Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-75

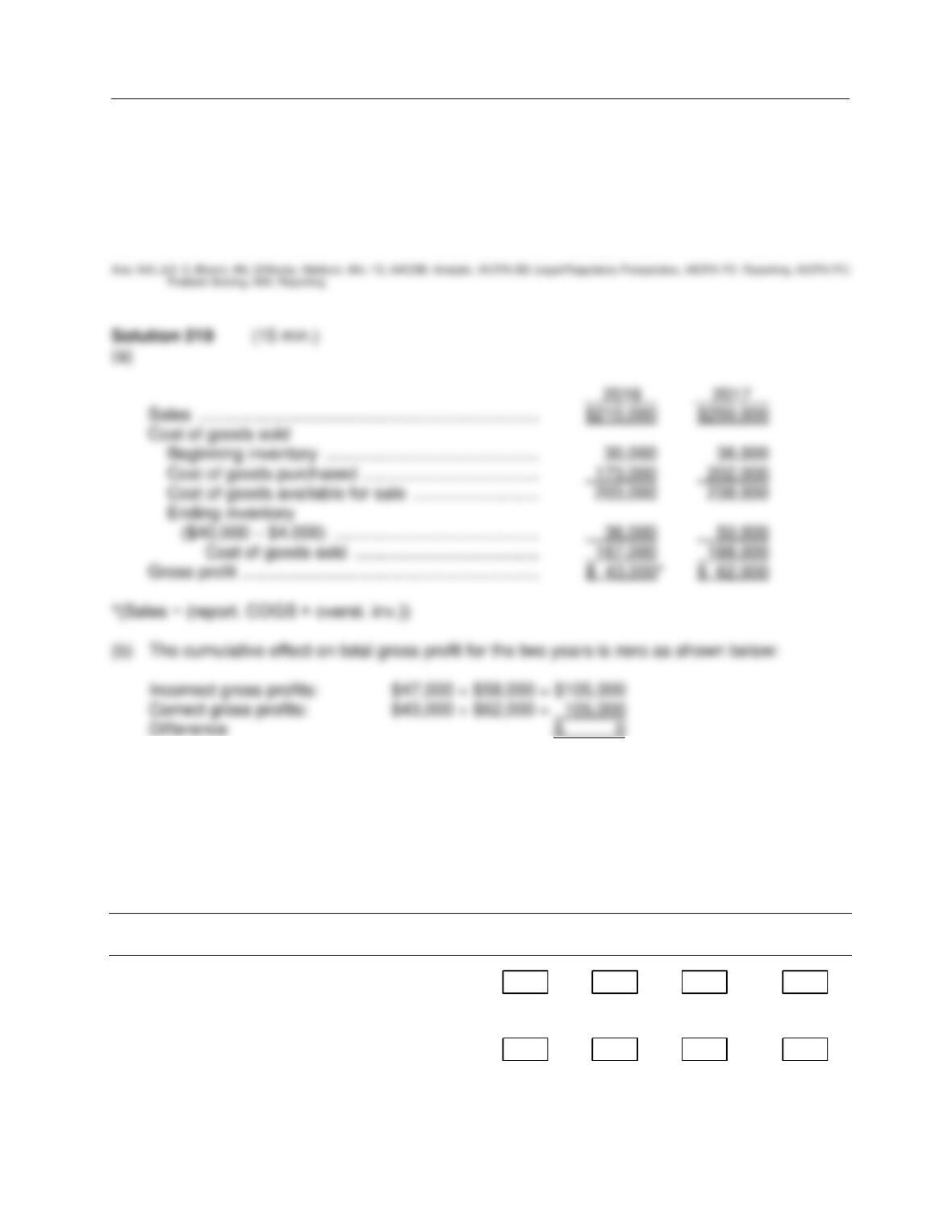

*Ex. 219 (Cont.)

Instructions

(a) Prepare correct income statement data for the 2 years.

(b) What is the cumulative effect of the inventory error on total gross profit for the 2 years?

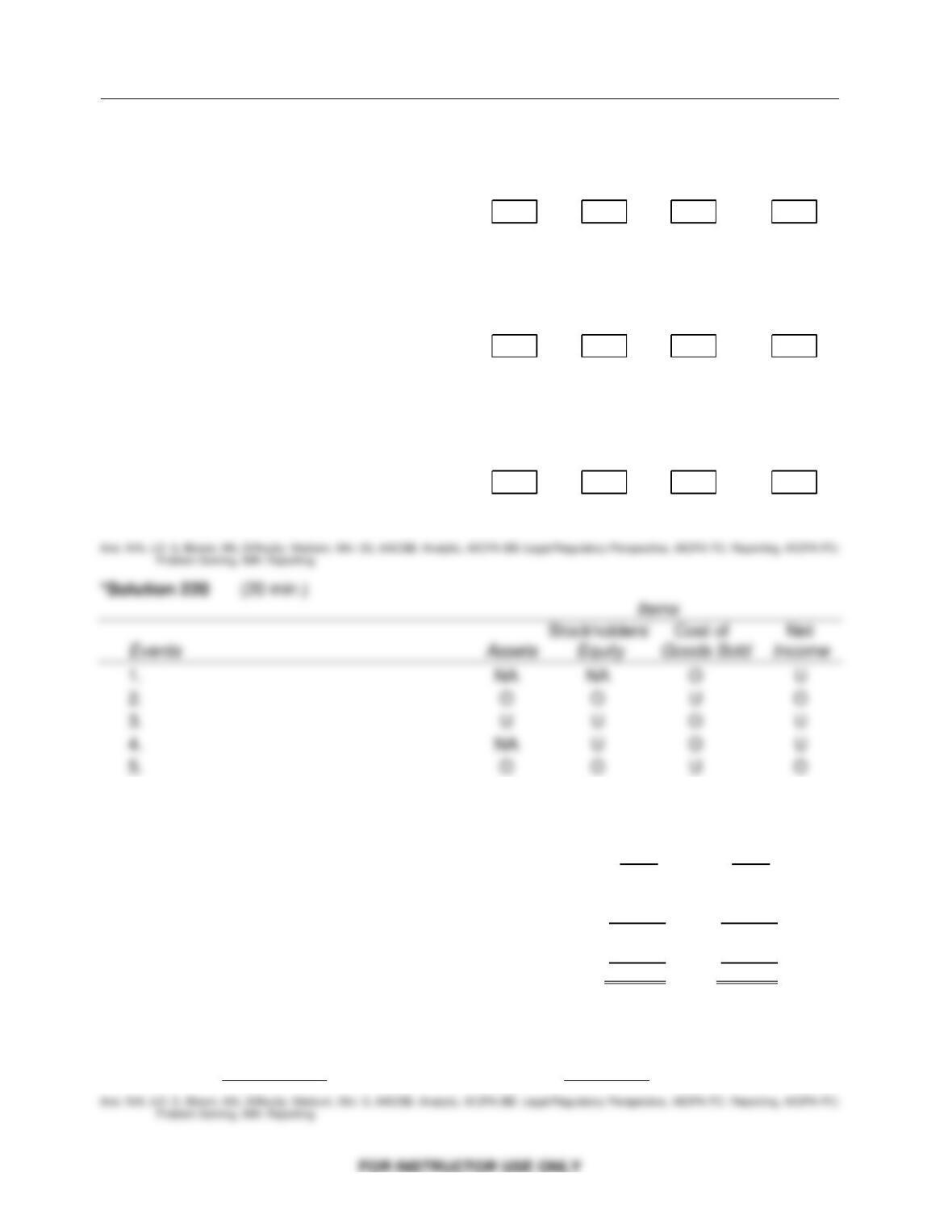

*Ex. 220

For each of the independent events listed below, analyze the impact on the indicated items at the

end of the current year by placing the appropriate code letter in the box under each item.

Code: O = item is overstated

U = item is understated

NA = item is not affected

Items

Stockholders’ Cost of Net

Events Assets Equity Goods Sold Income

1. The ending inventory in the previous period

was overstated.

_________________________________________________________________________________________________________________________

2. A physical count of goods on hand at the

end of the current year resulted in some

goods being counted twice.

_________________________________________________________________________________________________________________________

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

6-76

*Ex. 220 (Cont.)

3. Goods purchased on account in December

of the current year and shipped FOB

shipping point were recorded as purchases,

but were not included in the count of goods

on hand on December 31 because they had

not arrived by December 31.

_________________________________________________________________________________________________________________________

4. Goods purchased on account in December

of the current year and shipped FOB

destination were recorded as purchases, but

were not included in the count of goods on

hand on December 31 because they had not

arrived by December 31.

_________________________________________________________________________________________________________________________

5. The internal auditors discovered that the

ending inventory in the previous period was

understated $15,000 and that the ending

inventory in the current period was

overstated $25,000.

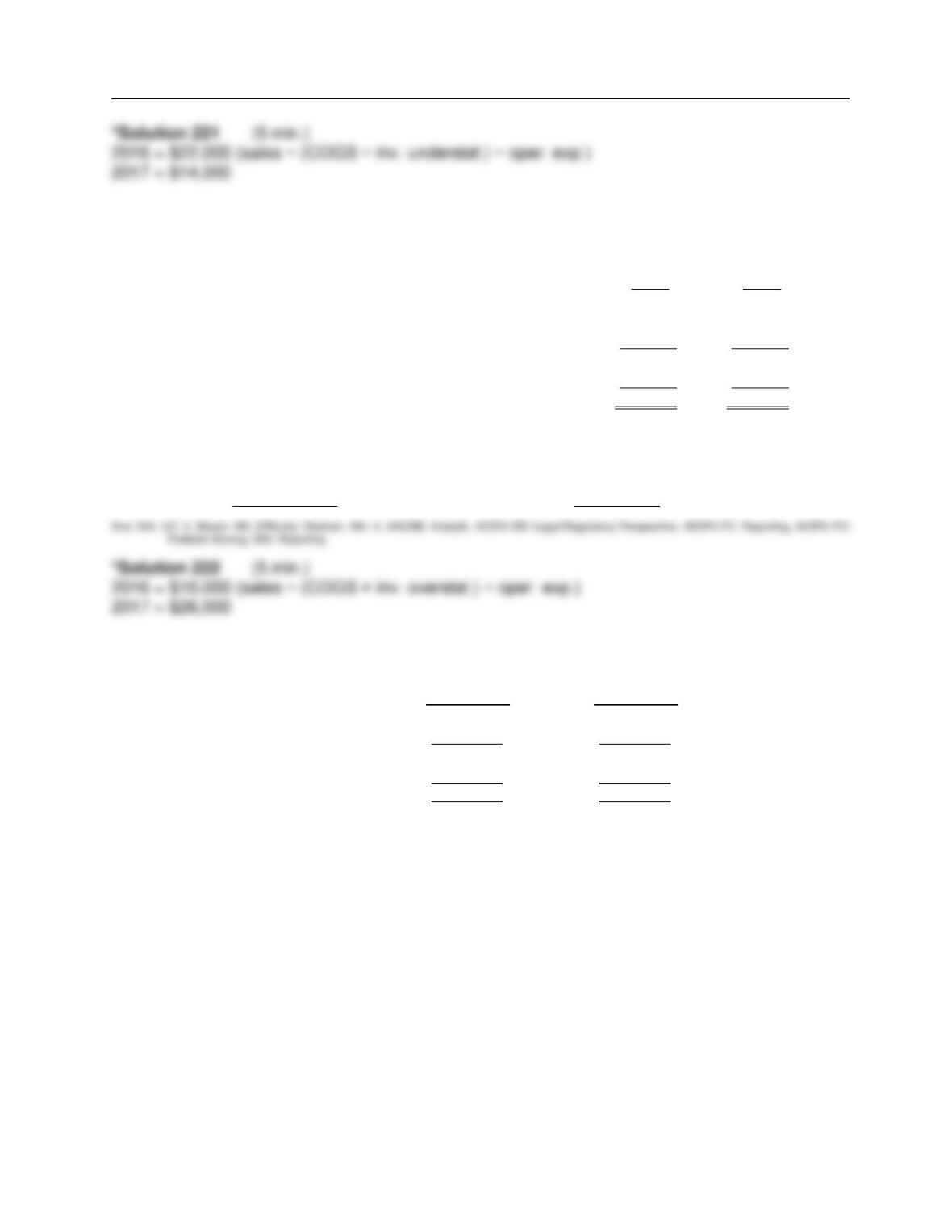

*Ex. 221

Condensed income statements for Swift Corporation are shown below for two years.

2016 2017

Sales $75,000 $90,000

Cost of Goods Sold 45,000 54,000

Gross Profit $30,000 $36,000

Operating Expense 15,000 15,000

Net Income $15,000 $21,000

Compute the corrected net income for 2016 and 2017 assuming that the inventory as of the end

of 2016 was mistakenly understated by $7,000.

2016 $ __________ 2017 $__________

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-77

*Ex. 222

Condensed income statements for Werly Corporation are shown below for two years.

2016 2017

Sales $75,000 $90,000

Cost of Goods Sold 45,000 54,000

Gross Profit $30,000 $36,000

Operating Expense 15,000 15,000

Net Income $15,000 $21,000

Compute the corrected net income for 2016 and 2017 assuming that the inventory as of the end

of 2016 was mistakenly overstated by $5,000.

2016 $ __________ 2017 $__________

*Ex. 223

Arnold Pharmacy reported cost of goods sold as follows:

2016 2017

Beginning inventory $ 54,000 $ 64,000

Cost of goods purchased 847,000 891,000

Cost of goods available for sale 901,000 955,000

Ending inventory 64,000 55,000

Cost of goods sold $837,000 $900,000

Arnold made two errors:

(1) 2016 ending inventory was overstated by $6,000.

(2) 2017 ending inventory was understated by $11,000.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

6-78

*Ex. 223 (Cont.)

Instructions

Assuming the errors had not been corrected, indicate the dollar effect that the errors had on the

items appearing on the financial statements listed below. Also indicate if the amounts are

overstated (O) or understated (U).

2016 2017

Overstated/ Overstated/

Amount Understated Amount Understated

Total assets $_________ _______ $_________ _______

Stockholders’ equity $_________ _______ $_________ _______

Cost of goods sold $_________ _______ $_________ _______

Net income $_________ _______ $_________ _______

Reporting and Analyzing Inventory

6-79

COMPLETION STATEMENTS

224. In a manufacturing company, goods that are ready to be sold to customers are referred to

as ________________, whereas in a merchandising company they are generally referred

to as _______________.

225. In a manufacturing company, there are three categories of inventory: they are

_____________________, _________________, and _________________.

226. When the terms of sale are FOB ______________, ownership of the goods passes to the

buyer when the public carrier accepts the goods from the seller.

227. The two inventory costing systems used are the ______________ and ______________.

228. When a business holds goods of other parties without taking ownership, and tries to sell

them for a fee, the goods are called ____________ goods.

229. Cost of goods available for sale must be allocated between cost of goods ___________

and ______________.

230. The ______________ method tracks the actual physical flow of each unit of inventory

available for sale; however, management may be able to manipulate ______________ by

using this method.

231. If the unit cost of inventory has continuously increased, the ______________, first-out

inventory valuation method will result in a higher valued ending inventory than if the

______________, first-out method had been used.

232. Under the LCM basis, market is defined as current ______________ cost.

233. The ______________ is calculated as cost of goods sold divided by average inventory.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

6-80

234. The _____________ is a required disclosure for companies that use LIFO.

Answers to Completion Statements

MATCHING

235. Match the items below by entering the appropriate code letter in the space provided.

A. Merchandise Inventory F. First-in, first-out (FIFO) method

B. Work in process G. Last-in, first-out (LIFO) method

C. FOB shipping point H. Average cost method

D. FOB destination I. LIFO reserve

E. Specific identification method J. Inventory turnover ratio

____ 1. The difference between inventory reported using LIFO and inventory using FIFO.

____ 2. Tracks the actual physical flow for each inventory item available for sale.

____ 3. Goods that are only partially completed in a manufacturing company.

____ 4. Cost of goods sold consists of the most recent inventory purchases.

____ 5. Goods ready for sale to customers by retailers and wholesalers.

____ 6. Title to the goods transfers when the public carrier accepts the goods from the

seller.

____ 7. Ending inventory valuation consists of the most recent inventory purchases.

____ 8. The same unit cost is used to value ending inventory and cost of goods sold.

____ 9. Title to goods transfers when the goods are delivered to the buyer.

____ 10. Measures the number of times the inventory sold during the period.

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-81

Answers to Matching

SHORT-ANSWER ESSAY QUESTIONS

S-A E 236

The periodic and the perpetual inventory systems are two methods that companies use to

account for inventories. Briefly describe the major features of each system and explain why a

physical inventory is necessary under both systems.

S-A E 237

What is the primary basis of accounting for inventories? What is the major objective in accounting

for inventories?

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

6-82

S-A E 238

A survey of major U.S. companies revealed that 77% of those companies used either LIFO or

FIFO cost flow methods, while 19% used average cost, and only 4% used other methods.

Requirement

Provide brief, yet concise responses to the following questions.

a. Why are LIFO and FIFO so popular?

b. Since computers and inventory management software are readily available, why aren’t

more companies using specific identification?

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-83

S-A E 239

Your office is on the 68th floor of your building. The CEO’s office is on the 77th floor. The two of

you are waiting for an elevator one morning. The CEO states “Our prices are rising and I want the

lowest net income for tax purposes and the highest ending inventory for external reporting

purposes. Which inventory method should we use?

Requirement

You have three minutes to respond to the CEO. What is your response?

S-A E 240

Your former college roommate is opening a new retail store and asks you “Which inventory

costing method should I use?”

What is your response? Include a comparison of the tax effect, balance sheet effect, and income

statement effect for FIFO versus LIFO.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

6-84

Solution 240 (Cont.)

S-A E 241

FIFO and LIFO are the two most common cost flow assumptions made in costing inventories.

The amounts assigned to the same inventory items on hand may be different under each cost

flow assumption. If a company has no beginning inventory, explain the difference in ending

inventory values under the FIFO and LIFO cost bases when the price of inventory items

purchased during the period have been (1) increasing, (2) decreasing, and (3) remained constant.

S-A E 242

Glenda Carson is studying for the next accounting midterm examination. What should Glenda

know about (a) departing from the cost basis of accounting for inventories and (b) the meaning of

“market” in the lower-of-cost-or-market method?

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-85

S-A E 243

What is the LIFO reserve? What are the consequences of ignoring a large LIFO reserve when

analyzing a company?

S-A E 244 (Ethics)

Angie and Neal Fry are department managers in the housewares and shoe departments,

respectively, for Calhouns, a large department store. Neal has observed Angie taking inventory

from her own department home, apparently without paying for it. He hesitates confronting Angie

because he is due to be promoted, and needs Angie’s recommendation. He also does not want to

notify the company management directly, because he doesn’t want an ethics investigation on his

record, believing that it will give him a “goody–goody” image. This week, Angie tried on several

pairs of expensive running shoes in his department before finding a pair that suited her. She did

not, however, buy them. That very pair was missing this morning.

Calhouns recently replaced its old periodic inventory system with a perpetual inventory system

using scanners and bar codes. In addition, the annual inventory is to be replaced by a monthly

inventory conducted by an independent firm. On hearing the news of the changes, Neal relaxes.

“The system will catch Angie now,” he says to himself.

Required:

1. Is Neal’s attitude justified? Why or why not?

2. What, if any, action should Neal take now?

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

6-86

S-A E 245 (Communication)

Al Bodkin, a new employee of Crafter’s Paradise, recorded $1,000 in consigned goods received

as part of the firm’s inventory. The goods were received one day after the end of the fiscal period,

but Al reasoned that the goods should be included in inventory sooner because Crafter’s paid the

freight. The mistake was brought to his attention by the purchasing department who said the

goods should not have been recorded as Crafter’s inventory at all. Al told Sid Goza, the

purchasing supervisor, that nobody needed to worry, because the mistake would cancel itself out

the following month. In Al’s opinion, there was no reason to get everyone excited over nothing,

especially since it was monthly, and not annual, financial statements that were affected. Sid Goza

has reported the problem to the accounting department.

Required:

You are Al’s supervisor. Write a memo to Al explaining why the error should have been corrected.

Reporting and Analyzing Inventory

6-87

IFRS QUESTIONS

1. The requirements for accounting for and reporting of inventories under IFRS, compared to

GAAP, tend to be more

a. detailed.

b. rules-based.

c. principles-based.

d. full of disclosure requirements.

2. The major IFRS requirements related to accounting for and reporting inventories are

a. the same as GAAP.

b. the same as GAAP with a couple of exceptions.

c. completely different fom GAAP.

d. not comparable to GAAP.

3. Inventory accounting under IFRS differs from GAAP in regard to

a. neither the use of LIFO nor lower-of-cost-or-market.

b. the use of LIFO but not lower-of-cost-or-market.

c. the use of lower-of-cost-or-market but not LIFO.

d. the use of LIFO and lower-of-cost-or-market.

4. Under GAAP, companies can choose which inventory system?

LIFO FIFO

a. Yes No

b. Yes Yes

c. No Yes

d. Yes No

5. Under IFRS, companies can choose which inventory system?

LIFO FIFO

a. Yes No

b. Yes Yes

c. No Yes

d. Yes No

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

6-88

6. Specific Identification can be used for inventory valuation under

GAAP IFRS

a. Yes No

b. Yes Yes

c. No No

d. No Yes

7. GAAP’s provision for ownership of goods (goods–in-transit or consigned goods), as well

as which costs to include in inventory, as compared to IFRS are:

Ownership of goods Costs to include in inventory

a. essentially similar essentially similar

b. essentially different essentially different

c. essentially similar essentially different

d. essentially different essentially similar

8. The only acceptable cost flow assumptions under IFRS are

a. FIFO and LIFO.

b. FIFO and average.

c. LIFO and average.

d. FIFO, LIFO and average.

9. LIFO can be used

a. under neither GAAP nor IFRS.

b. under IFRS but not GAAP.

c. under GAAP but not IFRS.

d. under both GAAP and IFRS.

10. IFRS defines market for lower-of-cost-or market as

a. net realizable value.

b. estimated selling price in the ordinary course of business.

c. replacement cost.

d. replacement cost less costs of disposal.

11. GAAP defines market for lower-of-cost-or market essentially as

a. net realizable value.

b. estimated selling price in the ordinary course of business.

c. replacement cost.

d. replacement cost less costs of disposal.