CHAPTER 6

COST-VOLUME-PROFIT ANALYSIS: ADDITIONAL ISSUES

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

True-False Statements

1.

1

K

7.

2

K

13.

3

C

19.

4

C

a25.

5

C

2.

1

K

8.

2

AP

14.

3

C

20.

4

K

a26.

5

K

3.

1

K

9.

2

AP

15.

3

K

a21.

5

K

a27.

5

K

4.

1

K

10.

2

K

16.

4

K

a22.

5

K

a28.

5

K

5.

2

K

11.

2

K

17.

4

K

a23.

5

K

a29.

5

K

6.

2

K

12.

3

K

18.

4

K

a24.

5

AP

a30.

5

K

Multiple Choice Questions

31.

1

K

50.

1

AP

69.

2

AP

88.

4

C

a107.

5

AP

32.

1

K

51.

1

K

70.

2

AP

89.

4

K

a108.

5

K

33.

1

K

52.

1

AP

71.

2

C

90.

4

K

a109.

5

K

34.

1

AP

53.

1

AP

72.

2

C

91.

4

K

a110.

5

C

35.

1

AP

54.

1

AP

73.

2

AP

92.

4

K

a111.

5

K

36.

1

AP

55.

1

K

74.

2

AP

a93.

5

K

a112.

5

K

37.

1

AP

56.

1

K

75.

2

AP

a94.

5

K

a113.

5

K

38.

1

K

57.

1

AP

76.

3

C

a95.

5

K

a114.

5

AP

39.

1

K

58.

1

AP

77.

3

C

a96.

5

K

a115.

5

AP

40.

1

AP

59.

1

AP

78.

3

K

a97.

5

K

a116.

5

AP

41.

1

AP

60.

2

K

79.

3

AP

a98.

5

K

a117.

5

AP

42.

1

AP

61.

2

C

80.

3

AP

a99.

5

K

a118.

5

C

43.

1

K

62.

2

AP

81.

4

K

a100.

5

K

a119.

5

C

44.

1

AP

63.

2

AP

82.

4

C

a101.

5

K

a120.

5

C

45.

1

AP

64.

2

AP

83.

4

C

a102.

5

K

a121.

5

K

46.

1

AP

65.

2

AP

84.

4

K

a103.

5

AP

a122.

5

K

47.

1

AP

66.

2

AP

85.

4

AP

a104.

5

AP

a123.

5

C

48.

1

AP

67.

2

AP

86.

4

AP

a105.

5

AP

a124.

5

K

49.

1

AP

68.

2

AP

87.

4

C

a106.

5

AP

a125.

5

K

Brief Exercises

126.

2

AP

128.

3

AP

130.

4

AP

a132.

5

AP

a134.

5

AP

127.

2

AP

129.

3

AP

131.

4

AP

a133.

5

AP

a135.

5

AP

Exercises

136.

1, 4

AP

140.

2

AP

144.

4

AN

a148.

5

AP

a152.

5

AP

137.

2

AP

141.

3

AN

145.

4

AP

a149.

5

AP

a153.

5

AP

138.

2

AP

142.

3

AN

146.

4

AP

a150.

5

AP

139.

2

AP

143.

3

AN

a147.

5

K

a151.

5

AP

Completion Statements

154.

1

K

157.

2

K

160.

4

K

a163.

5

K

155.

1

K

158.

3

K

a161.

5

K

a164.

5

K

156.

2

K

159.

4

K

a162.

5

K

a165.

5

K

aThis topic is dealt with in an Appendix to the chapter.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 2

SUMMARY OF LEARNING OBJECTIVES BY QUESTION TYPE

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Learning Objective 1

1.

TF

33.

MC

39.

MC

45.

MC

51.

MC

57.

MC

2.

TF

34.

MC

40.

MC

46.

MC

52.

MC

58.

MC

3.

TF

35.

MC

41.

MC

47.

MC

53.

MC

59.

MC

4.

TF

36.

MC

42.

MC

48.

MC

54.

MC

136.

Ex

31.

MC

37.

MC

43.

MC

49.

MC

55.

MC

154.

C

32.

MC

38.

MC

44.

MC

50.

MC

56.

MC

155.

C

Learning Objective 2

5.

TF

10.

TF

63.

MC

68.

MC

73.

MC

137.

Ex

157.

C

6.

TF

11.

TF

64.

MC

69.

MC

74.

MC

138.

Ex

7.

TF

60.

MC

65.

MC

70.

MC

75.

MC

139.

Ex

8.

TF

61.

MC

66.

MC

71.

MC

126.

BE

140.

Ex

9.

TF

62.

MC

67.

MC

72.

MC

127.

BE

156.

C

Learning Objective 3

12.

TF

15.

TF

78.

MC

128.

BE

142.

Ex

13.

TF

76.

MC

79.

MC

129.

BE

143.

Ex

14.

TF

77.

MC

80.

MC

141.

Ex

158.

C

Learning Objective 4

16.

TF

20.

TF

84.

MC

88.

MC

92.

MC

144.

Ex

160.

C

17.

TF

81.

MC

85.

MC

89.

MC

130.

BE

145.

Ex

18.

TF

82.

MC

86.

MC

90.

MC

131.

BE

a146.

Ex

19.

TF

83.

MC

87.

MC

91.

MC

136.

Ex

159.

C

Learning Objective 5a

21.

TF

30.

TF

101.

MC

110.

MC

119.

MC

134.

BE

161.

C

22.

TF

93.

MC

102.

MC

111.

MC

120.

MC

135.

BE

162.

C

23.

TF

94.

MC

103.

MC

112.

MC

121.

MC

147.

Ex

163.

C

24.

TF

95.

MC

104.

MC

113.

MC

122.

MC

148.

Ex

164.

C

25.

TF

96.

MC

105.

MC

114.

MC

123.

MC

149.

Ex

165.

C

26.

TF

97.

MC

106.

MC

115.

MC

124.

MC

150.

Ex

27.

TF

98.

MC

107.

MC

116.

MC

125.

MC

151.

Ex

28.

TF

99.

MC

108.

MC

117.

MC

132.

BE

152.

Ex

29.

TF

100.

MC

109.

MC

118.

MC

133.

BE

153.

Ex

Note: TF = True-False C = Completion Ex = Exercise

MC = Multiple Choice BE = Brief Exercise

The chapter also contains four Short-Answer Essay questions.

Cost-Volume-Profit Analysis: Additional Issues

6 – 3

CHAPTER LEARNING OBJECTIVES

1. Apply basic CVP concepts. The CVP income statement classifies costs and expenses as

variable or fixed and reports contribution margin in the body of the statement. Contribution

margin is the amount of revenue remaining after deducting variable costs. It can be

2. Explain the term sales mix and its effects on break-even sales. Sales mix is the relative

3 Determine sales mix when a company has limited resources. When a company has

limited resources, it is necessary to find the contribution margin per unit of limited resource.

This amount is then multiplied by the units of limited resource to determine which product

maximizes net income.

4. Indicate how operating leverage affects profitability. Operating leverage refers to the

degree to which a company’s net income reacts to a change in sales. Operating leverage is

a5. Explain the difference between absorption costing and variable costing. Under

absorption costing, fixed manufacturing costs are product costs. Under variable costing, fixed

manufacturing costs are period costs. If production volume exceeds sales volume, net

income under absorption costing will exceed net income under variable costing by the

amount of fixed manufacturing costs included in ending inventory that results from units

produced but not sold during the period. If production volume is less than sales volume, net

Test Bank for Managerial Accounting, Seventh Edition

6 – 4

TRUE-FALSE STATEMENTS

1. The CVP income statement classifies costs as variable or fixed and computes a

contribution margin.

2. In CVP analysis, cost includes manufacturing costs but not selling and administrative

expenses.

3. When a company is in its early stages of operation, its primary goal is to generate a target

net income.

4. The margin of safety tells a company how far sales can drop before it will be operating at

a loss.

5. Sales mix is a measure of the percentage increase in sales from period to period.

6. Sales mix is not important to managers when different products have substantially

different contribution margins.

7. The weighted-average contribution margin of all the products is computed when

determining the break-even sales for a multi-product firm.

8. If Buttercup, Inc. sells two products with a sales mix of 75% : 25%, and the respective

contribution margins are $80 and $240, then weighted-average unit contribution margin is

$120.

9. If fixed costs are $100,000 and weighted-average unit contribution margin is $50, then the

break-even point in units is 2,000 units.

10. Net income can be increased or decreased by changing the sales mix.

11. The break-even point in dollars is variable costs divided by the weighted-average

contribution margin ratio.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 5

12. When a company has limited resources, management must decide which products to

make and sell in order to maximize net income.

13. When a company has limited resources to manufacture products, it should manufacture

those products which have the highest unit contribution margin.

14. If a company has limited machine hours available for production, it is generally more

profitable to produce and sell the product with the highest contribution margin per machine

hour.

15. According to the theory of constraints, a company must identify its constraints and find

ways to reduce or eliminate them.

16. Cost structure refers to the relative proportion of fixed versus variable costs that a

company incurs.

17. Operating leverage refers to the extent to which a company’s net income reacts to a given

change in fixed costs.

18. The degree of operating leverage provides a measure of a company’s earnings volatility.

19. If Sprinkle Industries has a margin of safety ratio of .60, it could sustain a 60 percent

decline in sales before it would be operating at a loss.

20. A company with low operating leverage will experience a sharp increase in net income

with a given increase in sales.

a21. Variable costing is the approach used for external reporting under generally accepted

accounting principles.

a22. The difference between absorption costing and variable costing is the treatment of fixed

manufacturing overhead.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 6

a23. Selling and administrative costs are period costs under both absorption and variable

costing.

a24. Manufacturing cost per unit will be higher under variable costing than under absorption

costing.

a25. Some fixed manufacturing costs of the current period are deferred to future periods

through ending inventory under variable costing.

a26. When units produced exceed units sold, income under absorption costing is higher than

income under variable costing.

a27. When units sold exceed units produced, income under absorption costing is higher than

income under variable costing.

a28. When absorption costing is used for external reporting, variable costing can still be used

for internal reporting purposes.

a29. When absorption costing is used, management may be tempted to overproduce in a given

period in order to increase net income.

a30. The use of absorption costing facilitates cost-volume-profit analysis.

Answers to True-False Statements

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 7

MULTIPLE CHOICE QUESTIONS

31. Cost-volume-profit analysis is the study of the effects of

a. changes in costs and volume on a company’s profit.

b. cost, volume, and profit on the cash budget.

c. cost, volume, and profit on various ratios.

d. changes in costs and volume on a company’s profitability ratios.

32. The CVP income statement classifies costs

a. as variable or fixed and computes contribution margin.

b. by function and computes a contribution margin.

c. as variable or fixed and computes gross margin.

d. by function and computes a gross margin.

33. Contribution margin is the amount of revenue remaining after deducting

a. cost of goods sold.

b. fixed costs.

c. variable costs.

d. contra-revenue.

34. Moonwalker’s CVP income statement included sales of 5,000 units, a selling price of

$100, variable expenses of $60 per unit, and fixed expenses of $110,000. Contribution

margin is

a. $500,000.

b. $300,000.

c. $200,000.

d. $90,000.

35. Moonwalker’s CVP income statement included sales of 5,000 units, a selling price of

$100, variable expenses of $60 per unit, and fixed expenses of $110,000. Net income is

a. $500,000.

b. $200,000.

c. $190,000.

d. $90,000.

36. For Buffalo Co., at a sales level of 4,000 units, sales is $75,000, variable expenses total

$50,000, and fixed expenses are $21,000. What is the contribution margin per unit?

a. $5.25

b. $6.25

c. $12.50

d. $18.75

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 8

37. If contribution margin is $140,000, sales is $300,000, and net income is $40,000, then

variable and fixed expenses are

Variable Fixed

a. $160,000 $260,000

b. $160,000 $100,000

c. $100,000 $160,000

d. $440,000 $260,000

38. In a CVP income statement, cost of goods sold is generally

a. completely a variable cost.

b. completely a fixed cost.

c. neither a variable cost nor a fixed cost.

d. partly a variable cost and partly a fixed cost.

39. In a CVP income statement, a selling expense is generally

a. completely a variable cost.

b. completely a fixed cost.

c. neither a variable cost nor a fixed cost.

d. partly a variable cost and partly a fixed cost.

40. Hinge Manufacturing’s cost of goods sold is $420,000 variable and $240,000 fixed. The

company’s selling and administrative expenses are $300,000 variable and $360,000 fixed.

If the company’s sales is $1,580,000, what is its contribution margin?

a. $260,000

b. $860,000

c. $920,000

d. $980,000

41. Hinge Manufacturing’s cost of goods sold is $420,000 variable and $240,000 fixed. The

company’s selling and administrative expenses are $300,000 variable and $360,000 fixed.

If the company’s sales is $1,580,000, what is its net income?

a. $260,000

b. $860,000

c. $920,000

d. $980,000

42. Woolford’s CVP income statement included sales of 5,000 units, a selling price of $50,

variable expenses of $30 per unit, and net income of $25,000. Fixed expenses are

a. $75,000.

b. $100,000.

c. $150,000.

d. $250,000.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 9

43. The contribution margin ratio is

a. sales divided by contribution margin.

b. sales divided by fixed expenses.

c. sales divided by variable expenses.

d. contribution margin divided by sales.

44. For Pierce Company, sales is $500,000, variable expenses are $340,000, and fixed

expenses are $140,000. Pierce’s contribution margin ratio is

a. 4%.

b. 28%.

c. 32%.

d. 68%.

45. For Sanborn Co., sales is $1,000,000, fixed expenses are $300,000, and the contribution

margin per unit is $60. What is the break-even point?

a. $1,666,667 sales dollars

b. $500,000 sales dollars

c. 16,667 units

d. 5,000 units

46. For Franklin, Inc., sales is $2,000,000, fixed expenses are $600,000, and the contribution

margin ratio is 36%. What is net income?

a. $120,000

b. $216,000

c. $504,000

d. $720,000

47. For Franklin, Inc., sales is $2,000,000, fixed expenses are $600,000, and the contribution

margin ratio is 36%. What are the total variable expenses?

a. $384,000

b. $720,000

c. $1,280,000

d. $2,000,000

48. In 2016, Teller Company sold 3,000 units at $600 each. Variable expenses were $420 per

unit, and fixed expenses were $240,000. What was Teller’s 2016 net income?

a. $300,000

b. $540,000

c. $1,260,000

d. $1,800,000

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 10

49. In 2016, Teller Company sold 3,000 units at $600 each. Variable expenses were $420 per

unit, and fixed expenses were $270,000. The same selling price, variable expenses, and

fixed expenses are expected for 2017. What is Teller’s break-even point in sales dollars

for 2017?

a. $900,000

b. $2,700,000

c. $1,800,000

d. $2,571,429

50. In 2016, Teller Company sold 3,000 units at $600 each. Variable expenses were $420 per

unit, and fixed expenses were $270,000. The same selling price, variable expenses, and

fixed expenses are expected for 2017. What is Teller’s break-even point in units for 2017?

a. 1,500

b. 643

c. 450

d. 750

51. The required sales in units to achieve a target net income is

a. (sales + target net income) divided by contribution margin per unit.

b. (sales + target net income) divided by contribution margin ratio.

c. (fixed cost + target net income) divided by contribution margin per unit.

d. (fixed cost + target net income) divided by contribution margin ratio.

52. For Wickham Co., sales is $3,000,000, fixed expenses are $900,000, and the contribution

margin ratio is 36%. What is required sales in dollars to earn a target net income of

$600,000?

a. $1,666,667

b. $2,500,000

c. $4,166,667

d. $8,333,333

53. Warner Manufacturing reported sales of $2,000,000 last year (100,000 units at $20 each),

when the break-even point was 80,000 units. Warner’s margin of safety ratio is

a. 20%.

b. 25%.

c. 80%.

d. 120%.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 11

54. For Wilder Corporation, sales is $1,600,000 (8,000 units), fixed expenses are $480,000,

and the contribution margin per unit is $80. What is the margin of safety in dollars?

a. $80,000

b. $400,000

c. $720,000

d. $1,120,000

55. Margin of safety in dollars is

a. expected sales divided by break-even sales.

b. expected sales less break-even sales.

c. actual sales less expected sales.

d. expected sales less actual sales.

56. The margin of safety ratio is

a. expected sales divided by break-even sales.

b. expected sales less break-even sales.

c. margin of safety in dollars divided by expected sales.

d. margin of safety in dollars divided by break-even sales.

57. In 2016, Hagar Corp. sold 3,000 units at $500 each. Variable expenses were $350 per

unit, and fixed expenses were $780,000. The same variable expenses per unit and fixed

expenses are expected for 2017. If Hagar cuts selling price by 4%, what is Hagar’s break–

even point in units for 2017?

a. 5,200

b. 5,416

c. 5,760

d. 6,000

58. In 2016, Carow sold 3,000 units at $500 each. Variable expenses were $250 per unit, and

fixed expenses were $500,000. The same selling price is expected for 2017. Carow is

tentatively planning to invest in equipment that would increase fixed costs by 20%, while

decreasing variable costs per unit by 20%. What is Carow’s break-even point in units for

2017?

a. 2,000

b. 2,400

c. 2,500

d. 3,000

Test Bank for Managerial Accounting, Seventh Edition

6 – 12

59. In 2016, Raleigh sold 1,000 units at $500 each, and earned net income of $40,000.

Variable expenses were $300 per unit, and fixed expenses were $160,000. The same

selling price is expected for 2017. Raleigh’s variable cost per unit will rise by 10% in 2017

due to increasing material costs, so they are tentatively planning to cut fixed costs by

$10,000. How many units must Raleigh sell in 2017 to maintain the same income level as

2016?

a. 882

b. 1,000

c. 1,056

d. 1,118

60. Sales mix is

a. the relative percentage in which a company sells its multiple products.

b. the trend of sales over recent periods.

c. the mix of variable and fixed expenses in relation to sales.

d. a measure of leverage used by the company.

61. In a sales mix situation, at any level of units sold, net income will be higher if

a. more higher contribution margin units are sold than lower contribution margin units.

b. more lower contribution margin units are sold than higher contribution margin units.

c. more fixed expenses are incurred.

d. weighted-average unit contribution margin decreases.

62. Ramirez Corporation sells two types of computer hard drives. The sales mix is 30% (Q-

Drive) and 70% (Q-Drive Plus). Q-Drive has variable costs per unit of $90 and a selling

price of $150. Q-Drive Plus has variable costs per unit of $105 and a selling price of $195.

The weighted-average unit contribution margin for Ramirez is

a. $69.

b. $75.

c. $81.

d. $150.

63. Capitol Manufacturing sells 4,000 units of Product A annually, and 6,000 units of Product

B annually. The sales mix for Product A is

a. 40%.

b. 60%.

c. 67%.

d. Cannot determine from information given.

Cost-Volume-Profit Analysis: Additional Issues

6 – 13

64. Ramirez Corporation sells two types of computer hard drives. The sales mix is 30% (Q-

Drive) and 70% (Q-Drive Plus). Q-Drive has variable costs per unit of $90 and a selling

price of $150. Q-Drive Plus has variable costs per unit of $105 and a selling price of $195.

Ramirez’s fixed costs are $891,000. How many units of Q-Drive would be sold at the

break-even point?

a. 3,300

b. 4,455

c. 11,000

d. 7,700

Use the following information for questions 65 and 66.

Roosevelt Corporation has a weighted-average unit contribution margin of $30 for its two

products, Standard and Supreme. Expected sales for Roosevelt are 40,000 Standard and 60,000

Supreme. Fixed expenses are $1,800,000.

65. How many Standards would Roosevelt sell at the break-even point?

a. 24,000

b. 36,000

c. 40,000

d. 60,000

66. At the expected sales level, Roosevelt’s net income will be

a. $(300,000).

b. $ – 0 -.

c. $1,200,000.

d. $3,000,000.

Use the following information for questions 67–70.

Swanson Company has two divisions; Sporting Goods and Sports Gear. The sales mix is 65% for

Sporting Goods and 35% for Sports Gear. Swanson incurs $6,660,000 in fixed costs. The

contribution margin ratio for Sporting Goods is 30%, while for Sports Gear it is 50%.

67. The weighted-average contribution margin ratio is

a. 37%.

b. 40%.

c. 43%.

d. 50%.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 14

68. The break-even point in dollars is

a. $2,464,200.

b. $15,488,373.

c. $16,650,000.

d. $18,000,000.

69. What will sales be for the Sporting Goods Division at the break-even point?

a. $5,400,000

b. $6,300,000

c. $10,067,442

d. $11,700,000

70. What will be the total contribution margin at the break-even point?

a. $5,730,699

b. $6,660,000

c. $6,720,000

d. $7,740,000

71. A shift from low-margin sales to high-margin sales

a. may increase net income, even though there is a decline in total units sold.

b. will always increase net income.

c. will always decrease net income.

d. will always decrease units sold.

72. A shift from high-margin sales to low-margin sales

a. may decrease net income, even though there is an increase in total units sold.

b. will always decrease net income.

c. will always increase net income.

d. will always increase units sold.

Use the following information for questions 73 and 74.

MacCloud Industries has two divisions—Standard and Premium. Each division has hundreds of

different types of tennis racquets and tennis products. The following information is available:

Standard Division Premium Division Total

Sales $400,000 $600,000 $1,000,000

Variable costs 280,000 360,000

Contribution margin $120,000 $240,000

Total fixed costs $300,000

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 15

73. What is the weighted-average contribution margin ratio?

a. 34%

b. 35%

c. 36%

d. 50%

74. What is the break-even point in dollars?

a. $108,000

b. $833,333

c. $857,143

d. $882,353

75. The sales mix percentages for Novotna’s Boston and Seattle Divisions are 70% and 30%.

The contribution margin ratios are: Boston (40%) and Seattle (30%). Fixed costs are

$2,220,000. What is Novotna’s break-even point in dollars?

a. $777,000

b. $6,000,000

c. $6,342,856

d. $6,727,272

76. A company can sell all the units it can produce of either Product A or Product B but not

both. Product A has a unit contribution margin of $16 and takes two machine hours to make

and Product B has a unit contribution margin of $30 and takes three machine hours to

make. If there are 5,000 machine hours available to manufacture a product, income will be

a. $10,000 more if Product A is made.

b. $10,000 less if Product B is made.

c. $10,000 less if Product A is made.

d. the same if either product is made.

77. Brooks Corporation can sell all the units it can produce of either Plain or Fancy but not both.

Plain has a unit contribution margin of $72 and takes two machine hours to make and

Fancy has a unit contribution margin of $90 and takes three machine hours to make. There

are 2,400 machine hours available to manufacture a product. What should Brooks do?

a. Make Fancy which creates $18 more profit per unit than Plain does.

b. Make Plain which creates $6 more profit per machine hour than Fancy does.

c. Make Plain because more units can be made and sold than Fancy.

d. The same total profits exist regardless of which product is made.

78. What is the key factor in determining sales mix if a company has limited resources?

a. Contribution margin per unit of limited resource

b. The amount of fixed costs per unit

c. Total contribution margin

d. The cost of limited resources

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 16

79. Greg’s Breads can produce and sell only one of the following two products:

Oven Contribution

Hours Required Margin Per Unit

Muffins 0.2 $3

Coffee Cakes 0.3 $4

The company has oven capacity of 1,500 hours. How much will contribution margin be if it

produces only the most profitable product?

a. $15,000

b. $20,000

c. $22,500

d. $30,000

80. Curtis Corporation’s contribution margin is $25 per unit for Product A and $30 for Product

B. Product A requires 2 machine hours and Product B requires 4 machine hours. How

much is the contribution margin per unit of limited resource for each product?

A B

a. $12.50 $7.50

b. $12.50 $8.33

c. $10.00 $7.50

d. $10.00 $8.33

81. Cost structure

a. refers to the relative proportion of fixed versus variable costs that a company incurs.

b. generally has little impact on profitability.

c. cannot be significantly changed by companies.

d. refers to the relative proportion of operating versus nonoperating costs that a company

incurs.

82. Outsourcing production will

a. reduce fixed costs and increase variable costs.

b. reduce variable costs and increase fixed costs.

c. have no effect on the relative proportion of fixed and variable costs.

d. make the company more susceptible to economic swings.

83. Reducing reliance on human workers and instead investing heavily in computers and

online technology will

a. reduce fixed costs and increase variable costs.

b. reduce variable costs and increase fixed costs.

c. have no effect on the relative proportion of fixed and variable costs.

d. make the company less susceptible to economic swings.

Cost-Volume-Profit Analysis: Additional Issues

6 – 17

84. Cost structure refers to the relative proportion of

a. selling expenses versus administrative expenses.

b. selling and administrative expenses versus cost of goods sold.

c. contribution margin versus sales.

d. none of the above.

Use the following information for questions 85 and 86.

Mercantile Corporation has sales of $2,000,000, variable costs of $800,000, and fixed costs of

$900,000.

85. Mercantile’s degree of operating leverage is

a. 1.33.

b. 1.67.

c. 1.50.

d. 4.00.

86. Mercantile’s margin of safety ratio is

a. .15.

b. .25.

c. .33.

d. .75.

87. Which of the following statements is not true?

a. Operating leverage refers to the extent to which a company’s net income reacts to a

given change in sales.

b. Companies that have higher fixed costs relative to variable costs have higher

operating leverage.

c. When a company’s sales revenue is increasing, high operating leverage is good

because it means that profits will increase rapidly.

d. When a company’s sales revenue is decreasing, high operating leverage is good

because it means that profits will decrease at a slower pace than revenues decrease.

88. Miller Manufacturing’s degree of operating leverage is 1.5. Warren Corporation’s degree

of operating leverage is 3. Warren’s earnings would go up (or down) by ________ as

much as Miller’s with an equal increase (or decrease) in sales.

a. 1/2

b. 1.5 times

c. 2 times

d. 4.5 times

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 18

89. The margin of safety ratio

a. is computed as actual sales divided by break-even sales.

b. indicates what percent decline in sales could be sustained before the company would

operate at a loss.

c. measures the ratio of fixed costs to variable costs.

d. is used to determine the break-even point.

90. A cost structure which relies more heavily on fixed costs makes the company

a. more sensitive to changes in sales revenue.

b. less sensitive to changes in sales revenue.

c. either more or less sensitive to changes in sales revenue, depending on other factors.

d. have a lower break-even point.

91. A company with a higher contribution margin ratio is

a. more sensitive to changes in sales revenue.

b. less sensitive to changes in sales revenue.

c. either more or less sensitive to changes in sales revenue, depending on other factors.

d. likely to have a lower breakeven point.

92. The degree of operating leverage

a. does not provide a reliable measure of a company’s earnings volatility.

b. cannot be used to compare companies.

c. is computed by dividing total contribution margin by net income.

d. measures how much of each sales dollar is available to cover fixed expenses.

a93. Only direct materials, direct labor, and variable manufacturing overhead costs are

considered product costs when using

a. full costing.

b. absorption costing.

c. variable costing.

d. product costing.

a94. When a company assigns the costs of direct materials, direct labor, and both variable and

fixed manufacturing overhead to products, that company is using

a. operations costing.

b. absorption costing.

c. variable costing.

d. product costing.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 19

a95. Companies recognize fixed manufacturing overhead costs as period costs (expenses)

when incurred when using

a. full costing.

b. absorption costing.

c. product costing.

d. variable costing.

a96. Under absorption costing and variable costing, how are fixed manufacturing costs

treated?

Absorption Variable

a. Product Cost Product Cost

b. Product Cost Period Cost

c. Period Cost Product Cost

d. Period Cost Period Cost

a97. Under absorption costing and variable costing, how are variable manufacturing costs

treated?

Absorption Variable

a. Product Cost Product Cost

b. Product Cost Period Cost

c. Period Cost Product Cost

d. Period Cost Period Cost

a98. Under absorption costing and variable costing, how are direct labor costs treated?

Absorption Variable

a. Product Cost Product Cost

b. Product Cost Period Cost

c. Period Cost Product Cost

d. Period Cost Period Cost

a99. Fixed selling expenses are period costs

a. under both absorption and variable costing.

b. under neither absorption nor variable costing.

c. under absorption costing, but not under variable costing.

d. under variable costing, but not under absorption costing.

a100. Which cost is not charged to the product under variable costing?

a. Direct materials

b. Direct labor

c. Variable manufacturing overhead

d. Fixed manufacturing overhead

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 20

a101. Which cost is charged to the product under variable costing?

a. Variable manufacturing overhead

b. Fixed manufacturing overhead

c. Variable administrative expenses

d. Fixed administrative expenses

a102. Variable costing

a. is used for external reporting purposes.

b. is required under GAAP.

c. treats fixed manufacturing overhead as a period cost.

d. is also known as full costing.

Use the following information for questions 103–107.

Sprinkle Co. sells its product for $60 per unit. During 2016, it produced 60,000 units and sold

50,000 units (there was no beginning inventory). Costs per unit are: direct materials $15, direct

labor $9, and variable overhead $3. Fixed costs are: $720,000 manufacturing overhead, and

$90,000 selling and administrative expenses.

a103. The per unit manufacturing cost under absorption costing is

a. $24.

b. $27.

c. $39.

d. $40.

a104. The per unit manufacturing cost under variable costing is

a. $24.

b. $27.

c. $39.

d. $40.

a105. Cost of goods sold under absorption costing is

a. $1,350,000.

b. $1,620,000.

c. $1,950,000.

d. $1,560,000.

a106. Ending inventory under variable costing is

a. $270,000.

b. $390,000.

c. $600,000.

d. $1,350,000.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 21

a107. Under absorption costing, what amount of fixed overhead is deferred to a future period?

a. $30,000

b. $120,000

c. $150,000

d. $720,000

a108. Net income under absorption costing is gross profit less

a. cost of goods sold.

b. fixed manufacturing overhead and fixed selling and administrative expenses.

c. fixed manufacturing overhead and variable manufacturing overhead.

d. variable selling and administrative expenses and fixed selling and administrative

expenses.

a109. Net income under variable costing is contribution margin less

a. cost of goods sold.

b. fixed manufacturing overhead and fixed selling and administrative expenses.

c. fixed manufacturing overhead and variable manufacturing overhead.

d. variable selling and administrative expenses and fixed selling and administrative

expenses.

a110. The manufacturing cost per unit for absorption costing is

a. usually, but not always, higher than manufacturing cost per unit for variable costing.

b. usually, but not always, lower than manufacturing cost per unit for variable costing.

c. always higher than manufacturing cost per unit for variable costing.

d. always lower than manufacturing cost per unit for variable costing.

a111. The one primary difference between variable and absorption costing is that under

a. variable costing, companies charge the fixed manufacturing overhead as an expense

in the current period.

b. absorption costing, companies charge the fixed manufacturing overhead as an

expense in the current period.

c. variable costing, companies charge the variable manufacturing overhead as an

expense in the current period.

d. absorption costing, companies charge the variable manufacturing overhead as an

expense in the current period.

a112. Net income under absorption costing is higher than net income under variable costing

a. when units produced exceed units sold.

b. when units produced equal units sold.

c. when units produced are less than units sold.

d. regardless of the relationship between units produced and units sold.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 22

a113. Some fixed manufacturing overhead costs of the current period are deferred to future

periods under

a. absorption costing.

b. variable costing.

c. both absorption and variable costing.

d. neither absorption nor variable costing.

Use the following information for questions 114–118.

Nielson Corp. sells its product for $6,600 per unit. Variable costs per unit are: manufacturing,

$3,600, and selling and administrative, $75. Fixed costs are: $18,000 manufacturing overhead,

and $24,000 selling and administrative. There was no beginning inventory at 1/1/15. Production

was 20 units per year in 2015–2017. Sales were 20 units in 2015, 16 units in 2016, and 24 units

in 2017.

a114. Income under absorption costing for 2016 is

a. $4,800.

b. $8,400.

c. $9,600.

d. $13,200.

a115. Income under absorption costing for 2017 is

a. $19,800.

b. $23,400.

c. $24,600.

d. $28,200.

a116. Income under variable costing for 2016 is

a. $4,800.

b. $8,400.

c. $9,600.

d. $13,200.

a117. Income under variable costing for 2017 is

a. $19,800.

b. $23,400.

c. $24,600.

d. $28,200.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 23

a118. For the three years 2015–2017,

a. absorption costing income exceeds variable costing income by $8,000.

b. absorption costing income equals variable costing income.

c. variable costing income exceeds absorption costing income by $8,000.

d. absorption costing income may be greater than, equal to, or less than variable costing

income, depending on the situation.

a119. When production exceeds sales,

a. some fixed manufacturing overhead costs are deferred until a future period under

absorption costing.

b. some fixed manufacturing overhead costs are deferred until a future period under

variable costing.

c. variable and fixed manufacturing overhead costs are deferred until a future period

under absorption costing.

b. variable and fixed manufacturing overhead costs are deferred until a future period

under variable costing.

a120. When production exceeds sales,

a. ending inventory under variable costing will exceed ending inventory under absorption

costing.

b. ending inventory under absorption costing will exceed ending inventory under variable

costing.

c. ending inventory under absorption costing will be equal to ending inventory under

variable costing.

d. ending inventory under absorption costing may exceed, be equal to, or be less than

ending inventory under variable costing.

a121. Management may be tempted to overproduce when using

a. variable costing, in order to increase net income.

b. variable costing, in order to decrease net income.

c. absorption costing, in order to increase net income.

d. absorption costing, in order to decrease net income.

a122. If a division manager’s compensation is based upon the division’s net income, the

manager may decide to meet the net income targets by increasing production when using

a. variable costing, in order to increase net income.

b. variable costing, in order to decrease net income.

c. absorption costing, in order to increase net income.

d. absorption costing, in order to decrease net income.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 24

a123. Expected sales for next year for the Beresford Company is 150,000 units. Curt Planters,

manager of the Beresford Division, is under pressure to improve the performance of the

Division. As he plans for next year, he has to decide whether to produce 150,000 units or

170,000 units. The Beresford Company will have higher net income if Curt Planters

decides to produce

a. 170,000 units if income is measured under absorption costing.

b. 170,000 units if income is measured under variable costing.

c. 150,000 units if income is measured under absorption costing.

d. 150,000 units if income is measured under variable costing.

a124. Which of the following is a potential advantage of variable costing relative to absorption

costing?

a. Net income is affected by changes in production levels.

b. The use of variable costing is consistent with cost-volume-profit analysis.

c. Net income computed under variable costing is not closely tied to changes in sales

levels.

d. More than one of the above.

a125. Companies that use just-in-time processing techniques will

a. have greater differences between absorption and variable costing net income.

b. have smaller differences between absorption and variable costing net income.

c. not be able to use absorption costing.

d. not be able to use variable costing.

Answers to Multiple Choice Questions

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Cost-Volume-Profit Analysis: Additional Issues

6 – 25

BRIEF EXERCISES

BE 126

Archer Industries sells three different sets of sportswear. Sleek sells for $30 and has variable

costs of $18; Smooth sells for $50 and has variable costs of $30; Potent sells for $70 and has

variable costs of $45. The sales mix of the three sets is: Sleek, 50%; Smooth, 30%; and Potent,

20%.

Instructions

What is the weighted-average unit contribution margin?

BE 127

Lazaro Inc. sells two product lines. The sales mix of the product lines is: Standard, 60%; and

Deluxe, 40%. The contribution margin ratio of each line is: Standard, 40%; and Deluxe, 45%.

Lazaro’s fixed costs are $1,575,000.

Instructions

What is the dollar amount of Deluxe sales at the break-even point?

BE 128

Hunt, Inc. provided the following information concerning two products:

Product 12 Product 43

Contribution margin per unit $22 $18

Machine hours required for one unit 2 hours 1.5 hours

Instructions

Compute the contribution margin per unit of limited resource for each product. Which product

should Hunt tell its sales personnel to “push” to customers?

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 26

Solution 128 (3–5 min.)

BE 129

Gallery Corporation makes two products, footballs and baseballs. Additional information follows:

Footballs Baseballs

Units 2,000 2,500

Sales $60,000 $25,000

Variable costs 24,000 13,750

Fixed costs 10,000 5,250

Net income $26,000 $ 6,000

Yards of leather per unit 1.25 0.30

Profit per unit $13.00 $2.40

Contribution margin per unit $18.00 $4.50

Assume that Gallery is able to order an additional 2,500 yards of leather and wishes to maximize

its income. Of the additional units it produces, at least 500 of each product are necessary for

sales.

Instructions

How many units of each must be produced?

BE 130

Marina Manufacturing is considering buying new equipment for its factory. The new equipment

will reduce variable labor costs but increase depreciation expense. Contribution margin is

expected to increase from $250,000 to $300,000. Net income is expected to remain the same at

$100,000.

Instructions

Compute the degree of operating leverage before and after the purchase of the new equipment

and interpret your results.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 27

Solution 130 (4–6 min.)

BE 131

The degree of operating leverage for Gurney, Inc. and Dough Company are 2.4 and 5.6

respectively. Both have net incomes of $75,000. Determine their respective contribution margins.

aBE 132

Swift Co. produces footballs. It incurred the following costs this year:

Direct materials $35,000

Direct labor 31,000

Fixed manufacturing overhead 22,000

Variable manufacturing overhead 38,000

Fixed selling and administrative expenses 23,000

Variable selling and administrative expenses 14,000

Instructions

What are the total product costs for the company under variable costing?

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 28

aBE 133

Swift Co. produces footballs. It incurred the following costs this year:

Direct materials $40,000

Direct labor 31,000

Fixed manufacturing overhead 22,000

Variable manufacturing overhead 38,000

Fixed selling and administrative expenses 23,000

Variable selling and administrative expenses 14,000

Instructions

What are the total product costs for the company under absorption costing?

aBE 134

During 2016, Basler Manufacturing produced 60,000 units and sold 55,000 for $10 per unit.

Variable manufacturing costs were $4 per unit. Annual fixed manufacturing overhead was

$120,000 ($2 per unit). Variable selling and administrative costs were $1 per unit sold, and fixed

selling and administrative costs were $30,000.

Instructions

Prepare a variable costing income statement.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 29

aBE 135

During 2016, Basler Manufacturing produced 60,000 units and sold 55,000 for $10 per unit.

Variable manufacturing costs were $5 per unit. Annual fixed manufacturing overhead was

$120,000 ($2 per unit). Variable selling and administrative costs were $1 per unit sold, and fixed

selling and administrative costs were $30,000.

Instructions

Prepare an absorption costing income statement.

EXERCISES

Ex. 136

Kindle, Inc. manufactures cosmetic products that are sold through a network of sales agents. The

agents are paid a commission of 12.5% of sales. The income statement for the year ending

December 31, 2016, is as follow.

KINDLE, INC.

Income Statement

Year Ending December 31, 2016

Sales $130,000

Cost of goods sold

Variable $58,500

Fixed 14,350 72,850

Gross margin 57,150

Selling and marketing expenses

Commissions $16,250

Fixed costs 17,100 33,350

Operating income $ 23,800

The company is considering hiring its own sales staff to replace the network of agents. It will pay

its salespeople a commission of 10% and incur additional fixed costs of $13 million.

Instructions

(a) Under the current policy of using a network of sales agents, calculate Kindle, Inc.’s break-

even point in sales dollars for the year 2016.

(b) Calculate the company’s break-even point in sales dollars for the year 2016 if it hires its own

sales force to replace the network of agents.

(c) Calculate the degree of operating leverage at sales of $130 million if (1) Kindle, Inc. uses

sales agents, and (2) Kindle, Inc. employs its own sales staff.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 30

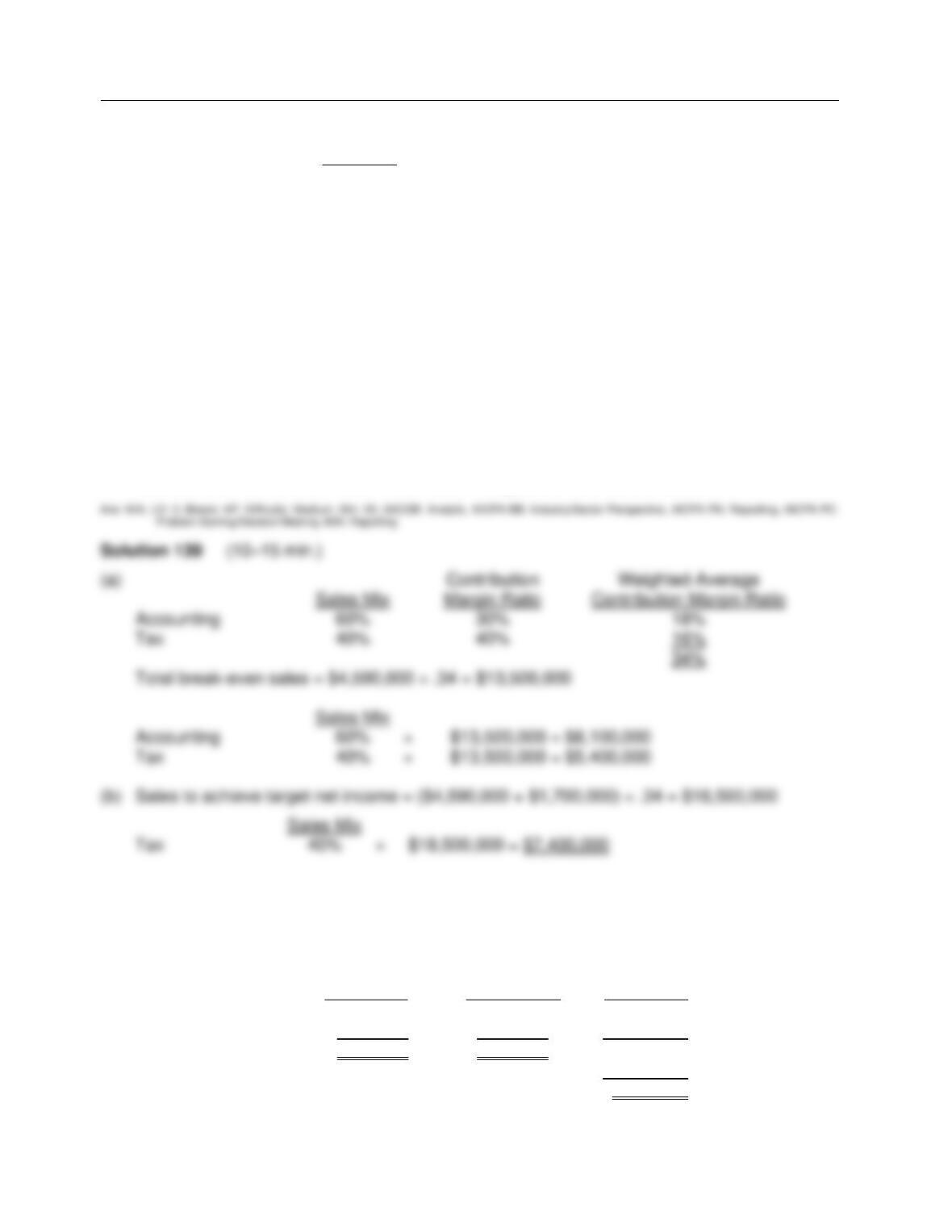

aSolution 136 (15–18 min.)

Ex. 137

Qwik Service has over 200 auto-maintenance service outlets nationwide. It provides primarily two

lines of service: oil changes and brake repair. Oil change-related services represent 75% of its

sales and provide a contribution margin ratio of 20%. Brake repair represents 25% of its sales

and provides a 60% contribution margin ratio. The company‘s fixed costs are $15,000,000 (that

is, $75,000 per service outlet).

Instructions

(a) Calculate the dollar amount of each type of service that the company must provide in order

to break even.

(b) The company has a desired net income of $45,000 per service outlet. What is the dollar

amount of each type of service that must be provided by each service outlet to meet its

target net income per outlet?

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 31

Solution 137 (12–15 min.)

Ex. 138

Seaver Corporation manufactures mountain bikes. It has fixed costs of $4,140,000. Seaver’s

sales mix and contribution margin per unit is shown as follows:

Sales Mix Contribution Margin

Green 25% $120

Brown 45% $ 60

Blue 30% $ 40

Instructions

Compute the number of each type of bike that the company would need to sell in order to break

even under this product mix.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 32

Ex 138 (cont.)

Sales Mix

Green 25% × 60,000 = 15,000 bikes

Brown 45% × 60,000 = 27,000 bikes

Blue 30% × 60,000 = 18,000 bikes

Ex. 139

DeMont Tax Services provides primarily two lines of service: accounting and tax. Accounting-

related services represent 60% of its revenue and provide a contribution margin ratio of 30%. Tax

services represent 40% of its revenue and provide a 40% contribution margin ratio. The

company’s fixed costs are $4,590,000.

Instructions

(a) Calculate the revenue from each type of service that the company must achieve to break

even.

(b) The company has a desired net income of $1,700,000. What amount of revenue would

DeMont earn from tax services if it achieves this goal with the current sales mix?

Ex. 140

Blue Chance Co. sells computers and video game systems. The business is divided into two

divisions along product lines. Variable costing income statements for the current year are

presented below:

Computers VG Systems Total

Sales $700,000 $300,000 $1,000,000

Variable costs 420,000 210,000 630,000

Contribution margin $280,000 $ 90,000 370,000

Fixed costs 296,000

Net income $ 74,000

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 33

Ex 140 (cont.)

Instructions

(a) Determine the sales mix and contribution margin ratio for each division.

(b) Calculate the company’s weighted-average contribution margin ratio.

(c) Calculate the company’s break-even point in dollars.

(d) Determine the sales level, in dollars, for each division at the break-even point.

Ex. 141

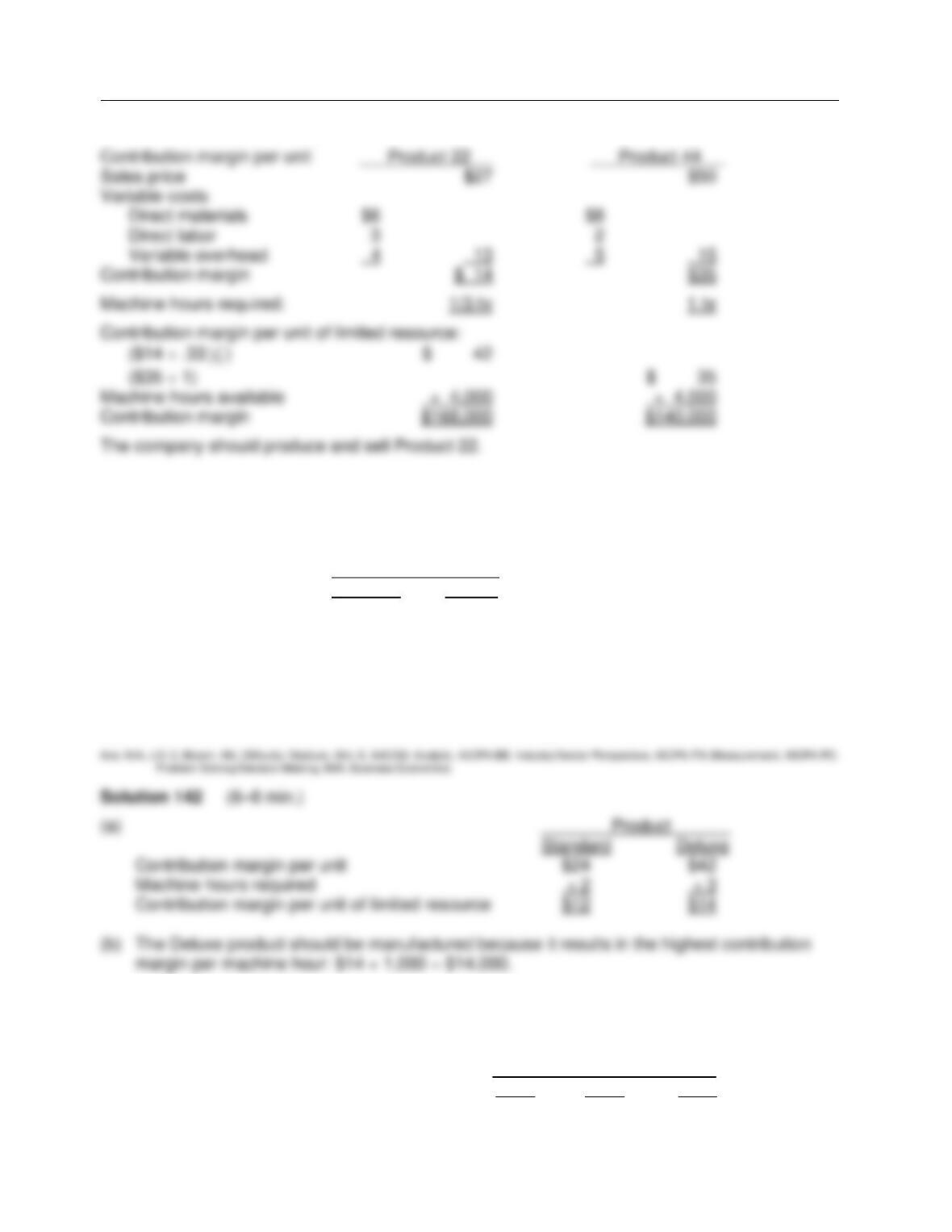

Hewitt Co. has 4,000 machine hours available to produce either Product 22 or Product 44. The

cost accounting department developed the following unit information for each product:

Product 22 Product 44

Sales price $27 $50

Direct materials 6 8

Direct labor 3 2

Variable manufacturing overhead 4 5

Fixed manufacturing overhead 3 5

Machine time required 20 minutes 60 minutes

Instructions

Management wants to know which product to produce in order to maximize the company’s

income. Taking into consideration the constraints under which the company operates, prepare a

report to show which product should be produced and sold.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 34

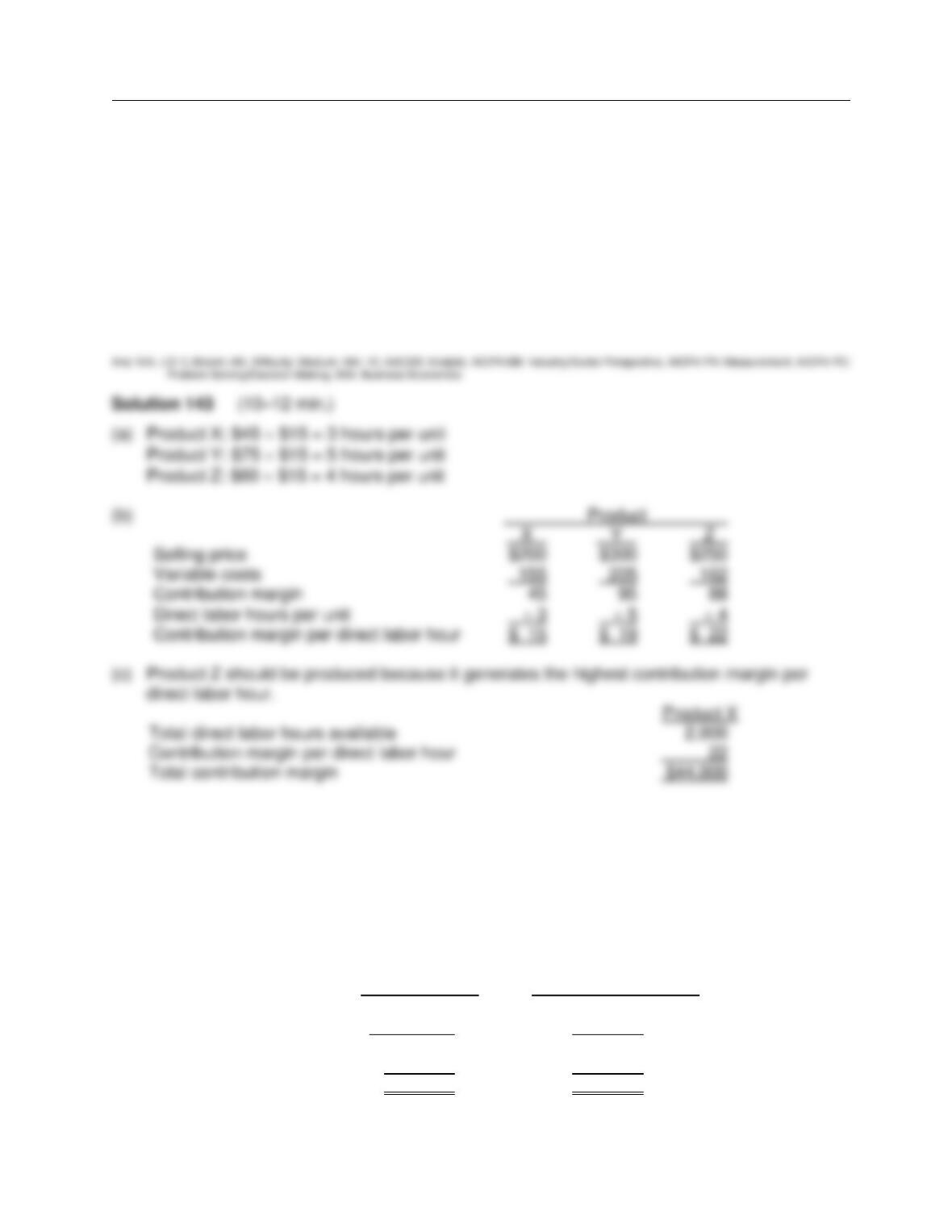

Solution 141 (10–12 min.)

Ex. 142

Reynolds, Inc. manufactures and sells two products. Relevant per unit data concerning each

product are given below:

Product

Standard Deluxe

Selling price $50 $75

Variable costs $26 $33

Machine hours 2 3

Instructions

(a) Compute the contribution margin per unit of limited resource for each product.

(b) If 1,000 additional machine hours are available, which product should be manufactured?

Ex. 143

Oscar Corporation produces and sells three products. Unit data concerning each product is

shown below.

Product

X Y Z

Selling price $200 $300 $250

Direct labor costs 45 75 60

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 35

Other variable costs 110 130 102

Ex 143 (cont.)

The company has 2,000 hours of labor available to build inventory in anticipation of the

company’s peak season. Management is trying to decide which product should be produced. The

direct labor hourly rate is $15.

Instructions

(a) Determine the number of direct labor hours per unit.

(b) Determine the contribution margin per direct labor hour.

(c) Determine which product should be produced and the total contribution margin for that

product.

Ex. 144

Shanahan Co. of Dublin, Ireland is contemplating a major change in its cost structure. Currently,

all of its drafting work is performed by skilled draftsmen. Mike Shanahan the owner, is considering

replacing the draftsmen with a computerized drafting system.

However, before making the change, Mike would like to know the consequences of the change,

since the volume of business varies significantly from year to year. Shown below are CVP income

statements for each alternative.

Manual System Computerized System

Sales $1,500,000 $1,500,000

Variable costs 1,200,000 900,000

Contribution margin 300,000 600,000

Fixed costs 150,000 450,000

Net income $150,000 $150,000

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 36

Ex. 144 (cont.)

Instructions

(a) Determine the degree of operating leverage for each alternative.

(b) Which alternative would produce the higher net income if sales increased by $300,000?

Ex. 145

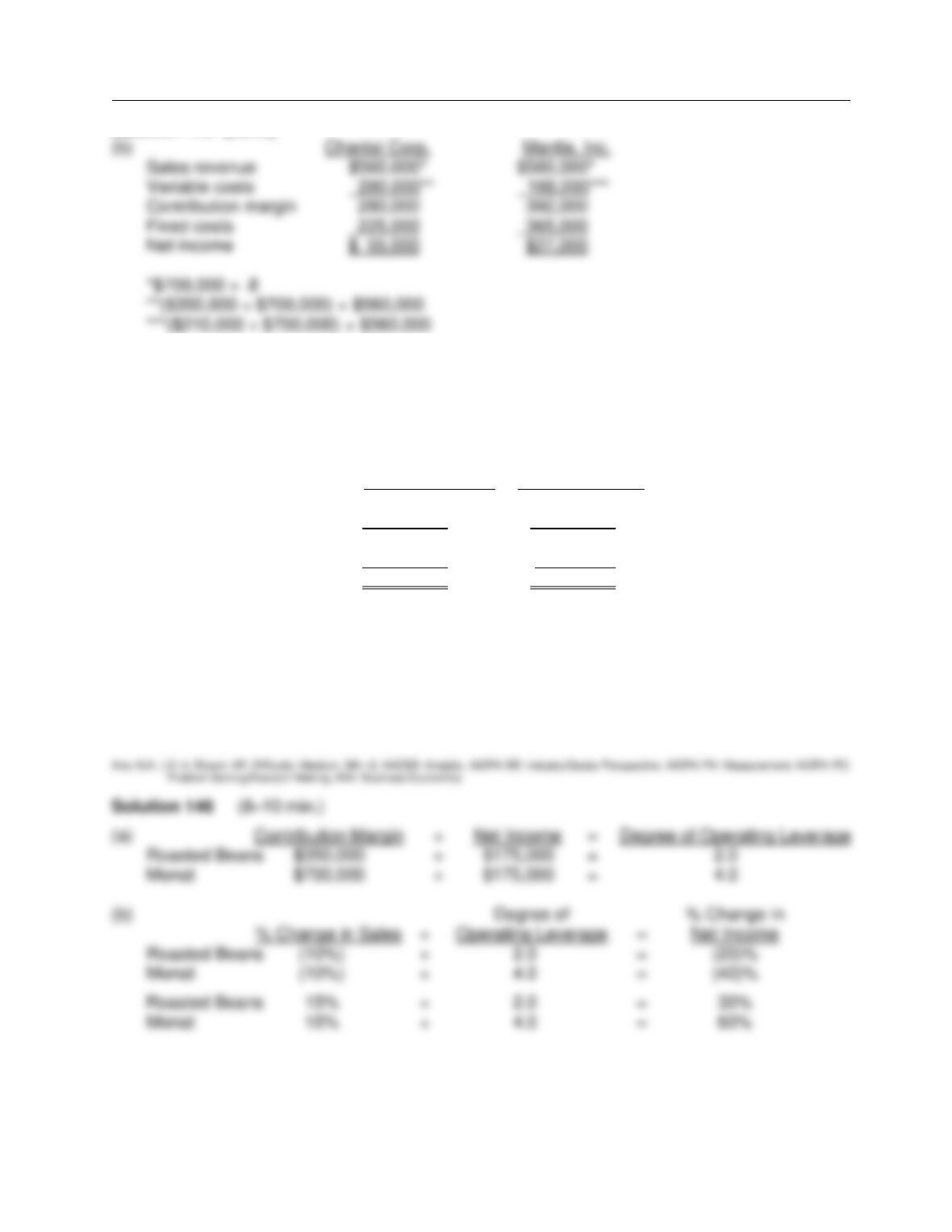

The following CVP income statements are available for Chantal Corp. and Mantle, Inc.

Chantal Corp. Mantle, Inc.

Sales revenue $700,000 $700,000

Variable costs 350,000 210,000

Contribution margin 350,000 490,000

Fixed costs 225,000 365,000

Net income $125,000 $125,000

Instructions

(a) Compute the degree of operating leverage for each company.

(b) Assume that sales revenue decreases by 20%. Prepare a CVP income statement for each

company.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 37

Solution 145 (cont.)

Ex. 146

An investment banker is analyzing two companies that specialize in the production and sale of

gourmet cappuccino and chai mixes. Roasted Beans Co. uses a labor-intensive approach and

Monat Industries uses a mechanized system. Variable costing income statements for the two

companies are shown below:

Roasted Beans Monat Industries

Sales $1,000,000 $1,000,000

Variable costs 650,000 300,000

Contribution margin 350,000 700,000

Fixed costs 175,000 525,000

Net Income $ 175,000 $ 175,000

The investment banker is interested in acquiring one of these companies. However, she is

concerned about the impact that each company’s cost structure might have on its profitability.

Instructions

(a) Calculate each company’s degree of operating leverage.

(b) Determine the effect on each company’s net income if sales decrease by 10% and if sales

increase by 15%. Do not prepare income statements.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 38

aEx. 147

Indicate with a check mark whether each of the following would be a product cost or a period cost

under an absorption or a variable system for Sour Industries.

Absorption Variable

Product Period Product Period

a. Direct materials ________ ________ ________ _______

b. Direct labor ________ ________ ________ _______

c. Factory utilities ________ ________ ________ _______

d. Factory rent ________ ________ ________ _______

e. Indirect labor ________ ________ ________ _______

f. Factory supervisor salaries ________ ________ ________ _______

g. Factory maintenance (variable) ________ ________ ________ _______

h. Factory depreciation ________ ________ ________ _______

i. Sales salaries ________ ________ ________ _______

j. Sales commissions ________ ________ ________ _______

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 39

aEx. 148

Nimble Corp. manufactures and sells a variety of camping products. Recently the company

opened a new plant to manufacture a deluxe portable cooking unit. Cost and sales data for the

first month of operations are shown below:

Manufacturing Costs

Fixed Overhead $140,000

Variable overhead $3 per unit

Direct labor $12 per unit

Direct material $30 per unit

Beginning inventory 0 units

Units produced 10,000

Units sold 9,000

Selling and Administrative Costs

Fixed $200,000

Variable $4 per unit sold

The portable cooking unit sells for $110. Management is interested in the opening month’s results

and has asked for an income statement.

Instructions

Assume the company uses absorption costing. Calculate the production cost per unit and prepare

an income statement for the month of June, 2016.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 40

aEx. 149

On-Road Wheels, Inc. manufactures a basic road bicycle. Production and sales data for the most

recent year are as follows (no beginning inventory):

Variable production costs $100 per bike

Fixed production costs $400,000

Variable selling and administrative costs $22 per bike

Fixed selling and administrative costs $550,000

Selling price $200 per bike

Production 20,000 bikes

Sales 18,000 bikes

Instructions

(a) Prepare a brief income statement using absorption costing.

(b) Compute the amount to be reported for inventory in the year-end absorption costing balance

sheet.

aEx. 150

On-Road Wheels, Inc. manufactures a basic road bicycle. Production and sales data for the most

recent year are as follows (no beginning inventory):

Variable production costs $95 per bike

Fixed production costs $400,000

Variable selling and administrative costs $22 per bike

Fixed selling and administrative costs $550,000

Selling price $200 per bike

Production 20,000 bikes

Sales 16,000 bikes

Instructions

(a) Prepare a brief income statement using variable costing.

(b) Compute the amount to be reported for inventory in the year-end variable costing balance

sheet.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 41

aSolution 150 (8–12 min.)

aEx. 151

Cutting Edge Corp. produces sporting equipment. In 2015, the first year of operations, Cutting

Edge produced 25,000 units and sold 22,000 units. In 2016, the production and sales results

were exactly reversed. In each year, selling price was $100, variable manufacturing costs were

$40 per unit, variable selling expenses were $8 per unit, fixed manufacturing costs were

$550,000, and fixed administrative expenses were $200,000.

Instructions

(a) Compute the net income under variable costing for each year.

(b) Compute the net income under absorption costing for each year.

(c) Reconcile the differences each year in income from operations under the two costing

approaches.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 42

aEx. 152

Graham is a division of Flynn, Inc. The division manufactures and sells a pump that is used in a

wide variety of applications. During the coming year, it expects to sell 30,000 units for $25 per

unit. Steve Moss, division manager, is considering producing either 30,000 or 35,000 units during

the period. Other information is presented in the schedule below:

Division Information – 2016

Beginning inventory 0

Expected sales in units 30,000

Selling price per unit $25

Variable manufacturing cost per unit $7

Fixed manufacturing overhead costs (total) $420,000

Fixed manufacturing overhead costs per unit

Based on 30,000 units ($420,000 ÷ 30,000) $14

Based on 35,000 units ($420,000 ÷ 35,000) $12

Manufacturing cost per unit

Based on 30,000 units ($7 variable + $14 fixed) $21

Based on 35,000 units ($7 variable + $12 fixed) $19

Selling and administrative expenses (all fixed) $25,000

Instructions

(a) Prepare an absorption costing income statement with one column showing the results if

30,000 units are produced and one column showing the results if 35,000 units are produced.

(b) Why is income different for the two production levels when sales is 30,000 units either way?

Cost-Volume-Profit Analysis: Additional Issues

6 – 43

aEx. 153

Graham is a division of Flynn, Inc. The division manufactures and sells a pump that is used in a

wide variety of applications. During the coming year, it expects to sell 30,000 units for $25 per

unit. Steve Moss, division manager, is considering producing either 30,000 or 40,000 units during

the period. Other information is presented in the schedule below:

Division Information – 2016

Beginning inventory 0

Expected sales in units 30,000

Selling price per unit $25

Variable manufacturing cost per unit $7

Fixed manufacturing overhead costs (total) $480,000

Fixed manufacturing overhead costs per unit

Based on 30,000 units ($480,000 ÷ 30,000) $16

Based on 40,000 units ($480,000 ÷ 40,000) $12

Manufacturing cost per unit

Based on 30,000 units ($7 variable + $16 fixed) $23

Based on 40,000 units ($7 variable + $12 fixed) $19

Selling and administrative expenses (all fixed) $25,000

Instructions

Prepare a variable costing income statement with one column showing the results if 30,000 units

are produced and one column showing the results if 40,000 units are produced.

COMPLETION STATEMENTS

154. The ______________ income statement classifies cost as variable or fixed and computes

a contribution margin.

155. _________________ tells a company how far sales can drop before it will be operating at

a loss.

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 44

156. ___________________ is the relative percentage in which a company sells its multiple

products.

157. When more than one product is sold, the break-even point can be determined by dividing

fixed expenses by _______________________.

158. When a company has ________________, management must decide which products to

make and sell in order to maximize net income.

159. ___________________ refers to the relative proportion of fixed versus variable costs that

a company incurs.

160. The _________________________ provides a measure of a company’s earnings volatility

and can be used to compare companies.

a161. Under _____________________ all manufacturing costs are charged to, or absorbed by,

the product.

a162. Fixed manufacturing costs are treated as period costs under ______________________.

a163. When production exceeds sales, a portion of the _____________________ is deferred to

a future period as part of the cost of ending inventory under absorption costing, but not

under variable costing.

a164. When units produced exceed units sold, income under absorption costing is ___________

than income under variable costing.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

6 – 45

a165. Management may be tempted to overproduce in a given period in order to increase net

income if _______________ is used for internal decision making.

Answers to Completion Statements

SHORT-ANSWER ESSAY QUESTIONS

S-A E 166

A CVP income statement is frequently prepared for internal use by management. Describe the

features of the CVP income statement that make it more useful for management decision-making

than the traditional income statement that is prepared for external users.

S-A E 167

Nancy Sound, president of Crosley Corp., has heard about operating leverage and asks you to

explain this term. What is operating leverage? How does a company increase its operating

leverage?

Test Bank for Managerial Accounting, Seventh Edition

FOR INSTRUCTOR USE ONLY

6 – 46

aS-A E 168

Define variable costing and absorption costing. What are some of the benefits to a manager from

using variable costing instead of absorption costing for internal decision making?

aS-A E 169

How do differences in production and sales levels affect income under absorption and variable

costing?