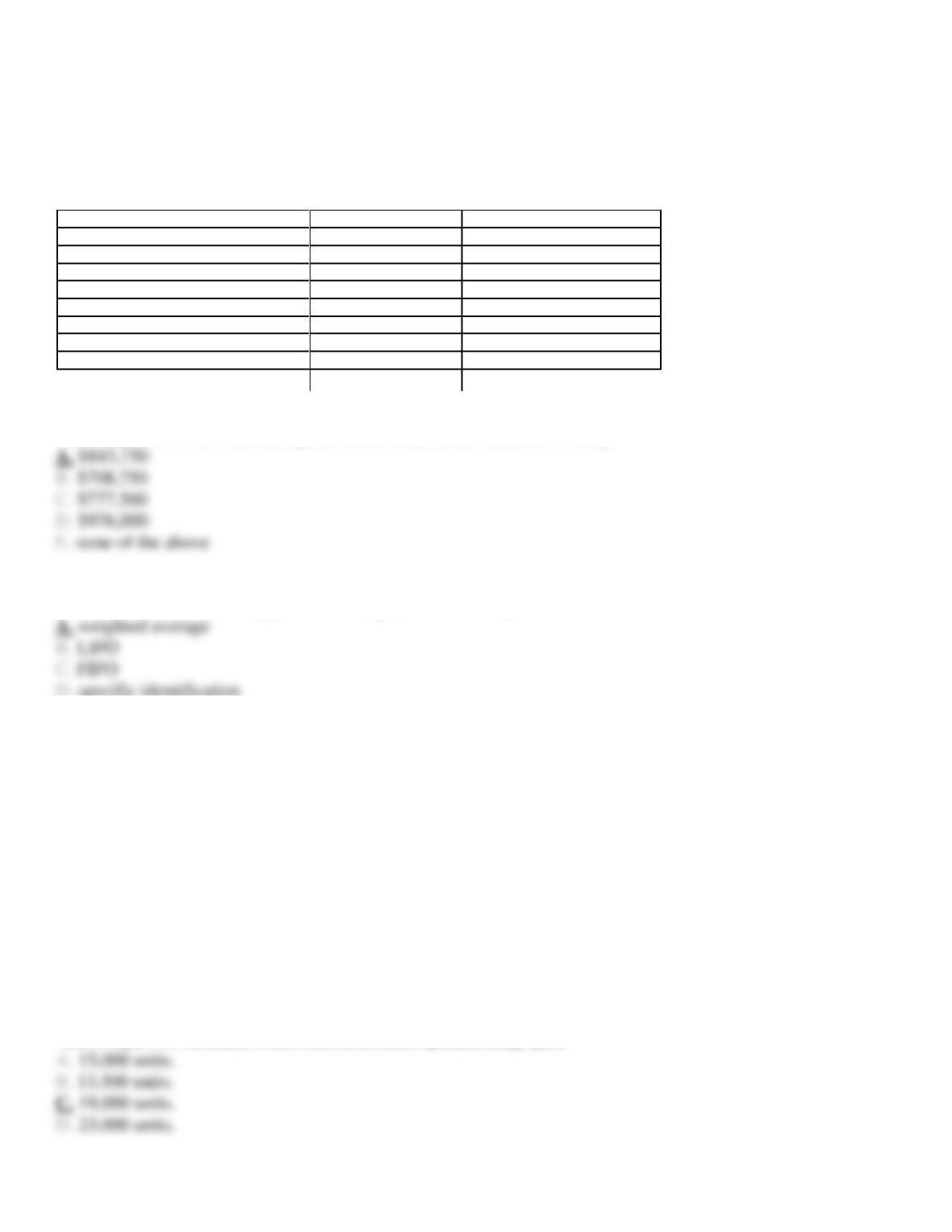

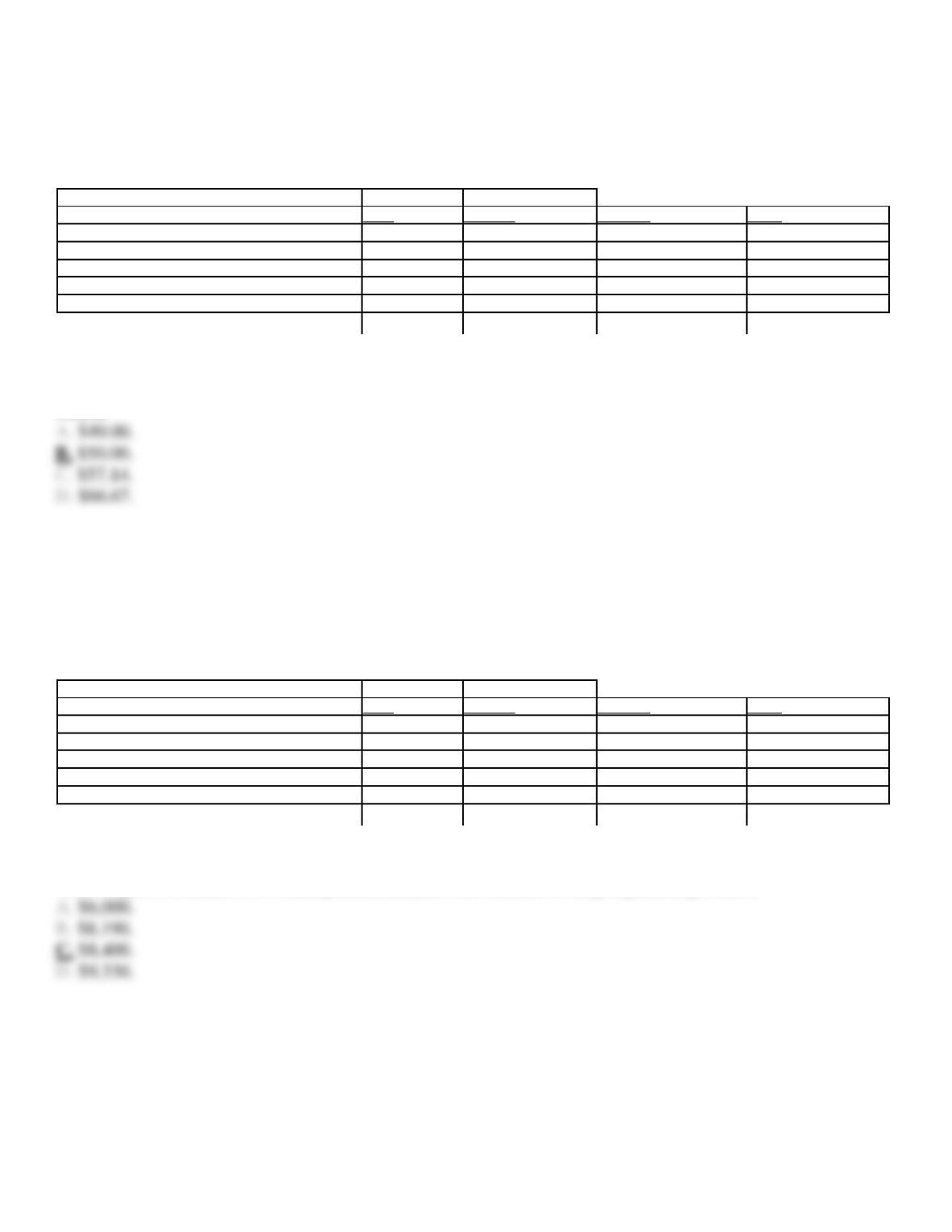

137. Figure 6-15

The Davidson Company uses a weighted average process costing system. The following information was

reported for the Assembly Process for January. Materials are added at the beginning of the process and are

100%.

Units:

units

% complete for conversions

work in process, 1/1

60,000

15%

started

105,000

work in process, 1/31

40,000

20%

Costs:

Materials

Conversion

beginning work in process

$ 16,500

$ 33,250

current costs

$643,500

$332,500

Refer to Figure 6-15. What is the cost assigned to the units completed and transferred to finishing?

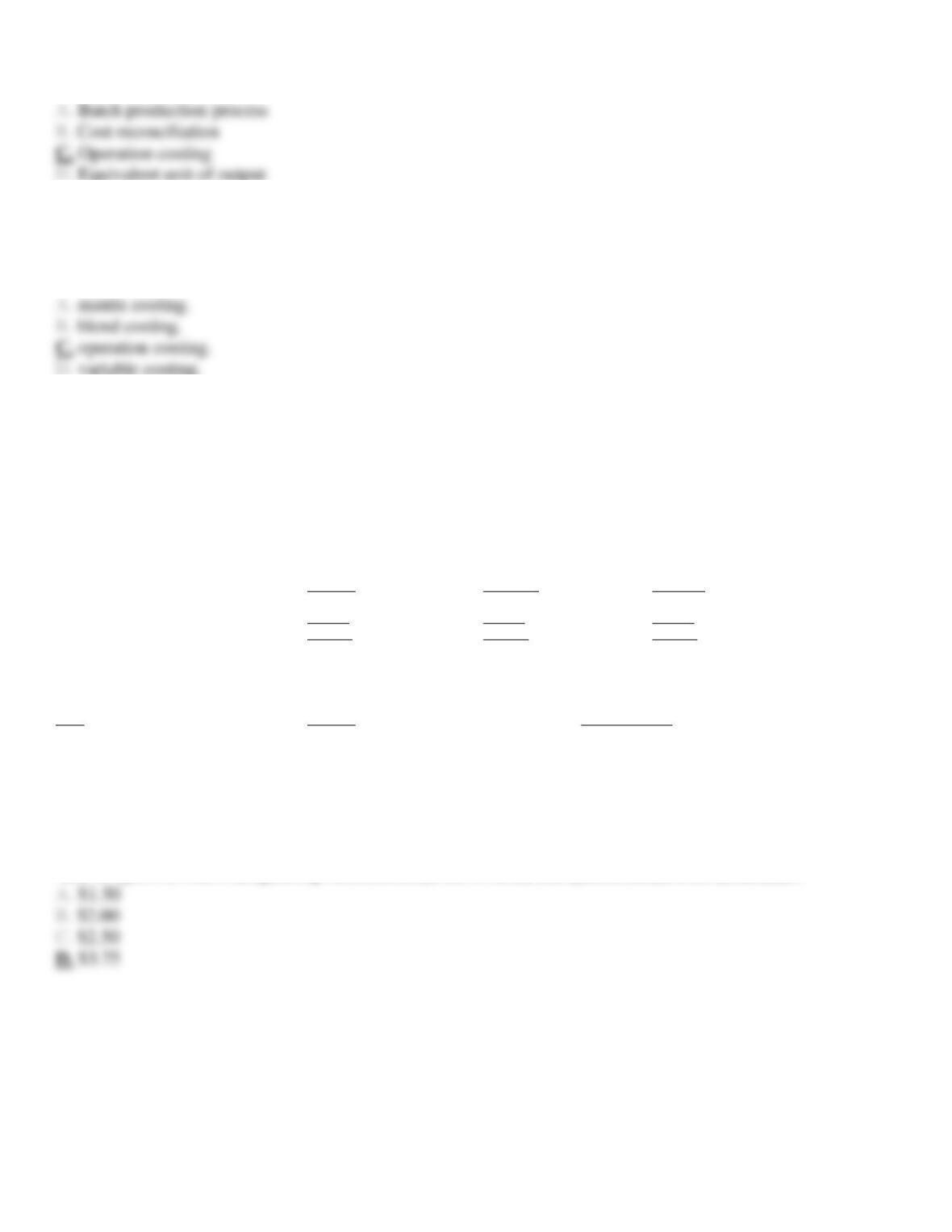

138. Which of the following process costing methods is simpler to use?

139. Figure 6-16

Ramses Corporation produces a product that passes through two processes. During April, the first department

transferred 19,000 units to the second department. The cost of the units transferred was $30,000. Materials are

added uniformly in the second process. The following information is provided about the second department’s

operations during October:

Units, beginning work in process

4,000

Units, ending work in process

5,500

Refer to Figure 6-16. The number of units started in the second department during April is

140. Figure 6-16

Ramses Corporation produces a product that passes through two processes. During April, the first department

transferred 19,000 units to the second department. The cost of the units transferred was $30,000. Materials are

added uniformly in the second process. The following information is provided about the second department’s

operations during October:

Units, beginning work in process

4,000

Units, ending work in process

5,500

Refer to Figure 6-16. The number of units completed in the second department during April is

141. Figure 6-16

Ramses Corporation produces a product that passes through two processes. During April, the first department

transferred 19,000 units to the second department. The cost of the units transferred was $30,000. Materials are

added uniformly in the second process. The following information is provided about the second department’s

operations during October:

Units, beginning work in process

4,000

Units, ending work in process

5,500

Refer to Figure 6-16. The number of units started and completed in the second department during April is

142. Materials are added to a second production department and will not increase the number of units produced

in this department. Adding materials to the second department will

143. Figure 6-17

Loganbery Corporation produces a product that passes through two processes. During January, the first

department transferred 20,000 units to the second department. The cost of the units transferred was $60,000.

Materials are added uniformly in the second process. The following information is provided about the first

department’s operations during January:

Units, beginning work in process (1/3 complete)

6,000

Units, ending work in process (1/2 complete)

4,000

Refer to Figure 6-17. The equivalent units for those transferred in from the prior department using weighted average is

144. Figure 6-17

Loganbery Corporation produces a product that passes through two processes. During January, the first

department transferred 20,000 units to the second department. The cost of the units transferred was $60,000.

Materials are added uniformly in the second process. The following information is provided about the first

department’s operations during January:

Units, beginning work in process (1/3 complete)

6,000

Units, ending work in process (1/2 complete)

4,000

Refer to Figure 6-17. The equivalent units for conversion using weighted average is

145. Figure 6-17

Loganbery Corporation produces a product that passes through two processes. During January, the first

department transferred 20,000 units to the second department. The cost of the units transferred was $60,000.

Materials are added uniformly in the second process. The following information is provided about the first

department’s operations during January:

Units, beginning work in process (1/3 complete)

6,000

Units, ending work in process (1/2 complete)

4,000

Refer to Figure 6-17. The equivalent units for those transferred in from the prior department using FIFO would be

146. Figure 6-17

Loganbery Corporation produces a product that passes through two processes. During January, the first

department transferred 20,000 units to the second department. The cost of the units transferred was $60,000.

Materials are added uniformly in the second process. The following information is provided about the first

department’s operations during January:

Units, beginning work in process (1/3 complete)

6,000

Units, ending work in process (1/2 complete)

4,000

Refer to Figure 6-17. The equivalent units for conversion using FIFO would be

147. The cost assigned to goods from a prior process is termed:

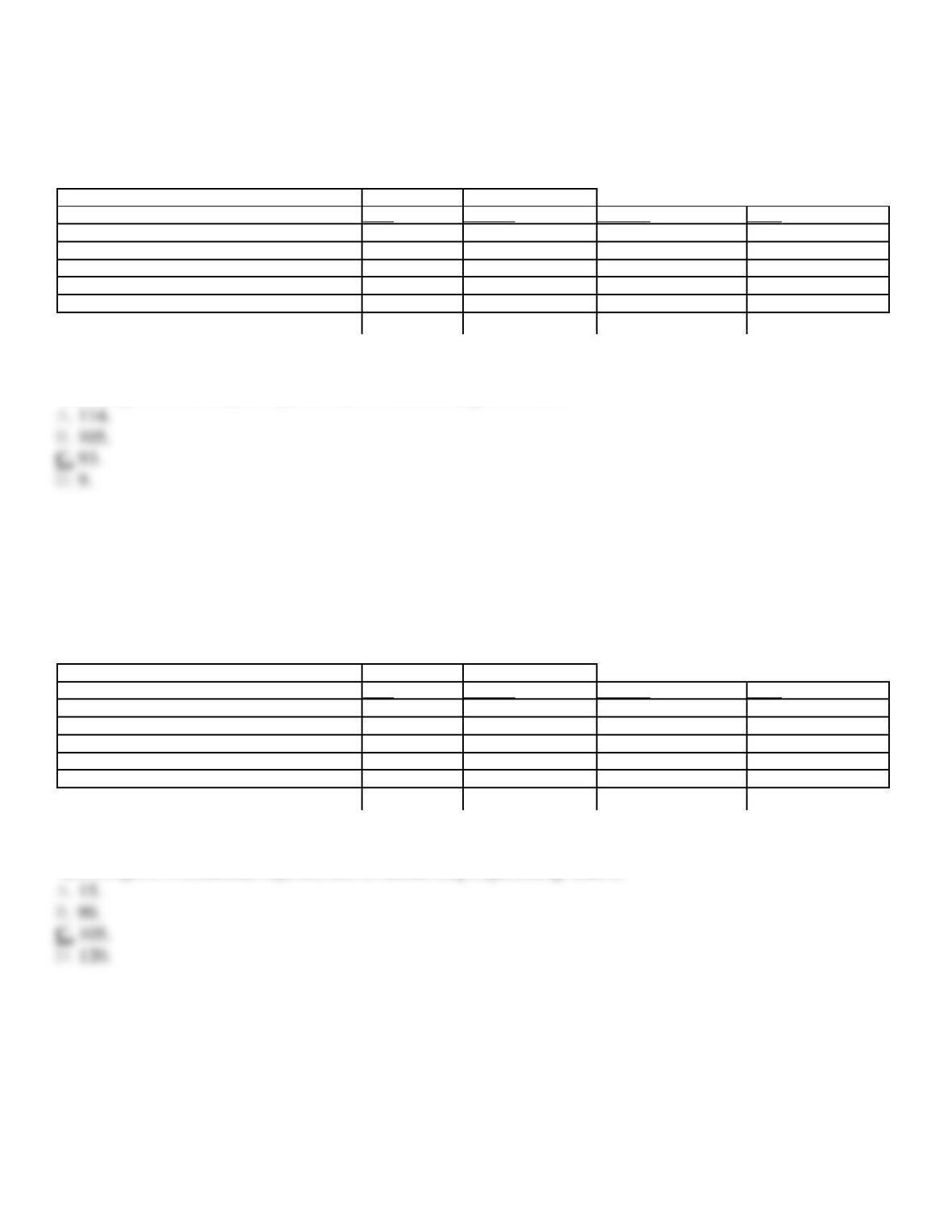

148. Figure 6-18

The Round Table Company makes carpenter’s squares and uses a process costing system. There is no spoilage.

Manufacturing goes through three departments: Forming, Finishing, and Packing. Unit data for these

departments are given below:

Forming

Finishing

Packing

Beginning inventory units

(80% complete)

1,000

2,000

3,000

Units started

8,000

?

?

Ending inventory units

(20% complete)

3,000

4,000

1,000

The Finishing Department adds materials at the point where processing is 50 percent complete.

Refer to Figure 6-18. The equivalent units for materials in the Finishing Department is

Weighted Average

FIFO

149. Refer to Figure 6-18. The equivalent units for transferred-in the Finishing Department is

Weighted Average

FIFO

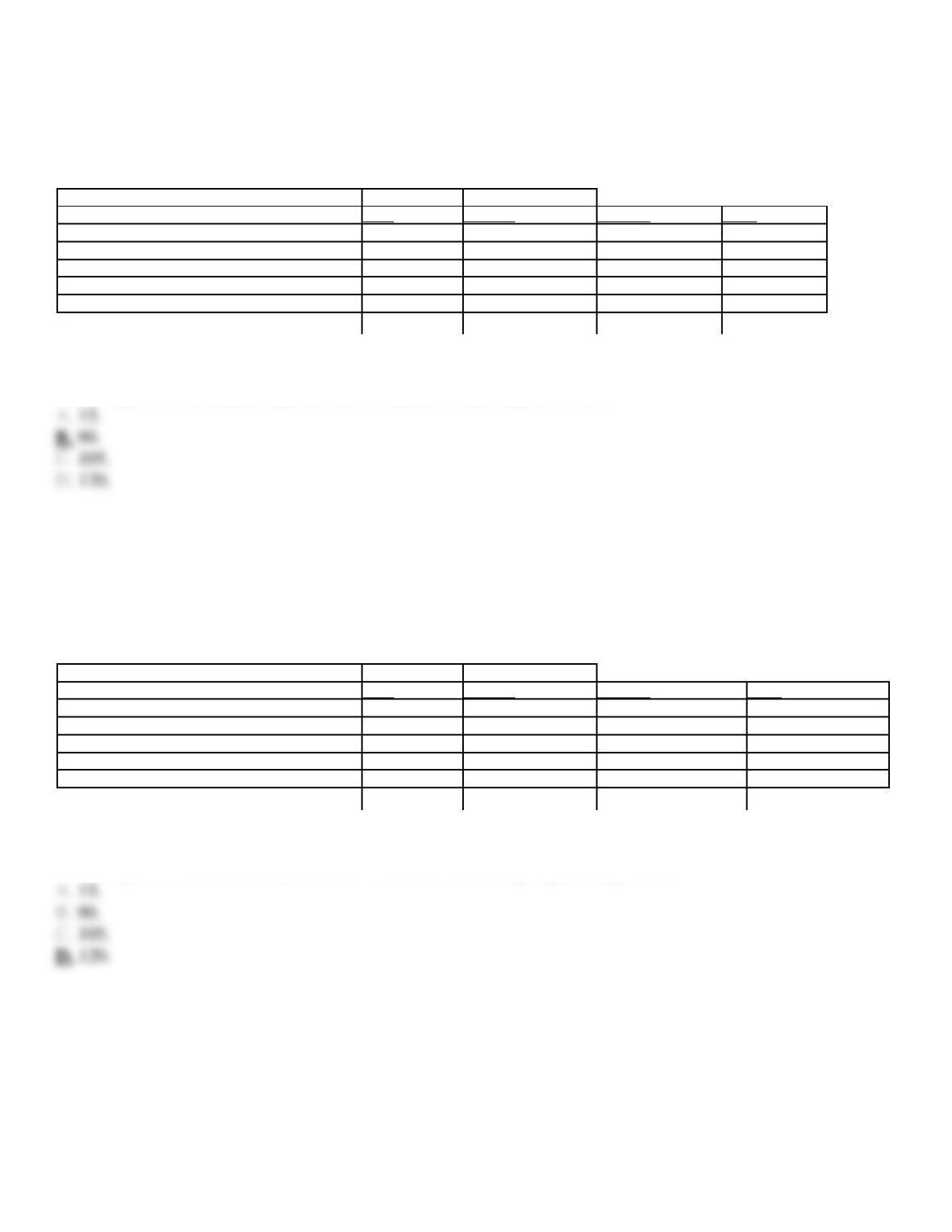

150. Figure 6-19

Mountainside Industries manufactures specialized plastic boxes in two processes: Molding and Packaging. In

the Packaging Department, materials are added at the end of the process. The following data are given:

Costs

Units

Trans.-in

Materials

Conv.

Work in process, July 1

30

$1,590

$-0-

$513

Transferred in during July

?

Completed during July

105

Work in process, July 31

15

Costs added during July

$4,410

$1,050

$1,767

The conversion process on the beginning inventory is 70 percent completed and the ending inventory is 60 percent completed.

Refer to Figure 6-19. Mountainside’s equivalent units for conversion using FIFO would be

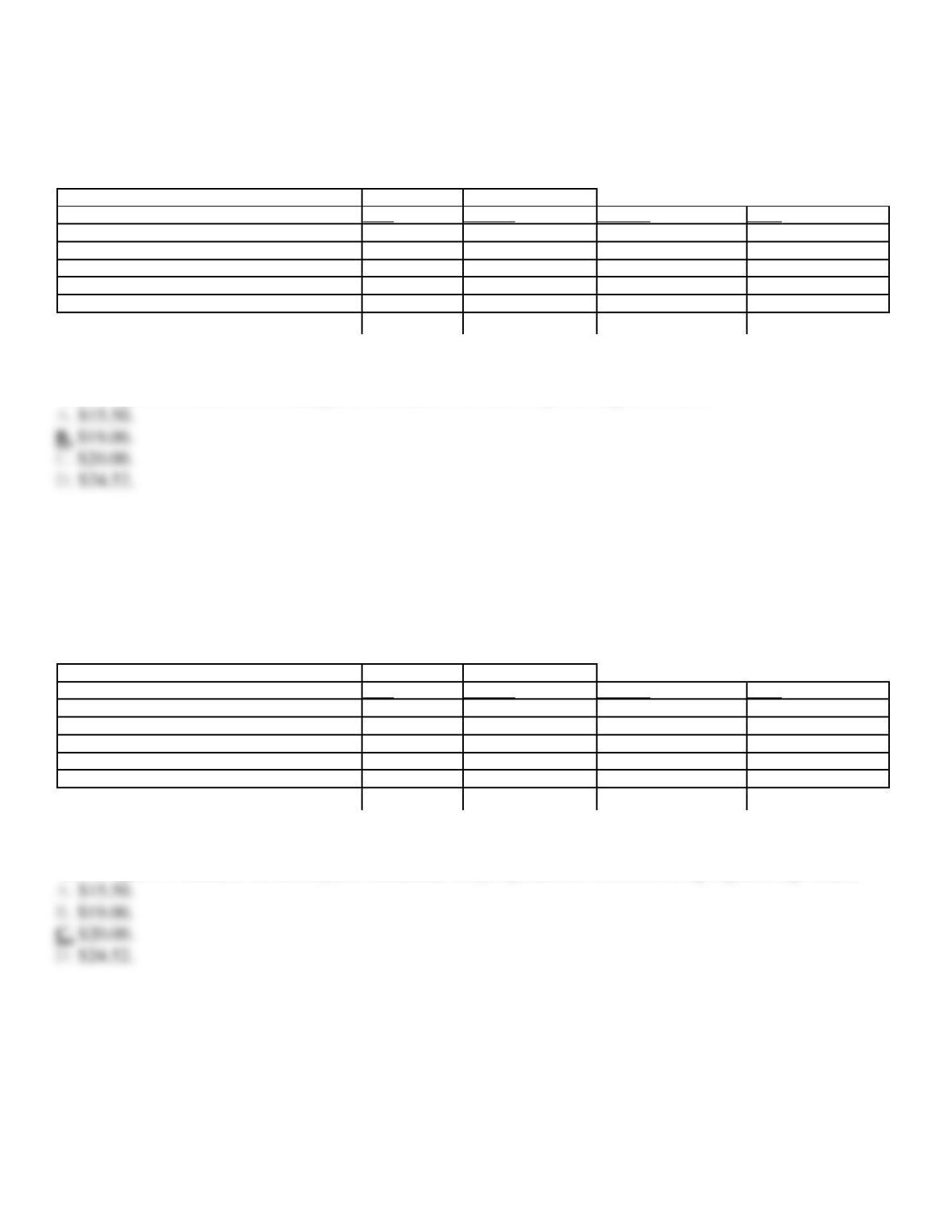

151. Figure 6-19

Mountainside Industries manufactures specialized plastic boxes in two processes: Molding and Packaging. In

the Packaging Department, materials are added at the end of the process. The following data are given:

Costs

Units

Trans.-in

Materials

Conv.

Work in process, July 1

30

$1,590

$-0-

$513

Transferred in during July

?

Completed during July

105

Work in process, July 31

15

Costs added during July

$4,410

$1,050

$1,767

The conversion process on the beginning inventory is 70 percent completed and the ending inventory is 60 percent completed.

Refer to Figure 6-19.Mountainside’s equivalent units for materials using weighted average would be

152. Figure 6-19

Mountainside Industries manufactures specialized plastic boxes in two processes: Molding and Packaging. In

the Packaging Department, materials are added at the end of the process. The following data are given:

Costs

Units

Trans.-in

Materials

Conv.

Work in process, July 1

30

$1,590

$-0-

$513

Transferred in during July

?

Completed during July

105

Work in process, July 31

15

Costs added during July

$4,410

$1,050

$1,767

The conversion process on the beginning inventory is 70 percent completed and the ending inventory is 60 percent completed.

Refer to Figure 6-19. Mountainside’s equivalent units for transferred-in units using FIFO would be

153. Figure 6-19

Mountainside Industries manufactures specialized plastic boxes in two processes: Molding and Packaging. In

the Packaging Department, materials are added at the end of the process. The following data are given:

Costs

Units

Trans.-in

Materials

Conv.

Work in process, July 1

30

$1,590

$-0-

$513

Transferred in during July

?

Completed during July

105

Work in process, July 31

15

Costs added during July

$4,410

$1,050

$1,767

The conversion process on the beginning inventory is 70 percent completed and the ending inventory is 60 percent completed.

Refer to Figure 6-19. Mountainside’s equivalent units for transferred-in units using weighted average would be

154. Figure 6-19

Mountainside Industries manufactures specialized plastic boxes in two processes: Molding and Packaging. In

the Packaging Department, materials are added at the end of the process. The following data are given:

Costs

Units

Trans.-in

Materials

Conv.

Work in process, July 1

30

$1,590

$-0-

$513

Transferred in during July

?

Completed during July

105

Work in process, July 31

15

Costs added during July

$4,410

$1,050

$1,767

The conversion process on the beginning inventory is 70 percent completed and the ending inventory is 60 percent completed.

Refer to Figure 6-19. Rounded to two decimal places, Mountainside’s conversion cost per unit using FIFO would be

155. Figure 6-19

Mountainside Industries manufactures specialized plastic boxes in two processes: Molding and Packaging. In

the Packaging Department, materials are added at the end of the process. The following data are given:

Costs

Units

Trans.-in

Materials

Conv.

Work in process, July 1

30

$1,590

$-0-

$513

Transferred in during July

?

Completed during July

105

Work in process, July 31

15

Costs added during July

$4,410

$1,050

$1,767

The conversion process on the beginning inventory is 70 percent completed and the ending inventory is 60 percent completed.

Refer to Figure 6-19. Rounded to two decimal places, Mountainside’s cost per equivalent unit for conversion using weighted average would be

156. Figure 6-19

Mountainside Industries manufactures specialized plastic boxes in two processes: Molding and Packaging. In

the Packaging Department, materials are added at the end of the process. The following data are given:

Costs

Units

Trans.-in

Materials

Conv.

Work in process, July 1

30

$1,590

$-0-

$513

Transferred in during July

?

Completed during July

105

Work in process, July 31

15

Costs added during July

$4,410

$1,050

$1,767

The conversion process on the beginning inventory is 70 percent completed and the ending inventory is 60 percent completed.

Refer to Figure 6-19. Rounded to two decimal places, Mountainside’s cost per equivalent units for transferred-in costs using weighted average

would be

157. Figure 6-19

Mountainside Industries manufactures specialized plastic boxes in two processes: Molding and Packaging. In

the Packaging Department, materials are added at the end of the process. The following data are given:

Costs

Units

Trans.-in

Materials

Conv.

Work in process, July 1

30

$1,590

$-0-

$513

Transferred in during July

?

Completed during July

105

Work in process, July 31

15

Costs added during July

$4,410

$1,050

$1,767

The conversion process on the beginning inventory is 70 percent completed and the ending inventory is 60 percent completed.

Refer to Figure 6-19. Rounded to two decimal places, Mountainside’s costs transferred out using weighted average would be

158. The costing system that uses job-order costing to assign material costs and process costing to assign

conversion costs is called:

159. When job-order costing is used to assign material costs and process costing is used to assign conversion

costs, it is called

160. Figure 6-20

Outrageous Cups Corp. manufactures cups. The company’s manufacturing operations and costs applied to

products for April were:

Molding

Heat-treat

Finishing

Direct labor

$25,000

$12,500

$ 7,500

Factory overhead

30,000

17,500

12,600

Total

$55,000

$30,000

$20,100

Three types of cups were produced in April. The quantities and direct materials costs were:

Type

Quantity

Direct Materials

Casts

5,000

$15,000

Cups

7,000

22,470

Mugs

8,000

32,500

Casts are produced in the Molding Department. Cups pass through the Molding and Finishing Departments. Mugs pass through all three departments.

An operations costing system is used.

Refer to Figure 6-20. What is Outrageous Cups’ conversion cost per unit for the heat-treat operation, rounded to two decimal places?

161. Figure 6-20

Outrageous Cups Corp. manufactures cups. The company’s manufacturing operations and costs applied to

products for April were:

Molding

Heat-treat

Finishing

Direct labor

$25,000

$12,500

$ 7,500

Factory overhead

30,000

17,500

12,600

Total

$55,000

$30,000

$20,100

Three types of cups were produced in April. The quantities and direct materials costs were:

Type

Quantity

Direct Materials

Casts

5,000

$15,000

Cups

7,000

22,470

Mugs

8,000

32,500

Casts are produced in the Molding Department. Cups pass through the Molding and Finishing Departments. Mugs pass through all three departments.

An operations costing system is used.

Refer to Figure 6-20. What is Outrageous Cups’ total cost for Casts in April?

162. Figure 6-20

Outrageous Cups Corp. manufactures cups. The company’s manufacturing operations and costs applied to

products for April were:

Molding

Heat-treat

Finishing

Direct labor

$25,000

$12,500

$ 7,500

Factory overhead

30,000

17,500

12,600

Total

$55,000

$30,000

$20,100

Three types of cups were produced in April. The quantities and direct materials costs were:

Type

Quantity

Direct Materials

Casts

5,000

$15,000

Cups

7,000

22,470

Mugs

8,000

32,500

Casts are produced in the Molding Department. Cups pass through the Molding and Finishing Departments. Mugs pass through all three departments.

An operations costing system is used.

Refer to Figure 6-20. What is Outrageous Cups’ total cost per unit for Cups in April?

163. The process that produces batches of different products which are identical in many ways but differ in

others is called:

164. Figure 6-21

Golden Ring Company produces two types of product: Large and Larger. Two work orders for two batches of

the products are shown below, along with some additional cost information:

Large

Larger

Work Order 10

Work Order 11

Direct materials (actual costs)

$45,000

$75,000

Applied conversion costs:

Mixing

?

?

Cooking

$12,000

$12,000

Bottling

$10,000

$15,000

Batch size (bottles)

5,000

5,000

In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year

were $50,000 for labor and $125,000 for overhead. Budgeted direct labor hours were 2,500. It takes three minutes to mix the ingredients needed for

each bottle.

Large (Work Order 10) and Larger (Work Order 11) flow through the Mixing Department first, then through the Cooking and Bottling departments.

Refer to Figure 6-21. What are Golden Ring Company’s conversion costs applied to Large (Work Order 10) from the Mixing Department for each

batch?

165. Figure 6-21

Golden Ring Company produces two types of product: Large and Larger. Two work orders for two batches of

the products are shown below, along with some additional cost information:

Large

Larger

Work Order 10

Work Order 11

Direct materials (actual costs)

$45,000

$75,000

Applied conversion costs:

Mixing

?

?

Cooking

$12,000

$12,000

Bottling

$10,000

$15,000

Batch size (bottles)

5,000

5,000

In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year

were $50,000 for labor and $125,000 for overhead. Budgeted direct labor hours were 2,500. It takes three minutes to mix the ingredients needed for

each bottle.

Large (Work Order 10) and Larger (Work Order 11) flow through the Mixing Department first, then through the Cooking and Bottling departments.

Refer to Figure 6-21. What is Golden Ring Company’s amount transferred from the Mixing Department to the Cooking Department for Work Order

10?

166. Figure 6-21

Golden Ring Company produces two types of product: Large and Larger. Two work orders for two batches of

the products are shown below, along with some additional cost information:

Large

Larger

Work Order 10

Work Order 11

Direct materials (actual costs)

$45,000

$75,000

Applied conversion costs:

Mixing

?

?

Cooking

$12,000

$12,000

Bottling

$10,000

$15,000

Batch size (bottles)

5,000

5,000

In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year

were $50,000 for labor and $125,000 for overhead. Budgeted direct labor hours were 2,500. It takes three minutes to mix the ingredients needed for

each bottle.

Large (Work Order 10) and Larger (Work Order 11) flow through the Mixing Department first, then through the Cooking and Bottling departments.

Refer to Figure 6-21. What is Golden Ring Company’s amount transferred from the Bottling Department to Finished Goods for Work Order 10?

167. Figure 6-21

Golden Ring Company produces two types of product: Large and Larger. Two work orders for two batches of

the products are shown below, along with some additional cost information:

Large

Larger

Work Order 10

Work Order 11

Direct materials (actual costs)

$45,000

$75,000

Applied conversion costs:

Mixing

?

?

Cooking

$12,000

$12,000

Bottling

$10,000

$15,000

Batch size (bottles)

5,000

5,000

In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year

were $50,000 for labor and $125,000 for overhead. Budgeted direct labor hours were 2,500. It takes three minutes to mix the ingredients needed for

each bottle.

Large (Work Order 10) and Larger (Work Order 11) flow through the Mixing Department first, then through the Cooking and Bottling departments.

Refer to Figure 6-21. What is Golden Ring Company’s unit cost of Large?

168. Figure 6-21

Golden Ring Company produces two types of product: Large and Larger. Two work orders for two batches of

the products are shown below, along with some additional cost information:

Large

Larger

Work Order 10

Work Order 11

Direct materials (actual costs)

$45,000

$75,000

Applied conversion costs:

Mixing

?

?

Cooking

$12,000

$12,000

Bottling

$10,000

$15,000

Batch size (bottles)

5,000

5,000

In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year

were $50,000 for labor and $125,000 for overhead. Budgeted direct labor hours were 2,500. It takes three minutes to mix the ingredients needed for

each bottle.

Large (Work Order 10) and Larger (Work Order 11) flow through the Mixing Department first, then through the Cooking and Bottling departments.

Refer to Figure 6-21. What is Golden Ring Company’s unit cost of Larger?

169. Figure 6-21

Golden Ring Company produces two types of product: Large and Larger. Two work orders for two batches of

the products are shown below, along with some additional cost information:

Large

Larger

Work Order 10

Work Order 11

Direct materials (actual costs)

$45,000

$75,000

Applied conversion costs:

Mixing

?

?

Cooking

$12,000

$12,000

Bottling

$10,000

$15,000

Batch size (bottles)

5,000

5,000

In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year

were $50,000 for labor and $125,000 for overhead. Budgeted direct labor hours were 2,500. It takes three minutes to mix the ingredients needed for

each bottle.

Large (Work Order 10) and Larger (Work Order 11) flow through the Mixing Department first, then through the Cooking and Bottling departments.

Refer to Figure 6-21. What is Golden Ring Company’s journal entry to record materials used in the Mixing Department for Work Order 10?

170. Figure 6-21

Golden Ring Company produces two types of product: Large and Larger. Two work orders for two batches of

the products are shown below, along with some additional cost information:

Large

Larger

Work Order 10

Work Order 11

Direct materials (actual costs)

$45,000

$75,000

Applied conversion costs:

Mixing

?

?

Cooking

$12,000

$12,000

Bottling

$10,000

$15,000

Batch size (bottles)

5,000

5,000

In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year

were $50,000 for labor and $125,000 for overhead. Budgeted direct labor hours were 2,500. It takes three minutes to mix the ingredients needed for

each bottle.

Large (Work Order 10) and Larger (Work Order 11) flow through the Mixing Department first, then through the Cooking and Bottling departments.

Refer to Figure 6-21. What is Golden Ring Company’s journal entry to apply conversion costs in the Mixing Department for Work Order 10?

171. Which of the following would NOT be true when there is spoilage?