198. Which of the following accounts would be included in the chart of accounts of a merchandising company

using the: (a) periodic inventory system, (b) perpetual inventory system, or (c) both systems?

(1) Sales Discounts

(2) Merchandise Inventory

(3) Sales

(4) Purchases Discounts

(5) Cost of Merchandise Sold

(6) Freight In

(7) Delivery Expense

(8) Sales Returns and Allowances

199. Journalize the following transactions for Armour Inc. using both the periodic inventory system and the

perpetual inventory system, presented in a side-by-side format shown at the end of this exercise.

Oct.7 Sold merchandise on credit to Rondo Distributors, terms n/30, FOB destination, $1,200; the cost of the

merchandise was $720.

Oct. 8 Purchased merchandise, $10,000, terms FOB shipping point, 2/15, n/30, with prepaid freight charges of

$525 added to the invoice.

PERIODIC INVENTORY

PERPETUAL INVENTORY

Accounts

DR

CR

|

DR

CR

|

|

|

|

|

|

|

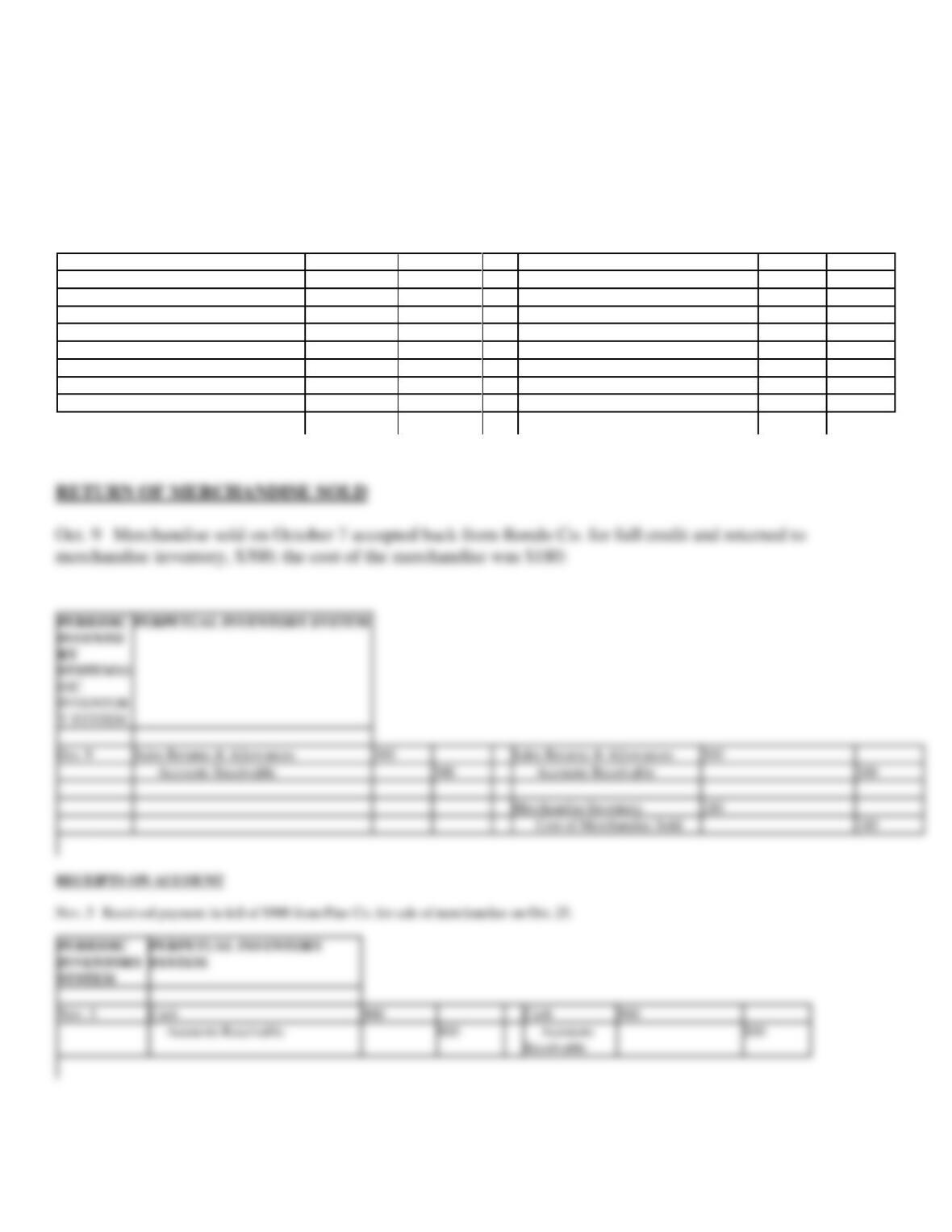

200. Journalize the following transactions for Dulcimer Inc. using both the periodic inventory system and the

perpetual inventory system, presented in a side-by-side format shown at the end of this exercise.

Oct. 9 Merchandise sold on October 7 accepted back from Rondo Co. for full credit and returned to

merchandise inventory, $300; the cost of the merchandise was $180.

Nov. 5 Received payment in full of $900 from Pine Co. for sale of merchandise on Oct. 25.

PERIODIC INVENTORY

PERPETUAL INVENTORY

Accounts

DR

CR

|

DR

CR

|

|

|

|

|

|

|

Oct. 9

Sales Returns & Allowances

Sales Returns & Allowances

Accounts Receivable

Accounts Receivable

Merchandise Inventory

Cost of Merchandise Sold

Nov. 5

Cash

Cash

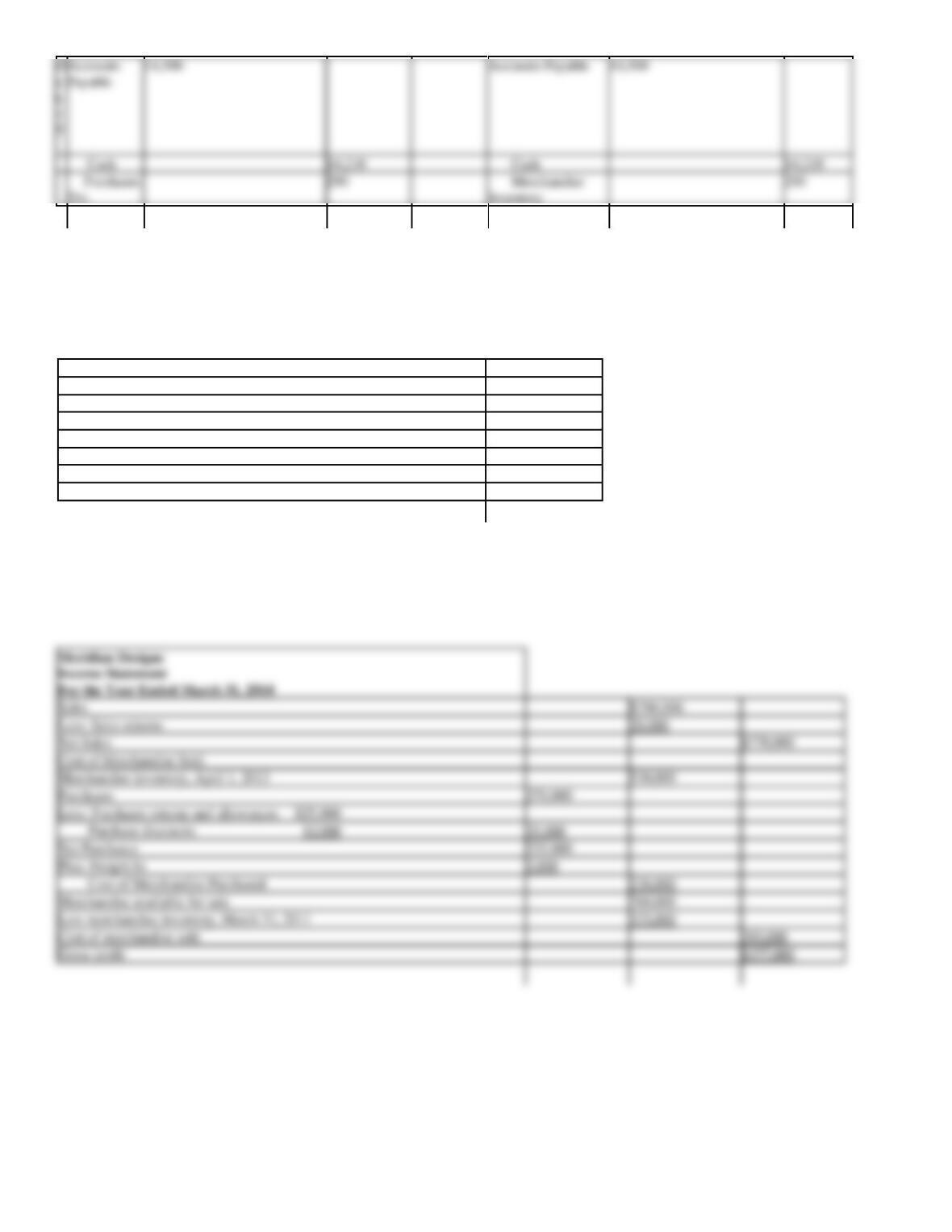

201. Journalize the following transactions for Donnell Inc. using both the periodic inventory system and the

perpetual inventory system, presented in a side-by-side format shown at the end of this exercise.

Oct. 5 Purchased $18,000 of merchandise from Rex on account, terms 2/10, n/30.

Oct. 8 Returned merchandise purchased on account on Oct. 5 amounting to $3,500.

Oct. 15 Paid for purchase of Oct. 5, less Oct. 8 return and purchase discount.

PERIODIC INVENTORY

PERPETUAL INVENTORY

Accounts

DR

CR

|

DR

CR

|

|

|

|

|

|

|

|

|

|

SYSTEM

INVENTORY SYSTEM

Oct. 8

Accounts Payable

3,500

Accounts Payable

3,500

202. The following data were extracted from the accounting records of Meridian Designs for the year ended

March 31, 2014.

Merchandise Inventory, April 1, 2013

$530,000

Merchandise Inventory, March 31, 2014

375,000

Purchases

270,000

Purchase Returns and Allowances

25,000

Purchase Discounts

10,000

Sales

790,000

Sales Returns

20,000

Freight In

3,000

Prepare the cost of merchandise sold section of the income statement for the year ended March 31, 2014, using the periodic method. Also determine

gross profit.

Sales

$790,000

Less: Sales returns

20,000

Net Sales

$770,000

Cost of Merchandise Sold

Merchandise inventory, April 1, 2013

530,000

Purchases

270,000

Less: Purchases returns and allowances $25,000

Purchase discounts 10,000

35,000

Net Purchases

235,000

Plus: Freight In

3,000

Cost of Merchandise Purchased

238,000

Merchandise available for sale

768,000

Less merchandise inventory, March 31, 2011

375,000

Cost of merchandise sold

393,000

Gross profit

$377,000

Cash

14,210

Cash

14,210

203. The following data for the current year ended June 30 were extracted from the accounting records of Excel

Co.:

Admisitrative Expenses

$28,750

Cost of merchandise sold

181,440

Interest Expense

3,600

Rent Revenue

1,500

Sales

548,000

Sales Returns and Allowances

9,000

Sales Discounts

4,560

Selling Expenses

65,000

Prepare a multiple-step income statement for the year ended June 30, 2014.

Sales

$548,000

Less: Sales Returns and Allowances

9,000

Sales Discounts

4,560

Net sales

534,440

Cost of merchandise sold

181,440

Gross profit

353,000

Operating expenses;

Selling Expenses

65,000

Administrative Expenses

28,750

Total Operating Expenses

93,750

Income from Operations

259,250

Other income and expense:

Rent revenue

1,500

Interest expense

3,600

Net income

$257,150

204. Selected data from the ledger of Morrison Co. after adjustment at September 30, 2011 the end of the fiscal

year, are listed as follows:

Accounts Receivable

$ 39,120

Office Equipment

$ 82,700

Accumulated Depreciation

60,540

Prepaid Insurance

4,680

Administrative Expenses

90,000

Note Payable

77,750

Bob Morrison, Capital

85,000

Salaries Payable

3,060

Cost of Merchandise Sold

550,000

Sales (net)

950,000

Bob Morrison, Drawing

65,000

Selling Expenses

102,000

Interest Revenue

10,000

Supplies

3,125

Prepare an income statement, using the single-step form, and a statement of owner’s equity.

Revenues:

Net sales

$950,000

Interest revenue

10,000

Total revenues

$960,000

Expenses:

Cost of merchandise sold

$550,000

Selling expenses

102,000

Administrative expenses

90,000

Total expenses

742,000

Net income

$ 218,000

Bob Morrison, capital, October 1, 2010

$85,000

Net income for the year

$218,000

Less withdrawals

65,000

Increase in owner’s equity

153,000

Bob Morrison, Capital, September 30, 2011

$238,000

205. Prepare (a) a single-step income statement, (b) a statement of owner’s equity, and (c) a balance sheet in

report form from the following data for Kooper Co., taken from the ledger after adjustment on December 31,

2010 the end of the fiscal year.

Accounts Payable

$ 97,200

Accounts Receivable

64,300

Accumulated Depreciation – Office Equipment

72,750

Accumulated Depreciation – Store Equipment

162,100

Administrative Expenses

56,500

Maeve Kooper, Capital

81,750

Cash

53,000

Cost of Merchandise Sold

121,700

Maeve Kooper, Drawing

52,000

Interest Expense

12,000

Merchandise Inventory

93,250

Note Payable, Due 2012

154,000

Office Equipment

149,750

Prepaid Insurance

6,500

Rent Revenue

17,500

Salaries Payable

28,700

Sales (net)

365,500

Selling Expenses

41,500

Store Equipment

325,000

Supplies

4,000

(a)

Revenues:

Net sales

$365,500

Rent revenue

17,500

Total revenues

$383,000

Expenses:

Cost of merchandise sold

$121,700

Selling expenses

41,500

Administrative expenses

56,500

Interest expense

12,000

Total expenses

231,700

Net income

$ 151,300

(b)

Maeve Kooper, capital, January 1, 2010

$81,750

Net income for year

$151,300

206. Prepare a multiple-step income statement for Armour Co. from the following data for the year ended

December 31, 2014.

Sales, $790,000; cost of merchandise sold, $330,000; administrative expenses, $35,000; interest expense,

$20,000; rent revenue, $25,000; sales returns and allowances, $35,000; selling expenses, $50,000.

207. Which of the following costs would be included in merchandise inventory?

(a)

Purchase price

(b)

Insurance in transit FOB shipping point

(c)

Freight for delivery FOB shipping point

(d)

Repair due to negligence of receiving clerk

(e)

Receiving Department employee salary

(f)

Cost of processing purchase orders

Revenue from sales:

Sales

$790,000

Less: Sales returns and allowances

35,000

Net sales

$755,000

Cost of merchandise sold

330,000

Gross profit

$425,000

Operating expenses:

Selling expenses

$50,000

Administrative expenses

35,000

Total operating expenses

85,000

Income from operations

$340,000

Other income:

Rent revenue

$ 25,000

Other expense:

Interest expense

20,000

5,000

Net income

$345,000

208. For each of the following, calculate the cost of inventory reported on the balance sheet.

(a)

The total merchandise on hand at the end of the year as determined by taking a physical inventory is $62,000. Of the $62,000, $8,000

has been sold FOB destination and is awaiting pickup by the carrier.

(b)

The total merchandise inventory counted at the end of the year was $63,000. Purchases for $6,000 are in transit under FOB shipping

point terms.

(c)

The total merchandise inventory counted at the end of the year was $75,000. Purchases for $5,000 are in transit under FOB destination

terms.

209. Using the perpetual inventory system, journalize the entries for the following selected transactions:

(a)

Sold merchandise on account, for $12,000. The cost of the merchandise sold was $6,500.

(b)

Sold merchandise to customers who used MasterCard and VISA, $9,500. The cost of the merchandise sold was $5,300.

(c)

Sold merchandise to customers who used American Express, $2,900. The cost of the merchandise sold was $1,700.

(d)

Paid an invoice from First National Bank for $385, representing a service fee for processing MasterCard and VISA sales.

(e)

Received $4,325 from American Express Company after a $115 collection fee had been deducted.

(a)

Accounts Receivable

12,000

Sales

12,000

Cost of Merchandise Sold

6,500

Merchandise Inventory

6,500

(b)

Cash

9,500

Sales

9,500

Cost of Merchandise Sold

5,300

Merchandise Inventory

5,300

Sales

2,900

Cost of Merchandise Sold

1,700

Merchandise Inventory

1,700

(d)

Credit Card Expense

Cash

(e)

Cash

4,325

(a)

$62,000

(b)

$69,000

(c)

$75,000

210. Merchandise with a list price of $4,200 and costing $2,300 is sold on account, subject to the following

terms: FOB destination, 2/10, n/30. The seller prepays the freight costs of $85 (debit Freight Out for the freight

costs). Prior to payment for the goods, the seller issues a credit memo for $750 to the customer for

merchandise costing $425 that is returned. The correct amount is received within the discount period. The

company uses a perpetual inventory system.

Record the foregoing transactions of the seller in the sequence indicated below.

(a)

Sold the merchandise, recognizing the sale and cost of merchandise sold.

(b)

Paid the freight charges.

(c)

Issued the credit memo.

(d)

Received payment from the customer.

(a)

Accounts Receivable

4,200

Sales

3,800

Cost of Merchandise Sold

2,300

Merchandise Inventory

2,300

(b)

Freight Out

Cash

(c)

Sales Returns and Allowances

Accounts Receivable

Merchandise Inventory

(d)

Cash

3,381

Sales Discounts

Accounts Receivable

3,450

211. Based on the information below, journalize the entries for the Seller and the Buyer. Both use a perpetual

inventory system.

(a)

Seller sold merchandise on account to the buyer, $4,750, terms 2/10, net 30, FOB shipping point. The cost of the merchandise is

$2,850. The seller prepays the freight of $75.

(b)

Buyer returns $ 700 of merchandise as defective. The cost of the merchandise is $420.

(c)

Buyer pays within the discount period.

Seller

Buyer

Accounts

DR

CR

DR

CR

Accounts Receivable

4,750

Merchandise Inventory

4,750

Cost of Merchandise Sold

2,850

Merchandise Inventory

2,850

Accounts Receivable

Merchandise Inventory

Cash

Accounts Payable

Sales Returns & Allow.

Accounts Payable

Accounts Receivable

Merchandise Inventory

Merchandise Inventory

Cost of Merchandise

Sold

Cash

3,969

Accounts Payable

4,050

Sales Discounts

Merchandise Inventory

Accounts Receivable

4,050

Cash

3,969

212. Details of a purchase invoice and related credit memo are summarized as follows:

Invoice:

Cost of merchandise listed on purchase invoice

$6,500

Prepaid freight charge added to invoice

150

Terms, FOB shipping point, 1/10, n/eom

Credit memo: Cost of merchandise returned

$1,500

Assume that the credit memo was received prior to payment and that the invoice is paid within the discount period. Determine the following:

(a)

Amount of the cash discount allowed.

(b)

Amount to be paid by the purchaser if the discount is taken.

(c)

Cost of the merchandise to the purchaser if the discount is NOT taken.

213. Conquest Company uses a perpetual inventory system. Conquest purchased $1,500 of merchandise on

account and payment was made within the discount period. The credit terms were 2/10,n/30. Journalize

Conquest’s purchase and payment.

(a)

Merchandise Inventory

1,500

Accounts Payable

1,500

(b)

Accounts Payable

1,500

Cash

1,470

Merchandise Inventory

30

(a)

$50

(b)

$5,100

(c)

$5,150