The Market Forces of Supply and Demand 1087

24.

Refer to Table 4-15. Assuming these are the only four suppliers in this market and the function

for market demand

is QD=1000-100P, where QD is the quantity demanded and P is the price,

what is the equilibrium quantity?

25.

Refer to Table 4-15. Assume these are the only four suppliers in this market and the function

for market demand is

QD=1000-100P, where QD is the quantity demanded and P is the price. If

the price is $6 per case, is there a

shortage or surplus, and how large is the shortage or surplus?

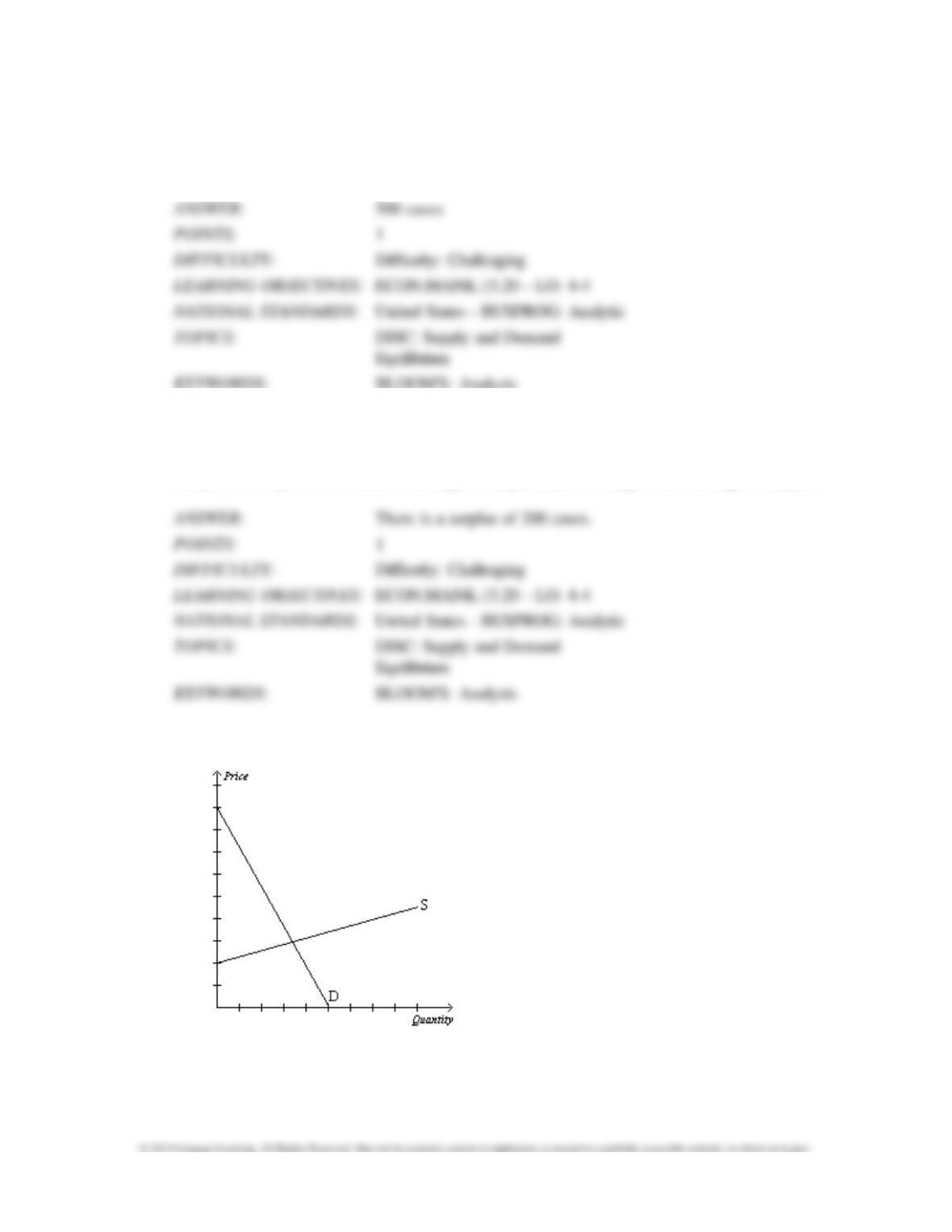

Figure 4-30

26.

Refer to Figure 4-30. In this market for iPhones, the technology improves while all other

factors remain constant. Which curve(s) shift(s) and in which direction?

27.

Refer to Figure 4-30. In this market for iPhones, the technology improves while all other

factors remain constant. Explain the change(s) in the equilibrium price and quantity.

28.

Refer to Figure 4-30. In this market for tablet computers, more suppliers enter the market and

the price of laptops,

a substitute good, increases, while all other factors remain constant. Which

curve(s) shift(s) and in which direction?

29.

Refer to Figure 4-30. In this market for tablet computers, more suppliers enter the market and

the price of laptops,

a substitute good, increases, while all other factors remain constant. Explain

the change(s) in the equilibrium price

and quantity.

30.

If corn is an input into the production of ethanol, will a decrease in the price of corn increase the

supply of ethanol or

decrease the supply of ethanol?

31.

Suppose researchers discover a new, lower cost method of producing calculators. As a result, will

the supply of

calculators increase or decrease?

1090 The Market Forces of Supply and Demand

Figure 4-31

Consider the market for 2-packs of light bulbs below.

32.

Refer to Figure 4–31. What are the values of the equilibrium price and quantity?

33.

Refer to Figure 4-31. At a price of $3, is there a shortage or surplus, and how large is the

shortage/surplus?

34.

Refer to Figure 4-31. At a price of $6, is there a shortage or surplus, and how large is the

shortage/surplus?

35.

Refer to Figure 4-31. Suppose there is an improvement in technology in this market and the

price of lamps, a

complementary good, increases. What changes do you predict in the equilibrium

price and quantity?

Table 4–16

The following table shows the supply and demand schedules in a market.

Price ($)

Quantity

Demanded

(units)

Quantity

Supplied

(units)

0

50

0

2

40

15

4

30

30

6

20

45

8

10

60

10

0

75

36.

Refer to Table 4-16. What is the equilibrium price in this market?

37.

Refer to Table 4-16. What is the equilibrium quantity in this market?

38.

Refer to Table 4–16. At a price of $2, will there be a surplus or shortage of units in this market?

39.

Refer to Table 4-16. At a price of $8, how large of a surplus will there be in this market?

40.

Refer to Table 4–16. If the supply curve shifts to the right, will the price in this market rise or

fall?

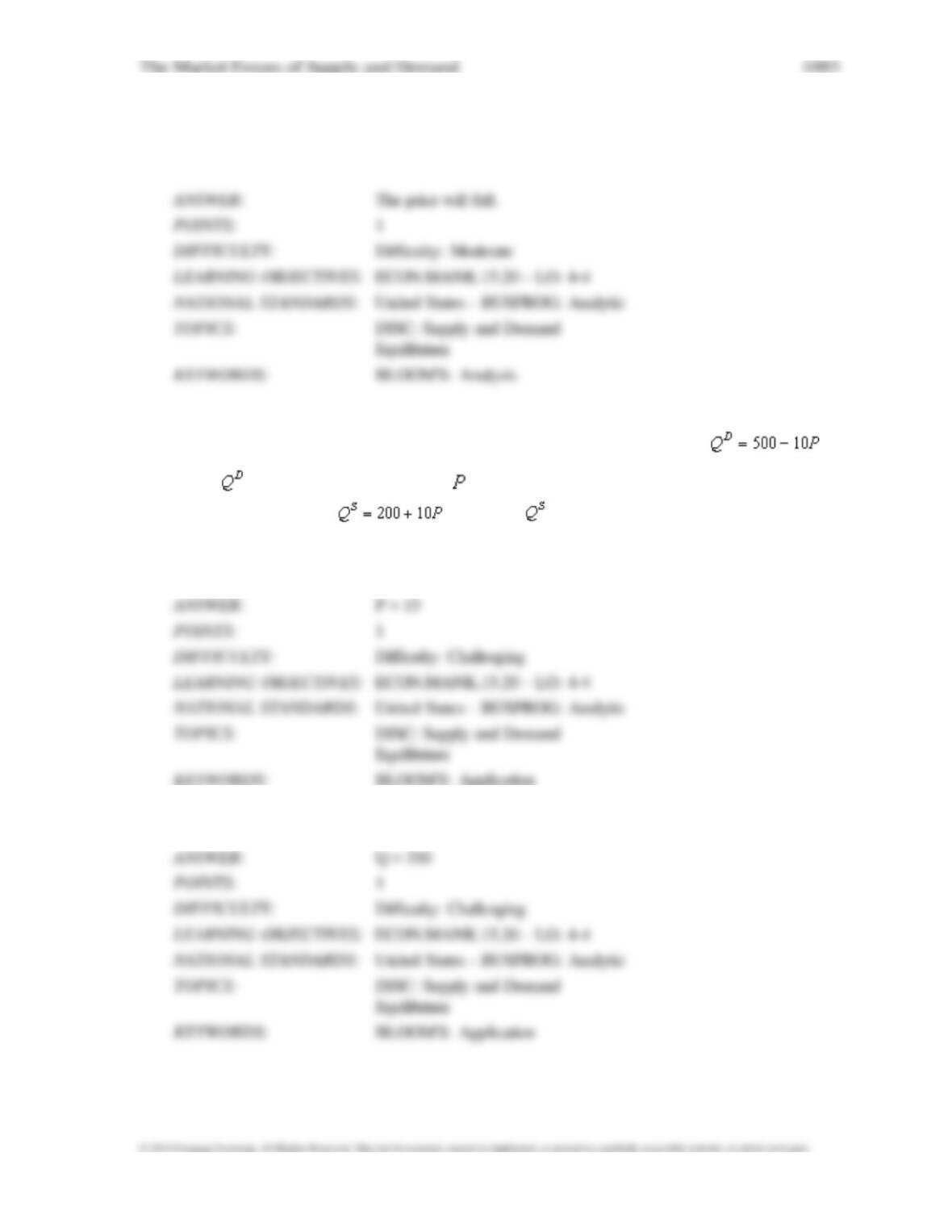

Scenario 4-1

Suppose the demand schedule in a market can be represented by the equation ,

where is the

quantity demanded and is the price. Also, suppose the supply schedule can be

represented by the equation , where is the quantity supplied.

41.

Refer to Scenario 4-1. What is the equilibrium price in this market?

42.

Refer to Scenario 4-1. What is the equilibrium quantity in this market?

43.

Refer to Scenario 4-1. Suppose the price is currently equal to 10 in this market. Is there a

shortage or surplus in

this market, and how large is the shortage/surplus?

44.

Refer to Scenario 4-1. Suppose the price is currently equal to 18 in this market. Is there a

shortage or surplus in

this market, and how large is the shortage/surplus?

45.

Refer to Scenario 4-1. Suppose the supply curve shifts to . What is the new

equilibrium price and

quantity in this market?

46.

Suppose the supply and demand of corn both increase. As a result, what will happen to the

equilibrium price and

equilibrium quantity in the market?

47.

If the supply of tennis balls, a complement to tennis racquets, decreases, what will happen to the

equilibrium price of

tennis balls and to the equilibrium price of tennis racquets?

48.

If the supply of pencils, a substitute for pens, increases, what will happen to the equilibrium price

of pencils and to

the equilibrium price of pens?

49.

If the price of steel, an input into the production of automobiles, rises, and at the same time the

price of gasoline

rises, what will happen to the equilibrium price and quantity of automobiles?

50.

If the demand for a good increases at the same time as the supply of the same good decreases,

what will happen to

the equilibrium price and quantity of the good?