93. The budgeted cell conversion cost rate includes which of the following?

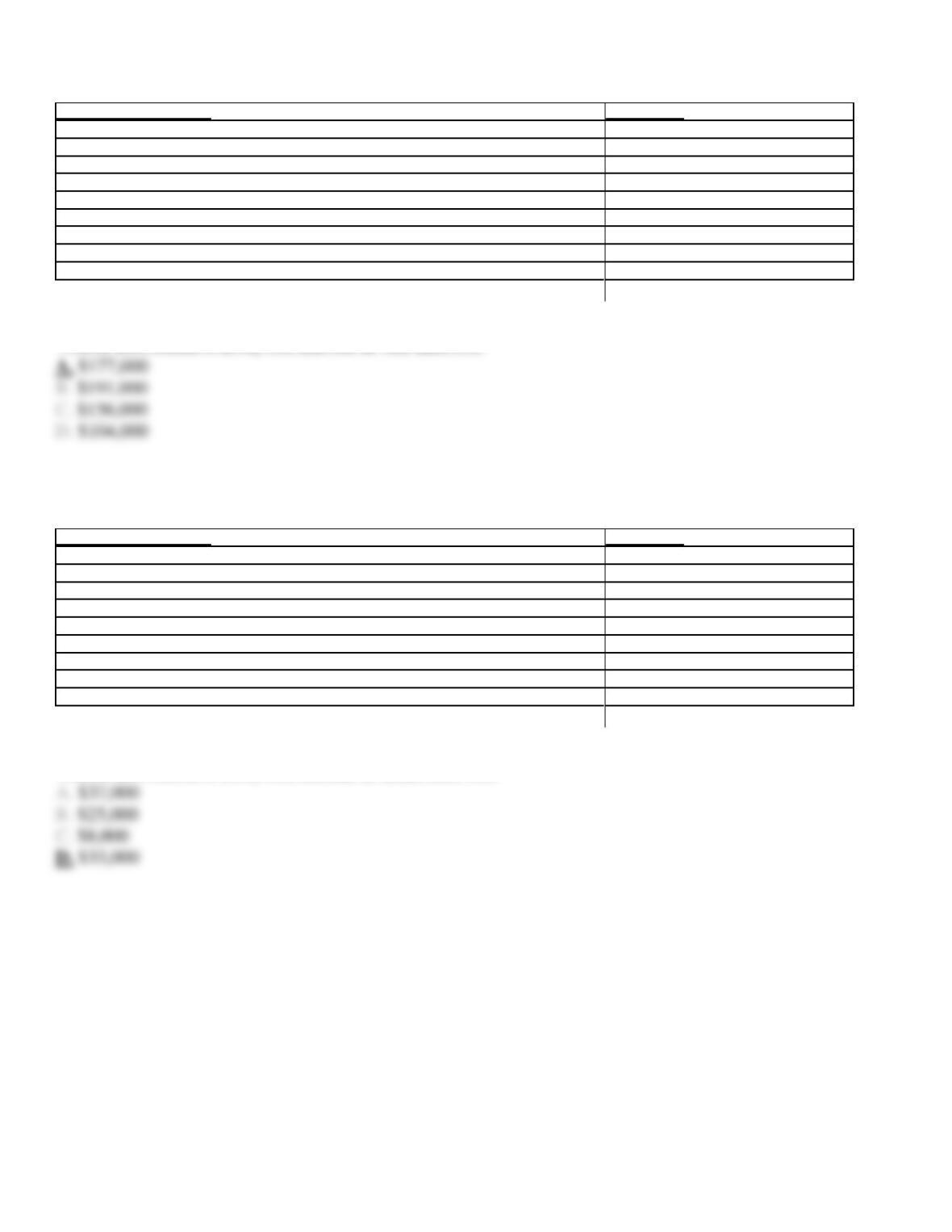

94. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Process audits

$50,000

Training of machine operators

28,000

Processing returned products

19,000

Scrap processing (disposal)

25,000

Rework

8,000

Preventative maintenance

30,000

Product design

46,000

Warranty work

12,000

Finished goods inspection

23,000

From the above schedule of activity costs, determine the total activity cost.

95. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Process audits

$50,000

Training of machine operators

28,000

Processing returned products

19,000

Scrap processing (disposal)

25,000

Rework

8,000

Preventative maintenance

30,000

Product design

46,000

Warranty work

12,000

Finished goods inspection

23,000

96. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Process audits

$50,000

Training of machine operators

28,000

Processing returned products

19,000

Scrap processing (disposal)

25,000

Rework

8,000

Preventative maintenance

30,000

Product design

46,000

Warranty work

12,000

Finished goods inspection

23,000

From the above schedule of activity costs, determine the value-added costs.

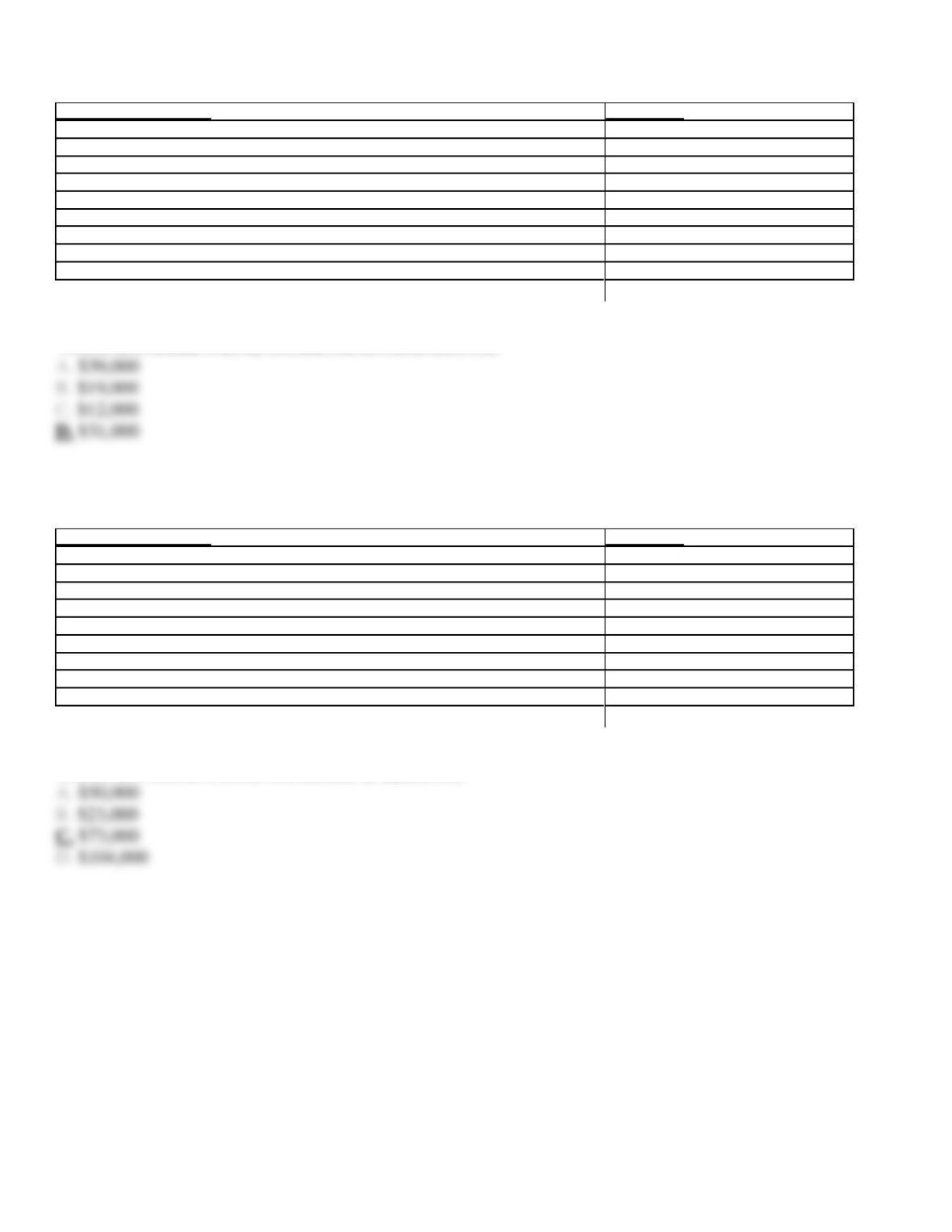

97. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Process audits

$50,000

Training of machine operators

28,000

Processing returned products

19,000

Scrap processing (disposal)

25,000

Rework

8,000

Preventative maintenance

30,000

Product design

46,000

Warranty work

12,000

Finished goods inspection

23,000

From the above schedule of activity costs, determine the internal failure costs.

98. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Process audits

$50,000

Training of machine operators

28,000

Processing returned products

19,000

Scrap processing (disposal)

25,000

Rework

8,000

Preventative maintenance

30,000

Product design

46,000

Warranty work

12,000

Finished goods inspection

23,000

From the above schedule of activity costs, determine the external failure costs.

99. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Process audits

$50,000

Training of machine operators

28,000

Processing returned products

19,000

Scrap processing (disposal)

25,000

Rework

8,000

Preventative maintenance

30,000

Product design

46,000

Warranty work

12,000

Finished goods inspection

23,000

From the above schedule of activity costs, determine the appraisal costs.

100. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Process audits

$50,000

Training of machine operators

28,000

Processing returned products

19,000

Scrap processing (disposal)

25,000

Rework

8,000

Preventative maintenance

30,000

Product design

46,000

Warranty work

12,000

Finished goods inspection

23,000

From the above schedule of activity costs, determine the prevention costs.

101. The local college is aggressively working in reducing the time that a student needs to enroll for each

semester. Which of the following changes would not help achieve this goal?

102. A college would like to increase enrollment by streamlining the enrollment process. Which of the

following would not fall in line with the college goal?

103. Which of the following statements is correct?

104. Which of the following is not a prevention cost?

105. Which of the following is not an external failure cost?

106. Which of the following statements best describes the relationship among the costs of quality?

107. Which of the following is a value-added activity?

108. Christmas Express makes wreaths in batch sizes of 12. The cutting & assembly process takes 7 minutes per

wreath and the decorating process time is 10 minutes per wreath. It takes 12 minutes to move the wreaths from

the cutting & assembly process to the decorating process.

(a) Compute the value-added, non-value-added, and the total lead time of the wreath process.

(b) Compute the value-added ratio. Round to the nearest decimal.

109. Which of the following are features of the just-in-time manufacturing system?

(a) maintaining excess inventory to ensure that products will always be available

(b) cross training of employees

(c) giving employees additional authority and responsibility

(d) product oriented layout

(e) increased set-up time

110. The Thudaka Company has budgeted its conversion cost for the small lamp production as $65,000 for

1,300 production hours. Each unit produced by the cell requires 15 minutes of process time. During the month,

3,800 units are manufactured in the cell. the estimated material cost is $18 per unit. Provide the following

journal entries.

(a) Materials are purchased to produce 4,000 units.

(b) Conversion costs are applied to 3,800 units of production.

(c) 3,650 units are placed into finished goods.

111. A quality control activity analysis indicated the following four activity costs of a hotel.

Verifying credit card information

$40,000

Customer service training

20,000

Discounting room rates due to poor customer service

16,000

Correcting charges to customer invoices

8,000

Total

$84,000

112. Connally Company’s payroll department required that every time card be checked twice to ensure pay

accuracy. The company has 1,000 employees and has determined that the checks cost the company $8,000 per

year. They have decided to change this policy and only check those names which appear on the exceptions

report and a random check on the entire payroll. Currently only 15% of the payroll is evaluated each payroll.

Determine the inspection activity cost per employee on the 1,000 employees both before and after the

improvement.

Cost of Quality Report

Prevention

$20,000

23.8%

2.7%

Appraisal

40,000

47.6%

5.3%

Internal Failure

16,000

19.1%

2.1%

External Failure

8,000

9.5%

1.1%

$84,000

100.0%

11.2%

113. Extreme Wreaths, Inc. makes wreaths in batch sizes of 15 at a time. The cutting & assembly process takes

10 minutes per wreath, and the decorating process time is 7 minutes per wreath. It takes 5 minutes to move the

wreaths from the cutting & assembly process to the decorating process.

In a effort to improve the lead time, the company has tried reducing the batch size to 10 units. The new process

is as follows: cutting & assembly process – 8 minutes. The decorating process is still 7 minutes per wreath. It

takes 5 minutes to move the wreaths from the cutting & assembly process to the decorating process.

(a) Compute the value-added, non-value-added, and the total lead time of the wreath process for both the old

and the new manufacturing process.

(b) Compute the value-added ratio for both the old and new process. Round to the nearest decimal.

114. Axelgold Company produces parts for the auto industry. Part X2 is machined in Department #1, which has

the following budgeted conversion costs:

Labor

$230,000

Depreciation

32,000

Maintenance

12,000

Supplies

26,000

Total

$300,000

All costs are driven by machine hours. Total possible hours for the year are 2,800. It takes .03 hours to machine one unit of Part X2.

(a)

Compute Department #1’s budgeted cell conversion cost rate for the current year.

Round to the nearest cent.

(b)

Compute Part X2’s budgeted cell conversion cost per unit. Round to the nearest cent.

115. Cariboo Pattern Company makes dressmakers’ patterns using a machine that stamps the pattern outline

onto tissue paper. The stamping center produced 40,000 patterns in August, with a machine time per pattern of

20 seconds. Annual budgeted cell conversion costs were as follows:

Maintenance and supplies

$ 650,000

Depreciation

700,000

Supporting labor

825,000

Total

$2,175,000

(a)

Budgeted cell conversion cost rate

= $300,000/2,800 hours

= $107.14 per machine hour

(b)

Part X2 machine hours

0.03

hrs. per unit

Budgeted cell conversion cost per unit

$ 3.21

per unit

116. Tucha Manufacturing Co. operates in a just-in–time (JIT) manufacturing environment. The company had

scheduled production of 95,000 units during February in its Y12 cell. Actual February production totaled

88,200 units. Tucha had budgeted conversion costs for February totaling $800,000 and budgeted production

hours totaling 2,000.

117. The Kwanika Co. operates in a just-in-time (JIT) manufacturing environment. During 2011, its first year of

operations, Kwanika budgeted for 40,000 hours in the production of 100,000 units in its cell X-22. Material

costs were $7 per unit. Cell X-22 conversion costs were budgeted for the year as follows:

Direct and indirect labor

$ 900,000

Machine depreciation

125,000

Maintenance and supplies

375,000

Utilities

225,000

Total

$1,625,000

During January, material for 8,400 units was purchased on account. There were 8,200 units manufactured and 8,000 were sold shipped to customers

for $35 each. Journalize: (a) the material purchases; (b) the application of conversion costs; (c) the transfer from work in process to finished goods;

and (d) the sales and associated cost of goods sold for the month of January.

Raw and In Process Inventory (8,400 ´ $7)

58,800

Accounts Payable

58,800

Raw and In Process Inventory (8,200 ´ $16.25)

133,250

Conversion Costs

133,250

Finished Goods Inventory (8,400 ´ $23.25)

190,650

Raw and In Process Inventory

190,650

Accounts Receivable (8,000 ´ $35)

280,000

Sales

280,000

Cost of Goods Sold (8,000 ´ $23.25)

186,000

Finished Goods Inventory

186,000

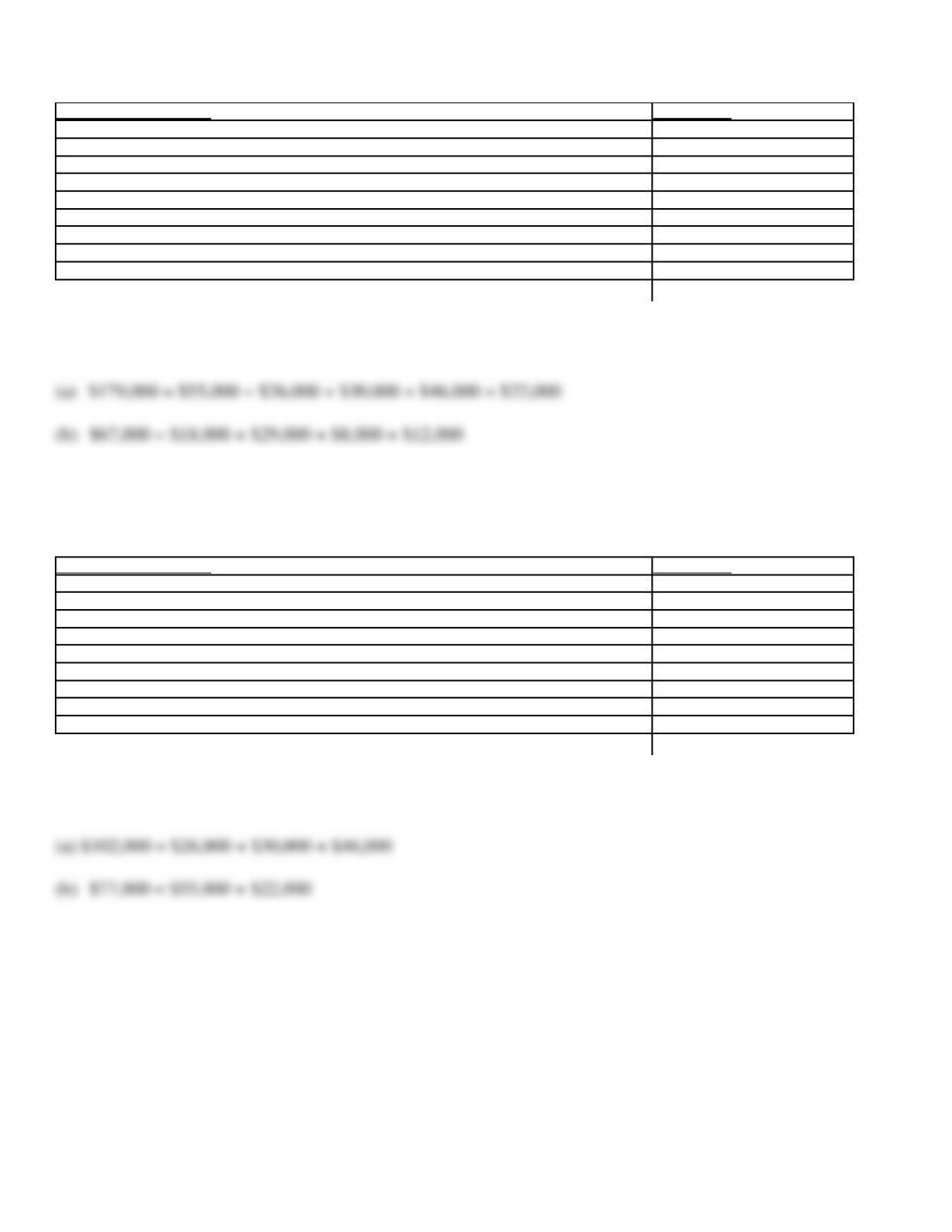

118. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Product testing

$55,000

Assessing vendor quality

26,000

Recalls

18,000

Rework

29,000

Scrap disposal

8,000

Product design

30,000

Training machine operators

46,000

Warranty work

12,000

Process audits

22,000

From the above schedule, calculate the (a) value-added and (b) non-value-added costs.

119. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Product testing

$55,000

Assessing vendor quality

26,000

Recalls

18,000

Rework

29,000

Scrap disposal

8,000

Product design

30,000

Training machine operators

46,000

Warranty work

12,000

Process audits

22,000

From the above schedule, calculate the (a) prevention and (b) appraisal costs.

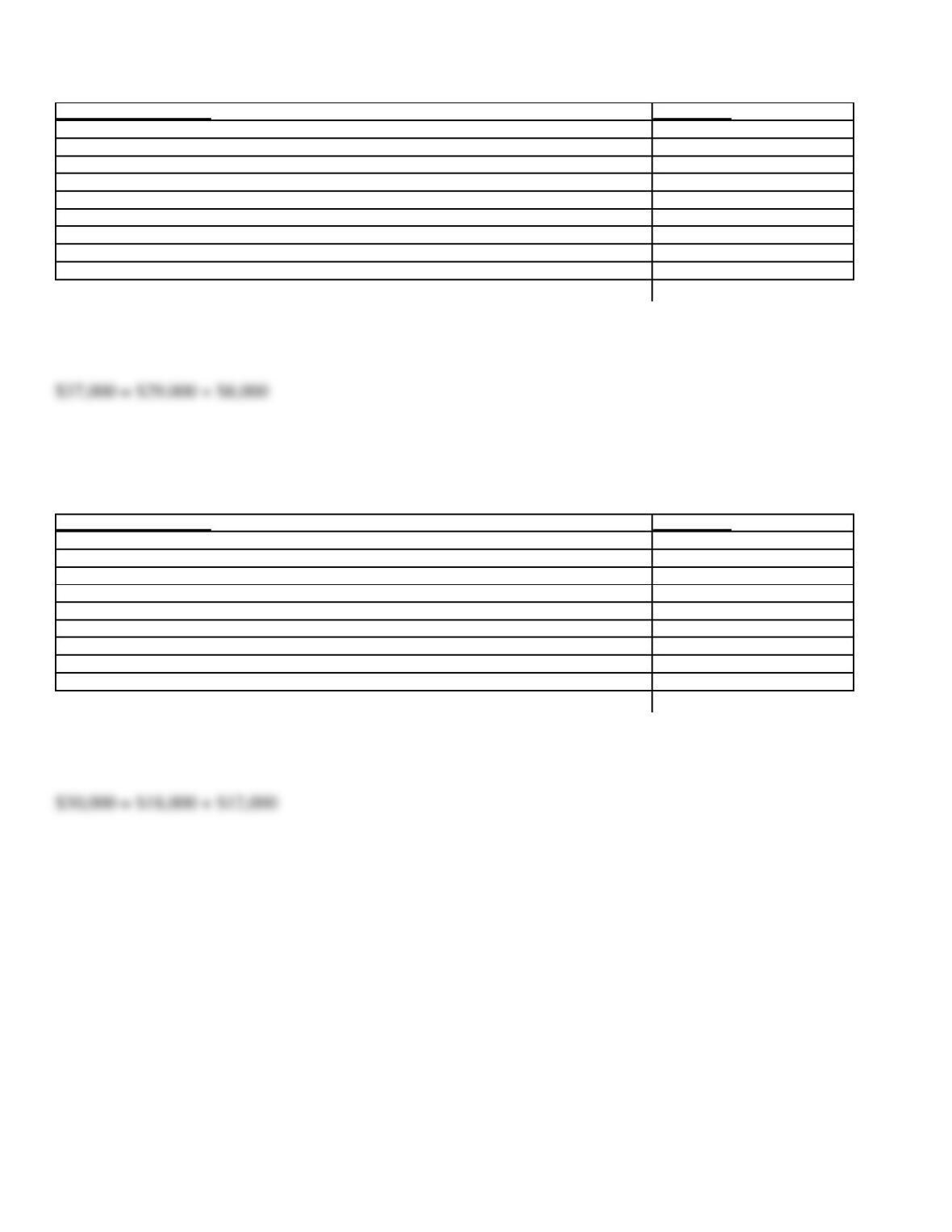

120. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Product testing

$55,000

Assessing vendor quality

26,000

Recalls

18,000

Rework

29,000

Scrap disposal

8,000

Product design

30,000

Training machine operators

46,000

Warranty work

12,000

Process audits

22,000

From the above schedule, calculate the internal failure costs.

121. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Product testing

$55,000

Assessing vendor quality

26,000

Recalls

18,000

Rework

29,000

Scrap disposal

8,000

Product design

30,000

Training machine operators

46,000

Warranty work

12,000

Process audits

22,000

From the above schedule, calculate the external failure costs.

122. Schedule of Activity Costs

Quality Control Activities

Activity Cost

Product testing

$55,000

Assessing vendor quality

26,000

Recalls

18,000

Rework

29,000

Scrap disposal

8,000

Product design

30,000

Training machine operators

46,000

Warranty work

12,000

Process audits

22,000

From the above schedule, compute the percentage of non-value-added activities.