Chapter 5: Inventories and Cost of Goods Sold

184. The cost of goods sold for Johnnie, Inc. totaled $1,305,000. Sales returns and purchase returns were $3,000 and

$4,000, respectively. Purchases totaled $1,300,000. Discounts taken by Johnnie totaled $7,000, while discounts

taken by customers totaled $5,000. Beginning inventory was $90,000. Determine the amount of ending inventory to

be reported on Johnnie, Inc.’s balance sheet.

185. Gently Used Cars is a dealer that uses the periodic inventory system. The data presented below is from the

accounting records of Gently for the year ended December 31, 2014.

Sales

$585,000

Sales Discounts

3,000

Purchases

420,000

Purchase Returns

5,000

Inventory (January 1)

33,000

Inventory (December 31)

37,000

Operating Expenses

146,000

Transportation-in

10,000

Retained Earnings (January 1)

71,000

Using the amounts provided above, calculate the cost of goods sold for 2014.

Carlton, Inc.

Carlton, Inc. reported the following information for 2015 and 2014:

2015

2014

Sales

$951,200

$890,000

Sales discounts

12,000

23,000

Purchases

580,000

600,000

Inventory, December 31

46,000

40,000

Transportation-in

18,000

19,000

Purchase discounts

4,000

5,000

186. Refer to the information for Carlton, Inc.

How much is the cost of purchases for 2015?

187. Refer to the information for Carlton, Inc.

What amount is cost of goods available for sale for 2015?

Chapter 5: Inventories and Cost of Goods Sold

188. Refer to the information for Carlton, Inc.

How much is cost of goods sold for 2015?

189. Refer to the information for Carlton, Inc.

How much is net sales for 2015? What other components that Carlton did not report could be included in this

computation?

190. Refer to the information for Carlton, Inc.

How much of every dollar is gross profit for 2015?

Cooking Corner

Cooking Corner reported inventory on its balance sheet at December 31, 2013 at $32,000. During 2014, Cooking

Corner purchased goods totaling $634,000 on account with terms of 2/10, n/30, FOB shipping point. Total charges

paid by Cooking Corner directly to the freight company were $1,000. At the end of 2014, inventory on hand totaled

to $45,000. Net sales for 2014 totaled $1,300,000. Cooking Corner employs a periodic inventory system.

191. Refer to the information about Cooking Corner.

How much would Cooking Corner pay its supplier if Cooking Corner paid for one-half of the goods acquired within

the discount period, and the other half after the expiration of the discount period?

192. Refer to the information about Cooking Corner.

How much is cost of goods available for sale for 2014 assuming Cooking Corner takes advantage of one-half of the

cash discounts?

193. Refer to the information about Cooking Corner.

How much is Cooking Corner’s cost of goods sold assuming that Cooking Corner takes advantage of one-half of

the cash discount?

Chapter 5: Inventories and Cost of Goods Sold

Digital Forces

Selected data from the financial statements for Digital Forces is presented below.

Net Sales—2015

$200,000

Cost of Sales—2015

136,000

Selling, General & Administrative Expenses—2015

63,000

Other Operating Expenses—2015

600

Income Taxes—2015

3,000

Inventories—Dec. 31, 2014

11,000

Inventories—Dec. 31, 2015

13,000

Retained Earnings—Dec. 31, 2015

39,000

194. Refer to the financial statement information for Digital Forces.

Determine the dollar amount of cost of goods purchased for Digital Forces for 2015.

195. Refer to the financial statement information for Digital Forces.

What portion of every dollar is available to cover operating costs and to contribute to profits for 2015?

196. The following data is available for one of the products sold by Wild Optics Company, which uses the periodic

inventory system:

Dec. 1

On hand, 10 units at $8.00 each

$ 80

5

Purchased 30 units at $7.80 each

234

18

Purchased 40 units at $8.15 each

326

24

Purchased 20 units at $8.25 each

165

Available for sale during December—100 units

$805

At the end of December, Wild Optics had 25 units on hand. The 75 units sold created revenue of $13 each.

Determine the amounts for the December 31 ending inventory, the cost of goods sold for December, and the gross

margin for December for each of the inventory costing methods listed below.

Ending Inventory

Cost of Goods Sold

Gross Profit

a. Weighted average

b. FIFO

c. LIFO

Chapter 5: Inventories and Cost of Goods Sold

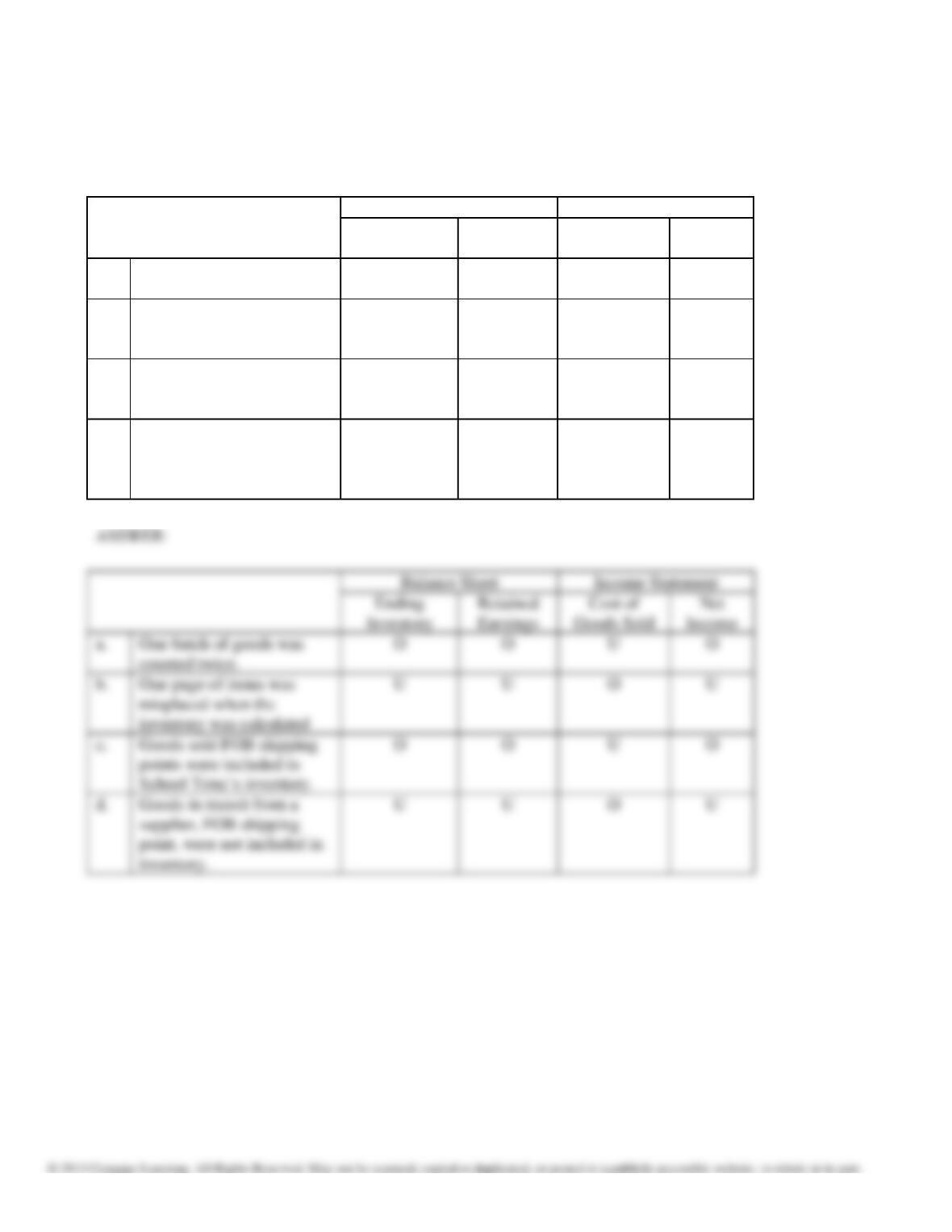

197. School Time Corp. completed a physical inventory at the end of 2014. A review of the physical inventory

procedures and records uncovered several errors that are described below. In the columns provided, indicate the

effect, if any, on the four financial statement items listed. Use the following codes for your answers:

O Overstatement U Understatement NE No Effect

Balance Sheet

Income Statement

Ending

Inventory

Retained

Earnings

Cost of

Goods Sold

Net

Income

a.

One batch of goods was

counted twice.

b.

One page of items was

misplaced when the

inventory was calculated

c.

Goods sold FOB shipping

point were included in

School Time’s inventory.

d.

Goods in transit from a

supplier, FOB shipping

point, were not included in

inventory.

Balance Sheet

Income Statement

Goods sold FOB shipping

points were included in

Chapter 5: Inventories and Cost of Goods Sold

198. The cost of Garmin Corp.’s inventory at the end of the year was $85,000; however, due to obsolescence, the cost to

replace the inventory was only $65,000. Prepare the journal entry needed at the end of the year.

199. Carrington, Inc. began the year with $130,000 in merchandise inventory and ended the year with $190,000. Sales

and cost of goods sold for the year were $900,000 and $640,000, respectively. (Use a 360 day year in your

calculations.)

Required:

1. Compute Carrington‘s inventory turnover ratio.

2. Compute the number of days’ sales in inventory.

Learning Tree, Inc.

The following data is available for one of the products sold by Learning Tree, Inc., which uses the perpetual

inventory system:

May 1 On hand, 1,000 units at $2.00 each $2,000

5 Purchased 2,000 units at $2.75 each 5,500

10 Sold 2,500 units at $16 each

18 Purchased 2,000 units at $4.00 each 8,000

24 Sold 1,500 units at $12 each

31 On hand, 1,000 units

200. Refer to the data for Learning Tree, Inc.

If the moving average method is used, what is the amount assigned to cost of goods sold for the 2,500 units sold on

May 10?

Chapter 5: Inventories and Cost of Goods Sold

201. Refer to the data for Learning Tree, Inc.

If the moving average method is used, what is the amount assigned to the ending inventory on May 30?

202. Refer to the data for Learning Tree, Inc.

If the LIFO method is used, what is the amount assigned to cost of goods sold for the 2,500 units sold on May 10?

203. Refer to the data for Learning Tree, Inc.

If the LIFO method is used, what is the amount assigned to the ending inventory on May 30?

204. Refer to the data for Learning Tree, Inc.

Explain why the amounts for ending inventory are different under the two average cost methods—weighted

average (periodic) and moving average (perpetual).

205. Refer to the data for Learning Tree, Inc.

Explain why the amounts are different for LIFO under periodic and perpetual inventory systems.

Share, Inc.

The following data is available for one of the products sold by Share, Inc., which uses a perpetual inventory system.

May 1 On hand, 10 units at $2 each

8 Sold 6 units at $10 each

14 Purchased 30 units at $3 each

23 Sold 24 units at $10 each

206. Refer to the data for Share, Inc.

If the moving average method is used, how much is cost of goods sold for May?

Chapter 5: Inventories and Cost of Goods Sold

207. Refer to the data for Share, Inc.

If the moving average method is used, how much is ending inventory on May 30?

208. Refer to the data for Share, Inc.

Required:

1. If the FIFO method is used, how much is ending inventory on May 30?

2. How does this differ from the amount calculated using a periodic system and FIFO?

209. Refer to the data for Share, Inc.

If the LIFO method is used, how much is cost of goods sold for May?

210. Describe how the inventories of manufacturers differ from the inventories of retailers.

211. Several transactions of sales and purchase activities for Genoa Department Store are described below.

A) Genoa purchases shoes from Nike on credit.

B) Genoa returns defective shoes to Nike before payment is made to Nike for the shoes

purchased in transaction A.

C) Genoa pays for the shoes purchased from Nike.

D) Genoa sells shoes to its customers for cash and on credit.

E) Credit customers return shoes to Genoa for a refund.

F) Credit customers pay their account balances to Genoa.

REQUIRED: For each transaction described above, describe the economic effects of the transaction on the

company under a periodic inventory system.

Chapter 5: Inventories and Cost of Goods Sold

212. Flores Department Store currently uses the periodic inventory system.

REQUIRED: Explain what the advantages would be to Flores if it uses the perpetual inventory system. Assume

that Flores can use a computer system which is linked to its cash registers and that all products have bar codes that

can be read by bar code readers attached to the cash registers.

213. Giant-Mart purchased a big shipment of shoes from Right Balance, Inc. on credit near the end of its accounting

period. Right Balance shipped the shoes in January and Giant-Mart received the shoes in February. Assume that

Giant-Mart’s accounting period ends on January 31, while Right Balance’s accounting period ends on May 31.

REQUIRED: If the shoes are shipped FOB destination, who will pay the freight costs? If the shoes are shipped

FOB shipping point, who will pay the freight costs?

214. Giant-Mart purchased a large shipment of shoes from Primus, Inc. on credit near the end of its accounting period.

Primus shipped the shoes in January and Giant-Mart received the shoes in February. Assume that Giant-Mart’s

accounting period ends on January 31, while Primus’ accounting period ends on May 31. Answer each independent

question in the set that follows.

REQUIRED: If the shoes are shipped FOB destination, when should Giant-Mart record the purchase? If the

shoes are shipped FOB shipping point, when should Giant-Mart record the purchase?

215. Giant-Mart purchased a large shipment of shoes from Primus, Inc. on credit near the end of its accounting period.

Primus shipped the shoes in January and Giant-Mart received the shoes in February. Assume that Giant-Mart’s

accounting period ends on January 31, while Giant’s accounting period ends on May 31. Answer each independent

question in the set that follows.

REQUIRED: Under what shipping terms would Giant-Mart include the shoes as part of inventory on its January

31 balance sheet?

Chapter 5: Inventories and Cost of Goods Sold

216. Explain the relationship between the valuation of inventory and income measurement as it relates to the balance

sheet and the income statement.

217. In the following information from the 2015 annual reports of Focal Point Industries all figures have been rounded to

millions of dollars.

Balance Sheet Data

May 31, 2015

May 31, 2014

Raw materials

$ 25.8

$ 52.1

Work in process

44.8

34.7

Finished goods

1,132.7

1,303.8

Inventories at FIFO

1,203.3

1,390.6

Adjustment to LIFO

5.6

21.9

Cash Flow Data (Operating Activities)

Net income

$451.4

$399.9

Additions to net income:

Depreciation

198.2

100.2

Amortization

30.6

49.0

Changes in assets and liabilities:

Inventories

197.3

(58.0)

Accounts payable and other

(170.4)

(70.1)

REQUIRED:

(1) Describe what costs are included in each of the three types of inventories listed above for Focal Point

Industries.

(2) Even though the footnote describing the inventory costing method(s) used by Focal Point Industries is not provided

above, what can you conclude about the inventory costing method(s) used by the company?

Chapter 5: Inventories and Cost of Goods Sold

218. In the following information from the 2015 annual reports of Focal Point Industries all figures have been rounded to

millions of dollars.

Balance Sheet Data

Raw materials

May 31, 2015

$ 25.8

May 31, 2014

$ 52.1

Work in process

44.8

34.7

Finished goods

1,132.7

1,303.8

Inventories at FIFO

1,203.3

1,390.6

Adjustment to LIFO

5.6

21.9

Cash Flow Data (Operating Activities)

Net income

$451.4

$399.9

Additions to net income:

Depreciation

198.2

100.2

Amortization

Changes in assets and liabilities:

Inventories

30.6

187.3

49.0

(58.0)

Accounts payable and other

(170.4)

(70.1)

REQUIRED:

(1) Explain what the amount “adjustment to LIFO” represents. What effects has this “adjustment” had on Focal

Point Industries’ net earnings in 2014 and 2015?

(2) What method of determining cash flows from operating activities has Focal Point Industries used in preparing its

statement of cash flows? Explain your answer.

(3) From 2014 to 2015, what change in the inventory balance (increase or decrease) occurred in each year as a

result of operating activities? What was the effect on the company’s cash flow each year as a result of the

inventory change?

Chapter 5: Inventories and Cost of Goods Sold

219. What is LIFO inventory liquidation? Why is it important to disclose the effects of a LIFO inventory liquidation

220. Carrington Inc. manufactures digital cameras and has experienced noticeable declines in the purchase price of

many of the components it uses, including memory components. Which inventory costing method should Carrington

use if it wants to maximize net income? Explain your answer.

221. If an entity overstates its ending inventory for the current year, what are the effects on assets, cost of goods sold,

income before taxes, and retained earnings for the current year?

222. Assume that a company is experiencing increasing inventory prices and prepares its financial statements in

accordance with IFRS. Which costing method should it use to pay the least amount of taxes? Explain your answer.

223. Bower Corp.’s cost of sales has remained steady over the last two years. During this same time period, however,

its inventory has increased considerably. What does this information tell you about the company’s inventory

turnover? Explain your answer.

Match the inventory-related accounts to costs that may be included in inventories for retailers and

manufacturers.

a. Merchandise Inventory

b. Raw Materials

c. Work in Process

d. Finished Goods

e. Cost of Goods Sold

Chapter 5: Inventories and Cost of Goods Sold

224. Cost of materials which are not yet entered into the production process.

225. Cost of completed, but unsold items.

226. Costs to purchase goods ready to sell.

227. Costs of direct materials, overhead, and direct labor used in unfinished goods.

228. Costs of direct materials, overhead, and direct labor used in goods that have been sold.

Match the terms with the descriptions related to merchandise sales and purchases.

a. Transportation-in

b. Perpetual inventory system

c. Net purchases

d. FOB Destination

e. Cost of goods available for sale

f. Periodic inventory system

g. FOB Shipping point

h. Delivery expense

229. Requires updating of the inventory account at the time of each purchase and each sale.

230. Shipping costs paid to acquire merchandise.

231. The seller is responsible for the cost of delivering the merchandise to the buyer.

232. Relies on a count of inventory on the last day of the year to determine amount on hand.

Chapter 5: Inventories and Cost of Goods Sold

233. The buyer must pay the shipping costs.

234. Sold merchandise on credit to customers.

235. Recorded cash sales for the day.

236. Gave a customer a cash refund.

237. Granted a customer a credit on its balance due for goods that were returned.

Match the costs that might be included as part of the cost of inventory to the listed accounting treatment.

a. Add to inventory cost

b. Subtract from inventory cost

c. Not an inventory cost

238. Invoice price paid for resale goods

239. Freight costs incurred by the buyer to ship goods to its place of business

240. Freight costs incurred by the seller to ship goods to its customers

241. Cost of storing the goods before they are sold to customers

242. Excise taxes paid on goods acquired

Chapter 5: Inventories and Cost of Goods Sold

243. Sales taxes paid on goods acquired

244. Income taxes paid on profits earned from selling goods to customers

245. Cost of insurance during transit to acquire inventory items

Identify which inventory costing method (LIFO or FIFO) achieves the effect listed in the following items:

a. LIFO

b. FIFO

246. Prices are rising; profits are higher with this method.

247. Prices are rising; cost of goods sold is lower with this method.

248. Prices are declining; income taxes are higher with this method.

249. Prices are declining; gross margin is higher with this method.

250. Which one of the following best explains the distinction between inventory and an operating asset?

a. ownership

b. intent

c. cost

d. purchase price

251. Which one of the following would not be found as an asset on the balance sheet of a manufacturer?

a. raw materials

b. work in process

c. finished goods

d. merchandise inventory

252. Finished goods are the equivalent of merchandise inventory for a retailer or wholesaler in that both represent the

inventory of goods held for sale.

a. True

b. False

Chapter 5: Inventories and Cost of Goods Sold

253. When inventory is sold by a wholesaler or retailer, it is recorded in a different account on the income statement

than a manufacturer would use.

a. True

b. False

254. Which one of the following statements is false regarding the gross profit ratio?

a. The gross profit ratio is calculated by dividing net sales by gross profit.

b. The gross profit ratio is a measure of profitability.

c. The gross profit ratio can help investors decide whether or not to buy a company’s stock.

d. The gross profit ratio should be compared with both a company’s prior years’ ratios and also competitor

ratios.

255. Which of the following would not be included in inventory costs?

a. Freight costs incurred by the buyer in shipping inventory to its place of business.

b. The cost of insurance taken out during the time that inventory is in transit.

c. The cost of storing inventory before it is ready to be sold.

d. Shelving to hold the inventory.

256. Assets are unexpired costs, and expenses are expired costs.

a. True

b. False

257. The value assigned to an asset such as inventory on the balance sheet determines the amount eventually recognized

as an expense on the income statement.

a. True

b. False

258. The effect of a misstatement of the year-end inventory is limited to the net income for that year.

a. True

b. False

259. If a company has a number of day’s sales in inventory equal to 60, that means that it takes about two months on

average to sell its inventory.

a. True

b. False

Chapter 5: Inventories and Cost of Goods Sold

260. Under the indirect method, an increase in accounts payable is added to net income to determine cash flow from

operating activities.

a. True

b. False

261. If the direct method is used to prepare the Operating Activities category of the statement of cash flows, the amount

of cash paid to suppliers of inventory is shown as an addition in this section of the statement.

a. True

b. False

262. The inventory costing method is applied after each sale of merchandise to update the Inventory account.

a. True

b. False

263. The lower the inventory turnover ratio, the less time inventory resides in storage.

a. True

b. False