Chapter 4 – Completing the Accounting Cycle

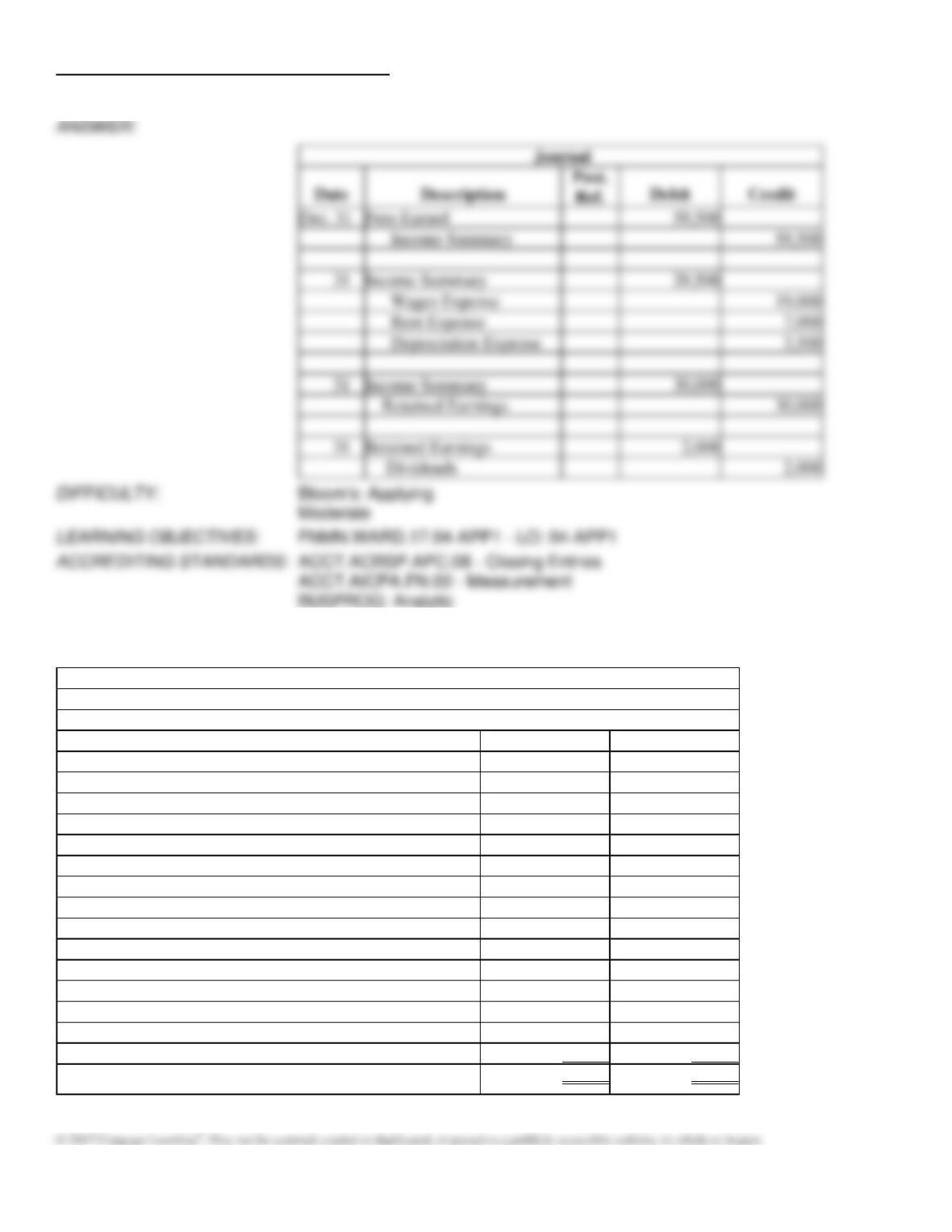

Fees Earned

31

Income Summary

31

Income Summary

31

Retained Earnings

LEARNING OBJECTIVES:

186. The following is the adjusted trial balance for Miller Company.

Miller Company

Adjusted Trial Balance

December 31

Cash

8,130

Accounts Receivable

3,300

Prepaid Expenses

2,750

Equipment

10,400

Accumulated Depreciation

2,200

Accounts Payable

2,700

Notes Payable

1,000

Common Stock

9,200

Retained Earnings

2,000

Dividends

4,870

Fees Earned

36,600

Wages Expense

12,450

Rent Expense

4,900

Utilities Expense

3,475

Depreciation Expense

2,150

Miscellaneous Expense

1,275

Totals

53,700

53,700

Prepare closing entries and the post-closing trial balance.

Chapter 4 – Completing the Accounting Cycle

Fees Earned

Income Summary

Income Summary

Retained Earnings

Accounts Receivable

Prepaid Expenses

Accumulated Depreciation

Accounts Payable

Common Stock

Retained Earnings

LEARNING OBJECTIVES:

187. The following are all the steps in the accounting cycle. List them in the order in which they should be done.

– Closing entries are journalized and posted to the ledger.

– An unadjusted trial balance is prepared.

– An optional end-of-period spreadsheet is prepared.

– A post-closing trial balance is prepared.

– Adjusting entries are journalized and posted to the ledger.

– Transactions are analyzed and recorded in the journal.

– Adjustment data are assembled and analyzed.

– Financial statements are prepared.

– An adjusted trial balance is prepared.

– Transactions are posted to the ledger.

Chapter 4 – Completing the Accounting Cycle

Transactions are analyzed and recorded in the journal.

Transactions are posted to the ledger.

Adjusting entries are journalized and posted to the ledger.

Financial statements are prepared.

Closing entries are journalized and posted to the ledger.

A post-closing trial balance is prepared.

LEARNING OBJECTIVES:

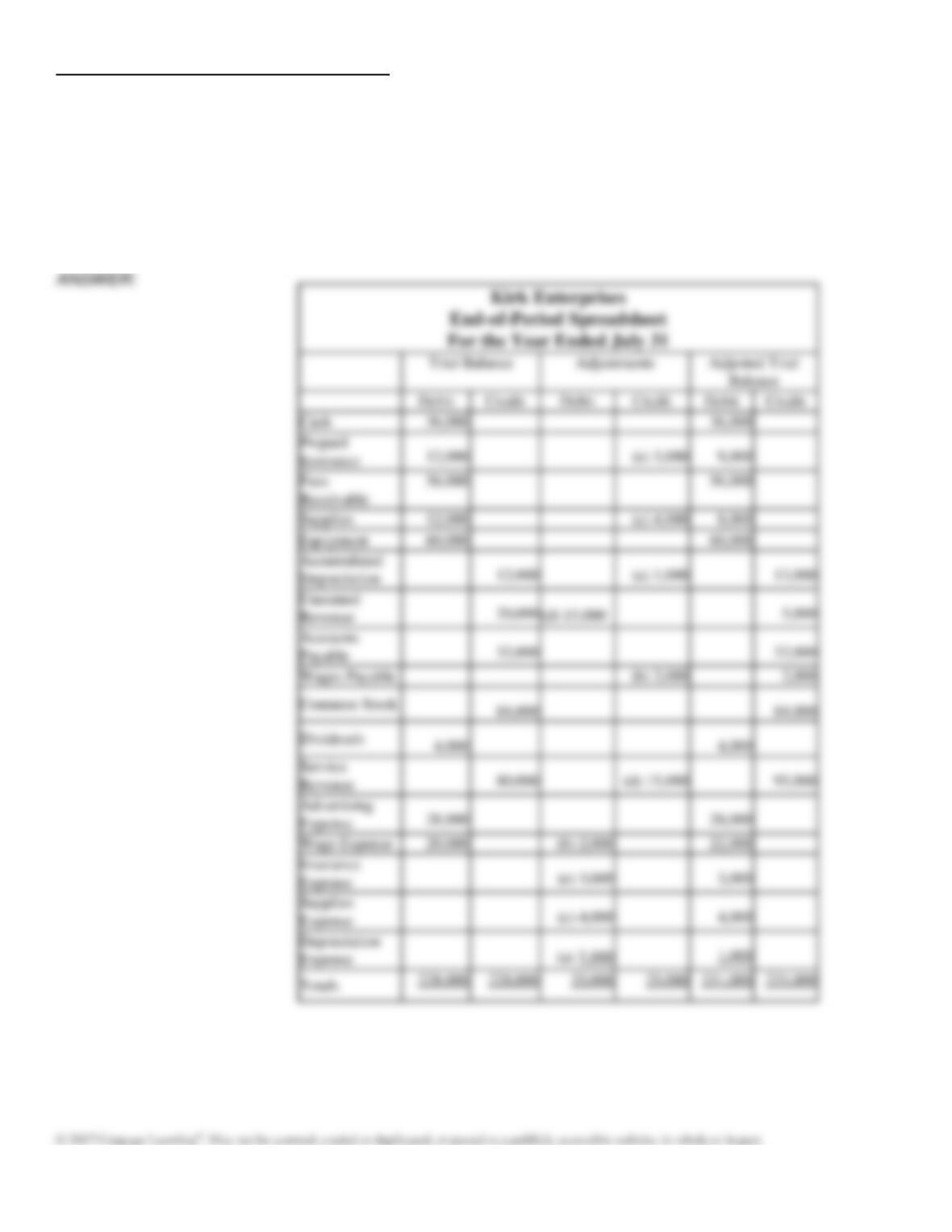

188. Kirk Enterprises offers rug cleaning services to business clients. Below is the trial balance for Kirk Enterprises,

which was prepared on the end-of-period spreadsheet for the year ended July 31.

Kirk Enterprises

End-of-Period Spreadsheet

For the Year Ended July 31

Trial Balance

Adjustments

Adjusted Trial

Balance

Debit

Credit

Debit

Credit

Debit

Credit

Cash

36,000

Prepaid Insurance

12,000

Fees Receivable

56,000

Supplies

12,000

Equipment

60,000

Accum. Depreciation

12,000

Unearned Revenue

20,000

Accounts Payable

32,000

Wages Payable

Common Stock

84,000

Dividends

4,000

Service Revenue

80,000

Advertising Expense

28,000

Wage Expense

20,000

Insurance Expense

Supplies Expense

Depreciation Expense

Totals

228,000

228,000

Chapter 4 – Completing the Accounting Cycle

REQUIRED: Enter the adjustment data in the work sheet for the transactions shown below and place the balances in the

Adjusted Trial Balance columns.

a) The equipment is estimated to last for 5 years with no salvage value. The asset will be depreciated evenly over its

useful life. Record one month’s depreciation.

b) Accrued wages, $2,000.

c) Unused supplies on hand, $8,000.

d) Of the unearned revenue, 75% has been earned.

e) Unexpired insurance remaining at the end of the month, $9,000.

Chapter 4 – Completing the Accounting Cycle

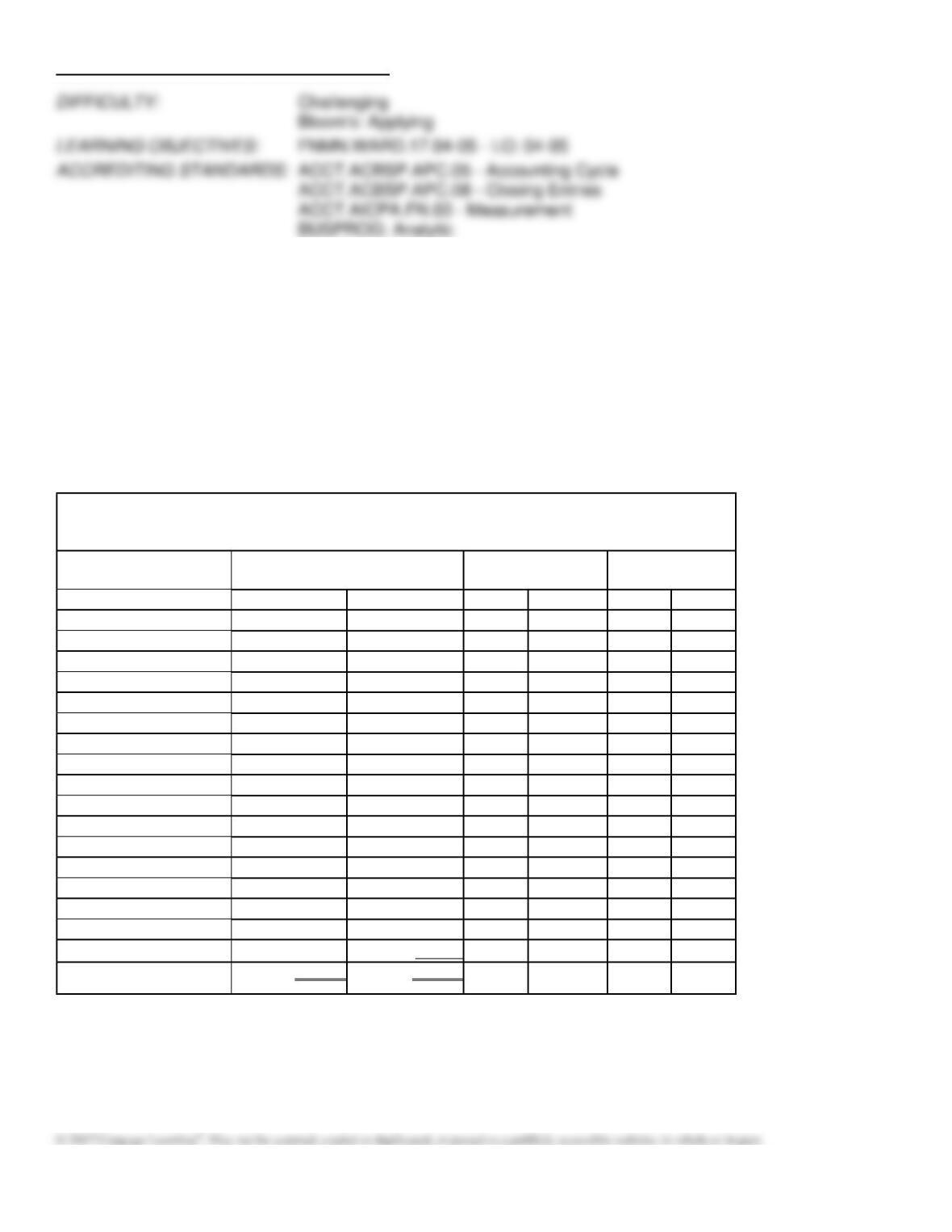

189. Kirk Enterprises offers rug cleaning services to business clients. Below is the adjustments data for the year ended

July 31. Using this information along with the spreadsheet below, record the adjusting entries in proper general journal

form.

Adjustments:

(a) The equipment is estimated to last for 5 years with no salvage value. The asset will be depreciated evenly over its

useful life. Record one month’s depreciation.

(b) Accrued wages, $2,000.

(c) Unused supplies on hand, $8,000.

(d) Of the unearned revenue, 75% has been earned.

(e) Unexpired insurance remaining at the end of the month, $9,000.

Kirk Enterprises

End-of-Period Spreadsheet

For the Year Ended July 31

Trial Balance

Adjustments

Adjusted Trial

Balance

Debit

Credit

Debit

Credit

Debit

Credit

Cash

36,000

Prepaid Insurance

12,000

Fees Receivable

56,000

Supplies

12,000

Equipment

60,000

Accumulated Depreciation

12,000

Unearned Revenue

20,000

Accounts Payable

32,000

Wages Payable

Common Stock

84,000

Dividends

4,000

Service Revenue

80,000

Advertising Expense

28,000

Wage Expense

20,000

Insurance Expense

Supplies Expense

Depreciation Expense

______

___

Totals

228,000

228,000

LEARNING OBJECTIVES:

Chapter 4 – Completing the Accounting Cycle

190. Alpha Company has current assets of $74,524, total assets of $203,310, total net income of $67,913, current

liabilities of $60,100, and total liabilities of $150,600.

What is Alpha Company’s working capital?

191. Alpha Company has current assets of $74,524, total assets of $203,310, total net income of $67,913, current

liabilities of $60,100, and total liabilities of $150,600.

What is Alpha Company’s current ratio?

Chapter 4 – Completing the Accounting Cycle

192. Calculate the current ratio for each business below. Which business has the best short-term solvency position given

your calculations?

Company

Current

Assets

Total

Assets

Current

Liabilities

Total

Liabilities

Net

Income

Current

Ratio

Alpha

Company

$74,524

$168,672

$60,100

$150,600

$94,958

Beta

Company

$207,536

$290,290

$152,600

$203,000

$207,536

Gamma

Company

$60,125

$66,929

$32,500

$52,700

$36,725

Delta

Company

$95,335

$182,520

$82,900

$135,200

$105,283

Assets

$60,100

1.24

Beta

Company

1.36

Gamma

Company

$32,500

1.85

Delta

Company

$82,900

1.15

Chapter 4 – Completing the Accounting Cycle

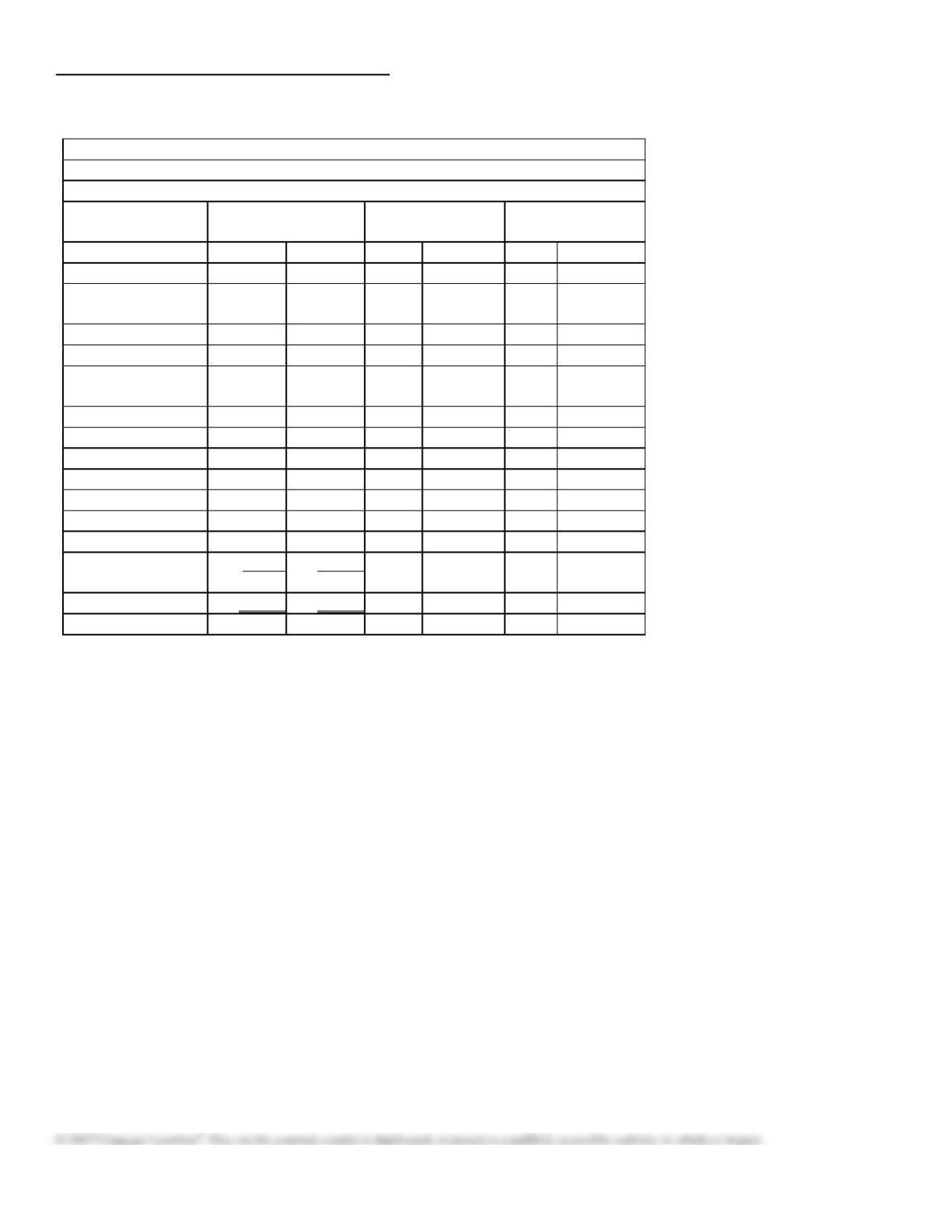

193. Complete the following end-of-period spreadsheet for Danilo Enterprises.

Danilo Enterprises

End-of-Period Spreadsheet

For the Year Ended December 31

Adjusted Trial

Balance

Income Statement

Balance Sheet

Account Title

Debit

Credit

Debit

Credit

Debit

Credit

Cash

14,500

Accounts

Receivable

7,500

Supplies

500

Equipment

20,500

Accumulated

Depr.—Equip.

15,000

Accounts Payable

9,500

Wages Payable

3,060

Common Stock

18,240

Dividends

1,000

Fees Earned

34,000

Wages Expense

18,000

Rent Expense

9,300

Depreciation

Expense

8,500

Totals

79,800

79,800

Net Income (Loss)

Chapter 4 – Completing the Accounting Cycle

Chapter 4 – Completing the Accounting Cycle

194. Explain how net income or loss is determined by using the end-of-period spreadsheets.

DIFFICULTY:

Bloom’s: Understanding

LEARNING OBJECTIVES:

195. If end-of-period spreadsheets are not considered part of the formal accounting records, then why are they used?

ANSWER:

DIFFICULTY:

Bloom’s: Remembering

LEARNING OBJECTIVES:

Match each journal entry that follows as one of the types of journal entries (a–c) below.

a.

Journal entries

b.

Adjusting journal entries

c.

Closing journal entries

DIFFICULTY:

Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.04-05 – LO: 04–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.06 – Recording Transactions

ACCT.ACBSP.APC.07 – Adjusting Entries

ACCT.ACBSP.APC.08 – Closing Entries

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

196. Cash 450

Fees Earned 450

197. Income Summary 650

Retained Earnings 650

Chapter 4 – Completing the Accounting Cycle

198. Utilities Expense 430

Cash 430

199. Wages Expense 870

Wages Payable 870

200. Unearned Revenue 985

Fees Earned 985

201. Income Summary 597

Rent Expense 200

Supplies Expense 180

Utilities Expense 110

Miscellaneous Exp. 107

202. Dividends 215

Cash 215

203. Accounts Receivable 325

Fees Earned 325

(Customer billed for services performed.)

204. Journalize the reversing entry on January 1 of the current year for the following adjusting journal entry from the prior

year:

Journal

Date

Description

Post Ref.

Debit

Credit

Dec. 31

Insurance Expense

2,500

Insurance Payable

2,500

Date

Jan. 1

Insurance Payable

Insurance Expense

Chapter 4 – Completing the Accounting Cycle

205. Zeta Company has 12 workers who each earn $15 per hour and generally work a 40–hour workweek, although at

times overtime work is required, for which workers are paid 1.5 times their regular hourly wage. Zeta pays wages in cash

on Friday of each week for work performed that week. Zeta’s Wages Expense ledger account for May is shown below.

Account: Wages Expense

Account Number 65

Balance

Date

Item

Post Ref.

Dr.

Cr.

Dr.

Cr.

May 5

32

7,200

7,200

May 12

33

9,360

16,560

May 19

35

7,200

23,760

May 26

37

8,010

31,770

May 31

Adjusting

38

4,320

36,090

May 31

Closing

38

36,090

–

–

During the period May 27 through June 2, Zeta’s workers worked a regular 40–hour week.

1. If Zeta Company uses reversing entries, journalize the entry made when payroll is paid in cash on June 2,

assuming that appropriate reversing entry(ies) have been made at the beginning of June. You may omit posting

references.

2. If Zeta Company does not use reversing entries, journalize the entry made when payroll is paid in cash on June 2.

You may omit posting references.

Jun. 1

Wages Payable

Post Ref.

Jun. 2

Wages Expense

Post Ref.

Jun. 2

Wages Payable

Wages Expense

Chapter 4 – Completing the Accounting Cycle