Chapter 6: Cash and Internal Control

90. The following set of items describes activities completed by a company in purchasing and paying for

merchandise. For each activity, identify whether or not the activity adheres to or violates sound

internal control procedures.

Although the department supervisor can indicate a preferred supplier or vendor on purchase requisitions, the

purchasing department has the responsibility for making the final decision on a vendor.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

91. The following set of items describes activities completed by a company in purchasing and paying for

merchandise. For each activity, identify whether or not the activity adheres to or violates sound

internal control procedures.

The receiving department compares the quantity received with the quantity printed on the receiving report when the

purchase order was prepared.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

92. The following set of items describes activities completed by a company in purchasing and paying for

merchandise. For each activity, identify whether or not the activity adheres to or violates sound

internal control procedures.

Extensions and footings on purchase invoices are verified before the invoices are approved for payment

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

93. The following set of items describes activities completed by a company in purchasing and paying for

merchandise. For each activity, identify whether or not the activity adheres to or violates sound

internal control procedures.

All documents attached to an invoice approval form are canceled before a check is signed.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

Chapter 6: Cash and Internal Control

94. The following set of items describes activities completed by a company in purchasing and paying for

merchandise. For each activity, identify whether or not the activity adheres to or violates sound internal

control procedures.

The clerk in the accounting department records both purchases and payments of invoices.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

95. The following set of items describes activities completed by a company in purchasing and paying for

merchandise. For each activity, identify whether or not the activity adheres to or violates sound internal

control procedures.

Checks are signed by designated officers in the finance department.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

96. The following set of items describes activities completed by a company in collecting cash for merchandise

sales. For each activity, identify whether or not the activity adheres to or violates sound internal control

procedures.

A single employee in the mailroom opens the mail, counts the money received, and prepares a control list of

the amount received.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

97. The following set of items describes activities completed by a company in collecting cash for merchandise

sales. For each activity, identify whether or not the activity adheres to or violates sound internal control

procedures.

An employee in the accounting department records cash receipts from customers and prepares a bank deposit slip.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

Chapter 6: Cash and Internal Control

98. The following set of items describes activities completed by a company in collecting cash for merchandise

sales. For each activity, identify whether or not the activity adheres to or violates sound internal control

procedures.

Cash register tapes are picked up daily by an employee from the accounting department.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

99. The following set of items describes activities completed by a company in collecting cash for merchandise

sales. For each activity, identify whether or not the activity adheres to or violates sound internal control

procedures.

An employee from the accounting department compares the control list and the cash register tapes with the bank

deposit slip.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

100. The following set of items describes activities completed by a company in collecting cash for merchandise

sales. For each activity, identify whether or not the activity adheres to or violates sound internal control

procedures.

Monthly statements, indicating the current balance due, are mailed to customers.

a. Adheres to sound internal control procedures

b. Violates sound internal control procedures

c. Neither strengthens nor violates internal control

101. Which one of the following is not a procedure in the approval of a specific invoice for payment?

a. The purchase requisition, purchase order, receiving report, and invoice are compared.

b. The extensions and footings on the invoice are verified.

c. An employee verifies that all of the approval activities have been completed before a check is prepared.

d. The purchasing department prepares a voucher to request payment.

102. What is the form sent by the seller to the buyer as evidence of a sale?

a. an invoice approval form

b. a purchase order

c. a receiving report

d. an invoice

Chapter 6: Cash and Internal Control

103. The department in an organization that is responsible for preparing the invoice approval form to document all of the

information about a particular purchase is:

a. the human resources department.

b. the purchasing department.

c. the receiving department.

d. the accounting department.

104. Which of the following is another term for the invoice approval form?

a. a receiving report

b. an invoice

c. a voucher

d. a remittance advice

105. A voucher is usually supported by

a. a supplier’s invoice

b. a purchase order

c. a receiving report

d. all of the above

106. The notification accompanying a check that indicates the specific invoice being paid is called a

a. remittance advice

b. voucher

c. debit memo

d. credit memo

107. A six–month certificate of deposit would be considered to be a cash equivalent.

a. True

b. False

108. Petty cash typically is composed of coins and currency kept on hand in a business to make minor disbursements.

a. True

b. False

Chapter 6: Cash and Internal Control

109. The key to the classification of an amount as cash is that it be available to pay debts within a three–month period

of time.

a. True

b. False

110. Some cash equivalents appear in the long term investment section of a balance sheet.

a. True

b. False

111. If collection of accounts receivable is assured, then accounts receivable are considered to be cash equivalents.

a. True

b. False

112. Treasury notes with a maturity of three months or less that are issued by the Federal Government are

cash equivalents.

a. True

b. False

113. A check written by a company but not yet presented to the bank for payment is called a check in transit.

a. True

b. False

114. When reconciling a bank account, the company does not have to prepare an adjusting entry for outstanding checks.

a. True

b. False

115. When reconciling a bank account, the company must prepare an adjusting entry for deposits in transit.

a. True

b. False

116. In a sound internal control system, all cash receipts should be deposited daily intact.

a. True

b. False

Chapter 6: Cash and Internal Control

117. Checks received from customers are considered to be cash in the company’s books.

a. True

b. False

118. The bank informs a customer that a service charge has been assessed on their account by including a credit

memorandum in the monthly bank statement.

a. True

b. False

119. On a bank reconciliation, outstanding checks are added to the cash balance per the bank statement.

a. True

b. False

120. When a bank pays interest or collects an amount owed to a company by one of the bank’s customers, the bank

issues a debit memorandum.

a. True

b. False

121. When a bank pays interest or collects an amount owed to a company by one of the bank’s customers, the bank

issues a credit memorandum.

a. True

b. False

122. On a bank reconciliation, bank charges for the month are added to the cash balance per the books.

a. True

b. False

123. On a bank reconciliation, interest earned for the month is added to the cash balance per the books.

a. True

b. False

124. A company prepares adjusting entries for debit memorandums but not for credit memorandums.

a. True

b. False

Chapter 6: Cash and Internal Control

125. The establishment of a petty cash fund has no effect on the company‘s total cash balance.

a. True

b. False

126. No special internal control procedures are necessary with a petty cash account because the amount is usually so

small.

a. True

b. False

127. An advantage of a strong system of internal control is that less testing of the accounting system is done by the

outside auditors.

a. True

b. False

128. A good system of internal control is important to make a company‘s accounting records completely foolproof.

a. True

b. False

129. An accounting system must be computerized in order to ensure the company has proper internal control.

a. True

b. False

130. Audit committees are required to consist of only directors who are key officers of the company.

a. True

b. False

131. According to the Sarbanes-Oxley Act of 2002, only external auditors can provide bookkeeping services for the

clients they audit.

a. True

b. False

132. One concern of the internal auditor is the efficiency with which the organization is run.

a. True

b. False

Chapter 6: Cash and Internal Control

133. If a company has internal auditors, it does not need to have external auditors.

a. True

b. False

134. Accounting controls primarily concern safeguarding of assets and ensuring the reliability of the financial

statements.

a. True

b. False

135. A company’s internal control system is designed by its external auditors.

a. True

b. False

136. The only reason a company needs to create an internal control system is to deter intentional fraudulent acts.

a. True

b. False

137. A good system of internal controls requires that the physical custody of assets be separated from the accounting

for those assets. This concept is known as safeguarding assets and records.

a. True

b. False

138. If a company hires honest employees, no internal control procedures are necessary.

a. True

b. False

139. As part of good internal control, disbursements can be made either by check or cash.

a. True

b. False

140. Most merchandisers receive checks and currency from customers in two ways: (1) cash received over the

counter from cash sales and (2) cash received in the mail from credit sales.

a. True

b. False

Chapter 6: Cash and Internal Control

141. Only one copy of the prelist should be prepared when an employee opens mail with customer payments to

avoid complexity in the accounting system and maintain control.

a. True

b. False

142. The use of customer statements as a control device will be effective only if the employees responsible for the

custody of cash received through the mail, for record keeping, and for authorization of adjustments to customers’

accounts are not allowed to prepare and mail statements to customers.

a. True

b. False

143. A purchase order is not the basis for recording a purchase and a liability.

a. True

b. False

144. Typically the classification known as readily available refers to investments that are converted into cash in

_______________ months or less.

145. The IFRS definition of cash equivalents is very similar to that used by .

146. are those investments that are readily convertible into known amounts of cash and that

have an original maturity to the investor of three months or less.

147. describes a form used by the accountant to reconcile the balance shown on

the bank statement for a particular account with the balance shown in the accounting records.

148. A check written by a company but not yet presented to the bank for payment is called a(n)

_________________________.

149. Items that are included on a bank statement and increase the bank account balance are called

_________________________.

150. A check that is returned or “bounces” because of insufficient funds is called a(n) .

Chapter 6: Cash and Internal Control

151. An amount recorded as an increase in the company‘s cash account at month-end, but which has not yet been

reflected on the bank statement is called a(n) .

152. Items that are included on a bank statement and decrease the bank account balance are called

_________________________.

153. If a company records a $310 receipt as $130, this type of error is called a(n) .

154. The audit committee of the board of directors provides direct contact between the

______________________________ and the ________________________________________.

155. is the body created by the Sarbanes-Oxley Act that was given the authority to set

auditing standards in the United States.

156. The is a subset of the board of directors that acts as a direct contact between

the stockholders and the independent accounting firm.

157. is a report required by section 404 of the Sarbanes-Oxley Act.

158. controls within a company are more concerned with efficient operations and

the adherence to management policies than with the accurate reporting of financial information.

159. controls primarily concern safeguarding of assets and ensuring the reliability of

the financial statements.

160. are the crucial link between economic transactions entered into by

an entity and the accounting for these events.

161. A(n) is a form that a department uses to initiate a request to order merchandise.

162. A(n) is a form sent by the purchasing department to the supplier.

Chapter 6: Cash and Internal Control

163. A(n) is a form sent by the seller to the buyer as evidence of a sale.

164. A(n) is a form used by the receiving department to account for the quantity and

condition of merchandise received from a supplier.

165. A(n) is a form the accounting department uses before making payment to document

the accuracy of all information about a purchase.

166. Select the action that matches the category of internal control procedures. (Select all that apply.)

Independent review and appraisal

a. One department should check on another

b. Internal audit staff ensure all is working as intended

c. Accounting and cash collection is properly separated

d. Blank checks are locked at all times when not in use

e. Origination of initial entry into accounting system

f. Specific authority is given by management for the performance of activities

167. French Corp. began the year with $18,000 in cash and another $6,500 in cash equivalents. During the year,

operations generated $132,000 in cash. Net cash used in investing activities during the year was $213,000, and the

company raised a net amount of $168,000 from financing activities.

REQUIRED:

Determine the year-end balance in cash and cash equivalents.

Chapter 6: Cash and Internal Control

168. Lower Enterprises invested its excess cash in the following instruments during December 2014:

Certificate of deposit, due January 31, 2017

$ 85,000

Certificate of deposit, due March 30, 2015

120,000

Commercial paper, original maturity date February 28, 2015

105,000

Deposit into a money market fund

45,000

Investment in stock

55,000

90–day Treasury bills

110,000

Treasury note, due December 1, 2042

REQUIRED:

400,000

Determine the amount of cash equivalents that should be combined with cash on the company’s balance sheet at

December 31, 2014, and for purposes of preparing a statement of cash flows for the year ended December 31,

2014.

Chapter 6: Cash and Internal Control

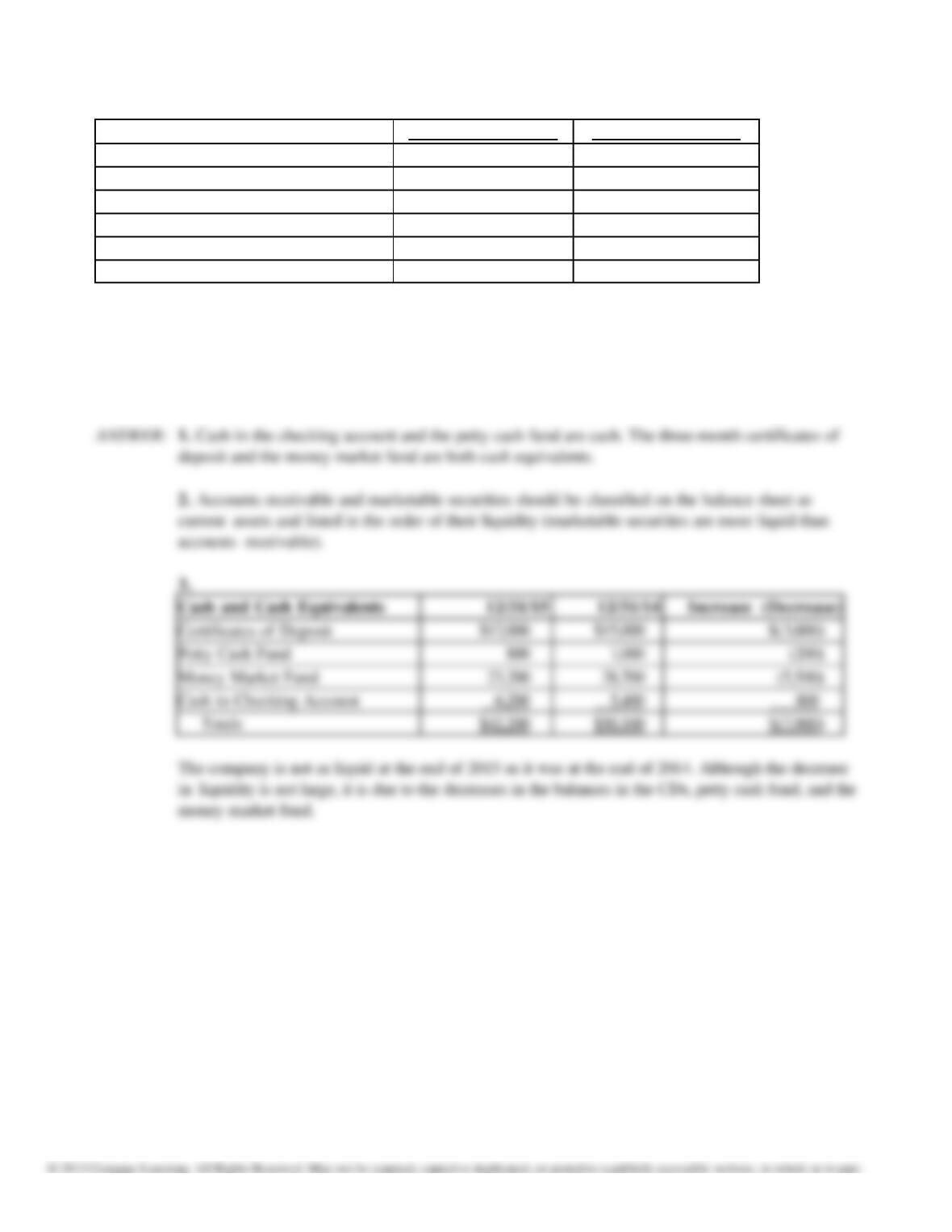

169. The following accounts are listed in a company’s general ledger:

December 31, 2015

December 31, 2014

Accounts Receivable

$12,300

$10,000

Certificates of Deposit (three months)

12,000

15,000

Marketable Securities

4,500

4,000

Petty Cash Fund

800

1,000

Money Market Fund

23,200

28,700

Cash in Checking Account

6,200

5,400

REQUIRED:

1. Which items are cash equivalents?

2. Explain where items that are not cash equivalents should be classified on the balance sheet.

3. What are the amount and the direction of change in cash and cash equivalents for 2015? Is the company as

liquid at the end of 2015 as it was at the end of 2014? Explain your answer.

Certificates of Deposit

Petty Cash Fund

(200)

Money Market Fund

Cash in Checking Account

6,200

5,400

800

Chapter 6: Cash and Internal Control

170. Houston Corp. prepares monthly bank reconciliations of its checking account balance. The bank statement for July

2014 indicated the following:

Balance, July 31, 2014

$63,400

Service charge for July

160

Interest earned during July

100

NSF check from Black Corp. (deposited by Houston)

1,150

Note ($3,000) and interest ($80) collected for Houston from a

customer of Houston’s

3,080

An analysis of canceled checks and deposits and the records of Houston revealed the following items:

Checking account balance per Houston’s books

$58,770

Outstanding checks as of July 31

4,630

Deposit in transit at July 31

1,780

Error in recording check #205 issued by Houston

90

The correct amount of check #205 is $540, but it was recorded as a cash disbursement of $450. The check was

issued to pay for merchandise purchases. The check appeared on the bank statement correctly.

A) Prepare a bank reconciliation schedule at July 31, 2014, in proper form.

B) What amount would Houston report on its balance sheet at July 31, 2014, for cash?

Balance per bank statement

Add: deposit in transit

Less: outstanding checks

Total

Balance per books

Add: interest earned

Add: note ($3,000) and interest ($80) collected by the bank

Less: NSF check

Less: service charges

Correction of error-check for $540 recorded as $450

Total

Chapter 6: Cash and Internal Control

171. Winslet Corp. prepares monthly bank reconciliations of its checking account balance. The bank statement for

May, 2014, indicated the following:

Balance, May 31, 2014

$29,700

Service charge for May

80

Interest earned during May

120

NSF check from Viacon Corp. (deposited by Winslet)

230

Note ($4,000) and interest ($100) collected for Winslet from a

customer of Winslet’s

4,100

An analysis of canceled checks and deposits and the records of Winslet Corp. revealed the following items:

Checking account balance per Winslet’s books

$26,040

Outstanding checks as of May 31

2,950

Deposit in transit at May 31

3,110

Error in recording check # 4456 issued by Winslet

90

The correct amount of check #4456 is $760. It was recorded as a cash disbursement of $670 by mistake. The

check was issued to pay for merchandise purchases. The check appeared on the bank statement correctly.

A) Prepare a bank reconciliation schedule at May 31, 2014 in proper form.

B) Explain how checking accounts, bank statements, and bank reconciliations are used by Winslet to control

its cash.

Balance per bank statement

Add: deposit in transit

Less: outstanding checks

Total

Balance per books

Add: interest earned

Add: note ($4,000) and interest ($100) collected by the bank

Less: NSF check

Less: service charges

Correction of error-check for $760 recorded as $670

Total