175. Figure 4-21

Appleby Manufacturing uses an activity-based costing system. The company produces Model F and Model G.

Information relating to the two products is as follows:

Model F

Model G

Units produced

24,000

30,000

Machine hours

7,500

8,500

Direct labor hours

8,000

12,000

Material handling (number of moves)

4,000

6,000

Setups

5,000

7,000

Purchase orders

30

40

Inspections

10,000

14,000

Product line variations

8

12

The following overhead costs are reported for the following activities of the production process:

Material handling

$ 40,000

Labor-related overhead

120,000

Setups

60,000

Product design

100,000

Batch inspections

120,000

Central purchasing

70,000

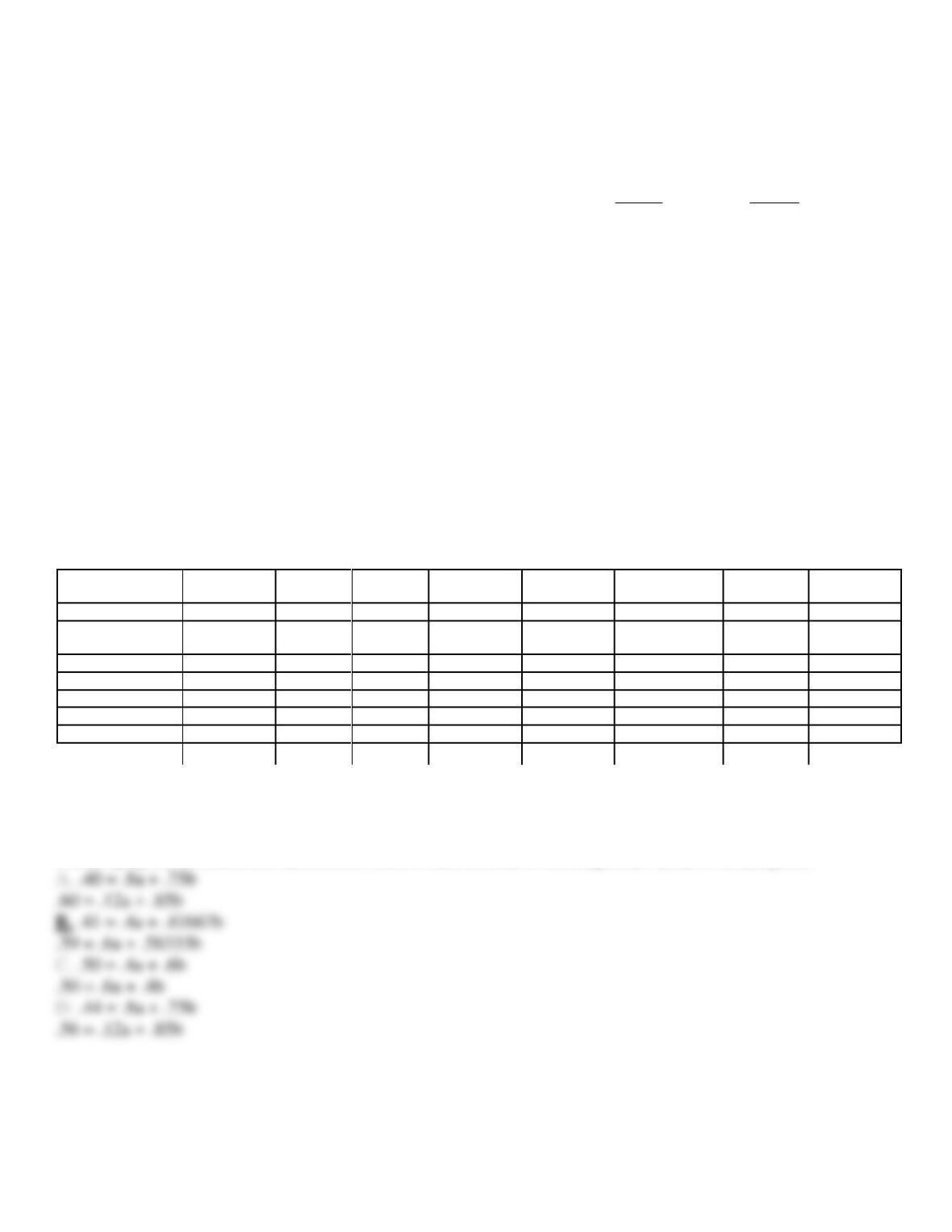

Jones manufacturing has used activity based costing to assign costs to Models F and G as given in the table below:

Activity

Cost Pool

Driver

Pool

Rate

Model F

Activity

Model F Cost

Model G Activity

Model G Cost

Total

Material handling

$40,000

10,000

$4

4,000

$16,000

6,000

$24,000

$40,000

Labor related

overhead

$120,000

20,000

$6

8,000

$48,000

12,000

$72,000

$120,000

Setups

$60,000

12,000

$5

5,000

$25,000

7,000

$35,000

$60,000

Product design

$100,000

20

$5,000

8

$40,000

12

$60,000

$100,000

Batch inspections

$120,000

24,000

$5

10,000

$50,000

14,000

$70,000

$120,000

Central purchasing

$70,000

70

$1,000

30

$30,000

40

$40,000

$70,000

total

$209,000

$301,000

$510,000

Appleby Manufacturing wants to implement an approximately relevant ABC system by using the two most expensive activities for cost assignment.

Refer to Figure 4-21. Under this new approach using consumption ratios for labor related and batch inspections, what set of equations would be used

to create equally accurate reduced ABC allocation rates (where a = labor hours and b = batch inspections)? (round to 5 decimal places)

176. Figure 4-21

Appleby Manufacturing uses an activity-based costing system. The company produces Model F and Model G.

Information relating to the two products is as follows:

Model F

Model G

Units produced

24,000

30,000

Machine hours

7,500

8,500

Direct labor hours

8,000

12,000

Material handling (number of moves)

4,000

6,000

Setups

5,000

7,000

Purchase orders

30

40

Inspections

10,000

14,000

Product line variations

8

12

The following overhead costs are reported for the following activities of the production process:

Material handling

$ 40,000

Labor-related overhead

120,000

Setups

60,000

Product design

100,000

Batch inspections

120,000

Central purchasing

70,000

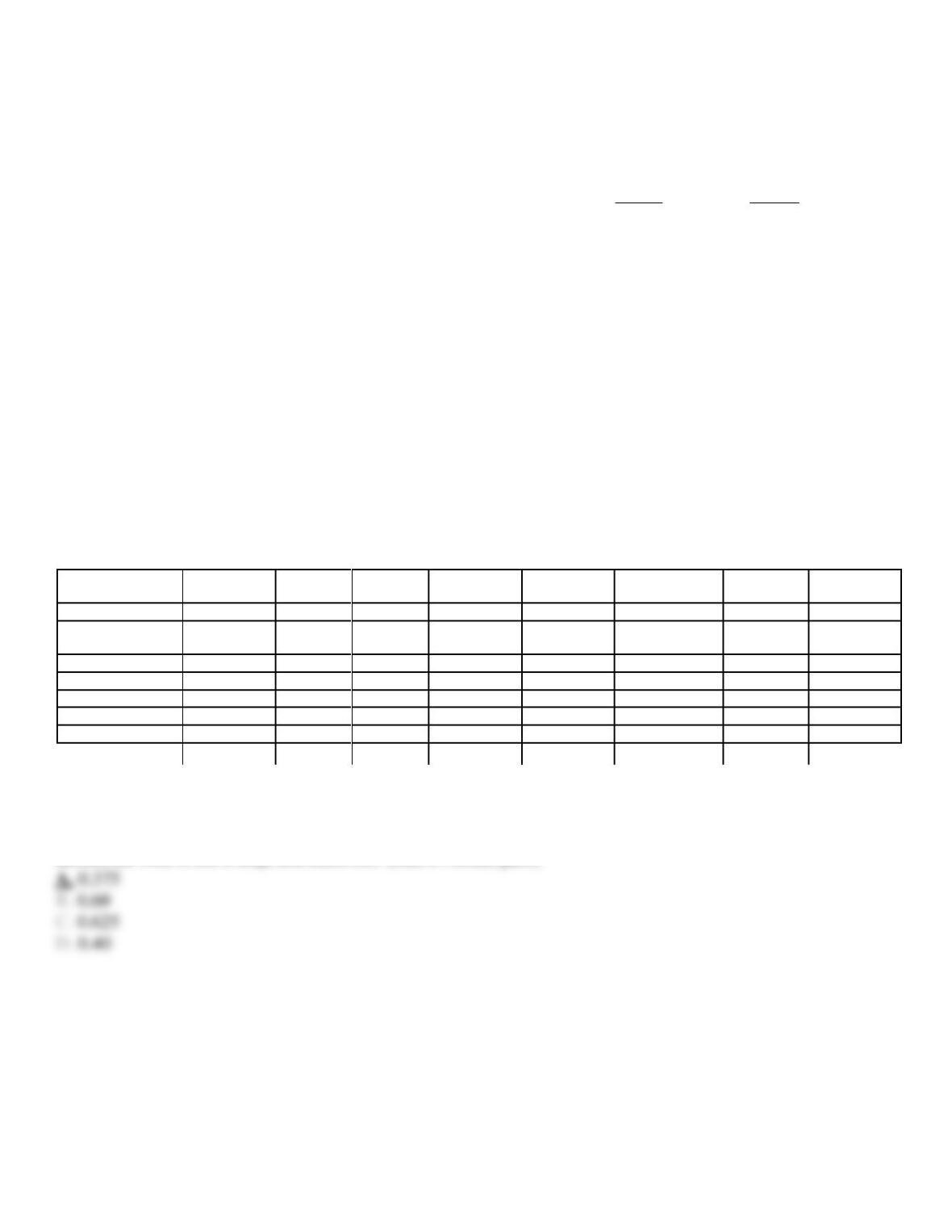

Jones manufacturing has used activity based costing to assign costs to Models F and G as given in the table below:

Activity

Cost Pool

Driver

Pool

Rate

Model F

Activity

Model F Cost

Model G Activity

Model G Cost

Total

Material handling

$40,000

10,000

$4

4,000

$16,000

6,000

$24,000

$40,000

Labor related

overhead

$120,000

20,000

$6

8,000

$48,000

12,000

$72,000

$120,000

Setups

$60,000

12,000

$5

5,000

$25,000

7,000

$35,000

$60,000

Product design

$100,000

20

$5,000

8

$40,000

12

$60,000

$100,000

Batch inspections

$120,000

24,000

$5

10,000

$50,000

14,000

$70,000

$120,000

Central purchasing

$70,000

70

$1,000

30

$30,000

40

$40,000

$70,000

total

$209,000

$301,000

$510,000

Appleby Manufacturing wants to implement an approximately relevant ABC system by using the two most expensive activities for cost assignment.

Refer to Figure 4-21. Under the equally accurate reduced ABC system, using consumption ratios for labor related and batch inspections, what

allocation rate would be used to assign labor related costs? (round to 5 decimal places)

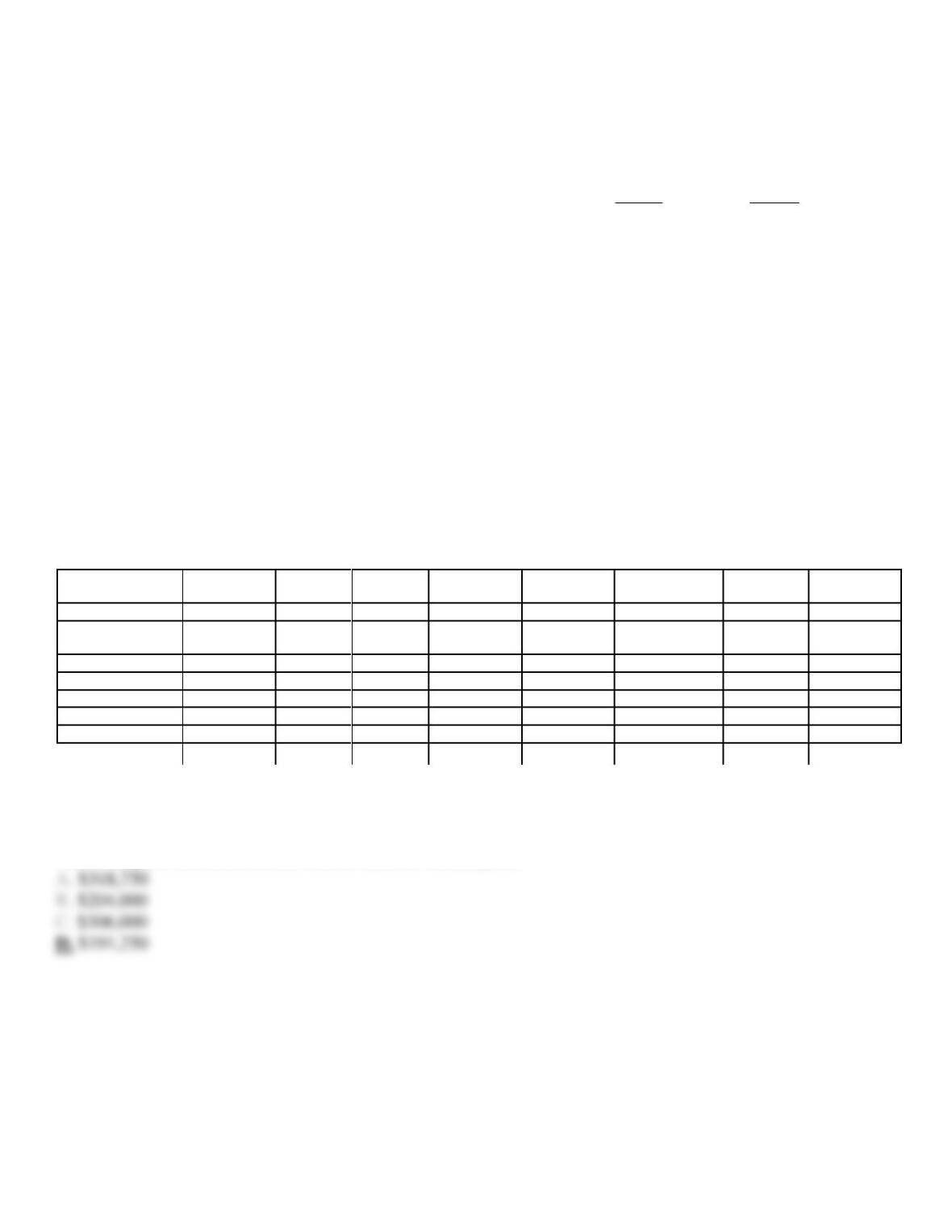

177. Figure 4-21

Appleby Manufacturing uses an activity-based costing system. The company produces Model F and Model G.

Information relating to the two products is as follows:

Model F

Model G

Units produced

24,000

30,000

Machine hours

7,500

8,500

Direct labor hours

8,000

12,000

Material handling (number of moves)

4,000

6,000

Setups

5,000

7,000

Purchase orders

30

40

Inspections

10,000

14,000

Product line variations

8

12

The following overhead costs are reported for the following activities of the production process:

Material handling

$ 40,000

Labor-related overhead

120,000

Setups

60,000

Product design

100,000

Batch inspections

120,000

Central purchasing

70,000

Jones manufacturing has used activity based costing to assign costs to Models F and G as given in the table below:

Activity

Cost Pool

Driver

Pool

Rate

Model F

Activity

Model F Cost

Model G Activity

Model G Cost

Total

Material handling

$40,000

10,000

$4

4,000

$16,000

6,000

$24,000

$40,000

Labor related

overhead

$120,000

20,000

$6

8,000

$48,000

12,000

$72,000

$120,000

Setups

$60,000

12,000

$5

5,000

$25,000

7,000

$35,000

$60,000

Product design

$100,000

20

$5,000

8

$40,000

12

$60,000

$100,000

Batch inspections

$120,000

24,000

$5

10,000

$50,000

14,000

$70,000

$120,000

Central purchasing

$70,000

70

$1,000

30

$30,000

40

$40,000

$70,000

total

$209,000

$301,000

$510,000

Appleby Manufacturing wants to implement an approximately relevant ABC system by using the two most expensive activities for cost assignment.

Refer to Figure 4-21. Under the equally accurate reduced ABC system, what are the global consumption ratios for Model F and Model G

178. Figure 4-21

Appleby Manufacturing uses an activity-based costing system. The company produces Model F and Model G.

Information relating to the two products is as follows:

Model F

Model G

Units produced

24,000

30,000

Machine hours

7,500

8,500

Direct labor hours

8,000

12,000

Material handling (number of moves)

4,000

6,000

Setups

5,000

7,000

Purchase orders

30

40

Inspections

10,000

14,000

Product line variations

8

12

The following overhead costs are reported for the following activities of the production process:

Material handling

$ 40,000

Labor-related overhead

120,000

Setups

60,000

Product design

100,000

Batch inspections

120,000

Central purchasing

70,000

Jones manufacturing has used activity based costing to assign costs to Models F and G as given in the table below:

Activity

Cost Pool

Driver

Pool

Rate

Model F

Activity

Model F Cost

Model G Activity

Model G Cost

Total

Material handling

$40,000

10,000

$4

4,000

$16,000

6,000

$24,000

$40,000

Labor related

overhead

$120,000

20,000

$6

8,000

$48,000

12,000

$72,000

$120,000

Setups

$60,000

12,000

$5

5,000

$25,000

7,000

$35,000

$60,000

Product design

$100,000

20

$5,000

8

$40,000

12

$60,000

$100,000

Batch inspections

$120,000

24,000

$5

10,000

$50,000

14,000

$70,000

$120,000

Central purchasing

$70,000

70

$1,000

30

$30,000

40

$40,000

$70,000

total

$209,000

$301,000

$510,000

Appleby Manufacturing wants to implement an approximately relevant ABC system by using the two most expensive activities for cost assignment.

Refer to Figure 4-21. Under the equally accurate reduced ABC system, using consumption ratios for labor related and batch inspections, the

overhead assigned to labor related activities would be? (round to 5 decimal places)

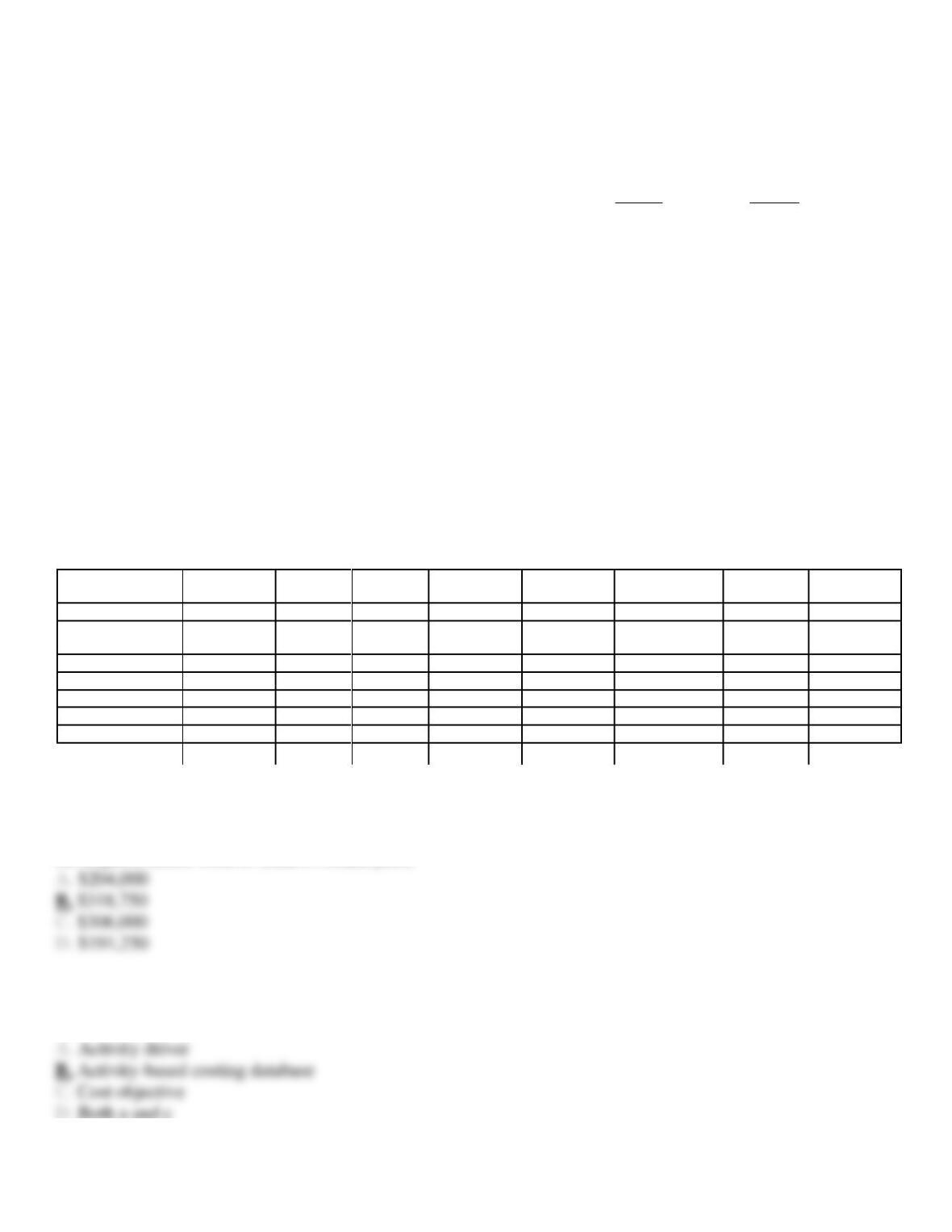

179. Figure 4-21

Appleby Manufacturing uses an activity-based costing system. The company produces Model F and Model G.

Information relating to the two products is as follows:

Model F

Model G

Units produced

24,000

30,000

Machine hours

7,500

8,500

Direct labor hours

8,000

12,000

Material handling (number of moves)

4,000

6,000

Setups

5,000

7,000

Purchase orders

30

40

Inspections

10,000

14,000

Product line variations

8

12

The following overhead costs are reported for the following activities of the production process:

Material handling

$ 40,000

Labor-related overhead

120,000

Setups

60,000

Product design

100,000

Batch inspections

120,000

Central purchasing

70,000

Jones manufacturing has used activity based costing to assign costs to Models F and G as given in the table below:

Activity

Cost Pool

Driver

Pool

Rate

Model F

Activity

Model F Cost

Model G Activity

Model G Cost

Total

Material handling

$40,000

10,000

$4

4,000

$16,000

6,000

$24,000

$40,000

Labor related

overhead

$120,000

20,000

$6

8,000

$48,000

12,000

$72,000

$120,000

Setups

$60,000

12,000

$5

5,000

$25,000

7,000

$35,000

$60,000

Product design

$100,000

20

$5,000

8

$40,000

12

$60,000

$100,000

Batch inspections

$120,000

24,000

$5

10,000

$50,000

14,000

$70,000

$120,000

Central purchasing

$70,000

70

$1,000

30

$30,000

40

$40,000

$70,000

total

$209,000

$301,000

$510,000

Appleby Manufacturing wants to implement an approximately relevant ABC system by using the two most expensive activities for cost assignment.

Refer to Figure 4-21. Under equally accurate reduced ABC system, using consumption ratios for labor related and batch inspections, the overhead

cost assigned to Model F would be? (round to 5 decimal places)

180. The collected data sets that are organized and interrelated for use by an organization’s ABC information

system is(are):

181. Figure 4-22

The Wellness Clinic is considering a time-driven activity based costing system. Given the following data:

Resources

Activities

time/activity

supervision

$ 60,000

treating patients

1.40 hr.

supplies and uniforms

$ 80,000

providing hygienic care

1.00 hr

salaries

$350,000

responding to requests

0.60 hr

computer

$ 10,000

monitoring patients

1.00 hr

monitor

$ 25,000

Total

$525,000

Total nursing hours

(practical capacity)

15,000

Refer to Figure 4-22. What is the capacity cost rate?

182. Figure 4-22

The Wellness Clinic is considering a time-driven activity based costing system. Given the following data:

Resources

Activities

time/activity

supervision

$ 60,000

treating patients

1.40 hr.

supplies and uniforms

$ 80,000

providing hygienic care

1.00 hr

salaries

$350,000

responding to requests

0.60 hr

computer

$ 10,000

monitoring patients

1.00 hr

monitor

$ 25,000

Total

$525,000

Total nursing hours

(practical capacity)

15,000

Refer to Figure 4-22. What is the activity rate for treating patients?

183. Figure 4-22

The Wellness Clinic is considering a time-driven activity based costing system. Given the following data:

Resources

Activities

time/activity

supervision

$ 60,000

treating patients

1.40 hr.

supplies and uniforms

$ 80,000

providing hygienic care

1.00 hr

salaries

$350,000

responding to requests

0.60 hr

computer

$ 10,000

monitoring patients

1.00 hr

monitor

$ 25,000

Total

$525,000

Total nursing hours

(practical capacity)

15,000

Refer to Figure 4-22. What is the activity rate for responding to requests?

184. The grouping of logically related information is called:

185. Which of the following statements is TRUE?

186. In an approximately relevant ABC system

187. In the time-driven ABC systems, managers

188. In a time-driven ABC system, once the managers determine the cost of per time unit of supplying

resources to activities, the next step would be

189. If operations run on less than full capacity, what is the result on cost driver rates?

190. Which of the following is NOT an advantage of a time-driven ABC system?

191. The Roanoke plant of the Virginia Company has two production departments: Extrusion and Assembly.

The plant produces two products: P and Q. Cost information for the production departments is given below:

Extrusion

$360,000

Assembly

750,000

The following table presents activity information about the departments and products:

Extrusion

Assembly

Total

Direct labor hours:

P

10,000

20,000

30,000

Q

10,000

30,000

40,000

Total

20,000

50,000

70,000

Machine hours:

P

5,000

1,000

6,000

Q

15,000

2,000

17,000

Total

20,000

3,000

23,000

Required:

a.

Compute the predetermined overhead rate for each department if Extrusion uses machine hours and Assembly uses labor hours.

b.

Calculate the per unit overhead rate for each product if 80,000 units of P were produced and 90,000 units of Q were produced.

a.

Extrusions

$ 360,000

Machine hours

20,000

Overhead rate

Assembly

750,000

Labor hours

50,000

Overhead rate

b.

P

Q

units produced

80,000

90,000

overhead applied to production

Extrusion:

$18 x 5000

$ 90,000

$18 x 15,000

$270,000

Assembly

$15 x 20,000

$300,000

Total

$390,000

$720,000

Overhead per Unit

$4.875

$8

192. Lavender Company has decided to use a predetermined rate to assign factory overhead to production. The

following predictions have been made for 2014:

Total factory overhead costs

$150,000

Direct labor hours

40,000 hours

Direct labor costs

$200,000

Machine hours

60,000 hours

Required:

a.

Compute the predetermined factory overhead rate under three different bases: (1) direct labor hours, (2) direct labor costs, and (3) machine

hours.

b.

Assume that actual factory overhead was $152,500 and that Lavender elected to apply factory overhead to Work in Process based on direct

labor hours. If actual direct labor was 42,000 hours for 2014, was factory overhead overapplied or underapplied? By how much?

c.

Lavender Company follows the policy of writing off any under- or overapplied factory overhead balance to Cost of Goods Sold at the end

of the year. Make the entry necessary at the end of 2014 to dispose of the factory overhead balance determined in Part (b).

(1) Direct labor hours: ($150,000/40,000 hours) = $3.75 per DLH

(2) Direct labor costs: ($150,000/$200,000) = 75% of DLC

(3) Machine hours: ($150,000/60,000 hours) = $2.50 per MH

Overhead applied (42,000 ´ $3.75)

$157,500

Actual overhead

152,500

Overapplied overhead by

$ 5,000

Factory Overhead

5,000

Cost of Goods Sold

5,000

193. The Custom Guitar Company uses a predetermined overhead rate of $5 per machine hour to apply

overhead. During the year, 32,500 machine hours were worked. Actual manufacturing overhead cost for the

year was $187,500. Company records showed the following account balances at the end of the year:

Materials

$ 22,500

Work in process

37,500

Finished goods

50,000

Cost of goods sold

112,500

Required:

a.

Determine the amount of underapplied or overapplied overhead.

b.

Assuming the amount of underapplied or overapplied overhead is material, determine underapplied or overapplied overhead that would be

allocated to the following accounts if the allocation is made using ending account balances:

Work in Process

Finished Goods

Cost of Goods Sold

c.

Assuming the amount of underapplied or overapplied overhead is material, calculate the new balance of the following accounts after

underapplied or overapplied overhead has been allocated:

Work in Process

Finished Goods

Cost of Goods Sold

d.

Determine the balance of Cost of Goods Sold if underapplied or overapplied overhead is immaterial.

$25,000 underapplied

$187,500 – ($5 ´ 32,500)

b.

Work in Process, $4,687.50

$25,000 ´ ($37,500/$200,000)

Finished Goods, $6,250.00

$25,000 ´ ($50,000/$200,000)

Cost of Goods Sold, $14,062.50

$25,000 ´ ($112,500/$200,000)

c.

Work in Process, $42,187.50 = $37,500 + $4687.50

Finished Goods, $56,250 = $50,000 + $6,250

Cost of Goods Sold, $126,562.50 = $112,500 + $14,062.50

d.

$137,500 = $112,500 + $25,000

194. The Anchorage plant of the Tundra Company produces two calculators and has two production

departments: assembly and packaging. Information for the products is given below:

Deluxe

Regular

Total

Units produced

20,000

200,000

Prime costs

$160,000

$1,500,000

$1,660,000

Direct labor hours

20,000

160,000

180,000

Number of setups

60

40

100

Machine hours

10,000

80,000

90,000

Inspection hours

2,000

16,000

18,000

Number of moves

180

120

300

The following table presents activity information about the departments and products:

Assembly

Packaging

Total

Direct labor hours:

Deluxe

10,000

10,000

20,000

Regular

150,000

10,000

160,000

Total

160,000

20,000

180,000

Machine hours:

Deluxe

2,000

8,000

10,000

Regular

8,000

72,000

80,000

Total

10,000

80,000

90,000

Overhead Costs:

Setting equipment

$120,000

$ 120,000

$240,000

Moving material

60,000

60,000

120,000

Machining

20,000

180,000

200,000

Inspection

16,000

144,000

160,000

Total

$216,000

$504,000

$720,000

Required:

a.

Compute the predetermined overhead rate for each department if Assembly uses labor hours and Packaging uses machine hours.

b.

Calculate the per unit cost for each product if departmental overhead rates are used. (Round to 2 decimal places)

c.

Compute the predetermined plant-wide overhead rate based on direct labor hours.

d.

Calculate the per unit cost of each product if a plantwide overhead rate is used.(Round to 2 decimal places)

e.

Calculate the overhead rates for each overhead activity.

f.

Calculate the per unit cost of each product if activity rates are used to assign overhead.

(Round to 2 decimal places)

a.

Assembly

$ 216,000

Labor hours

160,000

Overhead rate

$1.35

Packaging

$504,000

Machine hours

80,000

Overhead rate

$6.30

Units

20,000

200,000

Overhead applied to production

Assembly:

$1.35 ´ 10,000

13,500

Packaging

$6.30 ´ 8,000

50,400

$6.30 ´ 72,000

453,600

Overhead per Unit

$11.20

$10.78

Prime costs

$160,000

$1,500,000

Overhead costs

$4 ´ 20,000

80,000

Total costs

$240,000

$ 2,140,000

Unit cost

$10.70

Setting up equip

$240,000

$2,400 per setup

Machining

$200,000

90,000

$2.22 machine hour

Inspecting

$160,000

18,000

$8.89 per inspection hours

Units

20,000

200,000

Prime costs

$160,000

$1,500,000

$2,400 ´ 60

144,000

$2400 ´ 40

96,000

Moving materials

$400 ´ 120

48,000

Machining

$2.22 ´ 10,000

22,200

Inspecting

$8.89 ´ 2000

17,780

$8.89 ´ 16,000

142,240

Unit cost

$20.80

$9.82

195. Tusker Corporation manufactures two products (S and T). The overhead costs have been divided into four

cost pools that use the following activity drivers:

Number of

Number of

Machine

Packing

Product

Setups

Orders

Hours

Orders

S

20

35

1,000

75

T

5

70

1,500

125

Cost per pool

$15,000

$8,400

$120,000

$40,000

Required:

a.

Compute the allocation rates for each of the activity drivers listed.

b.

Allocate the overhead costs to Products S and T using activity-based costing.

c.

Compute the overhead rate using machine hours under the functional-based costing system.

d.

Allocate the overhead costs to Products S and T using the functional-based costing system overhead rate calculated in part (c).

Number of

Number of

Machine

Packing

Setups

Orders

Hours

Orders

Cost per pool

$15,000

$8,400

$120,000

$40,000

Allocation rate

$ 600

$ 80

$ 48

$ 200

b.

Product S

Product T

Number of setups

$12,000

$ 3,000

Number of orders

2,800

5,600

Machine hours

1,000 ´ $48 =

48,000

1,500 ´ $48 =

72,000

Packing orders

15,000

125 ´ $200 =

25,000

c.

($15,000 + $8,400 + $120,000 + $40,000)/2,500 = $73.36 per MH

d.

Product S: 1,000 ´ $73.36 = $73,360

Product T: 1,500 ´ $73.36 = $110,040