Chapter 3 – The Adjusting Process

166. On January 2, Safe Motorcycling Monthly received a check for $72 from a subscriber for a 12-month subscription.

The January issue was mailed on January 15. Prepare the necessary entries for the month of January.

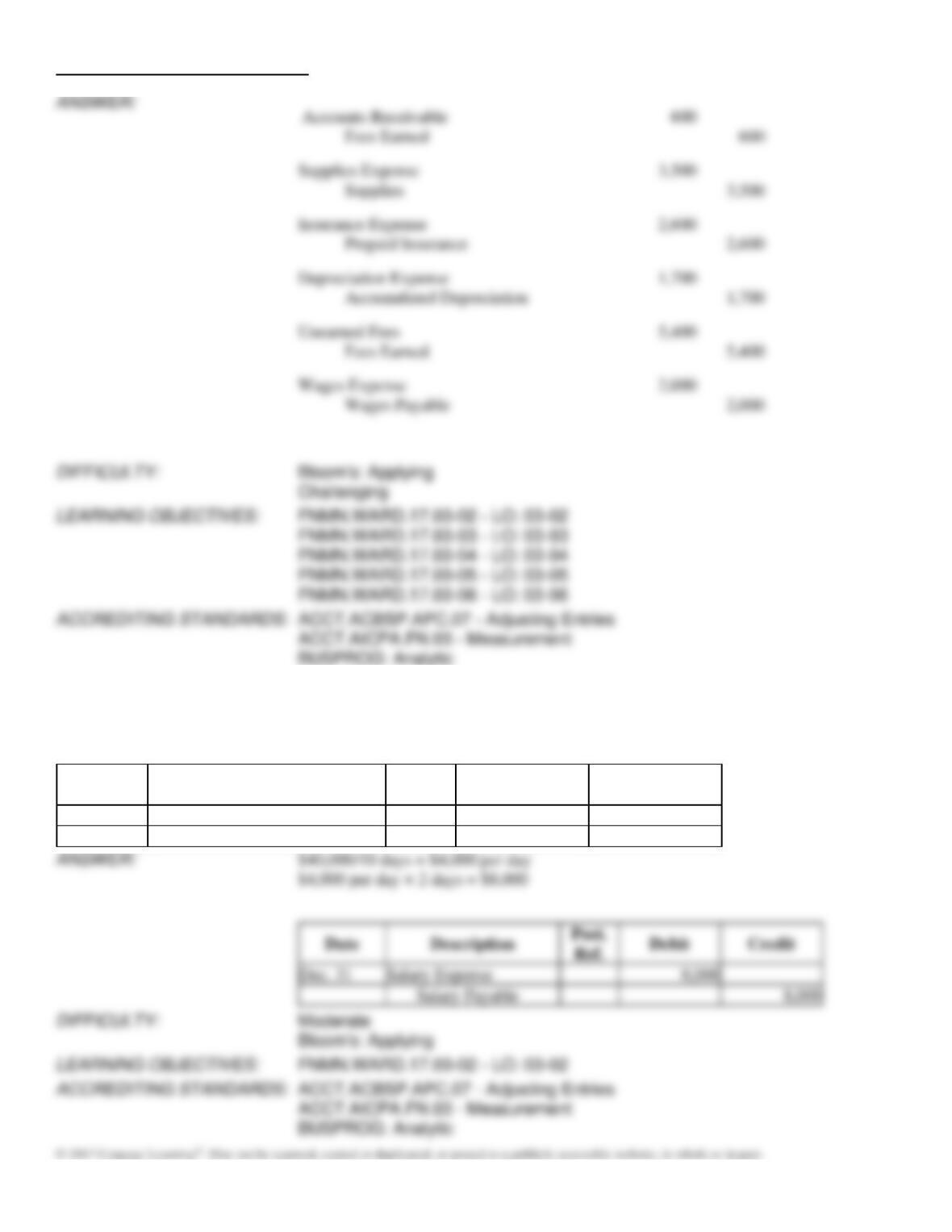

167. Prepare the December 31 adjusting entries for the following transactions. Omit explanations.

1. Fees accrued but not billed, $6,300

2. The Supplies account balance on December 31, $4,750; Supplies on hand, $960

3. Wages accrued but not paid, $2,700

4. Depreciation of office equipment, $1,650

5. Rent expired during year, $10,800

Date

Description

Post. Ref.

Debit

Credit

Chapter 3 – The Adjusting Process

Dec. 31

168. Prepare adjusting entries for the following transactions:

(a)

The beginning balance of the supplies account was $245. During the month the

company bought additional supplies in the amount of $735. At the end of the month a

physical inventory showed $343 of unused supplies.

(b)

The company has a 12% note payable in the amount of $17,000 due in 6 months. The

interest expense of $170 for the month has not been recorded.

(c)

The company has two employees. The manager is paid on the 15th of every month for

work performed during the first half of the month and on the 1st of the following month

for the work performed during the second half of the month. His monthly salary is

$5,500. The other employee is paid $650 for each 5-day work week (Monday –

Friday). The last day of the month fell on Thursday.

(d)

The unearned fees account shows a balance of $46,000. According to the manager 60%

of that amount has been earned.

(e)

At the end of the month $5,700 of services had been performed but not yet billed.

Chapter 3 – The Adjusting Process

Supplies Expense ($245 + $735 – $343)

Interest Expense [($17,000 × 12%)/12]

Wages and Salary Expense

Unearned Fees

($46,000 × 60%)

Accounts Receivable

169. Journalize the six entries to adjust the accounts at December 31. (Hint: One of the accounts was affected by two

different adjusting entries).

Unadjusted

Trial Balance

Adjusted

Trial Balance

Debit

Balances

Credit

Balances

Debit

Balances

Credit

Balances

Cash

5,000

5,000

Accounts Receivable

32,000

32,600

Supplies

3,600

100

Prepaid Insurance

4,000

1,400

Equipment

11,000

11,000

Accumulated Depreciation

1,700

Wages Payable

2,000

Unearned Fees

8,900

3,500

Common Stock

22,000

22,000

Fees Earned

69,000

75,000

Wages Expense

44,300

46,300

Supplies Expense

3,500

Insurance Expense

2,600

Depreciation Expense

1,700

Totals

99,900

99,900

104,200

104,200

Chapter 3 – The Adjusting Process

170. Bloom’s Company pays biweekly salaries of $40,000 every other Friday for a ten-day period ending on that day. The

last payday of December is Friday, December 27. Assuming the next pay period begins on Monday, December 30,

journalize the adjusting entry necessary at the end of the fiscal period (December 31).

Date

Description

Post.

Ref.

Debit

Credit

Chapter 3 – The Adjusting Process

171. A business pays biweekly salaries of $20,000 every other Friday for a ten-day period ending on that day. The last

payday of December is Friday, December 27. Assume the next pay period begins on Monday, December 30 and the

proper adjusting entry is journalized at the end of the fiscal period (December 31). Journalize the entry for the payment of

the payroll on Friday, January 10.

Date

Description

Post.

Ref.

Debit

Credit

172. At January 31, the end of the first month of the year, the usual adjusting entry transferring expired insurance to an

expense account is omitted. Which items will be incorrectly stated, because of the error, on (a) the income statement for

January and (b) the balance sheet as of January 31? Also indicate whether the items in error will be overstated or

understated.

Chapter 3 – The Adjusting Process

173. At the end of April, the first month of the company’s year, the usual adjusting entry transferring rent earned to a

revenue account from the unearned rent account was omitted. Indicate which items will be incorrectly stated, because of

the error, on (a) the income statement for April and (b) the balance sheet as of April 30. Also indicate whether the items

in error will be overstated or understated.

174. Salaries of $6,400 are paid for a five-day week on Friday. Prepare the adjusting journal entry that is required if the

month ends on Thursday.

175. Accrued salaries of $600 owed to employees for December 29, 30, and 31 are not taken into consideration in

preparing the financial statements for the year ended December 31. Indicate which items will be erroneously stated,

because of the error, on (a) the income statement for the year and (b) the balance sheet as of December 31. Also indicate

whether the items in error will be overstated or understated.

Chapter 3 – The Adjusting Process

176. For the year ending December 31, Beard Clinical Supplies Co. mistakenly omitted adjusting entries for (1) $9,800 of

unearned revenue that was earned, (2) earned revenue that was not billed of $10,200, and (3) accrued wages of

$7,000. Indicate the combined effect of the errors on (a) revenues, (b) expenses, and (c) net income.

177. On January 1, Great Designs Company had a debit balance of $1,450 in the office supplies account. During the

month, Great Designs purchased $115 and $160 of office supplies and journalized them to the asset account upon

purchasing. On January 31, an inspection of the office supplies cabinet shows that only $350 of office supplies remains.

Prepare the January 31 adjusting entry for office supplies.

178. For the year ending June 30, Island Clinical Services mistakenly omitted adjusting entries for (1) $1,500 of supplies

that were used, (2) unearned revenue of $4,200 that was earned, and (3) insurance of $5,000 that expired. What is the

combined effect of these errors on (a) revenues, (b) expenses, and (c) net income for the year ending June 30?

Chapter 3 – The Adjusting Process

179. On December 31, a business estimates depreciation on equipment used during the first year of operations to be

$2,900. (a) Journalize the adjusting entry required on December 31. (b) If the adjusting entry in (a) were omitted, which

items would be erroneously stated on (1) the income statement for the year and (2) the balance sheet as of December 31?

(b)

(1) Depreciation expense would be understated. Net income

would be overstated.

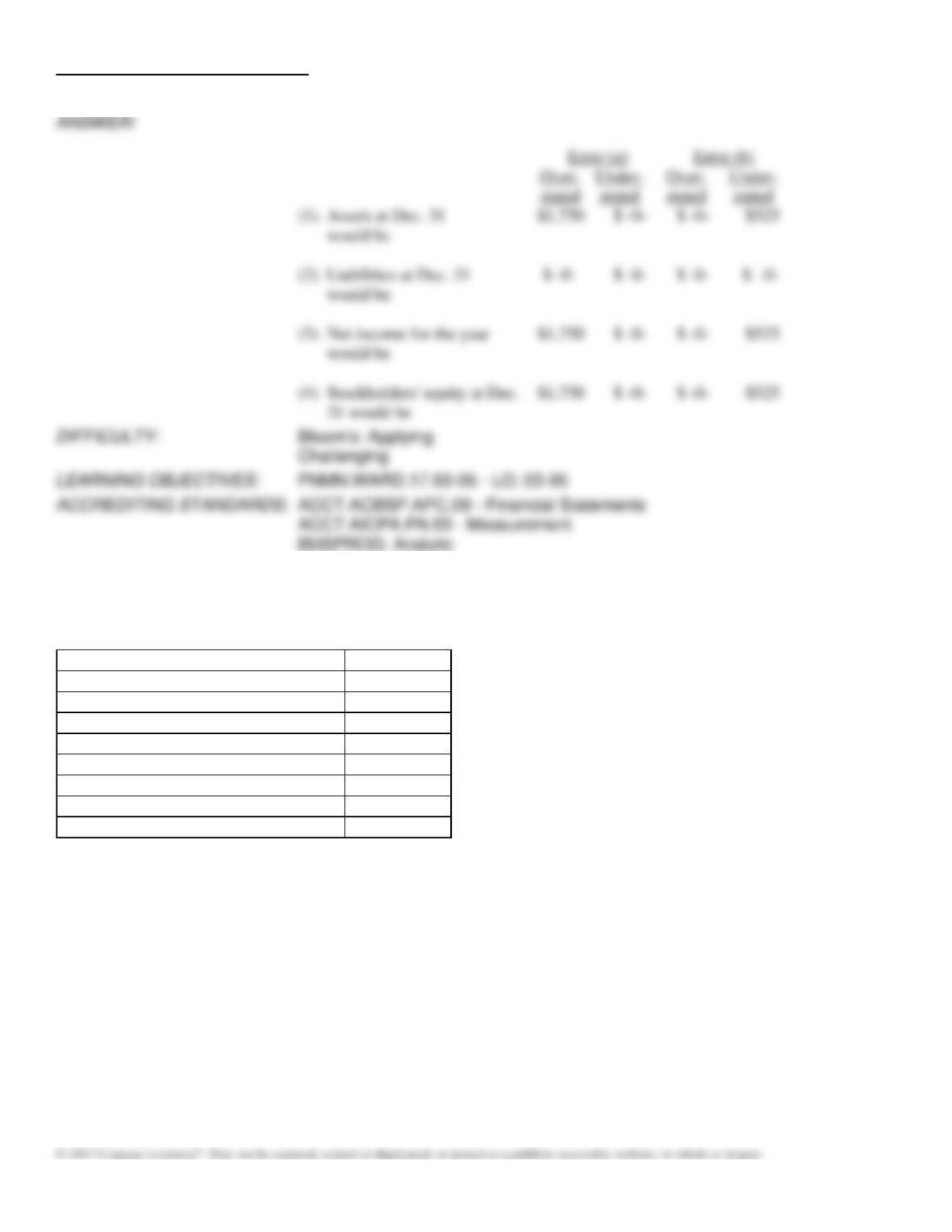

180. At the end of the fiscal year, the following adjusting entries were omitted:

(a)

No adjusting entry was made to transfer the $1,750 of prepaid insurance from the

asset account to the expense account.

(b)

No adjusting entry was made to record accrued fees of $525 for services provided

to customers.

Assuming that financial statements are prepared before the errors are discovered, indicate the effect of each error,

considered individually, by inserting the dollar amount in the appropriate spaces. Insert “0” if the error does not affect the

item.

Error (a)

Error (b)

Over-

stated

Under-

stated

Over-

stated

Under-

stated

(1) Assets at Dec. 31

would be

$

$

$

$

(2) Liabilities at Dec. 31

would be

$

$

$

$

Net income for the year

would be

$

$

$

$

Stockholders’ equity at Dec. 31

would be

$

$

$

$

Chapter 3 – The Adjusting Process

would be

181. Jordon James started JJJ Consulting on January 1. The following are the account balances at the end of the first

month of business, before adjusting entries were recorded:

Accounts Payable

$ 300

Accounts Receivable

750

Cash

6,300

Consulting Revenue

4,925

Equipment

7,000

Common Stock

15,000

Dividends

1,375

Prepaid Rent

4,000

Supplies

800

Adjustment data:

Supplies on hand at the end of the month, $200

Unbilled consulting revenue, $700

Rent expense for the month, $1,000

Depreciation on equipment, $90

(a) Prepare the required adjusting entries, adding accounts as needed.

(b) Prepare an adjusted trial balance for JJJ Consulting as of January 31.

Chapter 3 – The Adjusting Process

Chapter 3 – The Adjusting Process

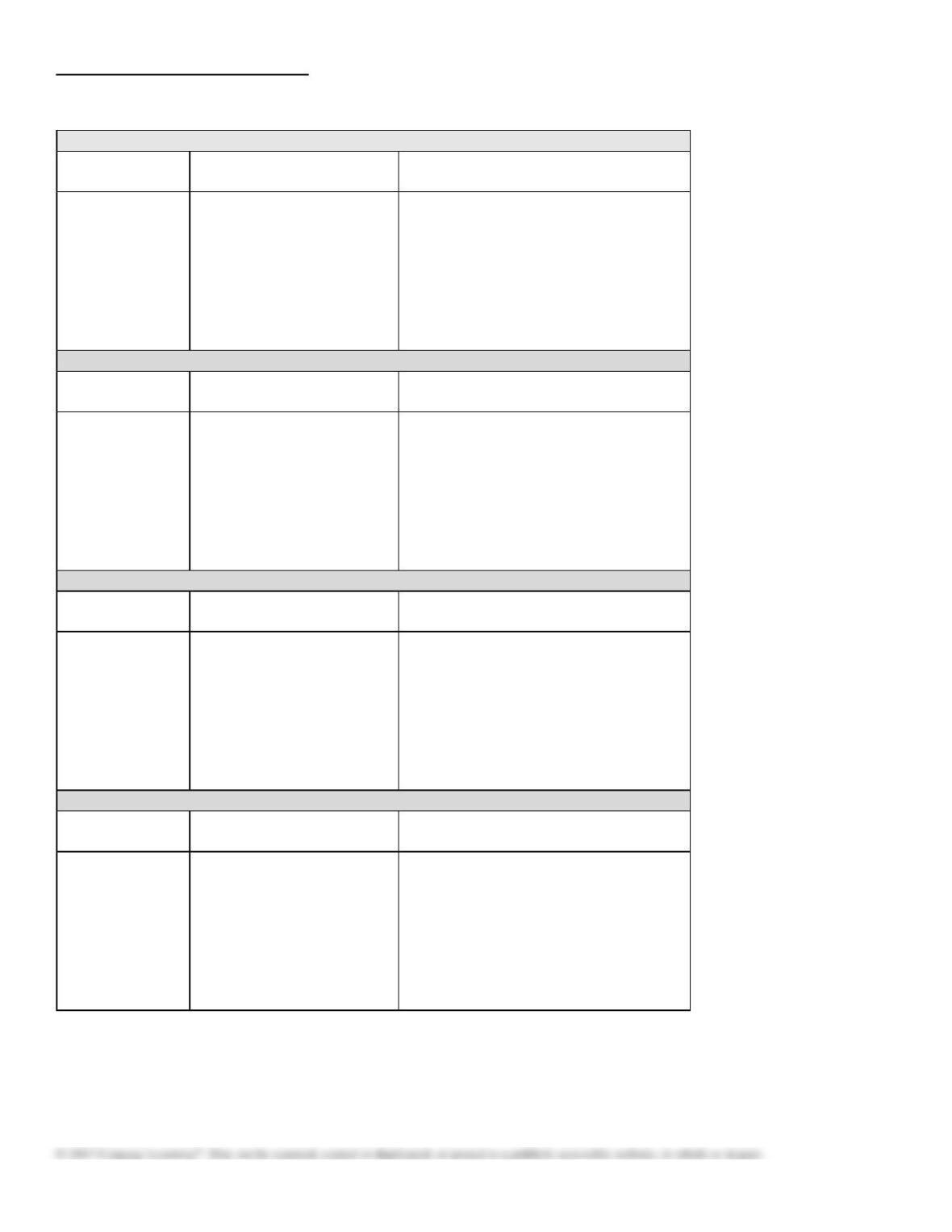

182. Complete the missing items in the Summary of Adjustments chart:

Prepaid Expenses

Examples

Adjusting Entry

Financial Statement Impact

if Adjusting Entry is Omitted

Supplies,

(a)

Dr. Expense

Cr. Asset

Income Statement:

Revenues: No effect

Expenses: Understated

Net income: (b)

Balance Sheet:

Assets: (c)

Liabilities: (d)

Stockholders’ equity: Overstated

Unearned Revenues

Examples

Adjusting Entry

Financial Statement Impact if

Adjusting Entry is Omitted

Unearned Rent,

(e)

(f)

Income Statement:

Revenues: (g)

Expenses: No effect

Net income: (h)

Balance Sheet:

Assets: (i)

Liabilities: Overstated

Stockholders’ equity: (j)

Accrued Revenues

Examples

Adjusting Entry

Financial Statement Impact if

Adjusting Entry is Omitted

Interest income

due on a note,

(k)

Dr. Asset

Cr. Revenue

Income Statement:

Revenues: (l)

Expenses: (m)

Net income: Understated

Balance Sheet:

Assets: (n)

Liabilities: (o)

Stockholders’ equity: Understated

Accrued Expenses

Examples

Adjusting Entry

Financial Statement Impact if

Adjusting Entry is Omitted

Interest due on a

note payable,

(p)

(q)

Income Statement:

Revenues: No effect

Expenses: (r)

Net income: (s)

Balance Sheet:

Assets: (t)

Liabilities: Understated

Stockholders’ equity: (u)

Chapter 3 – The Adjusting Process

Prepaid rent or Prepaid insurance

Fee or Magazine subscription received in

Dr. Liability, Cr. Revenue

Services performed but not yet billed

Unpaid wages

Dr. Expense, Cr. Liability

183. For each of the following errors, considered individually, indicate whether the error would cause the adjusted trial

balance totals to be unequal. If the error would cause the adjusted trial balance total to be unequal, indicate whether the

debit or credit total is higher and by how much.

a)

The adjustment for unearned fees of $3,260 was journalized as a debit to Accounts

Payable for $3,260 and a credit to Fees Earned of $3,260.

b)

The adjustment for supplies expense of $425 was journalized as a debit to Supplies

Expense for $542 and a credit to Supplies for $425.

Accounts Payable will be incorrect as the debit should have been made to

Unearned Fees instead of Accounts Payable.

The debit total exceeds the credit total by $117.

Chapter 3 – The Adjusting Process

184. Using the following account balances for Garry’s Tree Service, prepare a trial balance.

Cash

$25,000

Supplies

1,000

Accounts Payable

7,000

Common Stock

32,910

Wage Expense

2,000

Machinery

18,350

Wages Payable

3,600

Service Revenue

21,000

Rent Expense

11,500

Unearned Revenue

1,500

Accumulated Depreciation—Machinery

7,340

Prepaid Rent

12,200

Dividends

3,300

Cash

Supplies

Prepaid Rent

Machinery

Accumulated Depreciation—Machinery

Accounts Payable

Wages Payable

Unearned Revenue

Common Stock

Dividends

Service Revenue

Wage Expense

Rent Expense

185. Indicate whether the following error would cause the adjusted trial balance totals to be unequal. If the error would

cause the adjusted trial balance totals to be unequal, indicate whether the debit or credit total is higher and by how much.

The entry for $975 of supplies used during the period was journalized as a debit to Supplies Expense for $795 and credit

to Supplies for $975.

The total will be unequal with a credit total higher by $180 ($975 − $795).

Chapter 3 – The Adjusting Process

186. Indicate whether the following error would cause the adjusted trial balance totals to be unequal. If the error would

cause the adjusted trial balance totals to be unequal, indicate whether the debit or credit total is higher and by how much.

The adjustment for accrued fees of $1,170 was journalized as a debit to Accounts Receivable for $1,170 and a credit to

Fees Earned for $1,107.

The total will be unequal with a debit total higher by $63 ($1,170 − $1,107).

187. What is the purpose of an adjusted trial balance? What type(s) of error does it detect? What type(s) of error does it

not detect?

188. Two income statements for Midnight Enterprises are shown below:

Midnight Enterprises

Income Statement

For Year 1 and Year 2, Ended December 31

Year 2

Year 1

Fees earned

$674,350

$520,600

Operating expenses

472,045

338,390

Operating income

$202,305

$182,210

(a) Prepare a vertical analysis of Midnight Enterprises’ income statements.

(b) Does the vertical analysis indicate a favorable or unfavorable trend?

Chapter 3 – The Adjusting Process

Fees earned

Operating expenses

Operating income

LEARNING OBJECTIVES:

189. Two income statements for Danielle’s Design Services are shown below:

Danielle’s Design Services

Income Statements

For Years 1 and 2 Ending December 31

Year 2

Year 1

Fees earned

$765,340

$696,520

Operating expenses:

Wages expense

$254,000

$214,600

Rent expense

120,000

108,000

Supplies expense

76,500

98,715

Miscellaneous expense

11,680

16,420

Total operating expenses

$462,180

$437,735

Net income

$303,160

$258,785

(a) Prepare a vertical analysis of Danielle’s Design Services income statements.

(b) What types of trends are indicated: favorable or unfavorable?

(c) What other information would enhance the analysis?

Chapter 3 – The Adjusting Process

Chapter 3 – The Adjusting Process

Match the type of account (a – e) with the business transactions that follow.

a.

Prepaid expense

b.

Accrued expense

c.

Unearned revenue

d.

Accrued revenue

e.

None of these

DIFFICULTY:

Bloom’s: Remembering

Moderate

LEARNING OBJECTIVES:

FNMN.WARD.17.03-05 – LO: 03–05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.05 – Accounting Cycle

ACCT.ACBSP.APC.07 – Adjusting Entries

ACCT.ACBSP.APC.15 – Current Assets Reporting

ACCT.ACBSP.APC.16 – Current Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

190. Services provided that have not been recorded.

191. Paid for one year’s insurance policy.

192. Retainer fee received from a client for future legal representation.

193. Annual property taxes that are paid at the end of the year.

194. Electric bill to be paid next month.

195. Paid for a 6-month magazine subscription.

196. Received payment covering a 6-month magazine subscription.

197. Provided tutoring for a student that will be invoiced next month.

198. Received 6 months of rental payments from a tenant.

199. Paid 6 months of rental payments to the landlord.

200. Annual depreciation on equipment, recorded on a monthly basis.

Chapter 3 – The Adjusting Process

201. A contract to provide tutoring services beginning next month was signed.

Identify the effect (a – h) that omitting each of the following items would have on the balance sheet.

a.

Assets and stockholders’ equity overstated

b.

Assets and stockholders’ equity understated

c.

Assets overstated and stockholders’ equity understated

d.

Assets understated and stockholders’ equity overstated

e.

Liabilities and stockholders’ equity overstated

f.

Liabilities and stockholders’ equity understated

g.

Liabilities overstated and stockholders’ equity understated

h.

Liabilities understated and stockholders’ equity overstated

DIFFICULTY:

Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.03-05 – LO: 03-05

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.07 – Adjusting Entries

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

202. No adjustment was made for supplies used up during the month.

203. Wages are paid every Friday for the 5-day work week. The month ended on Monday and no adjustment was

recorded.

204. Interest earned on a note receivable was not recorded.

205. Services provided to customers on the last day of the month were not billed.

206. An attorney has earned 1/2 of a retainer fee that was received and recorded last month. No adjustment was recorded

for the amount earned.

207. Property taxes are paid annually. The estimated monthly amount for the taxes was not recorded.

208. Depreciation on equipment was not recorded.

209. A tenant paid 6 months’ rent in advance when he moved in on the first day of the month. No entry was made on the

last day of the month.