Chapter 6: Accounting for Merchandising Businesses

169.

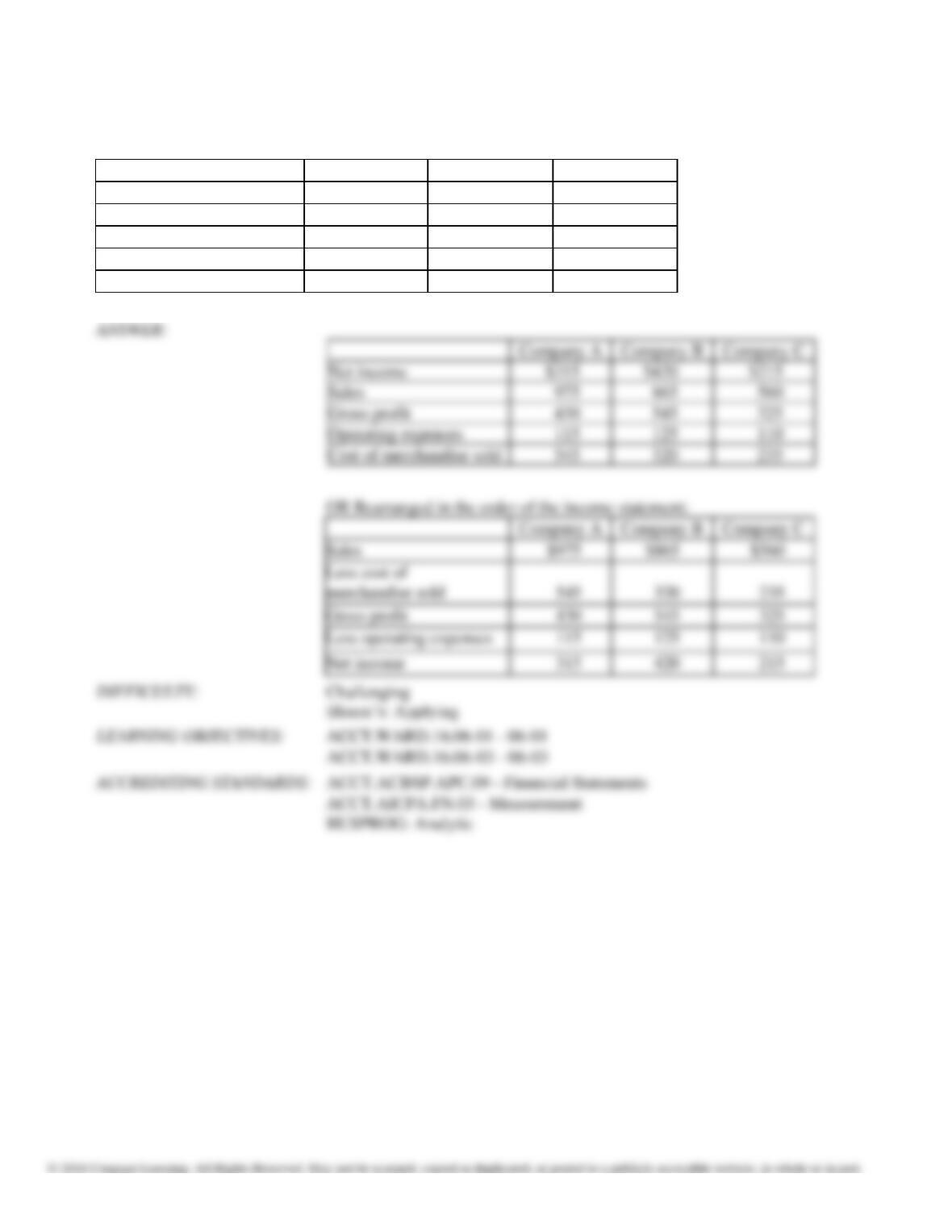

Complete the following data taken from the condensed income statements for merchandising Companies A, B,

and

C.

Company A

Company B

Company C

Net income

$315

$ ?

$215

Sales

?

865

560

Gross profit

430

?

325

Operating expenses

?

125

?

Cost of merchandise sold

545

320

?

Sales

Gross profit

Chapter 6: Accounting for Merchandising Businesses

170.

Complete the following data taken from the condensed income statements for merchandising Companies X, Y,

and

Z.

Company X

Company Y

Company Z

Net income (loss)

$220

$ ?

$( 70)

Sales

?

1,315

890

Gross profit

435

?

465

Operating expenses

?

565

?

Cost of merchandise sold

330

775

?

Sales

Gross profit

540

Less operating expenses

565

Net income or net loss

Chapter 6: Accounting for Merchandising Businesses

171.

During the current year, merchandise is sold for $137,500 cash and $425,600 on account. The cost of the

merchandise sold is $322,325. What is the amount of the gross profit?

172.

During the current year, merchandise is sold for $117,500 cash and $241,750 on account. The cost of the

merchandise sold is $157,400. What is the amount of the gross profit?

173.

During the current year, merchandise is sold for $86,000 cash and for $93,950 on account. The cost of

the

merchandise sold is $76,240. What is the amount of the gross profit?

Chapter 6: Accounting for Merchandising Businesses

174.

Travis Company purchased merchandise on account from a supplier for $5,700, terms 2/10, net 30.

Travis

Company paid for the merchandise within the discount period.

Under a perpetual inventory system, record the journal entries required for the above transactions.

175.

On March 25, Osgood Company sold merchandise on account, $10,000, terms n/30. The applicable sales

tax

percentage is 7.5%. Record the transaction.

Journal

Date

Description

Post.

Ref.

Debit

Credit

Chapter 6: Accounting for Merchandising Businesses

176.

On March 29, customers who owe $10,500 on account to Sonic Sales Company submit payments of

$4,250.

Journalize this event.

177.

Journalize the following merchandise transactions:

(a)

Sold merchandise on account, $17,300, with terms 2/10, net 30. The cost of

the

merchandise sold was $12,600.

(b)

Received payment within the discount period.

Chapter 6: Accounting for Merchandising Businesses

178.

Determine the amount to be paid in full settlement of each invoice, assuming that credit for returns and

allowances

was received prior to payment and that all invoices were paid within the discount period.

Merchandise

Freight Paid by

Seller

Freight Terms

Returns and

Allowances

(a)

$4,500

$140

FOB Shipping

Point,

2/10, net 30

$1,200

(b)

$7,650

$200

FOB Destination,

1/10, net 45

$450

Chapter 6: Accounting for Merchandising Businesses

179.

Sampson Co. sold merchandise to Batson Co. on account, $46,000, terms 2/15, net 45. The cost of the

merchandise sold is $38,500. The Batson Co. paid the invoice within the discount period. Prepare the entries

that

both Sampson and Batson Companies would record for the above. Assume both Sampson and Batson use a

perpetual inventory system.

180.

Which of the following costs would be included in merchandise inventory?

(a)

Purchase price

(b)

Insurance in transit FOB shipping point

(c)

Freight for delivery FOB shipping point

(d)

Repair due to negligence of receiving clerk

(e)

Receiving department employee salary

(f)

Cost of processing purchase orders

Chapter 6: Accounting for Merchandising Businesses

181.

On March 4, Micro Sales makes $4,850 in sales on bank credit cards which charge a 2.5% service charge and

deposits the funds into Micro Sales’ bank accounts at the end of the business day. Journalize the sales and

recognition of expense.

182.

Journalize the following transactions for Armour Inc. using both the periodic inventory system and the

perpetual

inventory system, presented in the side–by-side format of the form provided below.

Oct.7 Sold merchandise on credit to Rondo Distributors, terms n/30, the cost of the merchandise was $720.

Oct. 8 Purchased merchandise, $10,000, terms FOB shipping point, 2/15, n/30, with prepaid freight charges of

$525

added to the invoice.

PERIODIC INVENTORY PERPETUAL

INVENTORY

Description

DR

CR

|

Description

DR

CR

|

|

|

|

|

|

|

Chapter 6: Accounting for Merchandising Businesses

183.

What is the normal balance of the following accounts?

a.

Sales Tax Payable

b.

Merchandise Inventory

c.

Delivery Expense

d.

Cost of Merchandise Sold

e.

Customer Refunds Payable

f.

Estimated Returns Inventory

g.

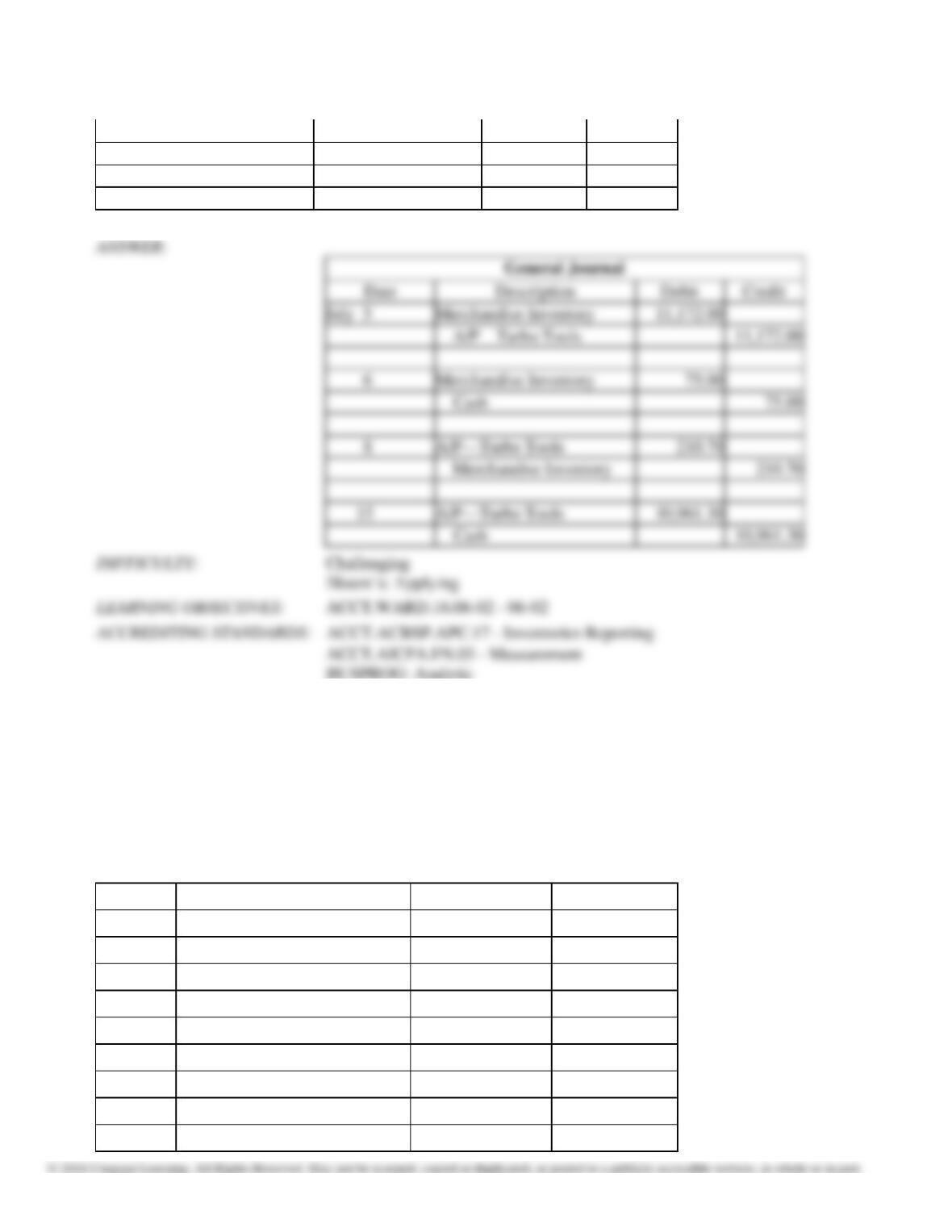

Sales

Chapter 6: Accounting for Merchandising Businesses

184.

For each of the following, calculate the cost of inventory reported on the balance sheet.

(a)

The total merchandise on hand at the end of the year as determined by taking a physical

inventory is $62,000. Of the $62,000, $8,000 has been sold FOB destination and is

awaiting

pickup by the carrier.

(b)

The total merchandise inventory counted at the end of the year was $63,000.

Excluded

from the count were purchases of $6,000 in transit under FOB shipping

point terms.

(c)

The total merchandise inventory counted at the end of the year was $75,000.

Excluded

from the count were purchases of $5,000 in transit under FOB destination

terms.

185.

Using the perpetual inventory system, journalize the entries for the following selected transactions:

(a)

Sold merchandise on account, for $12,000, terms n/30. The cost of the merchandise

sold

was $6,500.

(b)

Sold merchandise to customers who used MasterCard and VISA, $9,500. The cost of

the

merchandise sold was $5,300.

(c)

Sold merchandise to customers who used American Express, $2,900. The cost of the

merchandise sold was $1,700.

(d)

Paid an invoice from First National Bank for $385, representing a service fee for

processing

MasterCard and VISA sales.

(e)

Received $2,825 from American Express Company after a $75 collection fee had been

deducted.

Chapter 6: Accounting for Merchandising Businesses

186.

Merchandise with a list price of $4,200 and costing $2,300 is sold on account, subject to the following terms:

FOB

destination, 2/10, n/30. The seller prepays the freight costs of $85 (debit Delivery Expense for the freight

costs). Prior to payment for the goods, the seller issues a credit memo for $750 to the customer for merchandise

costing $425 that is returned. Payment is received within the discount period. The company uses a perpetual

inventory system.

Record the foregoing transactions of the seller in the sequence indicated below.

(a)

Sold the merchandise, recognizing the sale and cost of merchandise sold.

(b)

Paid the freight charges.

(c)

Issued the credit memo.

(d)

Received payment from the customer.

Chapter 6: Accounting for Merchandising Businesses

187.

Based on the information below, journalize the entries for the Seller and the Buyer. Both use a perpetual

inventory

system.

(a)

Seller sold merchandise on account to the buyer, $4,750, terms 2/10, net 30, FOB shipping

point. The cost of the merchandise is $2,850. The seller prepays the freight of $75.

(b)

Buyer returns $700 of merchandise as defective. The cost of the merchandise is $420.

(c)

Buyer pays within the discount period.

Seller Buyer

Description

DR

CR

Description

DR

CR

Chapter 6: Accounting for Merchandising Businesses

188.

Details of a purchase invoice and related credit memo are summarized as follows:

Invoice: Cost of merchandise listed on purchase invoice $6,500

Prepaid freight charge added to invoice 150

Terms, FOB shipping point, 1/10, n/eom

Credit memo: Cost of merchandise returned $1,500

Assume that the credit memo was received prior to payment and that the invoice is paid within the discount

period. Determine the following:

(a)

Amount of the cash discount allowed.

(b)

Amount to be paid by the purchaser if the discount is taken.

(c)

Cost of the merchandise to the purchaser if the discount is not taken.

189.

Conquest Company uses a perpetual inventory system. Conquest purchased $1,500 of merchandise on account

and

payment was made within the discount period. The credit terms were 2/10, n/30. Journalize Conquest’s

purchase

and payment.

Chapter 6: Accounting for Merchandising Businesses

190.

Merchandise with a list price of $4,700 is purchased on account, terms FOB shipping point, 1/10, n/30. The

seller

prepaid freight costs of $100. Prior to payment, $1,600 of the merchandise is returned. The invoice is paid

within

the discount period.

Record the foregoing transactions of the buyer in the sequence indicated below, assuming a perpetual

inventory

system is used.

(a)

Purchased the merchandise.

(b)

Recorded receipt of the credit memo for merchandise returned.

(c)

Paid the amount owed.

191.

Details of invoices for purchases of merchandise are as follows:

Returns and

Merchandise

Freight

Terms

Allowances

(a)

$2,800

$45

FOB shipping point, 1/10, n/30

$200

(b)

7,600

60

FOB destination, n/30

800

(c)

1,400

55

FOB shipping point, 2/10, n/30

600

(d)

500

50

FOB destination, 1/10, n/30

0

Determine the amount to be paid in full settlement of each of the invoices, assuming that credit for returns

and

allowances was received prior to payment and that all invoices were paid within the discount period.

Chapter 6: Accounting for Merchandising Businesses

192.

Journalize the entries to record the following selected transactions:

(a)

Sold $900 of merchandise on account, subject to 7% sales tax. The cost of the

merchandise sold was $510.

(b)

Paid $436 to the state sales tax department for taxes collected.

193.

Gadget Palace is a retailer selling unique hardware. Gadget Palace uses a perpetual inventory system. Journalize

the following transactions:

On July 5, Gadget Palace purchases inventory for sale from Turbo Tools for $11,400.00

with terms 2/10, n/30.

On July 6, Gadget Palace pays Fast Truck Transport $75 for freight in on the July 5

order.

On July 8, Gadget Palace receives a credit memo from Turbo Tools for $215.00 for

damaged merchandise.

On July 15, Gadget Palace pays Turbo Tools the balance due.

General Journal

Date

Description

Debit

Credit

Chapter 6: Accounting for Merchandising Businesses

194.

Marshall Supplies is a janitorial supply store that uses perpetual inventory. Journalize the following transactions:

On July 4, Marshall purchases inventory for sale from Tidy Wholesalers for $8,500.00

with terms 1/10, n/30.

On July 5, Marshall pays Express Transfer $45 for freight in on the July 4 order.

On July 7, Marshall buys an additional $11,985 in inventory from Tidy

Wholesalers

with terms 1/10, n/30.

On July 13, Marshall pays Tidy Wholesalers the balance due on both invoices

Journal

Date

Description

Debit

Credit

Chapter 6: Accounting for Merchandising Businesses

195.

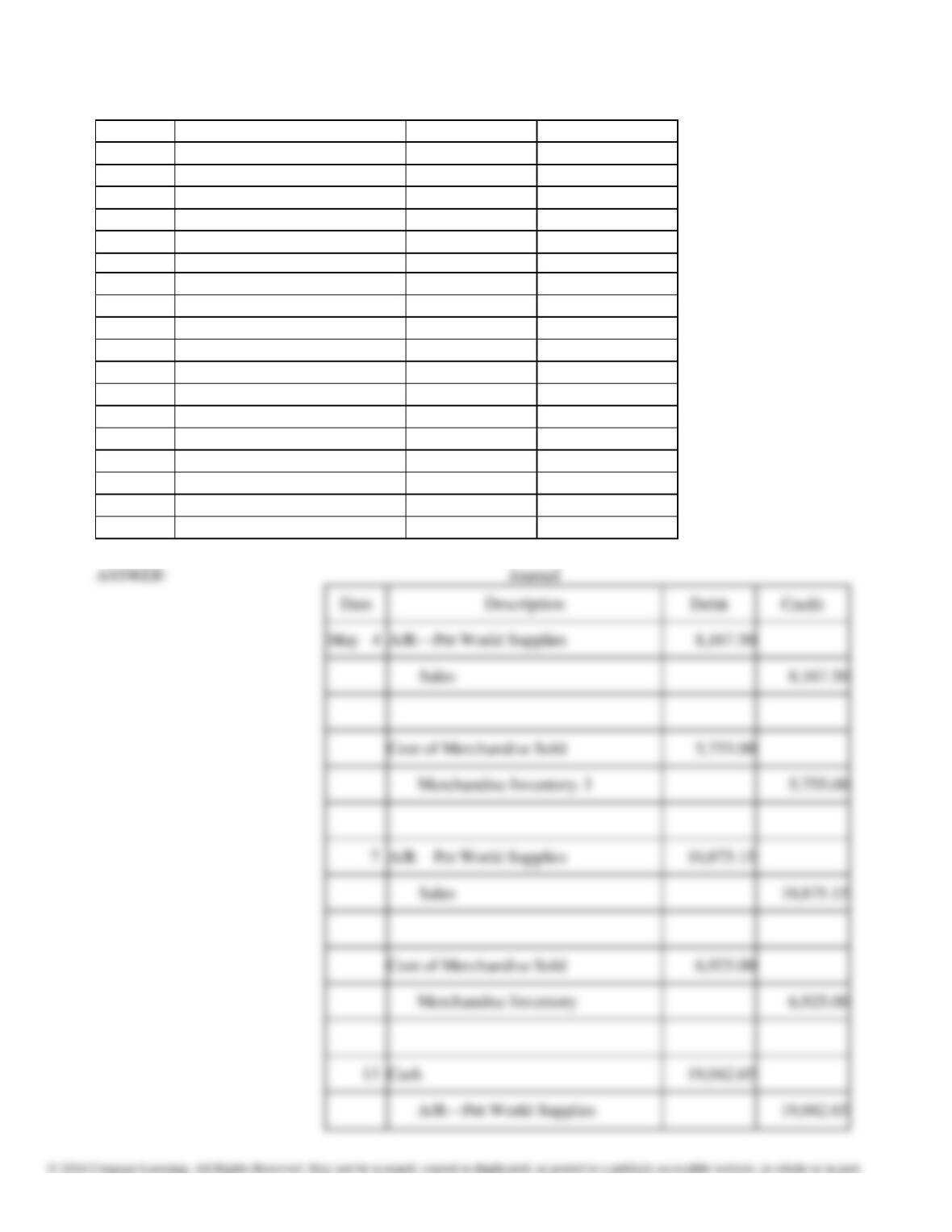

Bargain Wholesalers sells pet supplies to retailers including Pet World Supplies. Bargain Wholesalers uses

a

perpetual inventory. Journalize the following transactions:

May 4, Bargain Wholesalers sells inventory to Pet World Supplies for $8,250.00 with

terms 1/10, n/30. The cost of the merchandise is $5,755.00.

May 7, Bargain Wholesalers sells an additional $10,985 in inventory to Pet

World

Supplies with terms 1/10, n/30. The cost of the merchandise is $6,925.00.

May 13, Bargain Wholesalers receives a check from Pet World Supplies paying the

balance due on both invoices.

Chapter 6: Accounting for Merchandising Businesses

Journal

Date

Description

Debit

Credit

Chapter 6: Accounting for Merchandising Businesses

196.

On March 3, Bluebird Sales makes $4,350 in cash sales of general merchandise that has a cost of $1,512.

Bluebird

uses a perpetual inventory system.

(a)

Journalize the sale.

(b)

Journal the cost of merchandise sold.

197.

On March 5, Blowout Sales makes $22,500 in sales on the company’s own credit cards. The cost of merchandise

sold is $16,825. Journalize the sales and recognition of the cost of merchandise sold.

Chapter 6: Accounting for Merchandising Businesses

198.

On March 15, Monroe Sales sells $9,525 on account to Garrison Brewer with terms of 2/10, n/30. The cost of

merchandise sold was $6,905.

(a)

Journalize the sale and the recognition of the cost of the sale.

(b)

On March 20, a $125 credit memo is given to Garrison Brewer due to merchandise that was the wrong

color.

Journalize this event. The cost of the returned merchandise was $65.

(c)

On March 25, Garrison Brewer submits payment in full. Journalize this event.

199.

Journalize the following transactions assuming a perpetual inventory system:

May 5 Purchased merchandise from Archie Co., $6,000, terms FOB shipping point, 2/10, n/30.

Prepaid freight costs of $100 were added to the invoice.

12 Issued a debit memo to Archie Co. for $2,500 of merchandise returned from purchase on

May 5.

14 Paid Archie Co. for invoice of May 5, less debit memo of May 12 and discount.

Date

Description

Debit

Credit