Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 4: Income Measurement and Accrual Accounting

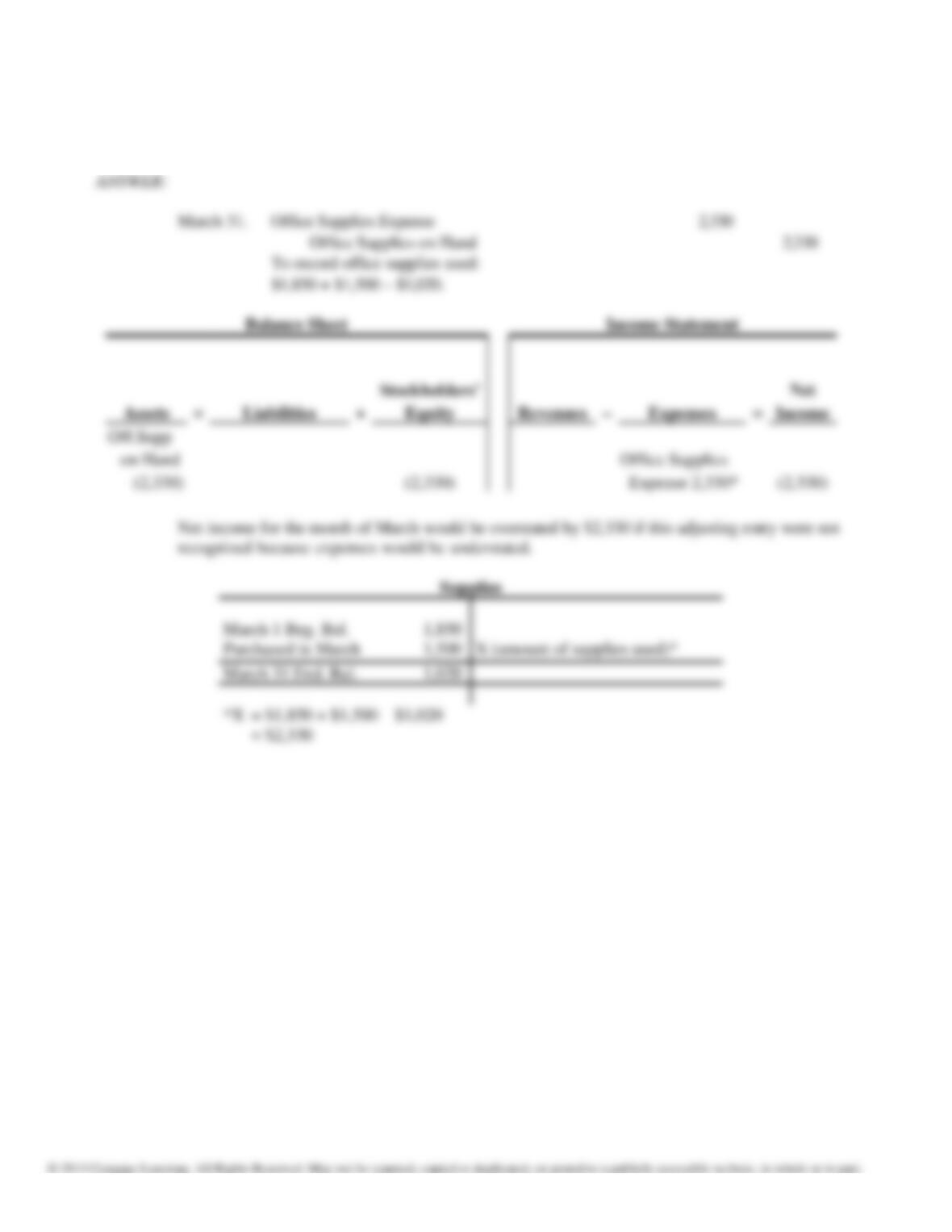

196. Quirin Corp. purchases office supplies once a month and prepares monthly financial statements. The asset account

Office Supplies on hand has a balance of $1,850 on March 1. Purchases of supplies during March amount to $1,500.

Supplies on hand at March 31 amount to $1,020. Prepare the necessary adjusting entry on Quirin’s books on March

31. What will be the effect on net income for March if this entry is not recorded?

Chapter 4: Income Measurement and Accrual Accounting

197. On May 1, 2014, Meehan Inc. lends $125,000 to Solar Power Inc. The loan will be repaid in 90 days with interest at

12%.

REQUIRED:

1. Prepare the journal entry on Meehan’s books on May 1, 2014.

2. Assume that Meehan prepares quarterly statements on May 30, 2014. Prepare the adjusting entry on Meehan’s

books on May 30, 2014 regarding the loan.

3. Prepare the entry on Meehan’s books on July 29, 2014, when Solar Power repays the principal and interest.

Chapter 4: Income Measurement and Accrual Accounting

198. Marion Construction owns property in Polk County. Marion’s 2014 property taxes amounted to $85,000. Polk

County will send out the 2015 property tax bills to property owners during April 2016. Taxes must be paid by June

1, 2016. Assume that Marion prepares adjusting entries only once a year, on December 31 for the entire year’s

taxes, and that property taxes for 2015 are expected to increase by 9% over those for 2014.

REQUIRED:

1. Prepare the adjusting entry required to record the 2015 property taxes payable on December 31, 2015.

2. Prepare the journal entry to record the payment of the 2015 property taxes on June 1, 2016.

Chapter 4: Income Measurement and Accrual Accounting

199. Brooke Accounting Services collected $15,000 from a customer on June 1 and agreed to provide accounting

services during the next six months. Brooke expects to provide an equal amount of services each month.

REQUIRED:

1. Prepare the journal entry for the receipt of the customer deposit on June 1.

2. Prepare the adjusting entry on June 30.

3. What will be the effect on net income for June if the entry in (2) is not recorded?

Chapter 4: Income Measurement and Accrual Accounting

200. On October 1, 2014, Winter Corp. buys a computer system for $270,000 in cash. Assume that the computer is

expected to have a five-year life and an estimated salvage value of $30,000 at the end of that time.

REQUIRED:

1. Prepare the journal entry to record the purchase of the computer on October 1, 2014.

2. Compute the depreciable cost of the computer.

3. Using the straight-line method, compute the monthly depreciation.

4. Prepare the adjusting entry to record depreciation at the end of October 2014.

5. Compute the computer’s carrying value that will be shown on Winter’s balance sheet prepared on December 31,

2014.

Chapter 4: Income Measurement and Accrual Accounting

5. Computer $270,000

Less: Accumulated depreciation (3 months × $4,000/month) (12,000)

Carrying value $258,000

201. Morgan Realty reported the following accounts on its income statement:

Commissions Earned

$83,000

Travel and Entertainment

4,500

Real Estate Board Fees Paid

8,000

Insurance Expired

780

Computer Line Charge

765

Advertising Expense

1,460

Depreciation on Computer

450

Office Supplies Used

940

Car Expenses

2,200

REQUIRED:

1. Prepare the necessary entries to close the temporary accounts.

2. Explain why the closing entries are necessary and when they should be recorded.

Chapter 4: Income Measurement and Accrual Accounting

202. The following accounts appear on Treetop Inc. 2014 financial statements. The accounts are listed in alphabetical

order, and the balance in each account is the normal balance for that account. All amounts are in millions of dollars.

Prepare closing entries for Treetop for 2014.

Cash Dividends Paid

$ 104

Cost of Sales and Related Buying and Occupancy Costs

4,317

Credit Card Revenues

325

Income Tax Expense

207

Interest Expense, net

126

Other Income and Expense, net

13

Net Sales

7,172

Selling, General and Administrative Expenses—Credit Segment

275

Selling, General and Administrative Expenses—Retail Stores,

Direct and Other Segments 2,228

Chapter 4: Income Measurement and Accrual Accounting

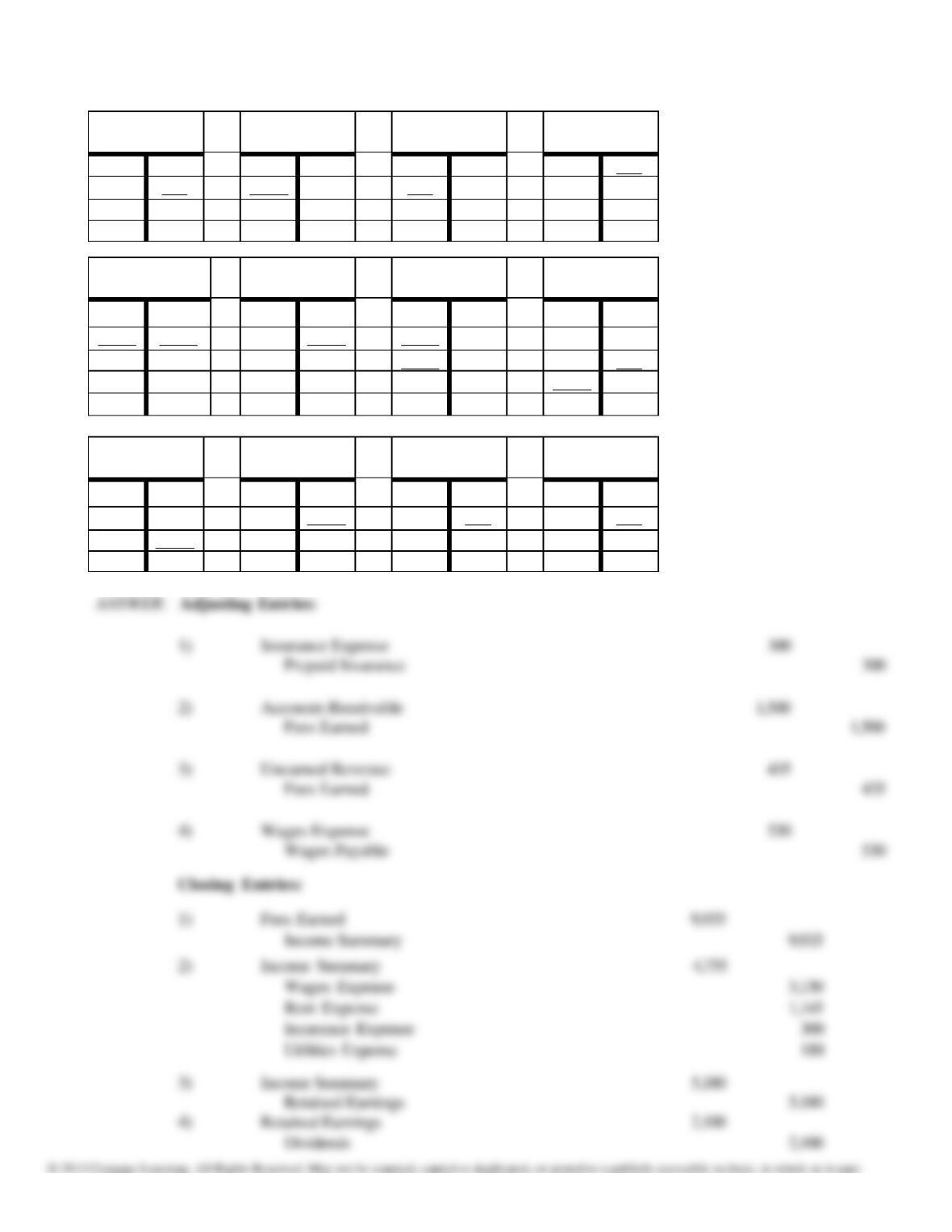

203. Reconstruct the adjusting and closing entries from the following T-Accounts.

Prepaid

Insurance

Accounts

Receivable.

Unearned

Revenues

Wages

Payable

1,200

6,000

1,350

530

300

1,500

435

530

900

7,500

915

Retained

Earnings

Dividends

Income

Summary

Fees Earned

12,280

2,100

9,935

8,000

2,100

5,180

2,100

4,655

1,500

15,360

0

5,280

435

0

9,935

0

Wages

Expense

Rent Expense

Insurance

Expense

Utilities

Expense

2,600

1,145

300

180

530

1,145

300

180

3,130

0

0

0

0

Chapter 4: Income Measurement and Accrual Accounting

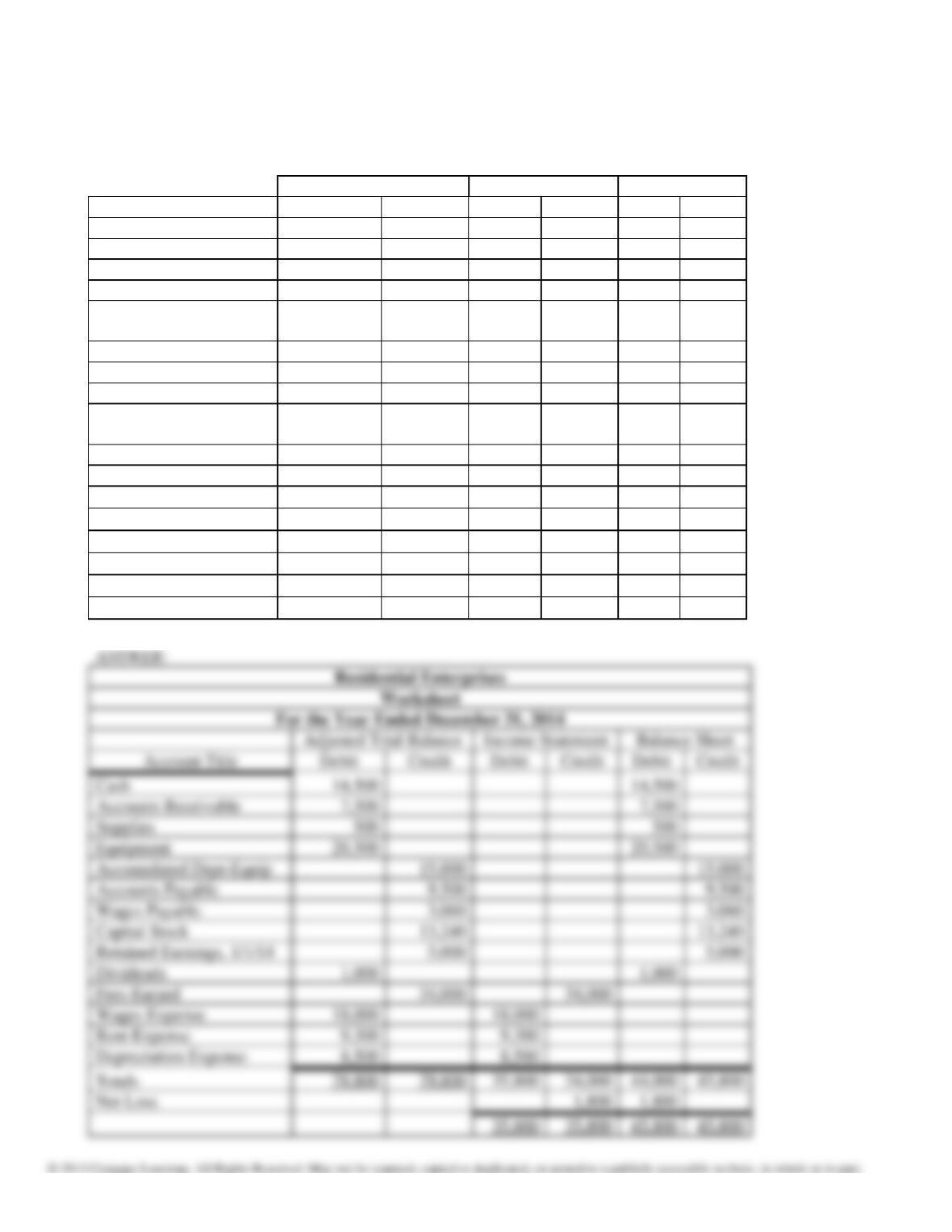

204. Complete the following work sheet for Residential Enterprises.

Residential Enterprises

Worksheet

For the Year Ended December 31, 2014

Adjusted Trial Balance

Income Statement

Balance Sheet

Account Title

Debit

Credit

Debit

Credit

Debit

Credit

Cash

14,500

Accounts Receivable

7,500

Supplies

500

Equipment

20,500

Accumulated Depr-

Equip

15,000

Accounts Payable

9,500

Wages Payable

3,060

Capital Stock

13,240

Retained Earnings,

1/1/14

5,000

Dividends

1,000

Fees Earned

34,000

Wages Expense

18,000

Rent Expense

9,300

Depreciation Expense

8,500

Totals

79,800

79,800

Net Income (Loss)

Chapter 4: Income Measurement and Accrual Accounting

205. What two choices must be made in the measurement process for a company that acquires a piece of equipment

and needs to record it in the accounting records? Explain.

206. Describe the benefit(s) of using the accrual process as compared to the cash basis.

207. Why does the accrual basis of accounting require adjustments, while the cash basis does not?

208. Why is the cash basis of accounting too limited for proper financial reporting?

209. What is the revenue recognition principle? Are there any exceptions to this rule? If so, what are they? If not,

explain why

210. What is the matching principle? How does it relate to the revenue recognition process?

211. What role do accounting records play in the adjustment process?

212. What is the significance of the timing in which cash is paid or received as it relates to the adjusting process?

Chapter 4: Income Measurement and Accrual Accounting

213. Explain the differences between the cash and accrual basis of accounting and how the adjusting process fits in.

214. Explain the purpose of a work sheet.

215. Does the Retained Earnings account that appears in the balance sheet credit column of a work sheet reflect the

beginning or the ending balance in the account? Explain.

216. Answer each of the following questions (a-c) with a separate short paragraph per question.

(a) What is the difference between a real account and a nominal account? Give an example of each type of

account. Why is this distinction important for the closing process?

(b) What two purposes are served in making closing entries?

(c) Why is the Dividends account closed directly to Retained Earnings rather than to the Income Summary

account?

217. Assuming the use of a work sheet, are the formal adjusting entries recorded and posted to the accounts before or

after the financial statements are prepared? Explain your answer. Would your answer change if a work sheet was

not prepared? Explain.

Chapter 4: Income Measurement and Accrual Accounting

218. The balance sheet columns of the work sheet for Barrows Corporation show total debits and total credits of

$245,000 each. Dividends for the period are $5,000. Accumulated depreciation is $15,000 at the end of the period.

Compute the amount that should appear on the formal balance sheet for total assets. How do you explain the

difference between this amount and the amount that appears as the total debits and total credits on the work sheet?

Select the correct revenue recognition principle for each of the following.

a. Recognize revenue over the passage of time.

b. Recognize revenue when the customer takes possession of the product.

c. Recognize revenue when cash is collected.

d. Recognize revenue when service is performed.

219. Interest

220. Rent

221. Merchandise

222. Carpet cleaning

Match the most probable matching method to the costs listed below.

a. Directly match a specific revenue.

b. Indirectly match with the period during which it will provide revenue.

c. Immediately recognize because no future benefits are expected.

223. Warehouse used for storing inventory goods

224. Commissions earned by sales people

225. Cost of two-year insurance policy

Chapter 4: Income Measurement and Accrual Accounting

226. Taxes owed on income earned during the current period

Match the following choices to the listed situation.

a. a deferred expense

b. a deferred revenue

c. an accrued liability

d. an accrued asset

227. One year's premium on truck insurance was paid in advance

228. Cash was collected from customers for rental of tents for next year

229. A warehouse building was acquired for cash

230. Income taxes are owed to the federal government at year end

231. Rent is owed by a tenant but not yet collected

For each transaction select the letter of the type of adjustment that would be required

a. Deferred expense

b. Deferred revenue

c. Accrued liability

d. Accrued asset

232. Depreciation on a delivery truck is recorded

233. Revenue is earned during the current period, although customers had paid in a previous period

234. Interest earned on notes receivable, but not yet received is recorded

235. The cost of supplies used during the current year is determined and recorded

236. The cost of salaries earned by employees, but not paid at the end of the accounting period is recorded

For each transaction select the letter of the type of adjustment that would be required.

a. Deferred expense

b. Deferred revenue

c. Accrued liability

d. Accrued asset

Chapter 4: Income Measurement and Accrual Accounting

237. Amounts earned, not received from customers are recorded

238. Magazine subscriptions are delivered during the current period, although customers had paid in a previous period

239. Interest is incurred on money borrowed from the bank, but not yet paid

240. The depreciation on office equipment used during the current year is recorded

241. The cost of commissions to salesmen that has been earned, but not paid at the end of the accounting period is

recorded

From the list of accounts below, determine whether the account would be a nominal account or a real

account.

a. nominal account

b. real account

242. Cash

243. Sales Revenue

244. Office Equipment

245. Depreciation Expense

246. Prepaid Rent

247. Unearned Revenue

248. Utilities Expense

249. Interest Payable

Chapter 4: Income Measurement and Accrual Accounting

250. A decline in purchasing power is evidenced by all of the following except:

a. inflation.

b. a continuing rise in the general level of prices in an economy.

c. buying the same amount of goods or services for a higher price a year later.

d. current value is equal to historical cost.

251. All of the following describe a revenue except:

a. A revenue can result in the inflow of assets.

b. A revenue can result in the settlement of liabilities from the delivery or distribution of goods.

c. A revenue can result in the settlement of liabilities from rendering services.

d. A revenue must involve an inflow of assets.

252. Which of the following statements is true concerning the matching principle?

a. All costs can be directly matched with revenue.

b. All costs can be indirectly matched with periods in which they provide a benefit.

c. The association of assets for a period with the liabilities necessary to generate the assets is known as the

matching principle.

d. Cost of goods sold matched with sales revenue is a classic example of direct matching under the matching

principle.

253. The unit of measure in Japan is the U.S. dollar.

a. True

b. False

254. The accounting profession is currently experimenting with financial statements adjusted for the changing value of

the dollar since inflation is increasing.

a. True

b. False

255. Because of its objective nature, historical cost is the attribute used to measure many of the assets recognized on the

balance sheet.

a. True

b. False

256. The income statement tells the reader about the actual cash inflows during a period of time.

a. True

b. False

257. The statement of cash flows reflects the revenues actually earned by the business, regardless of whether cash has

been collected.

a. True

b. False

258. The justification for the accrual basis of accounting lies in the needs of financial statement users for periodic

information on the financial position and the profitability of the entity.

a. True

b. False

259. The revenue recognition principle involves two factors: paid and incurred.

a. True

b. False

260. The revenue recognition principle does not pertain to long-term contracts, franchises, commodities, and installment

sales.

a. True

b. False

261. Conceptually, anytime a cost is incurred, an asset is acquired.

a. True

b. False

262. Costs incurred for purchases of merchandise result in an asset, Merchandise Inventory, and are eventually matched

with revenue at the time the product is sold.

a. True

b. False