compute (a) inventory turnover; (b) average daily cost of goods sold using a 365

day year; and (c) number of days’ sales in inventory.

Cost of goods sold $195,640

Inventory:

Beginning 20,500

Ending 18,628

(c) $19,564 ÷ $536 = 36.5 days

LEARNING OBJECTIVES:

174. During August, the first month of the fiscal year, sales totaled $875,000 and the cost of merchandise available for

sale totaled $850,000. Estimate the cost of the inventory as of August 31, based on an estimated gross profit rate of 45%.

Merchandise available for sale in August

August sales

Less estimated gross profit

Estimated ending inventory

LEARNING OBJECTIVES:

175. On the basis of the following data, estimate the cost of the inventory at March 31 by the retail method.

Cost

Retail

March 1

Inventory

$250,000

$ 350,000

March 1–31

Purchases (net)

850,000

1,650,000

March 1–31

Sales

845,000

Chapter 6 – Inventories

Inventory

176. On the basis of the following data, determine the estimated cost of the inventory as of March 31 by the retail method,

presenting details of the computation in good order.

Cost

Retail

Mar. 1

Inventory

$310,000

$550,000

1–31

Purchases (net)

307,250

515,000

1–31

Sales

400,000

Chapter 6 – Inventories

Match each description to the appropriate document used for inventory control (a–c).

a.

Receiving report

b.

Vendor’s invoice

c.

Purchase order

DIFFICULTY:

Easy

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.06-01 – LO: 06–01

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.17 – Inventories Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

177. last document in the chain, use to compare all three for accuracy

178. authorizes the purchase of inventory from an approved vendor

179. establishes an initial record of the receipt of inventory

Match each description to the appropriate cost flow assumption (a–d).

a.

Weighted average

b.

First-in, first-out (FIFO)

c.

Last-in, first-out (LIFO)

d.

Specific identification

DIFFICULTY:

Easy

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.06-02 – LO: 06–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.17 – Inventories Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

180. The cost of the units sold and in ending inventory is a weighted average of the purchase costs.

181. Cost flow is assumed to be in the reverse order of costs incurred.

182. Cost flow matches the unit sold to the unit purchased.

183. Cost flow is in the order in which the costs were incurred.

Chapter 6 – Inventories

Match each description to the appropriate inventory system (a or b).

a.

Perpetual

b.

Periodic

DIFFICULTY:

Easy

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.06-03 – LO: 06–03

FNMN.WARD.17.06-04 – LO: 06–04

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.17 – Inventories Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

184. This system can be costly and time consuming if not computerized.

185. Average cost is rarely used with this system.

186. Under this system, only revenue is recorded when sales are made.

187. When using this system, a physical inventory is necessary to determine cost of goods sold.

Match each description to the appropriate cost flow assumption (a–c).

a.

FIFO

b.

LIFO

c.

Weighted average

DIFFICULTY:

Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.06-02 – LO: 06–02

FNMN.WARD.17.06-03 – LO: 06–03

FNMN.WARD.17.06-04 – LO: 06–04

FNMN.WARD.17.06-05 – LO: 06–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.17 – Inventories Reporting

ACCT.AICPA.BB.01 – Industry

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

188. Produces the same cost of goods sold under both the periodic and the perpetual inventory systems

189. Rarely used with a perpetual inventory system

190. Produces results that are similar to the specific identification method

Chapter 6 – Inventories

191. Widely used for tax purposes

192. Never results in either the highest or lowest possible net income

193. Produces the highest gross profit when costs are decreasing

194. Produces the highest ending inventory when costs are increasing

195. Assigns the same value to all inventory units

196. Prohibited under International Financial Reporting Standards (IFRS)

197. Does not follow the physical flow of goods in most cases

198. Cost of the latest purchases are assigned to ending inventory

Match each situation to its impact (a–c) on the current year’s net income.

a.

Net income for the current year will be overstated.

b.

Net income for the current year will be understated.

c.

There will be no error effect on net income.

DIFFICULTY:

Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.06-06 – LO: 06–06

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.17 – Inventories Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

199. Purchased merchandise was shipped FOB shipping point on the last day of the year. The cost of the merchandise

was not included in ending inventory.

200. Merchandise was purchased FOB destination on the last day of the year. The cost of the merchandise purchased was

not included in ending inventory.

201. Merchandise held on consignment was included in the count of ending inventory.

202. A consignor included merchandise in the hands of the consignee in ending inventory.

Chapter 6 – Inventories

203. Beginning inventory was understated.

204. Merchandise that was sold and shipped FOB destination on the last day of the year was not included in the seller’s

ending inventory.

205. Merchandise that was sold and shipped FOB shipping point on the last day of the year was not included in the

seller’s ending inventory.

206. The beginning inventory was recorded as $10,000, when actual inventory on hand was $12,000.