5-15

6. The main ratio used by many financial analysts to examine a company’s short-term liquidity risk is the

current ratio. However, there are a number of problems that arise when this ratio is used to examine

short-term liquidity risk that may make the current ratio less useful than initially thought. Discuss the

interpretative problems of using the current ratio.

7. For each of the following factors, determine if the given change or level of that factor would lead an

analyst to believe that managers of a firm are more or less likely to engage in earnings manipulation:

Earnings Manipulation

More likely/less likely

1. Days Sales in Receivable Index increases

2. Gross Margin index decreases below 1

3. Asset Quality index increases

4. Depreciation index decreases to below 1

5. Leverage Index increases

8. One criticism of the interest and fixed charges coverage ratios as measures of long-term solvency risk

is that they use earnings rather than cash flows in the numerator. Detail how the interest coverage ratio

and fixed charges coverage ratio are calculated. In addition, discuss why using earnings in the

numerator is a problem and what method could be used to alleviate this problem.

ANS:

9. For each of the following scenarios, determine if it is an indicator of potential cash flow problems:

Potential future cash

flow problems

Yes/No

a.

Growth in accounts receivable or inventories that is less

the growth rate in sales.

b.

Increases in accounts payable that exceed the increase in

inventories.

c.

Capital expenditures that substantially exceed cash flow

from operations.

d.

Sales of marketable securities are less than purchases of

marketable securities.

e.

Other operating current liabilities that grow at a lesser

rate than sales.

f.

A reduction or elimination of dividend payments

g.

A substantial shift from long-term borrowing to short-

term borrowing.

b.

Increases in accounts payable that exceed the increase in

inventories.

c.

Capital expenditures that substantially exceed cash flow

from operations.

10. Discuss the differences between Chapter 7 and Chapter 11 bankruptcy filings?

11. What is the effect of the declaration of diviends have on the liquidity of a corporation?

PROBLEM

1. Given the following information, calculate for Year 2 the number of days of working capital financing

the firm will need to obtain from other sources?

Year 1

Year 2

Accounts Receivable, net

$ 518

$ 562

Accounts Payable

203

192

Inventory

535

564

Credit Sales

3,205

3,636

Cost of Goods Sold

2,037

2,294

Selling and Admin. Expense

1,081

1,131

5-18

2. Refer to the financial statement data for Patriot Corp. for 2011 and 2010. Complete the table by

computing the ratios.

Patriot Corp.

Balance Sheet

As of December 31,

2011

2010

Assets:

Cash and Cash Equivalents

$ 69,000

$ 55,250

Accounts Receivable

126,500

80,750

Inventory

92,000

63,750

Current Assets

287,500

199,750

Equipment

194,063

148,750

Less: Accumulated depreciation

-38,813

-29,750

Equipment-Net

155,250

119,000

Land

132,250

106,250

Total assets:

$575,000

$425,000

Liabilities:

Accounts Payable

$ 69,000

$ 42,500

Accrued Salaries Payable

51,750

42,500

Rent Expense Payable

35,750

28,500

Income Tax Payable

4,788

1,250

Current Liabilities

161,288

114,750

Long-term note payable

172,500

102,000

Total Liabilities

333,788

216,750

Stockholders’ Equity:

Common stock

115,000

89,250

Retained earnings

126,212

119,000

Total liabilities and stockholders’ equity:

$575,000

$425,000

Patriot Corp.

Income Statement

For the year ended December 31, 2011

Revenues

$ 373,750

Cost of goods sold

(224,250)

Gross Profit

$149,500

Operating Expenses

Depreciation expense

(9,062)

Salary expense

(56,063)

Insurance Expense

(44,850)

Rent Expense

(18,688)

Interest Expense

(6,120)

5-19

Total Operating Expenses

(134,783)

Income from Operations

14,717

Income Tax Expense

(4415)

Net income

$ 10,302

Dividends paid to Common Shareholders

$ 3,090

Financial Ratio to be calculated:

2011

2010

Current Ratio

Quick Ratio

Days Accounts Receivable

N/A

Days Inventory

N/A

Days Accounts Payable

N/A

Net Days Working Capital

N/A

Long-term Debt to Long-term Capital Ratio

Long-term Debt to Shareholders’ Equity ratio

Liabilities to Total Assets

Interest Coverage ratio

N/A

N/A – Not Applicable for the given year

3. Below is information from Darren Company’s 2012 financial statements.

As of Dec. 31, 2012

Dec. 31, 2011

Cash and short-term investments

$ 958,245

$ 745,800

Accounts Receivable (net)

125,850

135,400

Inventories

195,650

175,840

Prepaid Expenses and other current assets

45,300

30,860

Total Current Assets

$1,325,045

$1,087,900

Plant, Property and Equipment, net

1,478,320

1,358,700

Intangible Assets

125,600

120,400

2011

2010

5-20

Total Assets

$2,928,965

$2,567,000

Short-term borrowings

$ 25,190

$ 38,108

Current portion of long-term debt

45,000

40,000

Accounts payable

285,400

325,900

Accrued liabilities

916,722

705,891

Income taxes payable

125400

115600

Total Current Liabilities

$1,397,712

$1,225,499

Long-term Debt

450,000

430,000

Total Liabilities

$1,847,712

$1,655,499

Shareholders’ Equity

$1,081,253

$911,501

Total Liabilities and Shareholders’ Equity

$2,928,965

$2,567,000

Selected Income Statement Data – for the year ending December 31, 2012:

Net Sales

$3,210,645

Cost of Goods Sold

(2,310,210)

Operating Income

900,435

Net Income

324,850

Selected Statement of Cash Flow Data – for the year ending December 31, 2012:

Cash Flows from Operations

$584,750

Interest Expense

42,400

Income Tax Expense

114,200

Using this information calculate the following ratios:

2012

2011

Liabilities to Assets Ratio

Liabilities to Shareholders’ Equity Ratio

LT Debt to LT Capital Ratio

LT Debt to Shareholders’ Equity Ratio

Interest Coverage Ratio

N/A

Operating Cash Flow to Total Liabilities Ratio

N/A

4. Falcon Corporation has current assets of $400,000 and current liabilities of $275,000.

Liabilities to Assets Ratio

Liabilities to Shareholders’ Equity Ratio

LT Debt to LT Capital Ratio

LT Debt to Shareholders’ Equity Ratio

Interest Coverage Ratio

Operating Cash Flow to Total Liabilities Ratio

5-21

Required:

Compute the effect of each of the following transactions on Falcon’s current ratio:

a. Refinanced a $60,000 long-term mortgage with a short-term note.

b. Purchasing $108,000 of merchandise inventory with short-term accounts payable.

c. Paying $50,000 of short-term accounts payable.

d. Collecting $90,000 of short-term accounts receivable.

5 A. Hammer Corporation wrote off $185,000 of obsolete inventory at December 31, 2011.

Required:

What effect did this write-off have on the company’s 2011 current and quick ratios?

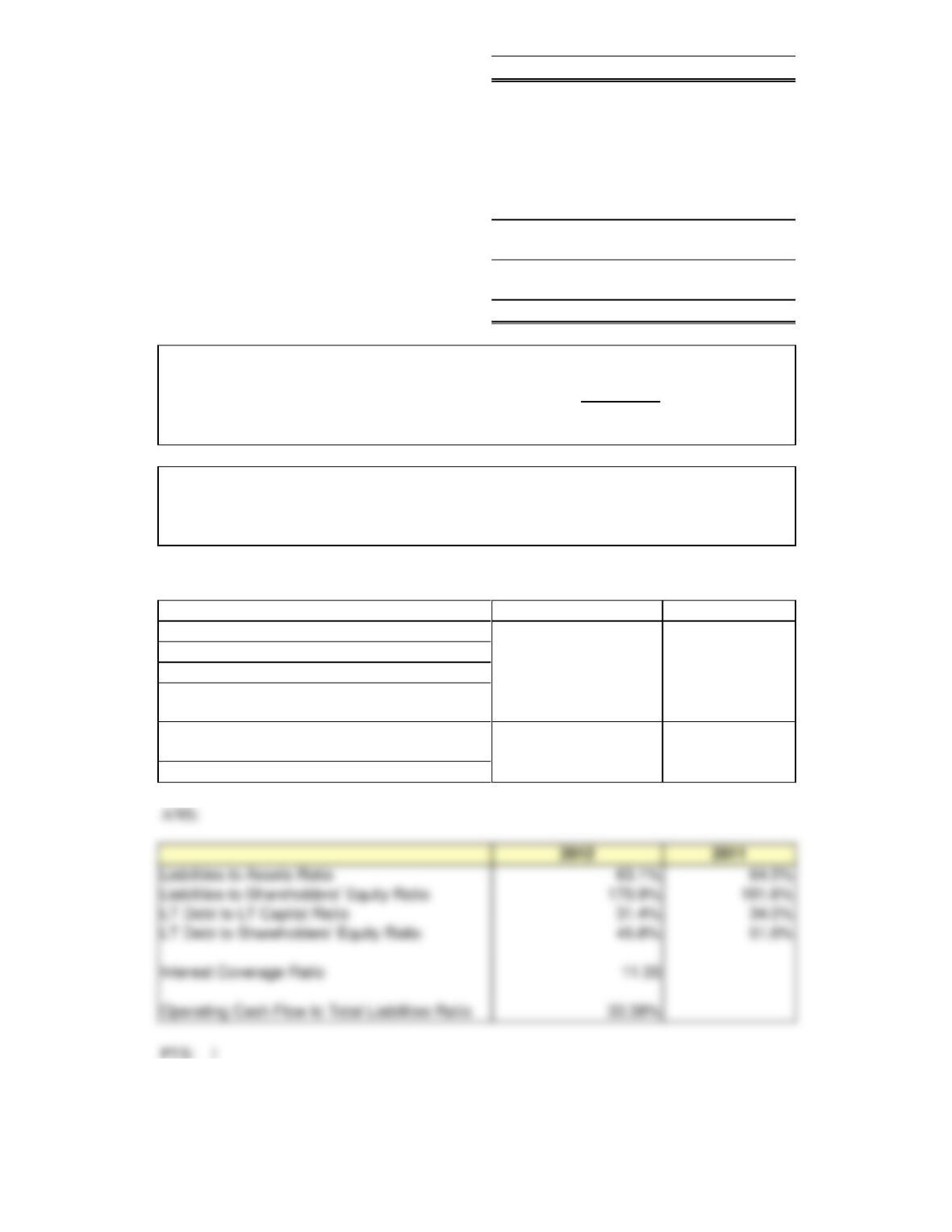

6. Selected risk ratios are presented for 2011 and 2010 for Techtron Company. Also, refer to the

financial statement data for the company.

2011

2010

Revenues to Cash Ratio

6.8

7.7

Days Revenues Held in Cash

54

47

Current Ratio

1.5

1.5

Quick Ratio

1.1

1.1

Operating Cash Flow to Average Current Liabilities

Ratio

47.3%

55.7%

Days Accounts Receivable

68

73

5-22

Days Inventory

51

68

Days Accounts Payable

47

49

Net Days Working Capital

72

91

Liabilities to Assets Ratio

0.559

0.621

Liabilities to Shareholders’ Equity Ratio

1.266

1.639

Long-Term Debt to Long-Term Capital Ratio

0.330

0.418

Long-Term Debt to Shareholders’ Equity Ratio

0.492

0.720

Operating Cash Flow to Total Liabilities Ratio

0.243

0.242

Interest Coverage Ratio

5.6

2.3

Financial Statements

INCOME STATEMENT (in millions)

Fiscal year end

2012

2011

2010

Sales

$2,500

$ 3,139

$ 2,816

Cost of Goods Sold

(1,252)

(1,288)

(1,099)

Selling, General & Admin. Exp.

Advertising

(387)

(364)

(297)

Research and Development

(157)

(143)

(154)

Royalty Expense

(223)

(248)

(296)

Other Selling and Administrative

(385)

(799)

(788)

Interest expense

(32)

(53)

(78)

Income tax expense

(64)

(69)

(29)

Net income

$ 196

$ 175

$ 75

Balance Sheet

Fiscal year end

2012

2011

2010

2009

ASSETS (in millions)

Cash

$ 625

$421

$ 496

$233

Accounts Receivable

579

607

555

572

Inventories

195

169

190

217

Prepayments

219

212

191

346

Total current assets

$1,618

$1,409

$1,432

$1,368

Property, plant & equipment

207

200

213

236

Other Assets

1,416

1,554

1,498

1,765

Total assets

$3,241

$3,163

$3,143

$3,369

LIABILITIES

Accounts payable

$ 168

$ 159

$ 166

$ 123

Short-term borrowing

342

24

223

36

Other current liabilities

584

749

578

599

Total current liabilities

$1,094

$ 939

$ 967

$ 758

Long term debt

303

687

857

1,166

Other noncurrent liabilities

149

141

128

92

Total liabilities

$1,546

$1,767

$1,952

$2,016

Common stock

$ 105

$ 105

$ 105

$ 105

Additional Paid-in Capital

381

398

458

455

Retained earnings

1,776

1,558

1,430

1,622

Accumulated Other Comprehensive Income

82

30

(47)

(68)

Treasury Stock

(649)

(695)

(755)

(761)

Total Shareholders’ equity

$1,695

$1,396

$1,191

$1,353

Total Liabilities & Shareholders’ Equity

$3,241

$3,163

$3,143

$3,369

STATEMENT OF CASH FLOWS (in millions)

Operations

2012

2011

2010

Net Income

$ 196

$ 175

$ 75

Depreciation & Amortization

146

164

184

(Increase) Decrease Accounts Receivables

28

(52)

17

(Increase) Decrease Inventories

(26)

21

27

(Increase) Decrease Prepayments

7

(21)

155

(Decrease) Increase Accounts Payable & Other

Current Liabilities

(90)

17

23

Net Addbacks and Subtractions from operations

(147)

112

221

Cash flows from operations

$ 195

$451

$480

Investing

Property Plant and Equipment acquired

($79)

($63)

($59)

Other Investing Transactions

(6)

(2)

(3)

Cash Flows from Investing

($85)

($65)

($62)

Financing

Increase in Common Stock

0

0

0

Increase (Decrease) in Short-term Borrowing

(318)

199

(187)

Increase (Decrease) in Long-term Borrowing

(384)

(170)

309

Acquisition of Common Stock

(46)

60

(6)

Dividends

(37)

(21)

(21)

Other Financing Transactions

879

243

(250)

Cash flow from Financing

$94

($311)

($155)

Change in Cash

$204

$75

$263

Cash – Beginning of Year

421

496

233

Cash – End of Year

$ 625

$ 421

$ 496

Required:

a. Calculate the amounts of these ratios for 2012.

b. Assess the changes in the short-term liquidity risk of Techtron between 2010 and

2012 and the level of that risk at the end of 2012.

c. Assess the changes in the long-term solvency risk of Techtron between 2010 and

2012 and the level of that risk at the end of 2012.

5-24

7. Below is selected data of Pronto Company:

Balance Sheet Data

As of December 31:

2012

2011

Accounts receivable

$671,000

$642,000

Allowance for doubtful accounts

31,000

22,000

Net accounts receivable

$640,000

$620,000

Inventories – LCM

$542,500

$642,500

Income Statement Data

Net credit sales

$3,150,000

$3,000,000

Net cash sales

800,000

600,000

Net sales

$3,950,000

$3,600,000

Cost of goods sold

$2,370,000

$2,160,000

Selling, general and adm. expenses

475,000

350,000

Other

150,000

125,000

Total operating expenses

$2,995,000

$2,635,000

Net income

$ 955,000

$ 965,000

Required:

a. What is the accounts receivable turnover for 2012?

b. What is the inventory turnover for 2012?

5-26

8. On January 1, 2012, Deputron Company’s beginning inventory was $600,000. During 2012,

the company purchased $2,600,000 of additional inventory, and on December 31, 2012

Creek’s ending inventory was $565,000.

Required:

What was Deputron’s inventory turnover for 2012?

9. Caraway Company’s net accounts receivable was $300,000 at December 31, 2012 and

$450,000 at December 31, 2013. Net cash sales for 2008 were $425,000. The accounts

receivable turnover for 2013 was 7.0, and this turnover figure was computed from net credit

sales for the year.

Required:

What were Caraway’s total net sales for 2013?

10. Foxmoor Company’s merchandise inventory and other related accounts for 2012 follow:

Sales

$3,100,000

Cost of Goods Sold

2,153,200

Merchandise Inventory

Beginning of Year

850,000

End of Year

995,000

5-27

Required:

Calculate Foxmoor’s inventory turnover during 2012 assuming that the merchandise inventory buildup

was relatively constant during the year.

11. Bragdon Company is consistently profitable. Its normal financial statement relationships are as

follows:

Current ratio

3.5:1

Inventory turnover

4.5 times

Liabilities to assets ratio

0.8: 1

Required: Determine whether each transaction or event that follows increased, decreased or had no

effect on each ratio.

1. Bragdon declared but did not pay a cash dividend.

2. Customers returned invoiced goods for which they had not paid.

3.Accounts payable were paid at year-end.

4. Bragdon recorded both a receivable from an insurance company and a loss on a building due to fire

damage.

5. Early in the year, Bragdon increased the selling price of one of its products because customer

demand far exceeded production capacity. The number of units sold this year was the same as last

year.

ANS: