FOR INSTRUCTOR USE ONLY

CHAPTER 6

INVENTORIES

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

True-False Statements

1.

1

C

8.

2

C

15.

3

K

a22.

7

C

sg29.

3

C

2.

1

C

9.

2

C

16.

3

C

a23.

7

K

sg30.

4

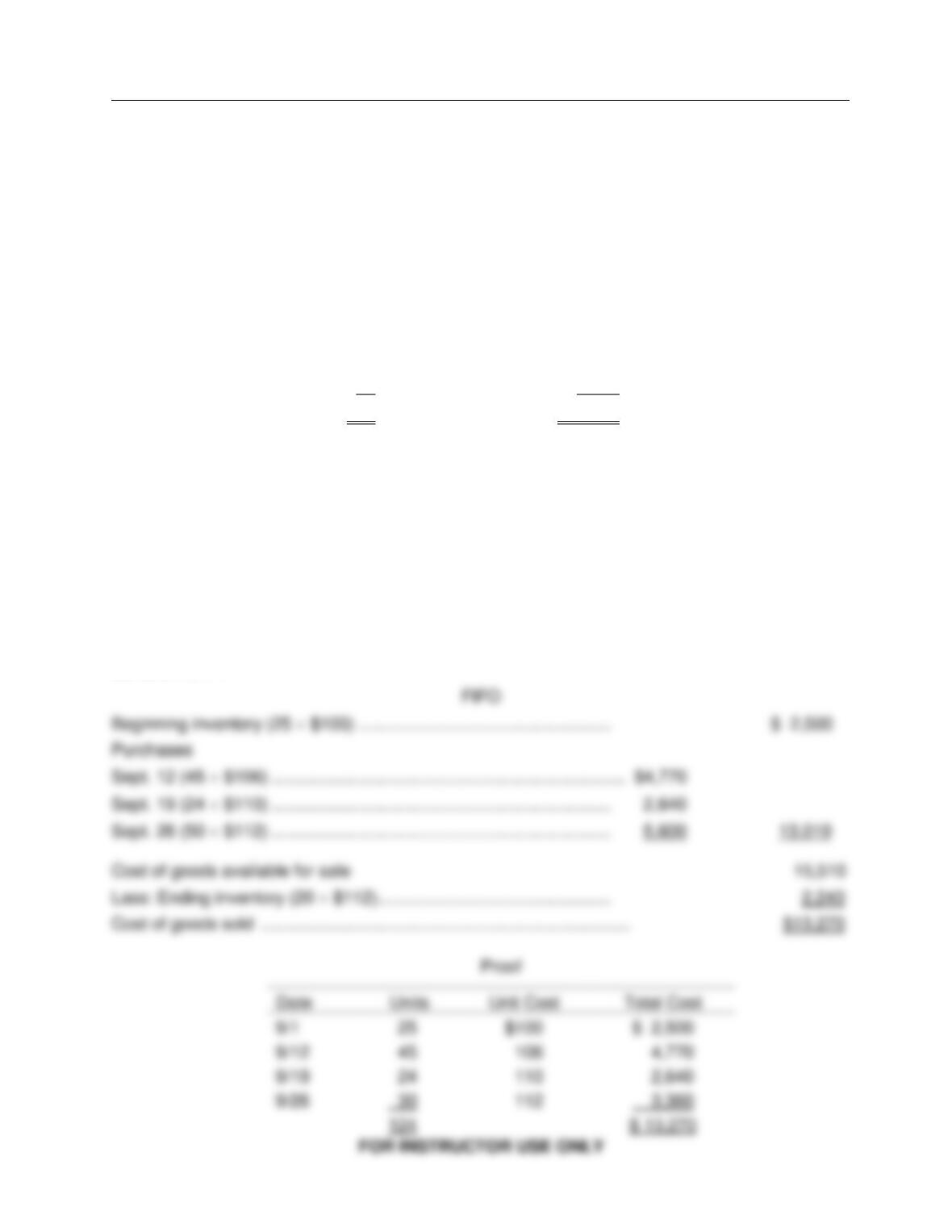

K

3.

1

K

10.

2

C

17.

4

K

a24.

8

K

sg31.

5

K

4.

1

K

11.

2

K

18.

4

K

a25.

8

K

sg,a32.

7

K

5.

1

K

12.

3

K

19.

5

C

sg26.

1

C

sg,a33.

8

K

6.

2

K

13.

3

K

20.

5

K

sg27.

2

K

7.

2

K

14.

3

K

21.

6

C

sg28.

2

K

Multiple Choice Questions

34.

1

K

64.

2

K

94.

2

AP

124.

5

C

st154.

3

K

35.

1

K

65.

2

AP

95.

2

AP

125.

5

C

sg155.

3

C

36.

1

K

66.

2

C

96.

2

AP

126.

5

AN

st156.

4

K

37.

1

K

67.

2

K

97.

3

AP

127.

5

AN

sg157.

5

AN

38.

1

K

68.

2

K

98.

3

AP

128.

5

AN

st158.

6

K

39.

1

K

69.

2

K

99.

3

AP

129.

5

C

sg,a159.

8

AP

40.

1

C

70.

2

K

100.

3

AP

130.

6

K

160.

9

K

41.

1

C

71.

2

C

101.

3

K

131.

6

K

161.

9

K

42.

1

C

72.

2

C

102.

3

C

132.

6

AP

162.

9

K

43.

1

K

73.

2

K

103.

3

C

133.

6

AP

163.

9

K

44.

1

C

74.

2

K

104.

3

C

134.

6

AP

164.

9

K

45.

1

C

75.

2

AP

105.

3

C

135.

6

AP

165.

9

K

46.

1

K

76.

2

AP

106.

2

K

a136.

7

AP

166.

9

K

47.

1

K

77.

3

AP

107.

2

K

a137.

7

AP

167.

9

K

48.

1

C

78.

2

AP

108.

3

C

a138.

7

AP

168.

9

K

49.

2

AP

79.

2

AP

109.

3

K

a139.

7

AP

169.

9

K

50.

2

AP

80.

2

AP

110.

3

K

a140.

7

AP

170.

9

K

51.

2

AP

81.

3

AP

111.

3

C

a141.

7

C

171.

9

K

52.

2

K

82.

2

AP

112.

3

AP

a142.

7

C

172.

9

K

53.

2

C

83.

2

AP

113.

3

AN

a143.

7

AP

173.

9

K

54.

2

C

84.

2

AP

114.

3

AN

a144.

8

C

174.

9

K

55.

2

AP

85.

2

AP

115.

3

K

a145.

8

C

175.

9

K

56.

2

K

86.

3

AP

116.

4

K

a146.

8

C

176.

9

K

57.

2

AP

87.

3

AP

117.

4

K

a147.

8

AP

177.

9

K

58.

2

AP

88.

2

AP

118.

4

K

a148.

8

AP

178.

9

K

59.

2

AP

89.

2

AP

119.

4

K

a149.

8

AP

179.

9

K

60.

2

AP

90.

2

AP

120.

4

K

st150.

1

K

61.

2

AP

91.

2

AP

121.

4

AP

sg151.

1

K

62.

2

C

92.

2

AP

122.

4

AP

st152.

2

K

63.

2

K

93.

2

AP

123.

4

AP

sg153.

2

AP

sg This question also appears in the Study Guide.

st This question also appears in a self-test at the student companion website.

a This question covers a topic in an appendix to the chapter.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

6 – 2

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Brief Exercises

180.

1

C

182.

2

AP

184.

2

AP

186.

2

K

188.

5

C

181.

2

AP

183.

2

AP

185.

2

AP

187.

4

AP

189.

6

AP

Exercises

190.

2

AP

196.

2

AP

202.

4

AP

208.

6

AP

a214.

8

AP

191.

2

AP

197.

3

AP

203.

3.

5

AN

209.

6

AP

a215.

8

AP

192.

2

AN

198.

3

E

204.

9.

5

AP

a210.

7

AP

193.

2

AP

199.

4

AN

205.

5

AN

a211.

7

AP

194.

2

AP

200.

4

AP

206.

5

AN

a212.

8

AP

195.

2

AP

201.

4

AP

207.

5

AN

a213.

8

AP

Completion Statements

216.

1

K

218.

2

K

220.

2

K

222.

3

K

224.

6

K

217.

1

K

219.

2

K

221.

3

K

223.

4

K

a225.

8

K

Matching Statements

226.

6

K

Short-Answer Essay

227.

2

K

229.

5

K

231.

3

233.

5

K

228.

3

K

230.

3

K

232.

4

234.

5

K

SUMMARY OF LEARNING OBJECTIVES BY QUESTION TYPE

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Learning Objective 1

1.

TF

5.

TF

36.

MC

40.

MC

44.

MC

48.

MC

216.

C

2.

TF

26.

TF

37.

MC

41.

MC

45.

MC

150.

MC

217.

C

3.

TF

34.

MC

38.

MC

42.

MC

46.

MC

151.

MC

4.

TF

35.

MC

39.

MC

43.

MC

47.

MC

180.

BE

Learning Objective 2

6.

TF

52.

MC

63.

MC

74.

MC

89.

MC

153.

MC

194.

Ex

7.

TF

53.

MC

64.

MC

75.

MC

90.

MC

181.

BE

195.

Ex

8.

TF

54.

MC

65.

MC

76.

MC

91.

MC

182.

BE

196.

Ex

9.

TF

55.

MC

66.

MC

78.

MC

92.

MC

183.

BE

218.

C

10.

TF

56.

MC

67.

MC

79.

MC

93.

MC

184.

BE

219.

C

11.

TF

57.

MC

68.

MC

80.

MC

94.

MC

185.

BE

220.

C

27.

TF

58.

MC

69.

MC

82.

MC

95.

MC

186.

BE

227.

SA

28.

TF

59.

MC

70.

MC

83.

MC

96.

MC

190.

Ex

49.

MC

60.

MC

71.

MC

84.

MC

106.

MC

191.

Ex

50.

MC

61.

MC

72.

MC

85.

MC

107.

MC

192.

Ex

51.

MC

62.

MC

73.

MC

88.

MC

152.

MC

193.

Ex

Learning Objective 3

12.

TF

77.

MC

99.

MC

105.

MC

113.

MC

198.

Ex

13.

TF

81.

MC

100.

MC

108.

MC

114.

MC

221.

C

14.

TF

86.

MC

101.

MC

109.

MC

115.

MC

222.

C

15.

TF

87.

MC

102.

MC

110.

MC

154.

MC

228.

SA

16.

TF

97.

MC

103.

MC

111.

MC

155.

MC

230.

SA

29.

TF

98.

MC

104.

MC

112.

MC

197.

Ex

231.

SA

Inventories

FOR INSTRUCTOR USE ONLY

6 – 3

SUMMARY OF LEARNING OBJECTIVES BY QUESTION TYPE

Learning Objective 4

17.

TF

116.

MC

119.

MC

122.

MC

187.

BE

201.

Ex

232.

SA

18.

TF

117.

MC

120.

MC

123.

MC

199.

Ex

202.

Ex

30.

TF

118.

MC

121.

MC

156.

MC

200.

Ex

223.

C

Learning Objective 5

19.

TF

124.

MC

127.

MC

157.

MC

204.

Ex

207.

Ex

234.

SA

20.

TF

125.

MC

128.

MC

188.

BE

205.

Ex

229.

SA

31.

TF

126.

MC

129.

MC

203.

Ex

206.

Ex

233.

SA

Learning Objective 6

21.

TF

131.

MC

133.

MC

135.

MC

189.

BE

209.

Ex

130.

MC

132.

MC

134.

MC

158.

MC

208.

Ex

224.

C

Learning Objective a7

a22.

TF

a32.

TF

a137.

MC

a139.

MC

a141.

MC

a143.

MC

a211.

Ex

a23.

TF

a136.

MC

a138.

MC

a140.

MC

a142.

MC

a210.

Ex

Learning Objective a8

a24.

TF

a146.

MC

160.

MC

165.

MC

170.

MC

175.

MC

a212.

Ex

a25.

TF

a147.

MC

161.

MC

166.

MC

171.

MC

176.

MC

a213.

Ex

a33.

TF

a148.

MC

162.

MC

167.

MC

172.

MC

177.

MC

a214.

Ex

a144.

MC

a149.

MC

163.

MC

168.

MC

173.

MC

178.

MC

a215.

Ex

a145.

MC

a159.

MC

164.

MC

169.

MC

174.

MC

179.

MC

a225.

C

Note: TF = True-False BE = Brief Exercise C = Completion

MC = Multiple Choice Ex = Exercise MA = Matching

SA = Short-Answer Essay

CHAPTER LEARNING OBJECTIVES

1. Determine how to classify inventory and inventory quantities. Merchandisers need only

one inventory classification, merchandise inventory, to describe the different items that make

up total inventory. Manufacturers, on the other hand, usually classify inventory into three

categories: finished goods, work in process, and raw materials. To determine inventory

quantities, manufacturers (1) take physical inventory of goods on hand and (2) determine the

ownership of goods in transit or on consignment.

2. Explain the accounting for inventories and apply the inventory cost flow methods. The

primary basis of accounting for inventories is cost. Cost of goods available for sale includes

(a) cost of beginning inventory and (b) the cost of goods purchased. The inventory cost flow

methods are specific identification, and three assumed cost flow methods—FIFO, LIFO, and

average-cost.

3. Explain the financial effects of the inventory cost flow assumptions. Companies may

allocate the cost of goods available for sale to cost of goods sold and ending inventory by

specific identification or by a method based on an assumed cost flow. When prices are rising,

the first-in, first-out (FIFO) method results in lower cost of goods sold and higher net income

than the other methods. The reverse is true when prices are falling. In the balance sheet,

FIFO results in an ending inventory that is closest to current value. Inventory under LIFO is

the farthest from current value. LIFO results in the lowest income taxes.

Test Bank for Financial Accounting, Ninth Edition

6 – 4

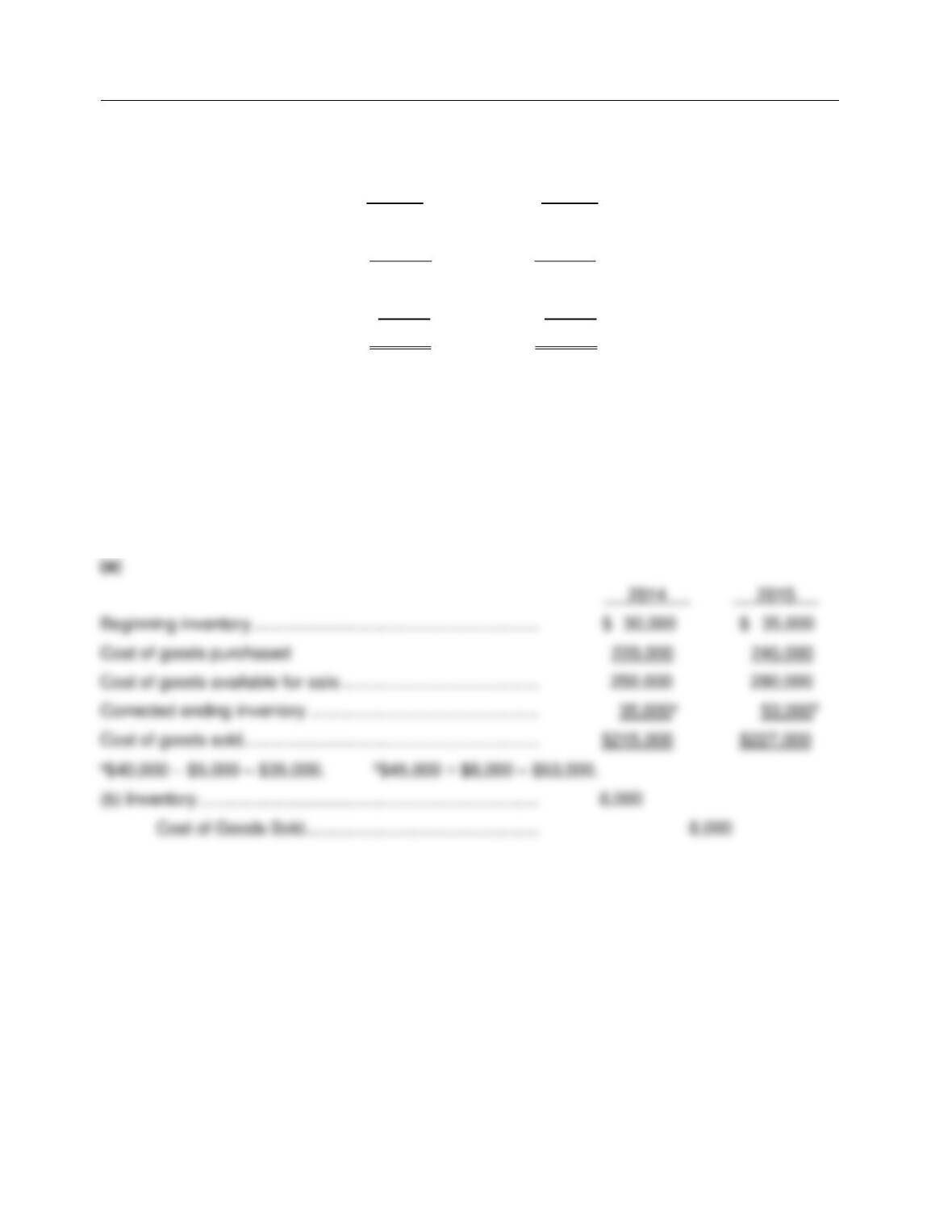

4. Explain the lower-of-cost-or-market basis of accounting for inventories. Companies use

the lower-of-cost-or-market (LCM) basis when the current replacement cost (market) is less

than cost. Under LCM, companies recognize the loss in the period in which the price decline

occurs.

5. Indicate the effects of inventory errors on the financial statements. In the income

statement of the current year: (a) An error in beginning inventory will have a reverse effect on

net income. (b) An error in ending inventory will have a similar effect on net income. In the

following period, its effect on net income for that period is reversed, and total net income for

the two years will be correct. In the balance sheet: Ending inventory errors will have the

same effect on total assets and total stockholder’s equity and no effect on liabilities.

6. Discuss the presentation and analysis of inventory. Inventory is classified in the balance

sheet as a current asset immediately below receivables. There also should be disclosure of

(1) the major inventory classifications,(2) the basis of accounting, and (3) the cost method.

The inventory turnover is cost of goods sold divided by average inventory. To convert it to

average days in inventory, divide 365 days by the inventory turnover.

a7. Apply the inventory cost flow methods to perpetual inventory records. Under FIFO and

a perpetual inventory system, companies charge to cost of goods sold the cost of the earliest

goods on hand prior to each sale. Under LIFO and a perpetual system, companies charge to

cost of goods sold the cost of the most recent purchase prior to sale. Under the moving–

average (average cost) method and a perpetual system, companies compute a new average

cost after each purchase.

a8. Describe the two methods of estimating inventories. The two methods of estimating

inventories are the gross profit method and the retail inventory method. Under the gross

profit method, companies apply a gross profit rate to net sales to determine estimated cost of

goods sold. They then subtract estimated cost of goods sold from cost of goods available for

sale to determine the estimated cost of the ending inventory. Under the retail inventory

method, companies compute a cost-to-retail ratio by dividing the cost of goods available for

sale by the retail value of the goods available for sale. They then apply this ratio to the

ending inventory at retail to determine the estimated cost of the ending inventory.

TRUE-FALSE STATEMENTS

1. Transactions that affect inventories on hand have an effect on both the balance sheet and

the income statement.

2. The more inventory a company has in stock, the greater the company’s profit.

3. Raw materials inventories are the goods that a manufacturer has completed and are

ready to be sold to customers.

Inventories

6 – 5

4. Goods that have been purchased FOB destination but are in transit, should be excluded

from a physical count of goods.

Test Bank for Financial Accounting, Ninth Edition

6 – 6

5. Goods out on consignment should be included in the inventory of the consignor.

6. The specific identification method of costing inventories tracks the actual physical flow of

the goods available for sale.

7. Management may choose any inventory costing method it desires as long as the cost flow

assumption chosen is consistent with the physical movement of goods in the company.

8. The first-in, first-out (FIFO) inventory method results in an ending inventory valued at the

most recent cost.

9. The expense recognition principle requires that the cost of goods sold be matched against

the ending merchandise inventory in order to determine income.

10. The specific identification method of inventory valuation is desirable when a company

sells a large number of low-unit cost items.

11. If a company has no beginning inventory and the unit cost of inventory items does not

change during the year, the value assigned to the ending inventory will be the same under

LIFO and average cost flow assumptions.

12. If the unit price of inventory is increasing during a period, a company using the LIFO

inventory method will show less gross profit for the period, than if it had used the FIFO

inventory method.

13. If a company has no beginning inventory and the unit price of inventory is increasing

during a period, the cost of goods available for sale during the period will be the same

under the LIFO and FIFO inventory methods.

14. A company may use more than one inventory costing method concurrently.

15. Use of the LIFO inventory valuation method enables a company to report paper or

phantom profits.

Inventories

6 – 7

16. If a company changes its inventory valuation method, the effect of the change on net

income should be disclosed in the financial statements.

17. Under the lower-of-cost-or-market basis, market is defined as current replacement cost.

18. Accountants believe that the write down from cost to market should not be made in the

period in which the price decline occurs.

19. An error that overstates the ending inventory will also cause net income for the period to

be overstated.

20. If inventories are valued using the LIFO cost flow assumption, they should not be

classified as a current asset on the balance sheet.

21. Inventory turnover is calculated as cost of goods sold divided by ending inventory.

a22. If a company uses the FIFO cost flow assumption, the cost of goods sold for the period

will be the same under a perpetual or periodic inventory system.

a23. In applying the LIFO assumption in a perpetual inventory system, the cost of the units

most recently purchased prior to sale is allocated first to the units sold.

a24. Under generally accepted accounting principles, management has the choice of physically

counting inventory on hand at the end of the year or using the gross profit method to

estimate the ending inventory.

a25. The retail inventory method requires a company to value its inventory on the balance

sheet at retail prices.

26. Finished goods are a classification of inventory for a manufacturer that are completed and

ready for sale.

Test Bank for Financial Accounting, Ninth Edition

6 – 8

27. Under the FIFO method, the costs of the earliest units purchased are the first charged to

cost of goods sold.

28. The cost of goods available for sale consists of the beginning inventory plus the cost of

goods purchased.

29. In a period of falling prices, the LIFO method results in a lower cost of goods sold than the

FIFO method.

30. The lower-of-cost-or-market basis is an example of the accounting concept of

conservatism.

31. Inventories are reported in the current assets section of the balance sheet immediately

below receivables.

a32. In a perpetual inventory system, the cost of goods sold under the FIFO method is based

on the cost of the latest goods on hand during the period.

a33. The gross profit method is based on the assumption that the rate of gross profit remains

constant from one year to the next.

Reporting

Answers to True-False Statements

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

34. Inventories affect

a. only the balance sheet.

b. only the income statement.

c. both the balance sheet and the income statement.

d. neither the balance sheet nor the income statement.

Inventories

6 – 9

35. Inventory is

a. reported under the classification of Property, Plant, and Equipment on the balance

sheet.

b. often reported as a miscellaneous expense on the income statement.

c. reported as a current asset on the balance sheet.

d. generally valued at the price for which the goods can be sold.

36. Items waiting to be used in production are considered to be

a. raw materials.

b. work in progress.

c. finished goods.

d. merchandise inventory.

37. In a manufacturing business, inventory that is ready for sale is called

a. raw materials inventory.

b. work in process inventory.

c. finished goods inventory.

d. store supplies inventory.

38. The factor which determines whether or not goods should be included in a physical count

of inventory is

a. physical possession.

b. legal title.

c. management’s judgment.

d. whether or not the purchase price has been paid.

39. If goods in transit are shipped FOB destination

a. the seller has legal title to the goods until they are delivered.

b. the buyer has legal title to the goods until they are delivered.

c. the transportation company has legal title to the goods while the goods are in transit.

d. no one has legal title to the goods until they are delivered.

40. An auto manufacturer would classify vehicles in various stages of production as

a. finished goods.

b. merchandise inventory.

c. raw materials.

d. work in process.

Test Bank for Financial Accounting, Ninth Edition

6 – 10

41. Which of the following should be included in the physical inventory of a company?

a. Goods held on consignment from another company.

b. Goods in transit to another company shipped FOB shipping point.

c. Goods in transit from another company shipped FOB shipping point.

d. Goods in transit to or from another company shipped FOB shipping point.

42. Manufacturers usually classify inventory into all the following general categories except

a. work in process

b. finished goods

c. merchandise inventory

d. raw materials

43. Freight terms of FOB shipping point mean that the

a. seller must debit freight out.

b. buyer must bear the freight costs.

c. goods are placed free on board at the buyer‘s place of business.

d. seller must bear the freight costs.

44. For companies that use a perpetual inventory system, all of the following are purposes for

taking a physical inventory except

a. to check the accuracy of the records.

b. to determine the amount of wasted raw materials.

c. to determine losses due to employee theft.

d. to determine ownership of the goods.

45. Fetherston Company’s goods in transit at December 31 include:

sales made purchases made

(1) FOB destination (3) FOB destination

(2) FOB shipping point (4) FOB shipping point

Which items should be included in Fetherston’s inventory at December 31?

a. (2) and (3)

b. (1) and (4)

c. (1) and (3)

d. (2) and (4)

46. The term “FOB” denotes

a. free on board.

b. freight on board.

c. free only (to) buyer.

d. freight charge on buyer.

Inventories

6 – 11

47. Under a consignment arrangement, the

a. consignor has ownership until goods are sold to a customer.

b. consignor has ownership until goods are shipped to the consignee.

c. consignee has ownership when the goods are in the consignee’s possession.

d. consigned goods are included in the inventory of the consignee.

48. As a result of a thorough physical inventory, Horace Company determined that it had

inventory worth $320,000 at December 31, 2015. This count did not take into

consideration the following facts: Herschel Consignment currently has goods worth

$47,000 on its sales floor that belong to Horace but are being sold on consignment by

Herschel. The selling price of these goods is $75,000. Horace purchased $22,000 of

goods that were shipped on December 27, FOB destination, that will be received by

Horace on January 3. Determine the correct amount of inventory that Horace should

report.

a. $320,000.

b. $340,000.

c. $367,000.

d. $387,000.

49. Partridge Bookstore had 500 units on hand at January 1, costing $9 each. Purchases and

sales during the month of January were as follows:

Date Purchases Sales

Jan. 14 375 @ $14

17 250 @ $10

25 250 @ $11

29 260 @ $16

Partridge does not maintain perpetual inventory records. According to a physical count,

365 units were on hand at January 31.

The cost of the inventory at January 31, under the FIFO method is:

a. $3,285.

b. $3,650.

c. $3,900.

d. $4,015.

Test Bank for Financial Accounting, Ninth Edition

6 – 12

50. Partridge Bookstore had 500 units on hand at January 1, costing $9 each. Purchases and

sales during the month of January were as follows:

Date Purchases Sales

Jan. 14 375 @ $14

17 250 @ $10

25 250 @ $11

29 260 @ $16

Partridge does not maintain perpetual inventory records. According to a physical count,

365 units were on hand at January 31.

The cost of the inventory at January 31, under the LIFO method is:

a. $3,285.

b. $3,650.

c. $3,900.

d. $4,015.

51. Nick’s Place recorded the following data:

Units Unit

Date Received Sold On Hand Cost

1/1 Inventory 600 $2.50

1/8 Purchased 1,000 1,600 3.00

1/12 Sold 1,200 300

The weighted average unit cost of the inventory at January 31 is:

a. $2.50.

b. $2.75.

c. $2.81.

d. $3.400.

52. Inventoriable costs include all of the following except the

a. freight costs incurred when buying inventory.

b. costs of the purchasing and warehousing departments.

c. cost of the beginning inventory.

d. cost of goods purchased.

53. Beginning inventory plus the cost of goods purchased equals

a. cost of goods sold.

b. cost of goods available for sale.

c. net purchases.

d. total goods purchased.

Inventories

6 – 13

54. Cost of goods sold is computed from the following equation:

a. beginning inventory – cost of goods purchased + ending inventory.

b. sales – cost of goods purchased + beginning inventory – ending inventory.

c. sales + gross profit – ending inventory + beginning inventory.

d. beginning inventory + cost of goods purchased – ending inventory.

55. A company just starting in business purchased three merchandise inventory items at the

following prices. First purchase $64; Second purchase $76; Third purchase $68. If the

company sold two units for a total of $200 and used FIFO costing, the gross profit for the

period would be

a. $56.

b. $60.

c. $62.

d. $68.

56. The LIFO inventory method assumes that the cost of the latest units purchased are

a. the last to be allocated to cost of goods sold.

b. the first to be allocated to ending inventory.

c. the first to be allocated to cost of goods sold.

d. not allocated to cost of goods sold or ending inventory.

57. A company just starting business made the following four inventory purchases in June:

June 1 150 units $ 390

June 10 200 units 585

June 15 200 units 630

June 28 150 units 510

$2,115

A physical count of merchandise inventory on June 30 reveals that there are 250 units on

hand. Using the LIFO inventory method, the value of the ending inventory on June 30 is

a. $683.

b. $825.

c. $1,290.

d. $1,432.

Test Bank for Financial Accounting, Ninth Edition

6 – 14

58. A company just starting business made the following four inventory purchases in June:

June 1 150 units $ 390

June 10 200 units 585

June 15 200 units 630

June 28 150 units 510

$2,115

A physical count of merchandise inventory on June 30 reveals that there are 250 units on

hand. Using the FIFO inventory method, the amount allocated to cost of goods sold for

June is

a. $683.

b. $825.

c. $1,290.

d. $1,432.

59. A company just starting business made the following four inventory purchases in June:

June 1 150 units $ 390

June 10 200 units 585

June 15 200 units 630

June 28 150 units 510

$2,115

A physical count of merchandise inventory on June 30 reveals that there are 250 units on

hand. Using the average-cost method, the amount allocated to the ending inventory on

June 30 is

a. $683.

b. $755.

c. $825.

d. $1,360.

60. A company just starting business made the following four inventory purchases in June:

June 1 150 units $ 390

June 10 200 units 585

June 15 200 units 630

June 28 150 units 510

$2,115

A physical count of merchandise inventory on June 30 reveals that there are 250 units on

hand.

The inventory method which results in the highest gross profit for June is

a. the FIFO method.

b. the LIFO method.

c. the weighted average unit cost method.

d. not determinable.

Inventories

6 – 15

61. A company purchased inventory as follows:

150 units at $5

350 units at $6

The average unit cost for inventory is

a. $5.00.

b. $5.50.

c. $5.70.

d. $6.00.

62. Which of the following items will increase inventoriable costs for the buyer of goods?

a. Purchase returns and allowances granted by the seller

b. Purchase discounts taken by the purchaser

c. Freight charges paid by the seller

d. Freight charges paid by the purchaser

63. Inventoriable costs may be thought of as a pool of costs consisting of which two

elements?

a. The cost of beginning inventory and the cost of ending inventory

b. The cost of ending inventory and the cost of goods purchased during the year

c. The cost of beginning inventory and the cost of goods purchased during the year

d. The difference between the costs of goods purchased and the cost of goods sold

during the year

64. The cost of goods available for sale is allocated between

a. beginning inventory and ending inventory.

b. beginning inventory and cost of goods on hand.

c. ending inventory and cost of goods sold.

d. beginning inventory and cost of goods purchased.

65. Indrisano’s Used Cars uses the specific identification method of costing inventory. During

March, Indrisano purchased three cars for $12,000, $14,400, and $19,200, respectively.

During March, two cars are sold for a total of $34,600. Indrisano determines that at March

31, the $14,400 car is still on hand. What is Indrisano’s gross profit for March?

a. $1,000.

b. $3,400.

c. $4,200.

d. $8,200.

Test Bank for Financial Accounting, Ninth Edition

6 – 16

66. Of the following companies, which one would not likely employ the specific identification

method for inventory costing?

a. Music store specializing in organ sales

b. Farm implement dealership

c. Antique shop

d. Hardware store

67. A problem with the specific identification method is that

a. inventories can be reported at actual costs.

b. management can manipulate income.

c. matching is not achieved.

d. the lower-of-cost-or-market basis cannot be applied.

68. The selection of an appropriate inventory cost flow assumption for an individual company

is made by

a. the external auditors.

b. the SEC.

c. the internal auditors.

d. management.

69. Which one of the following inventory methods is often impractical to use?

a. Specific identification

b. LIFO

c. FIFO

d. Average cost

70. Which of the following is not a common cost flow assumption used in costing inventory?

a. First-in, first-out

b. Middle-in, first-out

c. Last-in, first-out

d. Average cost

71. The accounting principle that requires that the cost flow assumption be consistent with the

physical movement of goods is

a. called the expense recognition principle.

b. called the consistency principle.

c. nonexistent; that is, there is no accounting requirement.

d. called the physical flow assumption.

Inventories

6 – 17

72. Which of the following statements is true regarding inventory cost flow assumptions?

a. A company may use more than one costing method concurrently.

b. A company must comply with the method specified by industry standards.

c. A company must use the same method for domestic and foreign operations.

d. A company may never change its inventory costing method once it has chosen a

method.

73. Which of the following statements is correct with respect to inventories?

a. The FIFO method assumes that the costs of the earliest goods acquired are the last to

be sold.

b. It is generally good business management to sell the most recently acquired goods

first.

c. Under FIFO, the ending inventory is based on the latest units purchased.

d. FIFO seldom coincides with the actual physical flow of inventory.

74. The cost of goods available for sale is allocated to the cost of goods sold and the

a. beginning inventory.

b. ending inventory.

c. cost of goods purchased.

d. gross profit.

75. At May 1, 2015, Kibbee Company had beginning inventory consisting of 200 units with a

unit cost of $7. During May, the company purchased inventory as follows:

800 units at $7

600 units at $8

The company sold 1,000 units during the month for $12 per unit. Kibbee uses the average

cost method. The average cost per unit for May is

a. $7.000.

b. $7.375.

c. $7.500.

d. $8.000.

Test Bank for Financial Accounting, Ninth Edition

6 – 18

76. At May 1, 2015, Kibbee Company had beginning inventory consisting of 200 units with a

unit cost of $7. During May, the company purchased inventory as follows:

800 units at $7

600 units at $8

The company sold 1,000 units during the month for $12 per unit. Kibbee uses the average

cost method. The value of Kibbee’s inventory at May 31, 2015 is

a. $3,000.

b. $4,425.

c. $4,500.

d. $7,500.

77. At May 1, 2015, Kibbee Company had beginning inventory consisting of 200 units with a

unit cost of $7. During May, the company purchased inventory as follows:

800 units at $7

600 units at $8

The company sold 1,000 units during the month for $12 per unit. Kibbee uses the average

cost method. Kibbee’s gross profit for the month of May is

a. $4,625.

b. $4,571.

c. $4,000.

d. $4,500.

78. Effie Company uses a periodic inventory system. Details for the inventory account for the

month of January, 2015 are as follows:

Units Per unit price Total

Balance, 1/1/15 200 $5.00 $1,000

Purchase, 1/15/15 100 5.30 530

Purchase, 1/28/15 100 5.50 550

An end of the month (1/31/15) inventory showed that 160 units were on hand. How many

units did the company sell during January, 2015?

a. 60

b. 160

c. 200

d. 240

Inventories

6 – 19

79. Effie Company uses a periodic inventory system. Details for the inventory account for the

month of January, 2015 are as follows:

Units Per unit price Total

Balance, 1/1/15 200 $5.00 $1,000

Purchase, 1/15/15 100 5.30 530

Purchase, 1/28/15 100 5.50 550

An end of the month (1/31/15) inventory showed that 160 units were on hand. If the

company uses FIFO, what is the value of the ending inventory?

a. $800

b. $832

c. $848

d. $868

80. Effie Company uses a periodic inventory system. Details for the inventory account for the

month of January, 2015 are as follows:

Units Per unit price Total

Balance, 1/1/15 200 $5.00 $1,000

Purchase, 1/15/15 100 5.30 530

Purchase, 1/28/15 100 5.50 550

An end of the month (1/31/15) inventory showed that 160 units were on hand. If the

company uses LIFO, what is the value of the ending inventory?

a. $800

b. $832

c. $848

d. $868

81. Effie Company uses a periodic inventory system. Details for the inventory account for the

month of January, 2015 are as follows:

Units Per unit price Total

Balance, 1/1/15 200 $5.00 $1,000

Purchase, 1/15/15 100 5.30 530

Purchase, 1/28/15 100 5.50 550

An end of the month (1/31/15) inventory showed that 160 units were on hand. If the

company uses FIFO and sells the units for $10 each, what is the gross profit for the

month?

a. $1,120

b. $1,188

c. $1,532

d. $1,600

Test Bank for Financial Accounting, Ninth Edition

6 – 20

82. Eneri Company‘s inventory records show the following data:

Units Unit Cost

Inventory, January 1 10,000 $9.20

Purchases: June 18 9,000 8.00

November 8 6,000 7.00

A physical inventory on December 31 shows 4,000 units on hand. Eneri sells the units for

$13 each. The company has an effective tax rate of 20%. Eneri uses the periodic

inventory method.

Under the FIFO method, the December 31 inventory is valued at

a. $28,000.

b. $32,267.

c. $32,960.

d. $36,800.

83. Eneri Company‘s inventory records show the following data:

Units Unit Cost

Inventory, January 1 10,000 $9.20

Purchases: June 18 9,000 8.00

November 8 6,000 7.00

A physical inventory on December 31 shows 4,000 units on hand. Eneri sells the units for

$13 each. The company has an effective tax rate of 20%. Eneri uses the periodic

inventory method. What is the cost of goods available for sale?

a. $169,200

b. $178,000

c. $206,000

d. $325,000

84. Eneri Company‘s inventory records show the following data:

Units Unit Cost

Inventory, January 1 10,000 $9.20

Purchases: June 18 9,000 8.00

November 8 6,000 7.00

A physical inventory on December 31 shows 4,000 units on hand. Eneri sells the units for

$13 each. The company has an effective tax rate of 20%. Eneri uses the periodic

inventory method. Under the LIFO method, cost of goods sold is

a. $28,000.

b. $169,200.

c. $173,040.

d. $178,000.

Inventories

6 – 21

85. Eneri Company‘s inventory records show the following data:

Units Unit Cost

Inventory, January 1 10,000 $9.20

Purchases: June 18 9,000 8.00

November 8 6,000 7.00

A physical inventory on December 31 shows 4,000 units on hand. Eneri sells the units for

$13 each. The company has an effective tax rate of 20%. Eneri uses the periodic

inventory method. The weighted-average cost per unit is

a. $8.00.

b. $8.01.

c. $8.24.

d. $9.30.

86. Eneri Company‘s inventory records show the following data:

Units Unit Cost

Inventory, January 1 10,000 $9.20

Purchases: June 18 9,000 8.00

November 8 6,000 7.00

A physical inventory on December 31 shows 4,000 units on hand. Eneri sells the units for

$13 each. The company has an effective tax rate of 20%. Eneri uses the periodic

inventory method. If the company uses FIFO, what is the gross profit for the period?

a. $95,000

b. $99,266

c. $99,960

d. $103,800

87. Eneri Company‘s inventory records show the following data:

Units Unit Cost

Inventory, January 1 10,000 $9.20

Purchases: June 18 9,000 8.00

November 8 6,000 7.00

A physical inventory on December 31 shows 4,000 units on hand. Eneri sells the units for

$13 each. The company has an effective tax rate of 20%. Eneri uses the periodic

inventory method. What is the difference in taxes if LIFO rather than FIFO is used?

a. $1,760 additional taxes

b. $992 additional taxes

c. $786 additional taxes

d. $992 tax savings

Test Bank for Financial Accounting, Ninth Edition

6 – 22

88. Priscilla has the following inventory information.

July 1 Beginning Inventory 20 units at $19 $ 380

7 Purchases 70 units at $20 1,400

22 Purchases 10 units at $23 230

$2,010

A physical count of merchandise inventory on July 31 reveals that there are 35 units on

hand. Using the average-cost method, the value of ending inventory is

a. $680.

b. $704.

c. $723.

d. $730.

89. Priscilla has the following inventory information.

July 1 Beginning Inventory 20 units at $19 $ 380

7 Purchases 70 units at $20 1,400

22 Purchases 10 units at $23 230

$2,010

A physical count of merchandise inventory on July 31 reveals that there are 35 units on

hand. Using the FIFO inventory method, the amount allocated to cost of goods sold for

July is

a. $1,280.

b. $1,287

c. $1,306.

d. $1,330.

90. Priscilla has the following inventory information.

July 1 Beginning Inventory 20 units at $19 $ 380

7 Purchases 70 units at $20 1,400

22 Purchases 10 units at $23 230

$2,010

A physical count of merchandise inventory on July 31 reveals that there are 35 units on

hand. Using the LIFO inventory method, the amount allocated to cost of goods sold for

July is

a. $1,280.

b. $1,287.

c. $1,306.

d. $1,330.

Inventories

6 – 23

91. Moroni Industries has the following inventory information.

July 1 Beginning Inventory 40 units at $120

5 Purchases 240 units at $112

14 Sale 160 units

21 Purchases 120 units at $115

30 Sale 140 units

Assuming that a periodic inventory system is used, what is the amount allocated to ending

inventory on a LIFO basis?

a. $11,500

b. $11,520

c. $33,960

d. $33,980

92. Moroni Industries has the following inventory information.

July 1 Beginning Inventory 40 units at $120

5 Purchases 240 units at $112

14 Sale 160 units

21 Purchases 120 units at $115

30 Sale 140 units

Assuming that a periodic inventory system is used, what is the amount allocated to ending

inventory on a FIFO basis?

a. $11,500

b. $11,520

c. $33,960

d. $33,980

93. Netta Shutters has the following inventory information.

Nov. 1 Inventory 30 units @ $8.00

8 Purchase 120 units @ $8.30

17 Purchase 60 units @ $8.40

25 Purchase 90 units @ $8.80

A physical count of merchandise inventory on November 30 reveals that there are 90 units

on hand. Assume a periodic inventory system is used. Cost of goods sold (rounded to the

nearest dollar) under the average-cost method is

a. $1,740.

b. $1,772.

c. $1,778.

d. $1,794.

Test Bank for Financial Accounting, Ninth Edition

6 – 24

94. Netta Shutters has the following inventory information.

Nov. 1 Inventory 30 units @ $8.00

8 Purchase 120 units @ $8.30

17 Purchase 60 units @ $8.40

25 Purchase 90 units @ $8.80

A physical count of merchandise inventory on November 30 reveals that there are 90 units

on hand. Assume a periodic inventory system is used. Ending inventory under FIFO is

a. $738.

b. $792.

c. $1,740.

d. $1,794.

95. Netta Shutters has the following inventory information.

Nov. 1 Inventory 30 units @ $8.00

8 Purchase 120 units @ $8.30

17 Purchase 60 units @ $8.40

25 Purchase 90 units @ $8.80

A physical count of merchandise inventory on November 30 reveals that there are 90 units

on hand. Assume a periodic inventory system is used. Ending inventory under LIFO is

a. $738.

b. $792.

c. $1,740.

d. $1,794.

96. Netta Shutters has the following inventory information.

Nov. 1 Inventory 30 units @ $8.00

8 Purchase 120 units @ $8.30

17 Purchase 60 units @ $8.40

25 Purchase 90 units @ $8.80

A physical count of merchandise inventory on November 30 reveals that there are 90 units

on hand. Assume a periodic inventory system is used. Assuming that the specific

identification method is used and that ending inventory consists of 20 units from each of

the three purchases and 30 units from the November 1 inventory, cost of goods sold is

a. $1,740.

b. $1,772.

c. $1,782.

d. $1,794.

Inventories

6 – 25

97. Romanoff Industries had the following inventory transactions occur during 2015:

Units Cost/unit

2/1/15 Purchase 54 $45

3/14/15 Purchase 93 $47

5/1/15 Purchase 66 $49

The company sold 150 units at $70 each and has a tax rate of 30%. Assuming that a

periodic inventory system is used, what is the company’s gross profit using LIFO?

(rounded to whole dollars)

a. $3,318

b. $3,552

c. $6,948

d. $7,182

98. Romanoff Industries had the following inventory transactions occur during 2015:

Units Cost/unit

2/1/15 Purchase 54 $45

3/14/15 Purchase 93 $47

5/1/15 Purchase 66 $49

The company sold 150 units at $70 each and has a tax rate of 30%. Assuming that a

periodic inventory system is used, what is the company’s after-tax income using LIFO?

(rounded to whole dollars)

a. $2,323

b. $2,486

c. $3,318

d. $3,552

99. Romanoff Industries had the following inventory transactions occur during 2015:

Units Cost/unit

2/1/15 Purchase 54 $45

3/14/15 Purchase 93 $47

5/1/15 Purchase 66 $49

The company sold 150 units at $70 each and has a tax rate of 30%. Assuming that a

periodic inventory system is used, what is the company’s gross profit using FIFO?

(rounded to whole dollars)

a. $3,318

b. $3,552

c. $6,948

d. $7,182

Test Bank for Financial Accounting, Ninth Edition

6 – 26

100. Romanoff Industries had the following inventory transactions occur during 2015:

Units Cost/unit

2/1/15 Purchase 54 $45

3/14/15 Purchase 93 $47

5/1/15 Purchase 66 $49

The company sold 150 units at $70 each and has a tax rate of 30%. Assuming that a

periodic inventory system is used, what is the company’s after-tax income using FIFO?

(rounded to whole dollars)

a. $2,322

b. $2,486

c. $3,318

d. $3,552

101. Companies adopt different cost flow methods for each of the following reasons except

a. balance sheet effects.

b. cost effects.

c. income statements effects.

d. tax effects.

102. In periods of rising prices, the inventory method which results in the inventory value on the

balance sheet that is closest to current cost is the

a. FIFO method.

b. LIFO method.

c. average-cost method.

d. tax method.

103. Two companies report the same cost of goods available for sale but each employs a

different inventory costing method. If the price of goods has increased during the period,

then the company using

a. LIFO will have the highest ending inventory.

b. FIFO will have the highest cost of good sold.

c. FIFO will have the highest ending inventory.

d. LIFO will have the lowest cost of goods sold.

104. If companies have identical inventoriable costs but use different inventory flow

assumptions when the price of goods have not been constant, then the

a. cost of goods sold of the companies will be identical.

b. cost of goods available for sale of the companies will be identical.

c. ending inventory of the companies will be identical.

d. net income of the companies will be identical.

Inventories

6 – 27

105. In a period of increasing prices, which inventory flow assumption will result in the lowest

amount of income tax expense?

a. FIFO

b. LIFO

c. Average Cost

d. Income tax expense for the period will be the same under all assumptions.

106. The specific identification method of costing inventories is used when the

a. physical flow of units cannot be determined.

b. company sells large quantities of relatively low cost homogeneous items.

c. company sells large quantities of relatively low cost heterogeneous items.

d. company sells a limited quantity of high-unit cost items.

107. The specific identification method of inventory costing

a. always maximizes a company’s net income.

b. always minimizes a company’s net income.

c. has no effect on a company’s net income.

d. may enable management to manipulate net income.

108. The managers of Constantine Company receive performance bonuses based on the net

income of the firm. Which inventory costing method are they likely to favor in periods of

declining prices?

a. LIFO

b. Average Cost

c. FIFO

d. Physical inventory method

109. In periods of inflation, phantom or paper profits may be reported as a result of using the

a. perpetual inventory method.

b. FIFO costing assumption.

c. LIFO costing assumption.

d. periodic inventory method.

110. Selection of an inventory costing method by management does not usually depend on

a. the fiscal year end.

b. income statement effects.

c. balance sheet effects.

d. tax effects.

Test Bank for Financial Accounting, Ninth Edition

6 – 28

111. In a period of rising prices, the costs allocated to ending inventory may be understated in

the

a. average-cost method.

b. FIFO method.

c. gross profit method.

d. LIFO method.

112. The accountant at Almira Company is figuring out the difference in income taxes the

company will pay depending on the choice of either FIFO or LIFO as an inventory costing

method. The tax rate is 30% and the FIFO method will result in income before taxes of

$8,190. The LIFO method will result in income before taxes of $7,290. What is the

difference in tax that would be paid between the two methods?

a. $270.

b. $630.

c. $900.

d. Cannot be determined from the information provided.

113. The accountant at Cedric Company has determined that income before income taxes

amounted to $7,000 using the FIFO costing assumption. If the income tax rate is 30% and

the amount of income taxes paid would be $315 greater if the LIFO assumption were

used, what would be the amount of income before taxes under the LIFO assumption?

a. $5,950

b. $7,000

c. $7,315

d. $8,050

114. The manager of Brick Company is given a bonus based on income before income taxes.

Net income, after taxes, is $11,200 for FIFO and $9,800 for LIFO. The tax rate is 30%.

The bonus rate is 20%. How much higher is the manager’s bonus if FIFO is adopted

instead of LIFO?

a. $84

b. $2,800

c. $400

d. $420

115. The consistent application of an inventory costing method is essential for

a. conservatism.

b. accuracy.

c. comparability.

d. efficiency.

Inventories

6 – 29

116. Which costing method cannot be used to determine the cost of inventory items before

lower-of-cost-or-market is applied?

a. Specific identification

b. FIFO

c. LIFO

d. All of these methods can be used.

117. Inventory is reported in the financial statements at

a. cost.

b. market.

c. the higher-of-cost-or-market.

d. the lower-of-cost-or-market.

118. The lower-of-cost-or–market basis of valuing inventories is an example of

a. comparability.

b. the cost principle.

c. conservatism.

d. consistency.

119. Under the lower-of-cost-or-market basis in valuing inventory, market is defined as

a. current replacement cost.

b. selling price.

c. historical cost plus 10%.

d. selling price less markup.

120. The lower-of-cost-or-market (LCM) basis may be used with all of the following methods

except

a. average cost.

b. FIFO.

c. LIFO.

d. The LCM basis may be used with all of these.

Test Bank for Financial Accounting, Ninth Edition

6 – 30

121. Alfalfa Company developed the following information about its inventories in applying the

lower-of-cost-or-market (LCM) basis in valuing inventories:

Product Cost Market

A $112,000 $120,000

B 80,000 76,000

C 155,000 162,000

If Alfalfa applies the LCM basis, the value of the inventory reported on the balance sheet

would be

a. $343,000.

b. $347,000.

c. $358,000.

d. $362,000.

122. Switzer, Inc. has 8 computers which have been part of the inventory for over two years.

Each computer cost $600 and originally retailed for $900. At the statement date, each

computer has a current replacement cost of $400. What value should Switzer, Inc., have for

the computers at the end of the year?

a. $2,400.

b. $3,200.

c. $4,800.

d. $7,200.

123. Switzer, Inc. has 8 computers which have been part of the inventory for over two years.

Each computer cost $600 and originally retailed for $900. At the statement date, each

computer has a current replacement cost of $400. How much loss should Switzer, Inc.,

record for the year?

a. $1,600.

b. $2,400.

c. $3,200.

d. $4,000.

124. Othello Company understated its inventory by $20,000 at December 31, 2014. It did not

correct the error in 2014 or 2015. As a result, Othello’s stockholder’s equity was:

a. understated at December 31, 2014, and overstated at December 31, 2015.

b. understated at December 31, 2014, and properly stated at December 31, 2015.

c. overstated at December 31, 2014, and overstated at December 31, 2015.

d. understated at December 31, 2014, and understated at December 31, 2015.

Inventories

6 – 31

125. Understating beginning inventory will understate

a. assets.

b. cost of goods sold.

c. net income.

d. stockholder’s equity.

126. An error in the physical count of goods on hand at the end of a period resulted in a

$15,000 overstatement of the ending inventory. The effect of this error in the current

period is

Cost of Goods Sold Net Income

a. Understated Understated

b. Overstated Overstated

c. Understated Overstated

d. Overstated Understated

127. If beginning inventory is understated by $13,000, the effect of this error in the current

period is

Cost of Goods Sold Net Income

a. Understated Understated

b. Overstated Overstated

c. Understated Overstated

d. Overstated Understated

128. A company uses the periodic inventory method and the beginning inventory is overstated

by $7,000 because the ending inventory in the previous period was overstated by $7,000.

The amounts reflected in the current end of the period balance sheet are

Assets Stockholder’s Equity

a. Overstated Overstated

b. Correct Correct

c. Understated Understated

d. Overstated Correct

129. Overstating ending inventory will overstate all of the following except

a. assets.

b. cost of goods sold.

c. net income.

d. stockholder’s equity.

Test Bank for Financial Accounting, Ninth Edition

6 – 32

130. Disclosures about inventory should include each of the following except the

a. basis of accounting.

b. costing method.

c. quantity of inventory.

d. major inventory classifications.

131. Days in inventory is calculated by dividing

a. the inventory turnover by 365 days.

b. average inventory by 365 days.

c. 365 days by the inventory turnover.

d. 365 days by average inventory.

132. The following information is available for Everett Company at December 31, 2015:

beginning inventory $80,000; ending inventory $120,000; cost of goods sold $1,050,000;

and sales $1,800,000. Everett’s inventory turnover in 2015 is

a. 8.7 times.

b. 10.5 times.

c. 13.2 times.

d. 18 times.

133. The following information was available for Pete Company at December 31, 2015:

beginning inventory $90,000; ending inventory $70,000; cost of goods sold $984,000; and

sales $1,350,000. Pete’s inventory turnover in 2015 was

a. 10.9 times.

b. 12.3 times.

c. 14.1 times.

d. 16.9 times.

134. The following information was available for Pete Company at December 31, 2015:

beginning inventory $90,000; ending inventory $70,000; cost of goods sold $984,000; and

sales $1,350,000. Pete’s days in inventory in 2015 was

a 21.6 days.

b. 25.9 days.

c. 29.7 days.

d. 33.5 days.

Inventories

FOR INSTRUCTOR USE ONLY

6 – 33

135. Delmar Company had beginning inventory of $90,000, ending inventory of $110,000, cost

of goods sold of $600,000, and sales of $960,000. Delmar’s days in inventory is:

a 38.0 days.

b. 54.3 days.

c. 60.8 days.

d. 67.5 days.

a136. During July, the following purchases and sales were made by Big Dan Company. There

was no beginning inventory. Big Dan Company uses a perpetual inventory system.

Purchases Sales

July 3 40 units @ $12 July 13 50 units

11 40 units @ $13 22 20 units

20 20 units @ $15

Under the FIFO method, the cost of goods sold for each sale is:

July 13 July 22

a. $600 $240

b. 610 260

c. 650 260

d. 750 300

a137. During July, the following purchases and sales were made by Big Dan Company. There

was no beginning inventory. Big Dan Company uses a perpetual inventory system.

Purchases Sales

July 3 40 units @ $12 July 13 50 units

11 40 units @ $13 22 20 units

20 20 units @ $15

Under the LIFO method, the cost of goods sold for each sale is:

July 13 July 22

a. $600 $240

b. 640 300

c. 650 300

d. 750 260

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

6 – 34

a138. Pappy’s Staff has the following inventory information.

July 1 Beginning Inventory 20 units at $90

5 Purchases 120 units at $92

14 Sale 80 units

21 Purchases 60 units at $95

30 Sale 56 units

Assuming that a perpetual inventory system is used, what is the ending inventory on a

FIFO basis?

a. $5,848

b. $5,860

c. $6,068

d. $6,346

a139. Pappy’s Staff Junkets has the following inventory information.

July 1 Beginning Inventory 20 units at $90

5 Purchases 120 units at $92

14 Sale 80 units

21 Purchases 60 units at $95

30 Sale 56 units

Assuming that a perpetual inventory system is used, what is the ending inventory on a

LIFO basis?

a. $5,848

b. $5,860

c. $6,068

d. $6,346

a140. Langer Company has the following inventory information.

July 1 Beginning Inventory 10 units at $90

5 Purchases 60 units at $92

14 Sale 40 units

21 Purchases 30 units at $95

30 Sale 28 units

Assuming that a perpetual inventory system is used, what is the ending inventory (round

all calculations to nearest dollar) under the moving-average cost method?

a. $2,930

b. $2,966

c. $2,986

d. $3,054

Inventories

FOR INSTRUCTOR USE ONLY

6 – 35

141. A new average cost is computed each time a purchase is made in the

a. average-cost method.

b. moving-average cost method.

c. weighted-average cost method.

d. All of these choices are correct.

a142. When valuing ending inventory under a perpetual inventory system, the

a. valuation using the LIFO assumption is the same as the valuation using the LIFO

assumption under the periodic inventory system.

b. moving average requires that a new average be computed after every sale.

c. valuation using the FIFO assumption is the same as under the periodic inventory

system.

d. earliest units purchased during the period using the LIFO assumption are allocated to

the cost of goods sold when units are sold.

a143. Sawyer Company uses the perpetual inventory system and the moving-average method

to value inventories. On August 1, there were 10,000 units valued at $30,000 in the

beginning inventory. On August 10, 20,000 units were purchased for $6 per unit. On

August 15, 24,000 units were sold for $12 per unit. The amount charged to cost of goods

sold on August 15 was

a. $30,000.

b. $108,000.

c. $120,000.

d. $144,000.

a144. Under the gross profit method, each of the following items are estimated except for the

a. cost of ending inventory.

b. cost of goods sold.

c. cost of goods purchased.

d. gross profit.

a145. Under the retail inventory method, the estimated cost of ending inventory is computed by

multiplying the cost-to-retail ratio by

a. net sales.

b. goods available for sale at retail.

c. goods purchased at retail.

d. ending inventory at retail.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

6 – 36

a146. Inventories are estimated

a. more frequently under a periodic inventory system than a perpetual inventory system.

b. using the wholesale inventory method.

c. more frequently under a perpetual inventory system than the periodic inventory system.

d. using the net method.

a147. Clooney Department Store estimates inventory by using the retail inventory method. The

following information was developed:

At Cost At Retail

Beginning inventory $360,000 $ 750,000

Goods purchased 900,000 1,350,000

Net sales 1,400,000

The estimated cost of the ending inventory is

a. $280,000.

b. $336,000.

c. $420,000.

d. $466,667.

a148. Turturro Department Store utilizes the retail inventory method to estimate its inventories. It

calculated its cost to retail ratio during the period at 75%. Goods available for sale at retail

amounted to $600,000 and goods were sold during the period for $420,000. The

estimated cost of the ending inventory is

a. $135,000.

b. $180,000.

c. $315,000.

d. $450,000.

a149. TB Nelson Company prepares monthly financial statements and uses the gross profit

method to estimate ending inventories. Historically, the company has had a 40% gross

profit rate. During June, net sales amounted to $180,000; the beginning inventory on June

1 was $54,000; and the cost of goods purchased during June amounted to $90,000. The

estimated cost of TB Nelson Company‘s inventory on June 30 is

a. $21,600.

b. $36,000.

c. $72,000.

d. $126,000.

Inventories

6 – 37

150. Goods in transit should be included in the inventory of the buyer when the

a. public carrier accepts the goods from the seller.

b. goods reach the buyer.

c. terms of sale are FOB destination.

d. terms of sale are FOB shipping point.

151. Inventory items on an assembly line in various stages of production are classified as

a. Finished goods.

b. Work in process.

c. Raw materials.

d. Merchandise inventory.

152. The cost flow method that often parallels the actual physical flow of merchandise is the

a. FIFO method.

b. LIFO method.

c. average-cost method.

d. gross profit method.

153. Goodman Company’s inventory records show the following data:

Units Unit Cost

Inventory, January 1 10,000 $9.00

Purchases: June 18 9,000 8.20

November 8 6,000 7.00

A physical inventory on December 31 shows 6,000 units on hand. Under the FIFO

method, the December 31 inventory is

a. $42,000.

b. $49,200.

c. $49,392.

d. $54,000.

154. In a period of inflation, the cost flow method that results in the lowest income taxes is the

a. FIFO method.

b. LIFO method.

c. average-cost method.

d. gross profit method.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

6 – 38

155. In a period of rising prices, FIFO will have

a. lower net income than LIFO.

b. lower cost of goods sold than LIFO.

c. lower income tax expense than LIFO.

d. lower net purchases than LIFO.

156. Under the LCM approach, the market value is defined as

a. FIFO cost.

b. LIFO cost.

c. current replacement cost.

d. selling price.

157. Penny Company made an inventory count on December 31, 2015. During the count, one

of the clerks made the error of counting an inventory item twice. For the balance sheet at

December 31, 2015, the effects of this error are

Assets Liabilities Stockholder’s Equity

a. overstated understated overstated

b. understated no effect understated

c. overstated no effect overstated

d. overstated overstated understated

158. The inventory turnover is computed by dividing cost of goods sold by

a. beginning inventory.

b. ending inventory.

c. average inventory.

d. 365 days.

a159. H. Hunter Company’s records indicate the following information for the year:

Merchandise inventory, 1/1 $ 550,000

Purchases 2,250,000

Net sales 3,200,000

On December 31, a physical inventory determined that ending inventory of $500,000 was

in the warehouse. H. Hunter’s gross profit on sales has remained constant at 30%.

H. Hunter suspects some of the inventory may have been taken by some new employees.

At December 31, what is the estimated cost of missing inventory?

a. $60,000

b. $100,000

c. $150,000

d. $1,340,000

Inventories

6 – 39

160. The requirements for accounting for and reporting of inventories under IFRS, compared to

GAAP, tend to be more

a. detailed.

b. rules-based.

c. principles-based.

d. full of disclosure requirements.

161. The major IFRS requirements related to accounting for and reporting inventories are

a. the same as GAAP.

b. the same as GAAP with a couple of exceptions.

c. completely different from GAAP.

d. not comparable to GAAP.

162. Inventory accounting under IFRS differs from GAAP in regard to

a. neither the use of LIFO nor lower-of-cost-or-market.

b. the use of LIFO but not lower-of-cost-or-market.

c. the use of lower-of–cost-or-market but not LIFO.

d. the use of LIFO and lower-of-cost-or-market.

163. Under GAAP, companies can choose which inventory system?

LIFO FIFO

a. Yes No

b. Yes Yes

c. No Yes

d. Yes No

164. Under IFRS, companies can choose which inventory system?

LIFO FIFO

a. Yes No

b. Yes Yes

c. No Yes

d. No No

165. GAAP’s definition for inventory and provision of guidelines for inventory accounting, as

compared to IFRS are:

Definitions for Inventory Guideliness for inventory accounting

a. essentially similar more detailed

b. essentially different more detailed

c. essentially similar less detailed

d. essentially different less detailed

Test Bank for Financial Accounting, Ninth Edition

6 – 40

166. Inventories are defined by IFRS as

a. held-for-sale in the ordinary course of business.

b. in the process of production for sale in the ordinary course of business.

c. in the form of materials or supplies to be consumed in the production process or in the

providing of services.

d. All of these answers are correct.

167. Specific Identification can be used for inventory valuation under

GAAP IFRS

a. Yes No

b. Yes Yes

c. No No

d. No Yes

168. Specific Identification must be used for inventory valuation where the inventory items are

not interchangeable under

GAAP IFRS

a. Yes No

b. Yes Yes

c. No No

d. No Yes

169. GAAP’s provision for ownership of goods (goods–in–transit or consigned goods), as well

as which costs to include in inventory, as compared to IFRS are:

Ownership of goods Costs to include in inventory

a. essentially similar essentially similar

b. essentially different essentially different

c. essentially similar essentially different

d. essentially different essentially similar

170. The only acceptable cost flow assumptions under IFRS are

a. FIFO and LIFO.

b. FIFO and average.

c. LIFO and average.

d. FIFO, LIFO and average.

171. LIFO can be used

a. under neither GAAP nor IFRS.

b. under IFRS but not GAAP.

c. under GAAP but not IFRS.

d. under both GAAP and IFRS.

Inventories

6 – 41

172. The requirement that companies use the same cost flow assumption of all goods of a

similar nature is found in

GAAP IFRS

a. Yes No

b. Yes Yes

c. No No

d. No Yes

173. IFRS defines market for lower-of-cost-or market as

a. net realizable value.

b. estimated selling price in the ordinary course of business.

c. replacement cost.

d. replacement cost less costs of disposal.

174. GAAP defines market for lower-of-cost-or market essentially as

a. net realizable value.

b. estimated selling price in the ordinary course of business.

c. replacement cost.

d. replacement cost less costs of disposal.

175. Inventory written down under lower-of-cost-or market may be written back up to original

cost in a subsequent period under

GAAP IFRS

a. Yes No

b. Yes Yes

c. No No

d. No Yes

176. The option to value inventory at fair value exists under

GAAP IFRS

a. Yes No

b. Yes Yes

c. No No

d. No Yes

177. Certain agricultural and mineral products can be reported at net realizable value under

GAAP IFRS

a. Yes No

b. Yes Yes

c. No No

d. No Yes

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

6 – 42

178. The convergence issue that will be most difficult to resolve in the area of inventory

accounting is:

a. FIFO.

b. LIFO.

c. ownership of goods.

d. costs to include in inventory.

179. The specific identification method

a. cannot be used under GAAP.

b. cannot be used under IFRS.

c. must be used under IFRS if the inventory items can be specifically identified.

d. must be used under IFRS if it would result in the lowest net income.

Answers to Multiple Choice Questions

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Inventories

6 – 43

BRIEF EXERCISES

BE 180

Waegelein Company identifies the following items for possible inclusion in the physical inventory.

Indicate whether each item should be included or excluded from the inventory taking.

1. Goods shipped on consignment by Waegelein to another company.

2. Goods in transit from a supplier shipped FOB destination.

3. Goods shipped via common carrier to a customer with terms FOB shipping point.

4. Goods held on consignment from another company.

BE 181

In the first month of operations, Mordica Company made three purchases of merchandise in the

following sequence: (1) 200 units at $6, (2) 300 units at $7, and (3) 400 units at $9. Assuming

there are 300 units on hand, compute the cost of the ending inventory under (1) the FIFO method

and (2) the LIFO method. Mordica uses a periodic inventory system.

BE 182

Flaherty Company had beginning inventory on May 1 of $12,000. During the month, the company

made purchases of $40,000 but returned $2,000 of goods because they were defective. At the

end of the month, the inventory on hand was valued at $15,500.

Calculate cost of goods available for sale and cost of goods sold for the month.

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

6 – 44

BE 183

Shellhammer Company‘s inventory records show the following data for the month of September:

Units Unit Cost

Inventory, September 1 100 $3.34

Purchases: September 8 450 3.50

September 18 350 3.70

A physical inventory on September 30 shows 200 units on hand. Calculate the value of ending

inventory and cost of goods sold if the company uses FIFO inventory costing and a periodic

inventory system.

BE 184

Shellhammer Company’s inventory records show the following data for the month of September:

Units Unit Cost

Inventory, September 1 100 $3.34

Purchases: September 8 450 3.50

September 18 350 3.70

A physical inventory on September 30 shows 200 units on hand. Calculate the value of ending

inventory and cost of goods sold if the company uses LIFO inventory costing and a periodic

inventory system.

BE 185

Shellhammer Company’s inventory records show the following data for the month of September:

Units Unit Cost

Inventory, September 1 100 $3.34

Purchases: September 8 450 3.50

September 18 350 3.70

Inventories

FOR INSTRUCTOR USE ONLY

6 – 45

BE 185 (Cont.)

A physical inventory on September 30 shows 200 units on hand. Calculate the value of the

ending inventory and cost of goods sold if the company uses weighted average inventory costing

and a periodic inventory system. Round cost per unit to 2 decimal places and ending inventory

and cost of goods sold to the nearest dollar.

BE 186

The following accounts are included in the ledger of Wainwright Company:

Advertising expense

Freight-in

Inventory

Purchases

Purchase returns and allowances

Sales revenue

Sales returns and allowances

Which of the accounts would be included in calculating cost of goods sold?

BE 187

The Vogelson Company accumulates the following cost and market data at December 31.

Inventory Categories Cost Data Market Data

Camera $11,000 $9,900

Camcorders 7,800 8,500

DVDs 14,000 12,000

What is the lower-of-cost-or-market value of the inventory?

Test Bank for Financial Accounting, Ninth Edition

FOR INSTRUCTOR USE ONLY

6 – 46

$29,700

BE 188

Garner Supply Company reports net income of $120,000 in 2015. The ending inventory did not

include goods valued at $7,000 that Garner had consigned to Sharif’s Gift Shop.