Chapter 4—Completing the Accounting Cycle Key

1. Cross-referencing is useful in assuring that the debits and credits are in balance.

2. When accounts do not appear on the unadjusted trial balance but are needed to post adjustments, they are

simply added to the account title column.

3. Once the adjusted trial balance is in balance, the flow of accounts will now go into the financial statements.

4. There is really no benefit in preparing financial statements in any particular order.

5. Current assets are also called as plant assets.

6. On the income statement, miscellaneous expenses are usually presented as the last item without regard to the

dollar amount.

7. The usual presentation of the retained earnings statement is (1) beginning retained earnings, (2) net income

or loss, (3) dividends (4) ending retained earnings.

8. The difference between a classified balance sheet and one that is not classified is that the classified one has

subheadings.

9. Cash and other assets that may reasonably be expected to be realized in cash, sold, or consumed through the

normal operations of a business, usually longer than one year, are called current assets.

10. Prepaid Insurance is an example of a current asset.

11. Land is an example of a plant asset.

12. Liabilities that will be due within one year or less and that are to be paid out of current assets are called

current liabilities.

13. The amount of the net income for a period appears on both the income statement and the balance sheet for

that period.

14. Accrued taxes payable are generally reported on the balance sheet as a current liability.

15. At the end of the fiscal period, prepaid expenses are reported on the income statement as expenses.

16. Office Equipment is an example of a current asset account.

17. Capital Stock and Dividends are reported in the stockholders’ equity section of the balance sheet.

18. Deferred expenses that benefit a relatively short period of time are listed on the balance sheet as current

assets.

19. Unearned revenues that will be earned in a relatively short period of time are listed on the balance sheet as

current assets.

20. Accrued expenses are ordinarily listed on the balance sheet as current assets.

21. Accrued revenues are ordinarily listed on the balance sheet as current liabilities.

22. The income statement is prepared from the adjusted trial balance or the income statement columns on the

work sheet.

23. Examples of temporary accounts are supplies and prepaid expenses which are in the ledger for just a short

time before they expire.

24. Accumulated Depreciation is a permanent account.

25. The dividends account is a temporary account.

26. The balance sheet accounts are referred to as real or permanent accounts.

27. Journalizing and posting the adjustments and closing entries updates the ledger for the new accounting

period.

28. The income summary account is closed to the retained earnings account.

29. The accumulated depreciation account is closed to the income summary account.

30. The dividends account is closed to the income summary account.

31. The trial balance prepared after all the closing entries have been posted is called a pre-closing trial balance.

32. Entries required to close the balances of the temporary accounts at the end of the period are called final

entries.

33. Journalizing and posting closing entries must be completed before financial statements can be prepared.

34. During the closing process, some balance sheet accounts are closed and end the period with a zero balance.

35. Closing entries are entered directly on to the work sheet.

36. The post-closing trial balance will generally have fewer accounts than the trial balance.

37. A post-closing trial balance contains only asset and liability accounts.

38. A post-closing trial balance should be prepared before the financial statements are prepared.

39. Cash, Accounts Payable, and Capital Stock are real accounts and do not get closed at the end of the period.

40. The income summary account is also known as the clearing account.

41. All income statement accounts will be closed at the end of the period.

42. Balance Sheet accounts are not considered real accounts.

43. It is not necessary to post the closing entries to the general ledger.

44. Once an account has been closed for the period, inserting a line in the balance columns zeros out the

account, making it ready for the following period.

45. The closing process is sometimes referred to as closing the books.

46. Accounts reported on the balance sheet that are carried forward from year to year are known as permanent

accounts.

47. Real accounts are not permanent accounts.

48. After analyzing transactions, the next step would be to post the transactions in the ledger.

49. The most important output of the accounting cycle is the financial statements.

50. The last step of the accounting cycle is to prepare a post-closing trial balance.

51. The accounting cycle begins with preparing an unadjusted trial balance.

52. Financial statements should be prepared before the closing entries are journalized and posted.

53. The unadjusted, adjusted, and post-closing trial balances are the three types of trial balances prepared in an

accounting cycle.

54. Any twelve-month accounting period adopted by a company is known as its fiscal year.

55. A fiscal year that ends when business activities have reached their lowest point is called the natural business

year.

56. All companies must use a calendar year as their fiscal year.

57. The majority of businesses end their fiscal year on December 31.

58. The work sheet is not considered a part of the formal accounting records.

59. The balances of the equity accounts from the Adjusted Trial Balance columns of the work sheet are

extended to the Retained Earnings Statement columns.

60. The work sheet is a working paper that accountants can use to summarize adjusting entries and the account

balances for the financial statements.

61. In a computerized accounting system, a work sheet may not be necessary because the software program

automatically posts entries to the accounts and prepares financial statements.

62. The trial balance may be listed on the work sheet instead of being prepared separately.

63. The totals of the Adjusted Trial Balance columns on a work sheet will always be the sum of the Trial

Balance column totals and the Adjustments column totals.

64. A work sheet heading is dated for a period of time.

65. On the work sheet, the capital stock and dividends account balances are extended to the Balance Sheet

columns.

66. After the account balances have been extended from the Adjusted Trial Balance columns on the work sheet,

the difference between the initial totals of the Balance Sheet debit and credit columns is net income or net loss.

67. After net income or loss is entered on the work sheet, the debit column total must equal the credit column

total of the Balance Sheet columns.

68. A net loss is shown on the work sheet in the credit columns of both the Income Statement columns and the

Balance Sheet columns.

69. Net income is shown on the work sheet in the Income Statement Debit column and the Balance Sheet Credit

column.

70. If the totals of the Income Statement debit and credit columns of a work sheet are $27,000 and $29,000,

respectively, after all account balances have been extended, the amount of the net loss is $2,000.

71. The work sheet and the financial statements both require dollar signs.

72. The balance in the retained earnings account on the work sheet will equal the amount presented in the

balance sheet.

73. Since the adjustments are entered on the work sheet, it is not necessary to record them in the journal or post

them to the ledger.

74. The chart of accounts, the journal, and the ledger are essential parts of the accounting system.

75. What is the major difference between the unadjusted trial balance and the adjusted trial balance?

76. Once the adjusting entries are posted, the adjusted trial balance is prepared to

77. When preparing the retained earnings statement, the beginning retained earnings balance can always be

found

78. Accumulated depreciation appears on the

79. Notes receivable due in 350 days appear on the

80. Unearned Fees appear on the

81. Which one of the fixed asset accounts listed below will not have a related contra asset account?

82. Prepaid insurance is reported on the balance sheet as a

83. The income statement is prepared from:

84. Which of the following is not showed on the retained earnings statement of a company?

85. The retained earnings statement should be prepared

86. The income statement should be prepared

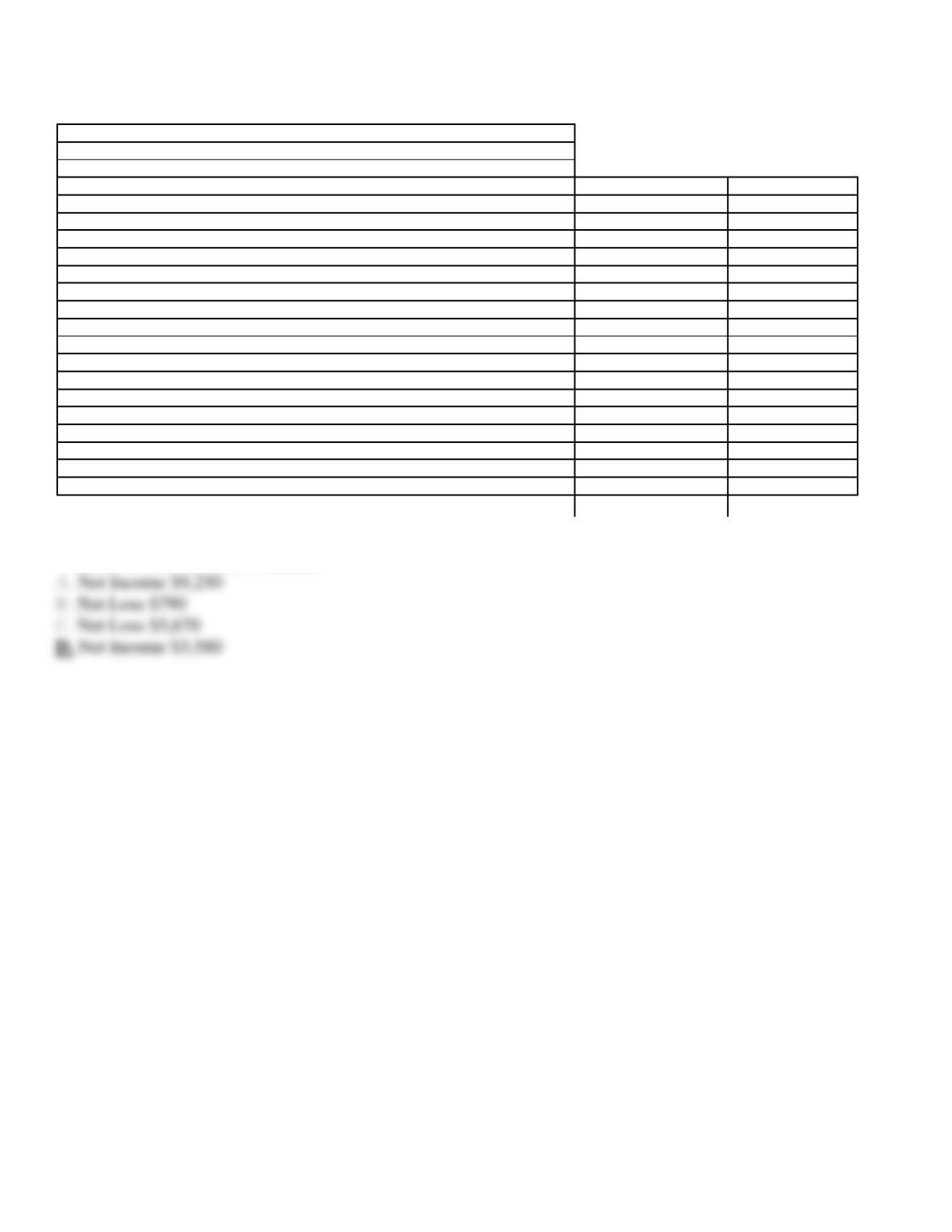

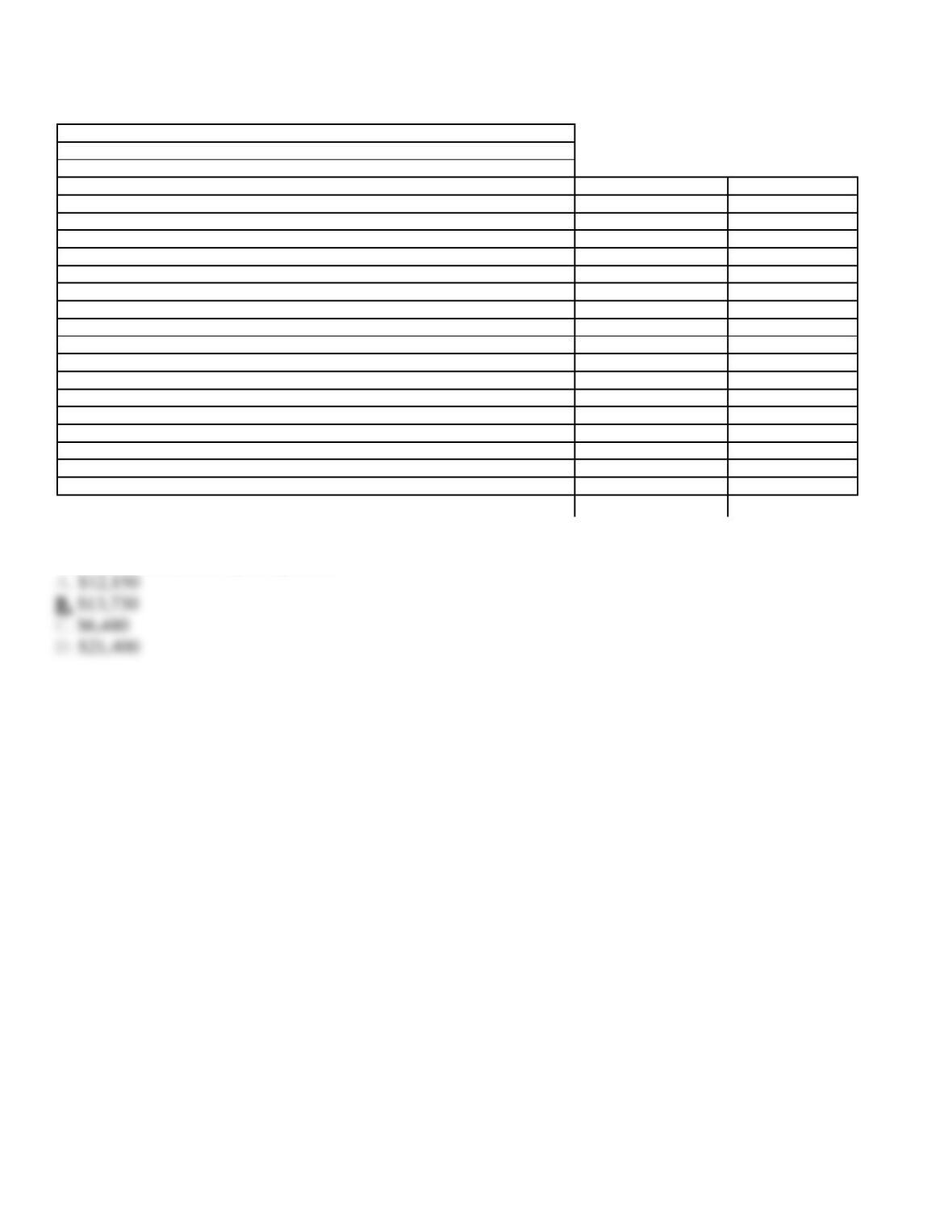

87. Use the information in the adjusted trial balance for Stockton Company to answer the questions that follow.

Stockton Company

Adjusted Trial Balance

For the Year Ended December 31, 20XX

Cash

$ 6,530

Accounts Receivable

2,100

Prepaid Expenses

700

Equipment

13,700

Accumulated Depreciation

$ 1,100

Accounts Payable

1,900

Notes Payable

4,300

Capital Stock

2,000

Retained Earnings

10,940

Dividends

790

Fees Earned

9,250

Wages Expense

2,500

Rent Expense

1,960

Utilities Expense

775

Depreciation Expense

250

Miscellaneous Expense

185

Totals

$29,490

$29,490

Determine the net income (loss) for the period.

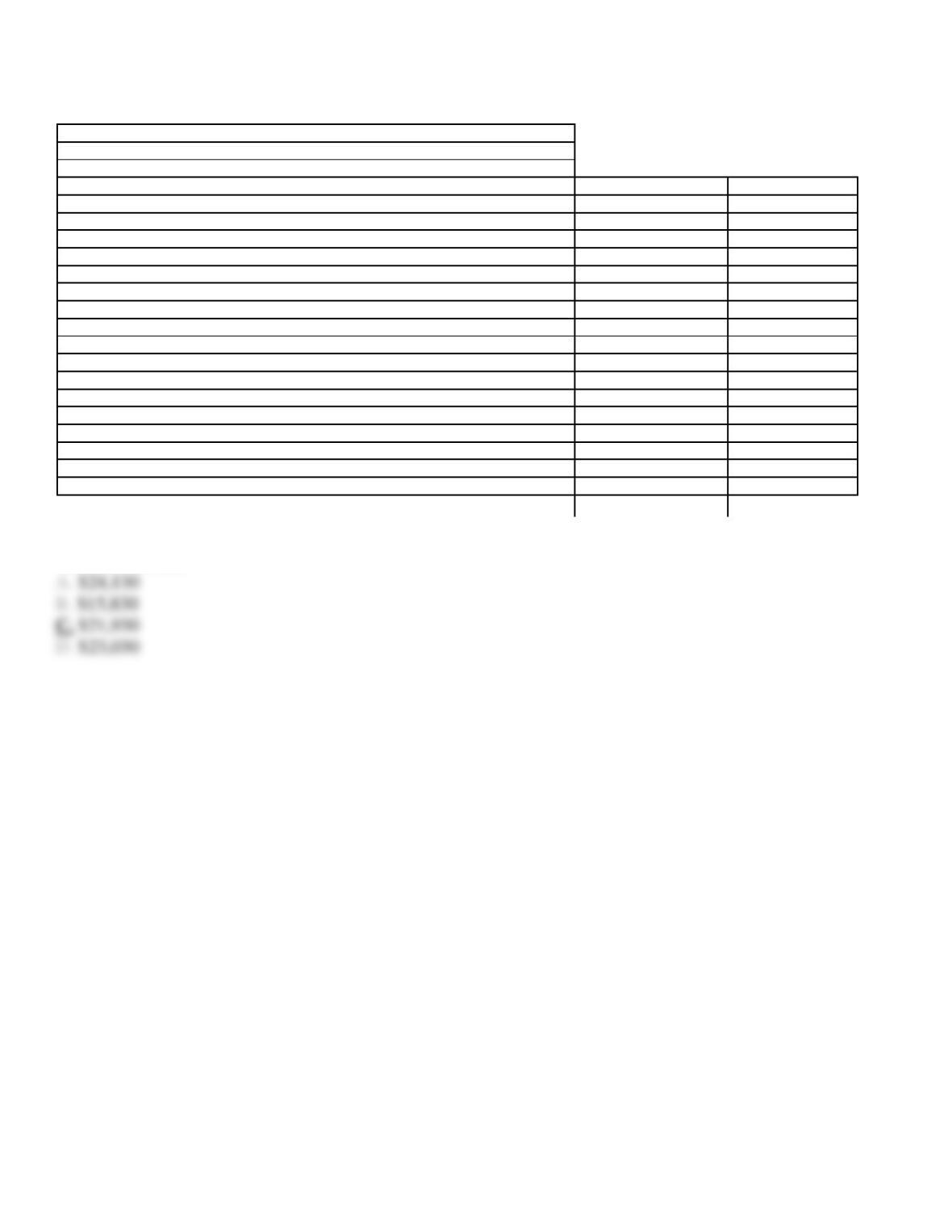

88. Use the information in the adjusted trial balance for Stockton Company to answer the questions that follow.

Stockton Company

Adjusted Trial Balance

For the Year Ended December 31, 20XX

Cash

$ 6,530

Accounts Receivable

2,100

Prepaid Expenses

700

Equipment

13,700

Accumulated Depreciation

$ 1,100

Accounts Payable

1,900

Notes Payable

4,300

Capital Stock

2,000

Retained Earnings

10,940

Dividends

790

Fees Earned

9,250

Wages Expense

2,500

Rent Expense

1,960

Utilities Expense

775

Depreciation Expense

250

Miscellaneous Expense

185

Totals

$29,490

$29,490

Determine the Retained Earnings ending balance.

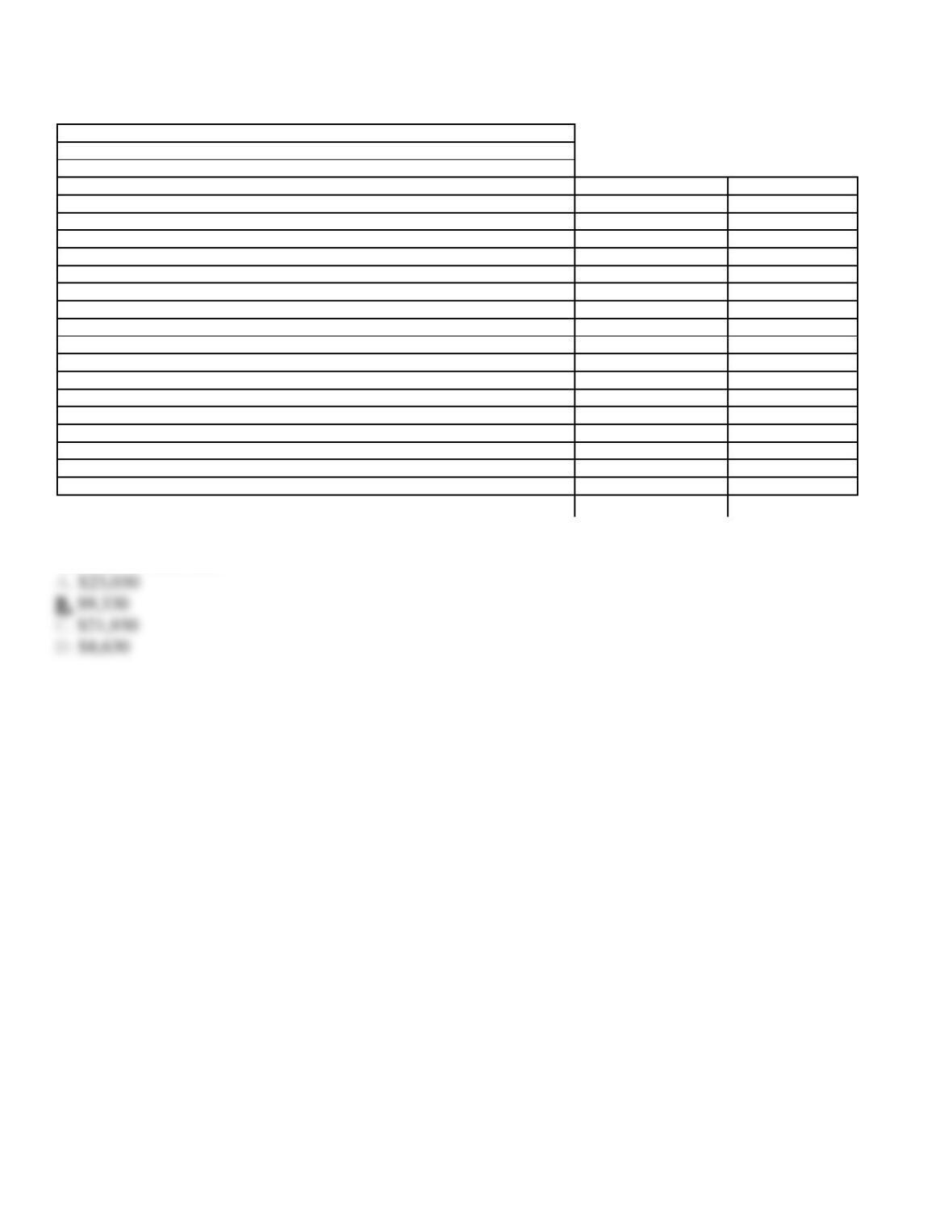

89. Use the information in the adjusted trial balance for Stockton Company to answer the questions that follow.

Stockton Company

Adjusted Trial Balance

For the Year Ended December 31, 20XX

Cash

$ 6,530

Accounts Receivable

2,100

Prepaid Expenses

700

Equipment

13,700

Accumulated Depreciation

$ 1,100

Accounts Payable

1,900

Notes Payable

4,300

Capital Stock

2,000

Retained Earnings

10,940

Dividends

790

Fees Earned

9,250

Wages Expense

2,500

Rent Expense

1,960

Utilities Expense

775

Depreciation Expense

250

Miscellaneous Expense

185

Totals

$29,490

$29,490

Determine total assets.

90. Use the information in the adjusted trial balance for Stockton Company to answer the questions that follow.

Stockton Company

Adjusted Trial Balance

For the Year Ended December 31, 20XX

Cash

$ 6,530

Accounts Receivable

2,100

Prepaid Expenses

700

Equipment

13,700

Accumulated Depreciation

$ 1,100

Accounts Payable

1,900

Notes Payable

4,300

Capital Stock

2,000

Retained Earnings

10,940

Dividends

790

Fees Earned

9,250

Wages Expense

2,500

Rent Expense

1,960

Utilities Expense

775

Depreciation Expense

250

Miscellaneous Expense

185

Totals

$29,490

$29,490

Determine the current assets.

91. Use the information in the adjusted trial balance for Stockton Company to answer the questions that follow.

Stockton Company

Adjusted Trial Balance

For the Year Ended December 31, 20XX

Cash

$ 6,530

Accounts Receivable

2,100

Prepaid Expenses

700

Equipment

13,700

Accumulated Depreciation

$ 1,100

Accounts Payable

1,900

Notes Payable

4,300

Capital Stock

2,000

Retained Earnings

10,940

Dividends

790

Fees Earned

9,250

Wages Expense

2,500

Rent Expense

1,960

Utilities Expense

775

Depreciation Expense

250

Miscellaneous Expense

185

Totals

$29,490

$29,490

Determine the total liabilities for the period.

92. The balance sheet should be prepared

93. The retained earnings statement begins with the beginning balance followed by

94. The income statement will include

95. The classified balance sheet will subsection the assets as follows

96. The classified balance sheet will have liabilities divided into the following subsections

97. Current liabilities are those liabilities that

98. On the balance sheet, stockholders’ equity is

99. Balance sheet accounts

100. On which financial statement will Income Summary be shown?

101. Which of the following is not true about closing entries?

102. The income summary account is also called

103. After posting the second closing entry to the income summary account, the balance will be equal to

104. What is the last account that should be listed in the post-closing trial balance?

105. Which of the following account groups are all considered nominal accounts?

106. There are four closing entries. The first one is to close ____, the second one is to close ____, the third one

is to close ____, and the last one is to close ____.

107. Closing entries

108. Closing entries are dated in the journal as of

109. Which of the accounts below would be closed by posting a debit to the account?

110. Which of the following accounts should be closed to Income Summary at the end of the fiscal year?

111. Which of the following accounts will not be closed to Income Summary at the end of the fiscal year?

112. Which of the following accounts will be closed to the retained earnings account at the end of the fiscal

year?

113. The entry to close the appropriate insurance account at the end of the accounting period is

114. Which of the following accounts ordinarily appears in the post-closing trial balance?

115. The post-closing trial balance differs from the adjusted trial balance in that it

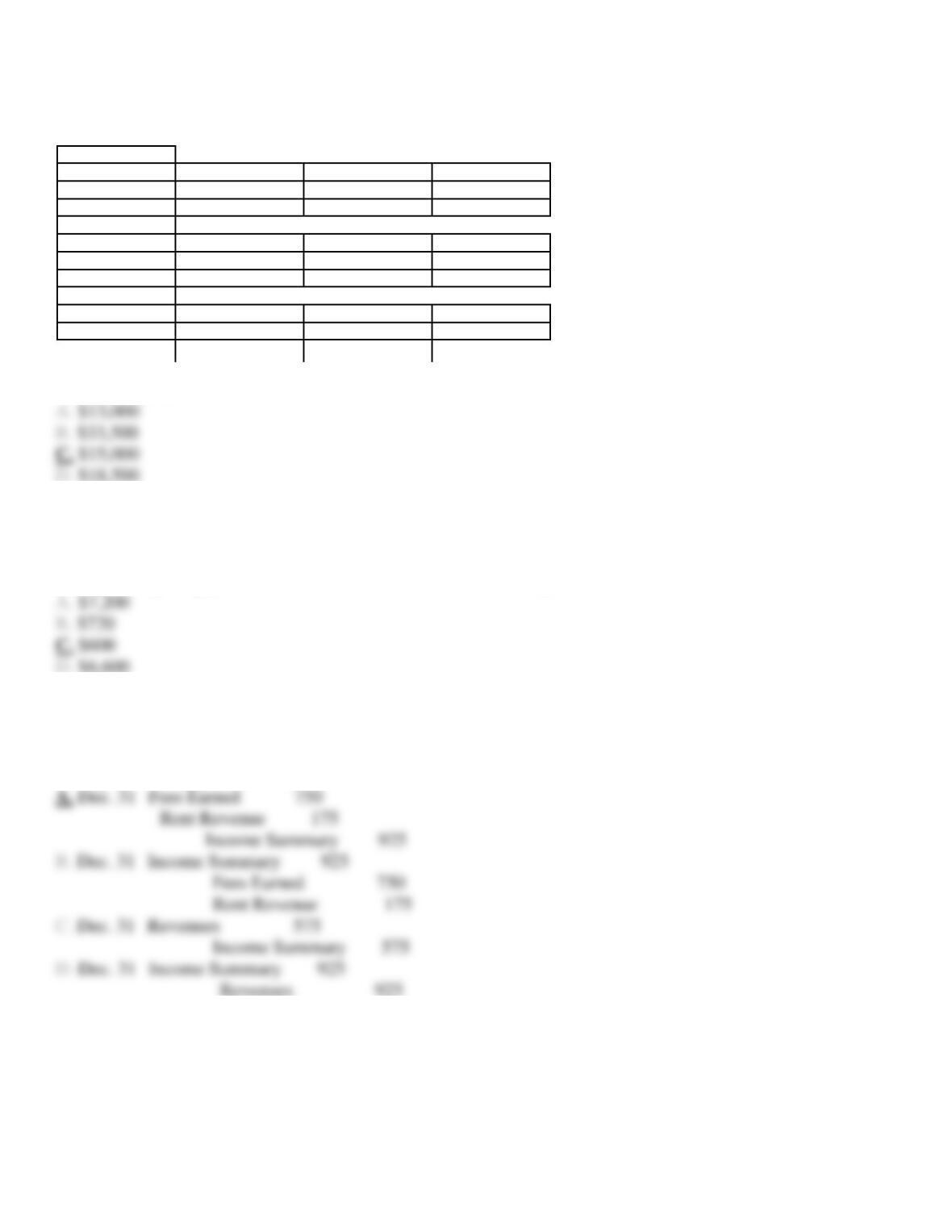

116. The following accounts were taken from the Adjusted Trial Balance columns of the work sheet:

Accumulated Depreciation

$ 3,200

Fees Earned

17,400

Depreciation Expense

1,300

Insurance Expense

200

Prepaid Insurance

4,800

Supplies

900

Supplies Expense

3,800

Net income for the period is

117. A summary of selected ledger accounts appear below for Alberto’s Plumbing Services for the current

calendar year-end.

Retained Earnings

12/31

8,500

1/1

6,500

12/31

15,000

Dividends

6/30

3,500

12/31

8,500

11/30

5,000

Income Summary

12/31

18,500

12/31

33,500

12/31

15,000

Net income for the period is

118. Amir Designs purchased a one-year liability insurance policy on March 1st of this year for $7,200 and

recorded it as a prepaid expense. Which of the following amounts would be recorded for insurance expense

during the adjusting process at the end of Amir’s first month of operations on March 31st?

119. The journal entry to close the Fees Earned, $750, and Rent Revenue, $175, accounts on December 31st

during the closing process would be: