Chapter 24—Differential Analysis and Product Pricing Key

1. Differential revenue is the amount of income that would result from the best available alternative proposed

use of cash.

2. Differential revenue is the amount of increase or decrease in revenue expected from a particular course of

action as compared with an alternative.

3. If the total unit cost of manufacturing Product Y is currently $36 and the total unit cost after modifying the

style is estimated to be $48, the differential cost for this situation is $48.

4. If the total unit cost of manufacturing Product Y is currently $36 and the total unit cost after modifying the

style is estimated to be $48, the differential cost for this situation is $12.

5. Hill Co. can further process Product O to produce Product P. Product O is currently selling for $60 per pound

and costs $42 per pound to produce. Product P would sell for $82 per pound and would require an additional

cost of $13 per pound to produce.

The differential revenue of producing Product P is $82 per pound.

6. Hill Co. can further process Product O to produce Product P. Product O is currently selling for $60 per pound

and costs $42 per pound to produce. Product P would sell for $82 per pound and would require an additional

cost of $13 per pound to produce.

The differential revenue of producing Product P is $22 per pound.

7. Hill Co. can further process Product O to produce Product P. Product O is currently selling for $60 per pound

and costs $42 per pound to produce. Product P would sell for $82 per pound and would require an additional

cost of $13 per pound to produce.

The differential cost of producing Product P is $13 per pound.

8. Hill Co. can further process Product O to produce Product P. Product O is currently selling for $60 per pound

and costs $42 per pound to produce. Product P would sell for $82 per pound and would require an additional

cost of $13 per pound to produce.

The differential cost of producing Product P is $55 per pound.

9. Opportunity cost is the amount of increase or decrease in cost that would result from the best available

alternative to the proposed use of cash or its equivalent.

10. Differential analysis can aid management in making decisions on a variety of alternatives, including

whether to discontinue an unprofitable segment and whether to replace usable plant assets.

11. A cost that will not be affected by later decisions is termed a sunk cost.

12. A cost that will not be affected by later decisions is termed an opportunity cost.

13. The amount of income that would result from an alternative use of cash is called opportunity cost.

14. Since the costs of producing an intermediate product do not change regardless of whether the intermediate

product is sold or processed further, these costs are not considered in deciding whether to further process a

product.

15. The costs of initially producing an intermediate product should be considered in deciding whether to further

process a product, even though the costs will not change, regardless of the decision.

16. In deciding whether to accept business at a special price, the short-run price should be set high enough to

cover all variable costs and expenses.

17. Eliminating a product or segment may have the long-term effect of reducing fixed costs.

18. Make or buy options often arise when a manufacturer has excess productive capacity in the form of unused

equipment, space, and labor.

19. In addition to the differential costs in an equipment replacement decision, the remaining useful life of the

old equipment and the estimated life of the new equipment are important considerations.

20. Manufacturers must conform to the Robinson-Patman Act which prohibits price discrimination within the

United States unless differences in prices can be justified by different costs of serving different customers.

21. When a company is showing a net loss, it is always best to discontinue the segment in order not to continue

with losses.

22. Discontinuing a segment or product may not be the best choice when the segment is contributing to fixed

expenses.

23. Make or buy decisions should be made only with related parties.

24. Depending on the capacity of the plant, a company may best be served by further processing some of the

product and leaving the rest as is, with no further processing.

25. A practical approach which is frequently used by managers when setting normal long-run prices is the cost-

plus approach.

26. The total cost concept includes all manufacturing costs plus selling and administrative expenses in the cost

amount to which the markup is added to determine product price.

27. The product cost concept includes all manufacturing costs plus selling and administrative expenses in the

cost amount to which the markup is added to determine product price.

28. The product cost concept includes all manufacturing costs in the cost amount to which the markup is added

to determine product price.

TRUE

29. In using the total cost concept of applying the cost-plus approach to product pricing, selling expenses,

administrative expenses, and profit are covered in the markup.

30. In using the product cost concept of applying the cost-plus approach to product pricing, selling expenses,

administrative expenses, and profit are covered in the markup.

31. In using the variable cost concept of applying the cost-plus approach to product pricing, fixed

manufacturing costs and fixed selling and administrative expenses must be covered by the markup.

32. In using the variable cost concept of applying the cost-plus approach to product pricing, fixed

manufacturing costs and both fixed and variable selling and administrative expenses must be covered by the

markup.

33. When estimated costs are used in applying the cost-plus approach to product pricing, the estimates should

be based upon normal levels of performance.

34. When estimated costs are used in applying the cost-plus approach to product pricing, the estimates should

be based upon ideal levels of performance.

35. A bottleneck begins when demand for the company’s product exceeds the ability to produce the product.

36. A bottleneck happens when a key piece of manufacturing machinery can produce 1000 units per hour and

demand for the product supports a production rate of 1200 units per hour.

37. When a bottleneck occurs between two products, the company must determine the contribution margin for

each product and manufacture the product that has the highest contribution margin per bottleneck hour.

38. The theory of constraints is a manufacturing strategy that focuses on reducing the influence of bottlenecks

on a process.

39. The lowest contribution margin per scarce resource is the most profitable.

40. Activity-based costing provides more accurate and useful cost data than traditional systems.

41. Activity-based costing is determined by charging products for only the services (activities) they used during

production.

42. Cost plus methods determine the normal selling price by estimating a cost amount per unit and adding a

markup.

43. Under the total cost concept, manufacturing cost plus desired profit is included in the total cost per unit.

44. Under the variable cost concept, only variable costs are included in the cost amount per unit to which the

markup is added.

45. The desired selling price for a product will be the same under both variable and total cost.

46. The amount of increase or decrease in revenue that is expected from a particular course of action as

compared with an alternative is termed:

47. The amount of increase or decrease in cost that is expected from a particular course of action as compared

with an alternative is termed:

48. A cost that will not be affected by later decisions is termed a(n):

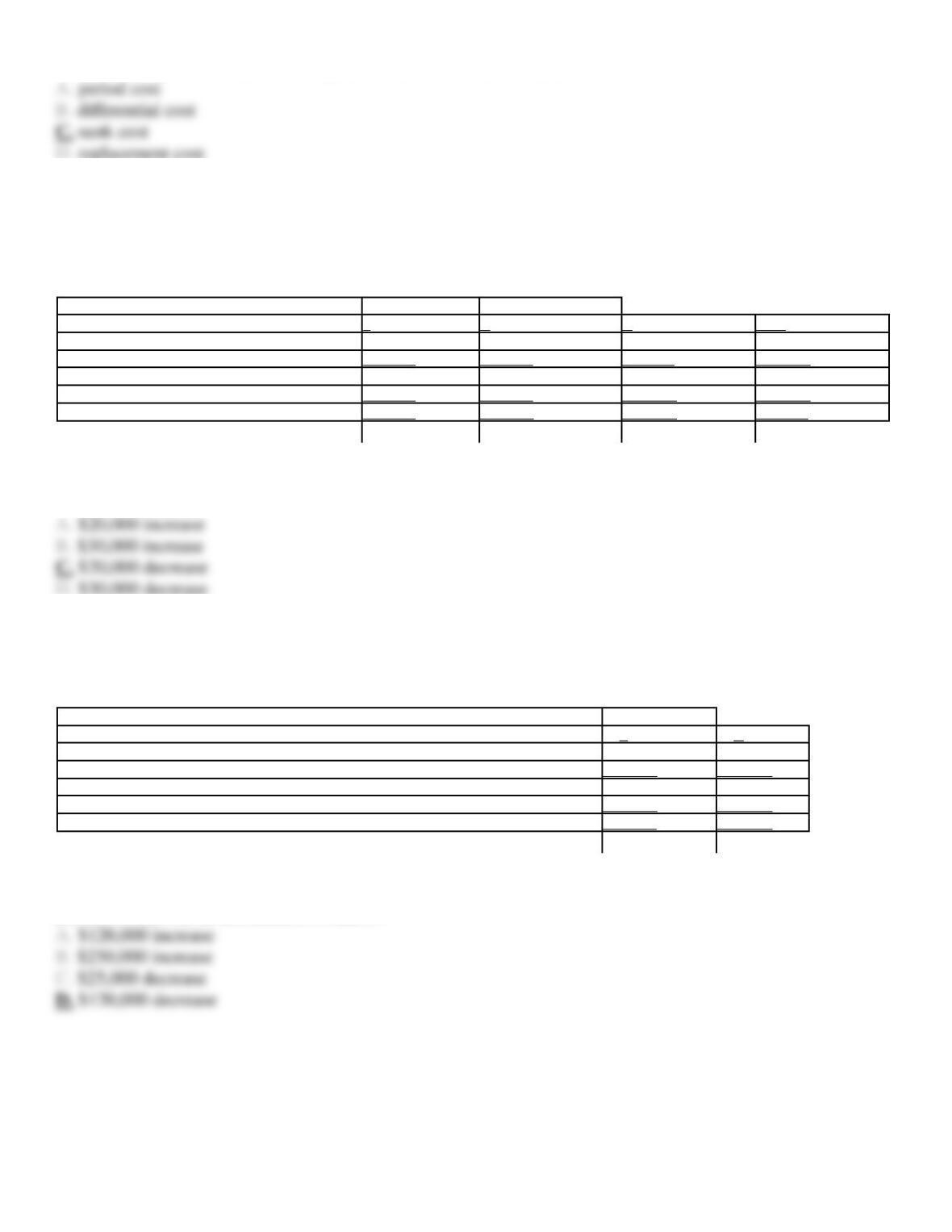

49. The condensed income statement for a business for the past year is presented as follows:

Product

F

G

H

Total

Sales

$300,000

$210,000

$340,000

$850,000

Less variable costs

180,000

190,000

220,000

590,000

Contribution margin

$120,000

$ 20,000

$120,000

$260,000

Less fixed costs

50,000

50,000

40,000

140,000

Income (loss) from oper.

$ 70,000

$ (30,000)

$ 80,000

$120,000

Management is considering the discontinuance of the manufacture and sale of Product G at the beginning of the current year. The discontinuance

would have no effect on the total fixed costs and expenses or on the sales of Products F and H. What is the amount of change in net income for the

current year that will result from the discontinuance of Product G?

50. The condensed income statement for a business for the past year is as follows:

Product

T

U

Sales

$660,000

$320,000

Less variable costs

540,000

220,000

Contribution margin

$ 120,000

$100,000

Less fixed costs

145,000

40,000

Income (loss) from operations

$ (25,000)

$ 60,000

Management is considering the discontinuance of the manufacture and sale of Product T at the beginning of the current year. The discontinuance

would have no effect on the total fixed costs and expenses or on the sales of Product U. What is the amount of change in net income for the current

year that will result from the discontinuance of Product T?

51. A business is operating at 90% of capacity and is currently purchasing a part used in its manufacturing

operations for $15 per unit. The unit cost for the business to make the part is $20, including fixed costs, and

$12, not including fixed costs. If 30,000 units of the part are normally purchased during the year but could be

manufactured using unused capacity, what would be the amount of differential cost increase or decrease from

making the part rather than purchasing it?

52. A business is operating at 70% of capacity and is currently purchasing a part used in its manufacturing

operations for $24 per unit. The unit cost for the business to make the part is $36, including fixed costs, and

$28, not including fixed costs. If 15,000 units of the part are normally purchased during the year but could be

manufactured using unused capacity, what would be the amount of differential cost increase or decrease from

making the part rather than purchasing it?

53. The amount of income that would result from an alternative use of cash is called:

54. Pheasant Co. can further process Product B to produce Product C. Product B is currently selling for $30 per

pound and costs $28 per pound to produce. Product C would sell for $60 per pound and would require an

additional cost of $24 per pound to produce. What is the differential cost of producing Product C?

55. Partridge Co. can further process Product J to produce Product D. Product J is currently selling for $21 per

pound and costs $15.75 per pound to produce. Product D would sell for $38 per pound and would require an

additional cost of $9.25 per pound to produce.

What is the differential cost of producing Product D?

56. Partridge Co. can further process Product J to produce Product D. Product J is currently selling for $21 per

pound and costs $15.75 per pound to produce. Product D would sell for $38 per pound and would require an

additional cost of $9.25 per pound to produce.

What is the differential revenue of producing Product D?

57. Quail Co. can further process Product B to produce Product C. Product B is currently selling for $60 per

pound and costs $42 per pound to produce. Product C would sell for $92 per pound and would require an

additional cost of $13 per pound to produce. What is the differential revenue of producing and selling Product

C?

58. Raven Company is considering replacing equipment which originally cost $500,000 and which has

$420,000 accumulated depreciation to date. A new machine will cost $790,000. What is the sunk cost in this

situation?

59. Raptor Company is considering replacing equipment which originally cost $500,000 and which has

$420,000 accumulated depreciation to date. A new machine will cost $790,000 and the old equipment can be

sold for $8,000. What is the sunk cost in this situation?

60. A business is considering a cash outlay of $250,000 for the purchase of land, which it could lease for

$35,000 per year. If alternative investments are available which yield an 18% return, the opportunity cost of the

purchase of the land is:

61. A business is considering a cash outlay of $300,000 for the purchase of land, which it could lease for

$36,000 per year. If alternative investments are available which yield an 18% return, the opportunity cost of the

purchase of the land is:

62. A business is considering a cash outlay of $400,000 for the purchase of land, which it could lease for

$40,000 per year. If alternative investments are available which yield a 21% return, the opportunity cost of the

purchase of the land is:

63. A business received an offer from an exporter for 20,000 units of product at $15 per unit. The acceptance of

the offer will not affect normal production or domestic sales prices. The following data are available:

Domestic unit sales price

$21

Unit manufacturing costs:

Variable

12

Fixed

5

What is the differential revenue from the acceptance of the offer?

64. A business received an offer from an exporter for 10,000 units of product at $17.50 per unit. The acceptance

of the offer will not affect normal production or domestic sales prices. The following data is available:

Domestic unit sales price

$20

Unit manufacturing costs:

Variable

11

Fixed

1

What is the differential revenue from the acceptance of the offer?

65. A business received an offer from an exporter for 10,000 units of product at $17.50 per unit. The acceptance

of the offer will not affect normal production or domestic sales prices. The following data is available:

Domestic unit sales price

$20

Unit manufacturing costs:

Variable

11

Fixed

1

What is the differential cost from the acceptance of the offer?

66. A business received an offer from an exporter for 10,000 units of product at $17.50 per unit. The acceptance

of the offer will not affect normal production or domestic sales prices. The following data is available:

Domestic unit sales price

$20

Unit manufacturing costs:

Variable

11

Fixed

1

What is the amount of gain or loss from acceptance of the offer?

67. A business received an offer from an exporter for 30,000 units of product at $16 per unit. The acceptance of

the offer will not affect normal production or domestic sales prices. The following data are available:

Domestic unit sales price

$22

Unit manufacturing costs:

Variable

11

Fixed

6

What is the differential cost from the acceptance of the offer?

68. A business received an offer from an exporter for 30,000 units of product at $16 per unit. The acceptance of

the offer will not affect normal production or domestic sales prices. The following data are available:

Domestic unit sales price

$22

Unit manufacturing costs:

Variable

11

Fixed

6

What is the amount of the gain or loss from acceptance of the offer?

69. Relevant revenues and costs refer to:

70. Assume that Penguin Co. is considering disposing of equipment that cost $50,000 and has $40,000 of

accumulated depreciation to date. Penguin Co. can sell the equipment through a broker for $25,000 less 5%

commission. Alternatively, Teal Co. has offered to lease the equipment for five years for a total of $48,750.

Penguin will incur repair, insurance, and property tax expenses estimated at $10,000. At lease-end, the

equipment is expected to have no residual value. The net differential income from the lease alternative is:

71. Sparrow Co. is currently operating at 80% of capacity and is currently purchasing a part used in its

manufacturing operations for $8.00 a unit. The unit cost for Sparrow Co. to make the part is $9.00, which

includes $.60 of fixed costs. If 4,000 units of the part are normally purchased each year but could be

manufactured using unused capacity, what would be the amount of differential cost increase or decrease for

making the part rather than purchasing it?

72. Heston and Burton, CPAs, currently work a five-day week. They estimate that net income for the firm

would increase by $75,000 annually if they worked an additional day each month. The cost associated with the

decision to continue the practice of a five-day work week is an example of:

73. Starling Co. is considering disposing of a machine with a book value of $12,500 and estimated remaining

life of five years. The old machine can be sold for $1,500. A new high-speed machine can be purchased at a

cost of $25,000. It will have a useful life of five years and no residual value. It is estimated that the annual

variable manufacturing costs will be reduced from $26,000 to $23,500 if the new machine is purchased. The

total net differential increase or decrease in cost for the new equipment for the entire five years is:

74. Nighthawk Inc. is considering disposing of a machine with a book value of $22,500 and an estimated

remaining life of three years. The old machine can be sold for $6,250. A new machine with a purchase price of

$68,750 is being considered as a replacement. It will have a useful life of three years and no residual value. It is

estimated that the annual variable manufacturing costs will be reduced from $43,750 to $20,000 if the new

machine is purchased. The net differential increase or decrease in cost for the entire three years for the new

equipment is:

75. Falcon Co. produces a single product. Its normal selling price is $30.00 per unit. The variable costs are

$19.00 per unit. Fixed costs are $25,000 for a normal production run of 5,000 units per month. Falcon received

a request for a special order that would not interfere with normal sales. The order was for 1,500 units and a

special price of $20.00 per unit. Falcon Co. has the capacity to handle the special order and, for this order, a

variable selling cost of $1.00 per unit would be eliminated.

If the order is accepted, what would be the impact on net income?

76. Falcon Co. produces a single product. Its normal selling price is $30.00 per unit. The variable costs are

$19.00 per unit. Fixed costs are $25,000 for a normal production run of 5,000 units per month. Falcon received

a request for a special order that would not interfere with normal sales. The order was for 1,500 units and a

special price of $20.00 per unit. Falcon Co. has the capacity to handle the special order and, for this order, a

variable selling cost of $1.00 per unit would be eliminated.

Should the special order be accepted?

77. Mighty Safe Fire Alarm is currently buying 50,000 motherboard from MotherBoard, Inc. at a price of $65

per board. Mighty Safe is considering making its own boards. The costs to make the board are as follows:

Direct Materials $32 per unit, Direct labor $10 per unit, Variable Factory Overhead $16.00, Fixed Costs for the

plant would increase by $75,000. Which option should be selected and why?

78. Super Security Company manufacturers home alarms. Currently it is manufacturing one of its components

at a variable cost of $45 and fixed costs of $15 per unit. An outside provider of this component has offered to

sell Safe Security the component for $50. Determine the best plan and calculate the savings.

79. Discontinuing a product or segment is a huge decision that must be carefully analyzed. Which of the

following would be a valid reason not to discontinue an operation?

80. Which of the following would be considered a sunk cost?

81. All of the following should be considered in a make or buy decision except

82. Which of the following reasons would cause a company to reject an offer to accept business at a special

price?

83. A practical approach which is frequently used by managers when setting normal long-run prices is the:

84. Which of the following is NOT a cost concept commonly used in applying the cost-plus approach to product

pricing?

85. When using the total cost concept of applying the cost-plus approach to product pricing, what is included in

the markup?

86. When using the product cost concept of applying the cost-plus approach to product pricing, what is included

in the markup?

87. When using the variable cost concept of applying the cost-plus approach to product pricing, what is

included in the markup?

88. What cost concept used in applying the cost-plus approach to product pricing covers selling expenses,

administrative expenses, and desired profit in the “markup”?

89. What cost concept used in applying the cost-plus approach to product pricing includes only desired profit in

the “markup”?

90. What cost concept used in applying the cost-plus approach to product pricing includes only total

manufacturing costs in the “cost” amount to which the markup is added?

91. Contractors who sell to government agencies would be most likely to use which of the following cost

concepts in pricing their products?

92. The target cost approach assumes that:

93. Magpie Corporation uses the total cost concept of product pricing. Below is cost information for the

production and sale of 60,000 units of its sole product. Magpie desires a profit equal to a 25% rate of return on

invested assets of $700,000.

Fixed factory overhead cost

$38,700

Fixed selling and administrative costs

7,500

Variable direct materials cost per unit

4.60

Variable direct labor cost per unit

1.88

Variable factory overhead cost per unit

1.13

Variable selling and administrative cost per unit

4.50

The dollar amount of desired profit from the production and sale of the company’s product is:

94. Magpie Corporation uses the total cost concept of product pricing. Below is cost information for the

production and sale of 60,000 units of its sole product. Magpie desires a profit equal to a 25% rate of return on

invested assets of $700,000.

Fixed factory overhead cost

$38,700

Fixed selling and administrative costs

7,500

Variable direct materials cost per unit

4.60

Variable direct labor cost per unit

1.88

Variable factory overhead cost per unit

1.13

Variable selling and administrative cost per unit

4.50

The cost per unit for the production and sale of the company’s product is:

95. Magpie Corporation uses the total cost concept of product pricing. Below is cost information for the

production and sale of 60,000 units of its sole product. Magpie desires a profit equal to a 25% rate of return on

invested assets of $700,000.

Fixed factory overhead cost

$38,700

Fixed selling and administrative costs

7,500

Variable direct materials cost per unit

4.60

Variable direct labor cost per unit

1.88

Variable factory overhead cost per unit

1.13

Variable selling and administrative cost per unit

4.50

The markup percentage on total cost for the company’s product is:

96. Magpie Corporation uses the total cost concept of product pricing. Below is cost information for the

production and sale of 60,000 units of its sole product. Magpie desires a profit equal to a 25% rate of return on

invested assets of $700,000.

Fixed factory overhead cost

$38,700

Fixed selling and administrative costs

7,500

Variable direct materials cost per unit

4.60

Variable direct labor cost per unit

1.88

Variable factory overhead cost per unit

1.13

Variable selling and administrative cost per unit

4.50

The unit selling price for the company’s product is:

97. Mallard Corporation uses the product cost concept of product pricing. Below is cost information for the

production and sale of 45,000 units of its sole product. Mallard desires a profit equal to a 12% rate of return on

invested assets of $800,000.

Fixed factory overhead cost

$82,000

Fixed selling and administrative costs

45,000

Variable direct materials cost per unit

5.50

Variable direct labor cost per unit

7.65

Variable factory overhead cost per unit

2.25

Variable selling and administrative cost per unit

.90

The dollar amount of desired profit from the production and sale of the company’s product is:

98. Mallard Corporation uses the product cost concept of product pricing. Below is cost information for the

production and sale of 45,000 units of its sole product. Mallard desires a profit equal to a 12% rate of return on

invested assets of $800,000.

Fixed factory overhead cost

$82,000

Fixed selling and administrative costs

45,000

Variable direct materials cost per unit

5.50

Variable direct labor cost per unit

7.65

Variable factory overhead cost per unit

2.25

Variable selling and administrative cost per unit

.90

The cost per unit for the production of the company’s product is: