150. An analysis of the general ledger accounts indicates that equipment, with an original cost of $134,000 and

accumulated depreciation of $105,000 on the date of sale, was sold for $20,000 during the year. Using this

information, indicate the items to be reported on the statement of cash flows using the indirect method.

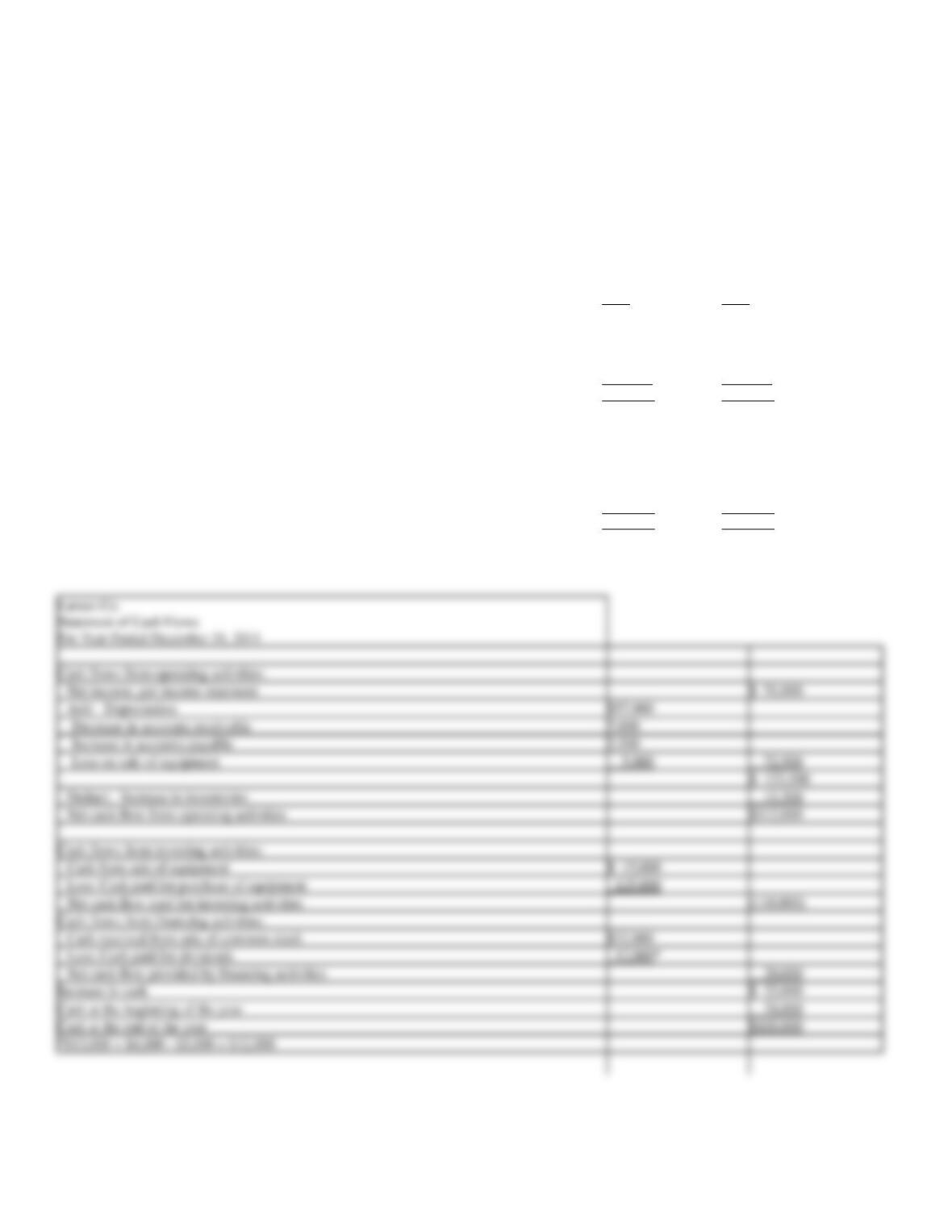

151. On the basis of the following data for Larson Co. for the year ending December 31, 2011 and the preceding

year ended December 31, 2010, prepare a statement of cash flows. Use the indirect method of reporting cash

flows from operating activities. In addition to the balance sheet data, assume that:

Equipment costing $125,000 was purchased for cash.

Equipment costing $85,000 with accumulated depreciation of $65,000 was sold for $15,000.

The stock was issued for cash.

The only entries in the retained earnings account were net income of $51,000 and cash dividends declared of

$13,000.

Year

Year

2011

2010

Cash

$100,000

$ 78,000

Accounts receivable (net)

78,000

85,000

Inventories

101,500

90,000

Equipment

410,000

370,000

Accumulated depreciation

(150,000)

(158,000)

$539,500

$465,000

Accounts payable (merchandise creditors)

$ 58,500

$ 55,000

Cash dividends payable

5,000

4,000

Common stock, $10 par

200,000

170,000

Paid-in capital in excess of par—

common stock

62,000

60,000

Retained earnings

214,000

176,000

$539,500

$465,000

Cash flows from operating activities:

Net income, per income statement

$ 51,000

Add: Depreciation

$57,000

Decrease in accounts receivable

7,000

Increase in accounts payable

3,500

Loss on sale of equipment

5,000

72,500

$ 123,500

Deduct: Increase in inventories

11,500

Net cash flow from operating activities

$112,000

Cash flows from investing activities:

Cash from sale of equipment

$ 15,000

Less: Cash paid for purchase of equipment

125,000

Net cash flow used for investing activities

(110,000)

Cash flows from financing activities:

Cash received from sale of common stock

$32,000

Less: Cash paid for dividends

12,000*

Net cash flow provided by financing activities

20,000

Increase in cash

$ 22,000

Cash at the beginning of the year

78,000

Cash at the end of the year

$100,000

*$13,000 + $4,000 – $5,000 = $12,000

152. The comparative balance sheet of Posner Company, for 2011 and the preceding year ended December 31,

2010, appears below in condensed form:

Year

Year

2011

2010

Cash

$ 53,000

$ 50,000

Accounts receivable (net)

37,000

48,000

Inventories

108,500

100,000

Investments

…..

70,000

Equipment

573,200

450,000

Accumulated depreciation-equipment

(142,000)

(176,000)

$629,700

$542,000

Accounts payable

$ 62,500

$ 43,800

Bonds payable, due 2011

…..

100,000

Common stock, $10 par

325,000

285,000

Paid-in capital in excess of par—

common stock

80,000

55,000

Retained earnings

162,200

58,200

$629,700

$542,000

Sales

$625,700

Cost of merchandise sold

340,000

Gross profit

$285,700

Operating expenses:

Depreciation expense

$26,000

Other operating expenses

68,000

94,000

Income from operations

$191,700

Other income:

Gain on sale of investment

$ 4,000

Other expense:

Interest expense

6,000

(2,000)

Income before income tax

$189,700

Income tax

60,700

Net income

$129,000

(a)

Fully depreciated equipment costing $60,000 was scrapped, no salvage, and equipment was purchased for $183,200.

(b)

Bonds payable for $100,000 were retired by payment at their face amount.

(c)

5,000 shares of common stock were issued at $13 for cash.

(d)

Cash dividends declared and paid, $25,000.

153. The comparative balance sheet of Barry Company, for 2011 and the preceding year ended December 31,

2010, appears below in condensed form:

Year

Year

2011

2010

Cash

$ 72,000

$ 42,500

Accounts receivable (net)

61,000

70,200

Inventories

121,000

105,000

Investments

…..

100,000

Equipment

515,000

425,000

Accumulated depreciation-equipment

(153,000)

(175,000)

$616,000

$567,700

Accounts payable

$ 59,750

$ 47,250

Bonds payable, due 2011

…..

75,000

Common stock, $20 par

375,000

325,000

Premium on common stock

50,000

25,000

Retained earnings

131,250

95,450

$616,000

$567,700

Additional data for the current year are as follows:

(a)

Net income, $75,800.

(b)

Depreciation reported on income statement, $38,000.

(c)

Fully depreciated equipment costing $60,000 was scrapped, no salvage, and equipment was purchased for $150,000.

(d)

Bonds payable for $75,000 were retired by payment at their face amount.

(e)

2,500 shares of common stock were issued at $30 for cash.

Cash dividends declared and paid, $40,000.

(g)

Investments of $100,000 were sold for $125,000.

154. The Dickinson Company reported net income of $155,000 for the current year. Depreciation recorded on

buildings and equipment amounted to $65,000 for the year. In addition, a building with an original cost of

$250,000 and accumulated depreciation of $190,000 on the date of the sale, was sold for $75,000. Balances of

the current asset and current liability accounts at the beginning and end of the year are as follows:

End of Year

Beginning of Year

Cash

$20,000

$15,000

Accounts receivable

19,000

32,000

Inventories

50,000

65,000

Accounts payable

12,000

18,000

Instructions

Prepare the cash flows from the operating activities section of the statement of cash flows using the indirect method.

Net income

$155,000

Adjustments to reconcile net income to net cash provided by operating activities:

Depreciation expense

65,000

Gain on sale of building

(15,000)

Decrease in accounts receivable

13,000

Decrease in inventories

15,000

Decrease in accounts payable

(6,000)

Net cash provided by operating activities

$227,000

155. The net income reported on an income statement for the current year was $58,000. Depreciation recorded

on fixed assets for the year was $24,000. In addition, equipment with an original cost of $130,000 and

accumulated depreciation of $115,000 on the date of the sale, was sold for $20,000. Balances of the current

asset and current liability accounts at the end and beginning of the year are listed below. Prepare the cash flows

from operating activities section of a statement of cash flows using the indirect method.

End

Beginning

Cash

$65,000

$ 70,000

Accounts receivable (net)

70,000

63,000

Inventories

85,000

102,000

Prepaid expenses

4,000

4,500

Accounts payable

(merchandise creditors)

50,000

58,000

Cash dividends payable

4,500

6,500

Salaries payable

6,000

7,500

Cash flows from operating activities:

Net income, per income statement

$58,000

Add: Depreciation

$24,000

Decrease in inventories

17,000

Decrease in prepaid expenses

500

41,500

$99,500

Deduct: Gain on sale of equipment

$ 5,000

Increase in accounts receivable (net)

7,000

Decrease in accounts payable

8,000

Decrease in salaries payable

1,500

21,500

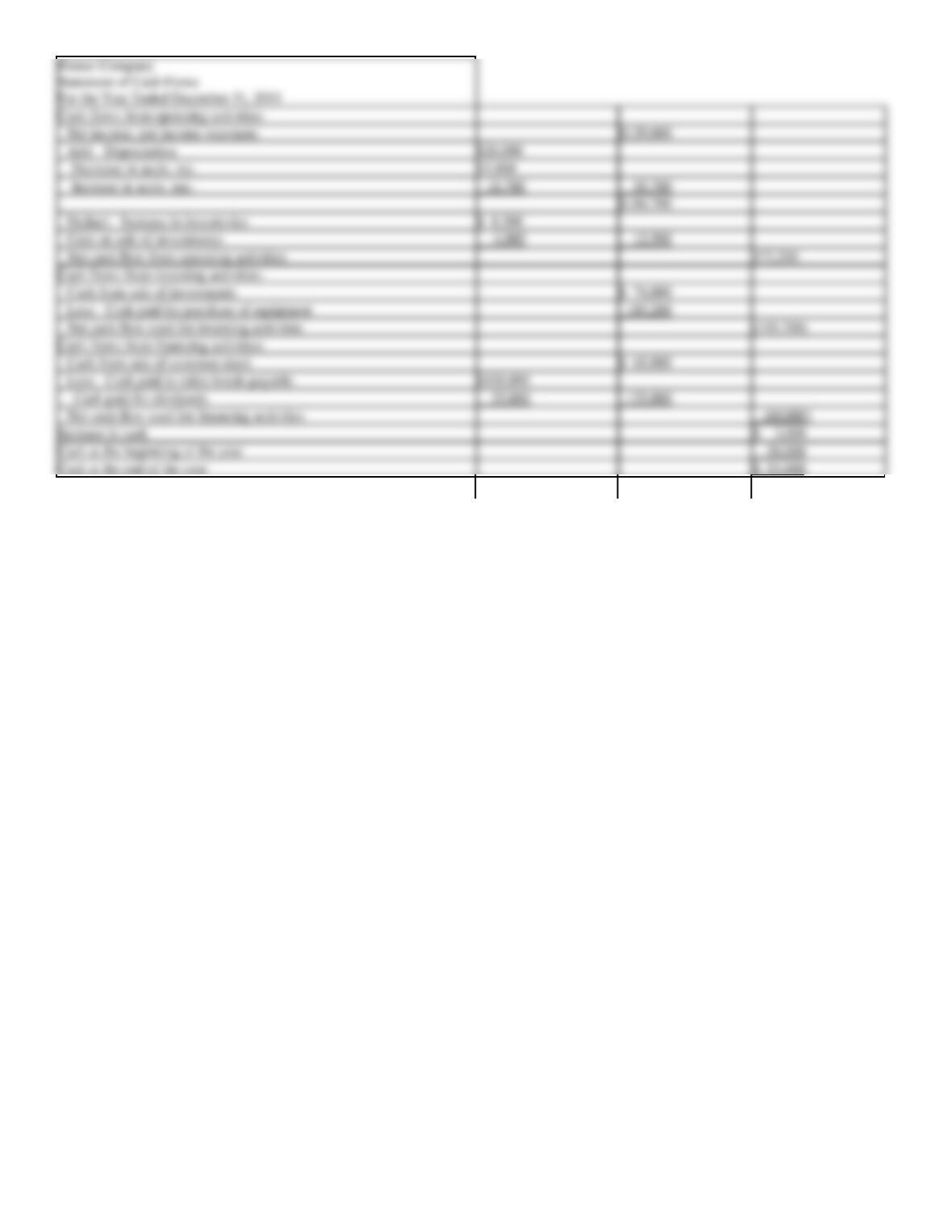

156. On the basis of the following data for Grant Co. for 2011 and the preceding year ended December 31,

2010, prepare a statement of cash flows. Use the indirect method of reporting cash flows from operating

activities. Assume that equipment costing $125,000 was purchased for cash and equipment costing $85,000

with accumulated depreciation of $65,000 was sold for $15,000; that the stock was issued for cash; and that the

only entries in the retained earnings account were net income of $56,000 and cash dividends declared of

$18,000.

Year

Year

2011

2010

Cash

$90,000

$ 78,000

Accounts receivable (net)

78,000

85,000

Inventories

106,500

90,000

Equipment

410,000

370,000

Accumulated depreciation

(150,000)

(158,000)

$534,500

$465,000

Accounts payable (merchandise creditors)

$ 53,500

$ 55,000

Cash dividends payable

5,000

4,000

Common stock, $10 par

200,000

170,000

Paid-in capital in excess of par—

common stock

62,000

60,000

Retained earnings

214,000

176,000

$534,500

$465,000

Cash flows from operating activities:

Add: Depreciation

$57,000

Decrease in accounts receivable

7,000

Loss on sale of equipment

5,000

69,000

$125,000

Deduct: Increase in inventories

16,500

Decrease in accounts payable

1,500

18,000

Net cash flow from operating activities

$107,000

Cash flows from investing activities:

Cash from sale of equipment

$ 15,000

Less: Cash paid for purchase of equipment

125,000

Net cash flow used for investing activities

(110,000)

Cash flows from financing activities:

Cash received from sale of common stock

$32,000

Less: Cash paid for dividends

17,000*

Net cash flow provided by financing activities

15,000

Increase in cash

$ 12,000

Cash at the beginning of the year

78,000

Cash at the end of the year

$90,000

*$18,000 + $4,000 – $5,000 = $17,000

157. Balances of the current asset and current liability accounts at the end and beginning of the year are as

follows:

End

Beginning

Cash

$ 62,000

$73,000

Accounts receivable (net)

75,000

60,000

Inventories

54,000

47,000

Accounts payable

(merchandise creditors)

43,000

37,000

Salaries payable

2,800

3,800

Sales (on account)

210,000

Cost of merchandise sold

70,000

Operating expenses other than depreciation

67,000

Use the direct method to prepare the cash flows from operating activities section of a statement of cash flows.

Cash flows from operating activities:

Cash received from customers

$195,000

Less: Cash payments for merchandise

$71,000

Cash payments for operating

expenses

68,000

139,000

Net cash flow from operating activities

$ 56,000

158. The comparative balance sheet of Colson Company, for 2011 and the preceding year ended December 31,

2010 appears below in condensed form:

Year

Year

2011

2010

Cash

$ 45,000

$ 53,500

Accounts receivable (net)

51,300

58,000

Inventories

147,200

135,000

Investments

0

60,000

Equipment

493,000

375,000

Accumulated depreciation-equipment

(113,700)

(128,000)

$622,800

$553,500

Accounts payable

$ 61,500

$ 42,600

Bonds payable, due 2014

0

100,000

Common stock, $10 par

250,000

200,000

Paid-in capital in excess of par—

common stock

75,000

50,000

Retained earnings

236,300

160,900

$622,800

$553,500

Sales

$623,000

Cost of merchandise sold

348,500

Gross profit

$274,500

Operating expenses:

Depreciation expense

$24,700

Other operating expenses

75,300

100,000

Income from operations

$174,500

Other income:

Gain on sale of investment

$ 5,000

Other expense:

Interest expense

12,000

(7,000)

Income before income tax

$167,500

Income tax

64,100

Net income

$103,400

(a)

Fully depreciated equipment costing $39,000 was scrapped, no salvage, and equipment was purchased for $157,000.

(b)

Bonds payable for $100,000 were retired by payment at their face amount.

(c)

5,000 shares of common stock were issued at $15 for cash.

(d)

Cash dividends declared were paid $28,000.

(e)

All sales are on account.

159. The cash flows from operating activities are reported by the direct method on the statement of cash

flows. Determine the following:

(a)

If sales for the current year were $475,000 and accounts receivable increased by $39,000 during the year, what was the amount of cash

received from customers?

(b)

If income tax for the current year was $39,000 and income tax payable decreased by $11,000 during the year, what was the amount of

cash payments for income tax?

160. Selected data for the current year ended December 31 are as follows:

Balance

Balance

December 31

January 1

Accrued expenses (operating expenses)

$29,500

$ 22,000

Accounts payable (merchandise creditors)

90,000

135,000

Inventories

42,500

68,000

Prepaid expenses

23,000

20,000

During the current year, the cost of merchandise sold was $620,000 and the operating expenses other than depreciation were $142,000. The direct

method is used for presenting the cash flows from operating activities on the statement of cash flows.

Determine the amount reported on the statement of cash flows for (a) cash payments for merchandise and (b) cash payments for operating expenses.

161. Based on the following, what is free cash flow?

Cash from Operations

$155,000

Cash from Investing

$(30,000)

Cash from Financing

$ 30,000

Cost of merchandise sold

$620,000

Add decrease in accounts payable

45,000

$665,000

Deduct decrease in inventories

25,500

Cash payments for merchandise

$639,500

Operating expenses other than depreciation

$142,000

Deduct increase in accrued expenses

7,500

$134,500

Add increase in prepaid expenses

3,000

Cash payments for operating expenses

$137,500

162. Balances of the current asset and current liability accounts at the end and beginning of the year are as

follows:

End

Beginning

Cash

$ 67,000

$73,000

Accounts receivable (net)

73,000

60,000

Inventories

54,000

47,000

Accounts payable

(merchandise creditors)

43,000

37,000

Salaries payable

2,800

3,800

Sales (on account)

210,000

Cost of merchandise sold

70,000

Operating expenses other than depreciation

67,000

Use the direct method to prepare the cash flows from operating activities section of a statement of cash flows.

Cash flows from operating activities:

Cash received from customers

$197,000

Less: Cash payments for merchandise

$71,000

Cash payments for operating

expenses

68,000

139,000

Net cash flow from operating activities

$ 58,000

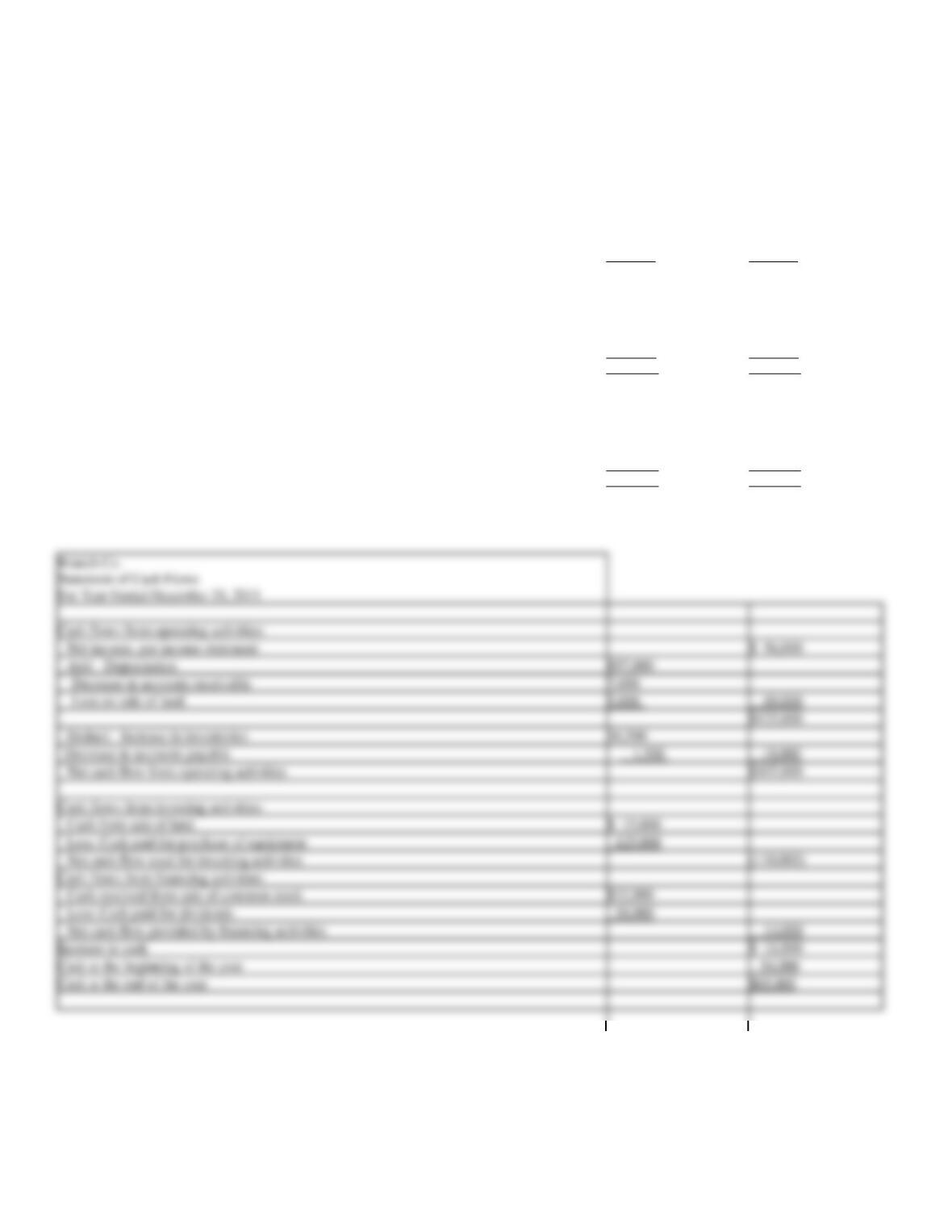

163. On the basis of the following data for Branch Co. for the year ended December 31, 2011 and the preceding

year, prepare a statement of cash flows using the indirect method of reporting cash flows from operating

activities.

Assume that equipment costing $125,000 was purchased for cash and the land was sold for $15,000. The stock

was issued for cash and the only entries in the retained earnings account were net income of $56,000 and cash

dividends declared and paid of $18,000.

Year

Year

2011

2010

Cash

$65,000

$ 54,000

Accounts receivable (net)

78,000

85,000

Inventories

106,500

90,000

Land

—

20,000

Equipment

495,000

370,000

Accumulated depreciation

(215,000)

(158,000)

$529,500

$461,000

Accounts payable (merchandise creditors)

$ 53,500

$ 55,000

Common stock, $10 par

200,000

170,000

Paid-in capital in excess of par—

common stock

62,000

60,000

Retained earnings

214,000

176,000

$529,500

$461,000

Cash flows from operating activities:

Add: Depreciation

$57,000

Decrease in accounts receivable

7,000

Loss on sale of land

5,000

69,000

$125,000

Deduct: Increase in inventories

16,500

Decrease in accounts payable

1,500

18,000

Net cash flow from operating activities

$107,000

Cash flows from investing activities:

Cash from sale of land

$ 15,000

Less: Cash paid for purchase of equipment

125,000

Net cash flow used for investing activities

(110,000)

Cash flows from financing activities:

Cash received from sale of common stock

$32,000

Less: Cash paid for dividends

18,000

Net cash flow provided by financing activities

14,000

Increase in cash

$ 11,000

Cash at the beginning of the year

54,000

Cash at the end of the year

$65,000

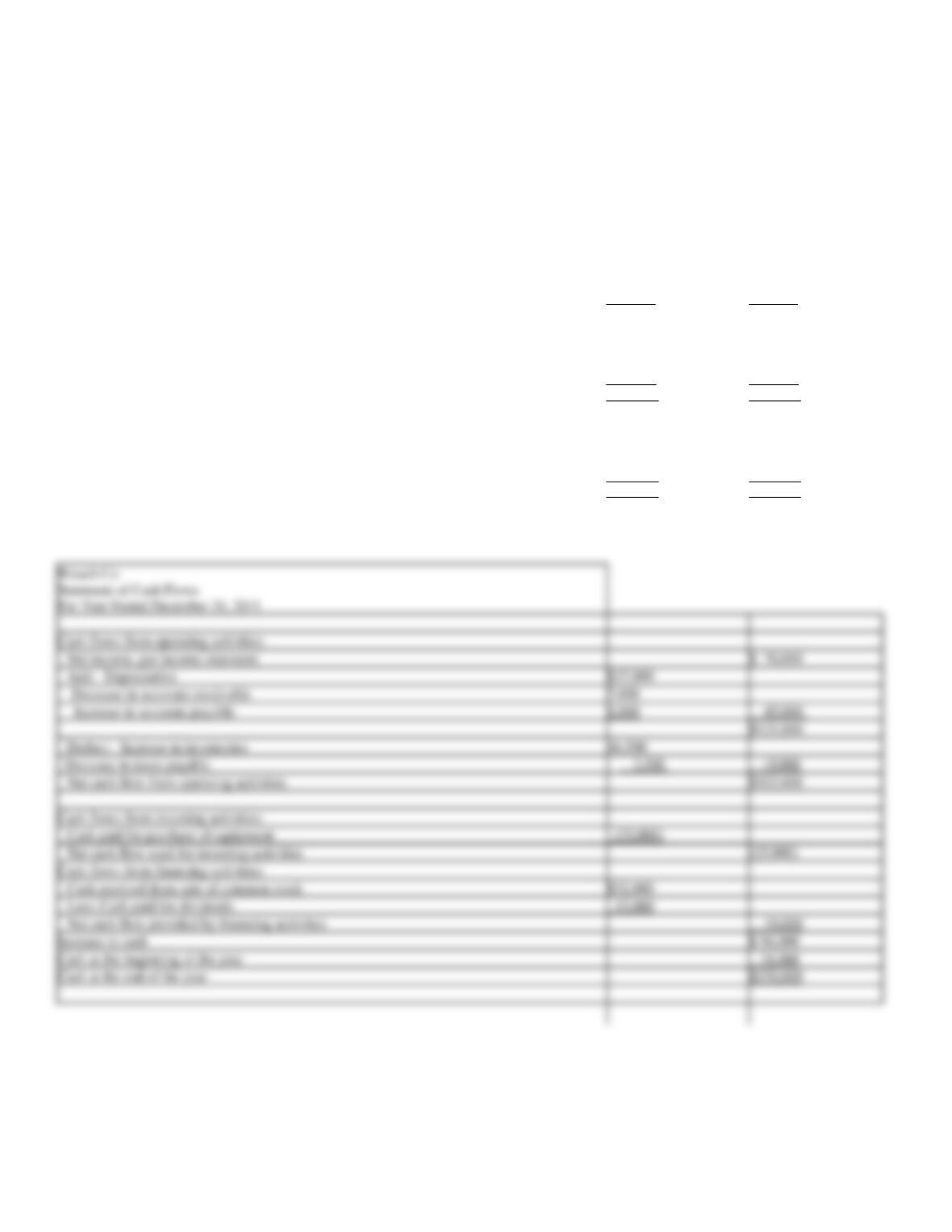

164. On the basis of the following data for Breach Co. for the year ended December 31, 2011 and the preceding

year, prepare a statement of cash flows using the indirect method of reporting cash flows from operating

activities.

Assume that equipment costing $25,000 was purchased for cash and no long term assets were sold during the

period.

Stock was issued for cash – 3,200 shares at par.

Net income for 2010 was $76,000.

Cash dividends declared and paid were $13,000.

Year

Year

2011

2010

Cash

$170,000

$ 74,000

Accounts receivable (net)

78,000

85,000

Inventories

106,500

90,000

Equipment

395,000

370,000

Accumulated depreciation

(195,000)

(158,000)

$554,500

$461,000

Accounts payable (merchandise creditors)

$ 51,000

$ 50,000

Taxes payable

2,500

5,000

Common stock, $10 par

262,000

230,000

Retained earnings

239,000

176,000

$554,500

$461,000

Cash flows from operating activities:

Net income, per income statement

$ 76,000

Add: Depreciation

$37,000

Decrease in accounts receivable

7,000

Increase in accounts payable

1,000

45,000

$121,000

Deduct: Increase in inventories

16,500

Decrease in taxes payable

2,500

19,000

Net cash flow from operating activities

$102,000

Cash flows from investing activities:

Cash paid for purchase of equipment

(25,000)

Net cash flow used for investing activities

(25,000)

Cash flows from financing activities:

Cash received from sale of common stock

$32,000

Less: Cash paid for dividends

13,000

Net cash flow provided by financing activities

19,000

Increase in cash

$ 96,000

Cash at the beginning of the year

74,000

Cash at the end of the year

$170,000

165. Complete each of the columns on the table below, indicating in which section each item would be reported

on the statement of cash flow (Operating, Investing, or Financing), the amount that would be reported, and

whether the item would create an increase or decrease in cash. For item that affect more than one section of the

statement, indicate all affected. Assume the indirect method of reporting cash flows operating activities.

The first item has been completed as an example.

Item

Statement Section

Amount

to Report

+/– Effect

on Cash

Depreciation of $20,000 for the period

Operating

$20,000

Increase

Issuance of common stock for $30,000

Increase in Accounts Payable of $7,000

Retirement of $100,000 Bonds Payable at 97.

Purchase of long term investments for $76,500

Dividends declared and paid of $8,300

Increase in Prepaid Rent of $4,500

Decrease in Inventory of $5,300

Purchase of equipment for $17,600 cash.

Sale of land originally costing $60,000 for $66,000

Decrease in Taxes Payable for $2,100

Issuance of common stock for $30,000

Financing

30,000

Increase

Increase in Accounts Payable of $7,000

Operating

7,000

Increase

Retirement of $100,000 Bonds Payable at 97.

Operating

3,000

Increase

Purchase of long term investments for $76,500

Investing

76,500

Decrease

Dividends declared and paid of $8,300

Financing

8,300

Decrease

Increase in Prepaid Rent of $4,500

Operating

4,500

Decrease

Decrease in Inventory of $5,300

Operating

5,300

Increase

Purchase of equipment for $17,600 cash.

Investing

17,600

Decrease

Decrease in Taxes Payable for $2,100

Operating

2,100

Decrease