96. Which of the following increases the likelihood that a group of sellers can increase profits as the result

of collusion?

a.

the presence of a large number of firms in the industry

b.

intense quality competition among firms

c.

low barriers to entry into the industry

d.

a stable demand for the product

97. Which of the following is an obstacle that would reduce the likelihood of effective collusion among

oligopolists?

a.

a highly inelastic market demand for the product

b.

a small number of firms in the market

c.

production of a homogeneous product

d.

highly unstable demand for the product

98. Which of the following will be an obstacle to oligopolistic collusion in a market?

a.

government regulations restricting entry

b.

a relatively small number of oligopolistic firms

c.

unstable demand conditions

d.

uniform products

99. When members of an oligopolistic industry agree to collude, raising their product price substantially

above average cost, the passage of time (months and years)

a.

is usually needed for the members to solidify their cooperation.

b.

usually results in finer control of prices and markets by the group and larger profit

margins.

c.

is likely to erode the agreement, as ways to cheat are developed by some participants and

new entry is encouraged by the high price.

d.

seldom has any impact on the agreement, as long as the participants maintain high profit

levels as a result of the agreement.

100. Which one of the following factors reduces the likelihood that a cartel agreement will lead to higher

producer profit?

a.

significant barriers to entry into the cartelized market

b.

the development of substitutes for the good produced by the cartel

c.

government restrictions that limit competition from new rivals

d.

a small number of sellers involved in the cartel agreement

101. If entry-restricting legal barriers effectively organized the funeral home industry of a large city into a

monopoly cartel, economic theory indicates that, compared to the previously competitive situation,

a.

the price of funeral services would decline, and output would increase.

b.

both the price and output of funeral services would decline.

c.

the price of funeral services would increase, and output would decline.

d.

both the price and output of funeral services would increase.

102. In an oligopolistic market, if rival sellers act independently, each will have a strong incentive to

a.

reduce price in order to increase sales and gain a larger share of the total market.

b.

increase price in order to get a larger share of the market and make larger profits.

c.

restrict output and raise price in order to achieve higher profits.

d.

maintain agreements to lower price and decrease product quality in order to earn higher

profits.

103. “Market power” is an expression used to indicate that a firm has

a.

no rivals.

b.

the power to sell a given output at whatever price it chooses.

c.

some freedom from the rigors of intense competition.

d.

a monopoly over the product it produces.

104. “Market power” is an expression used to indicate that a firm has

a.

the power to sell a given output at whatever price it chooses.

b.

no freedom from the rigors of intense competition.

c.

a monopoly over the product it produces.

d.

enough market share to be somewhat insulated from competition.

105. The prisoners’ dilemma is used to illustrate the basic idea that

a.

oligopolistic firms would be better off if they collude, but each has an incentive to cheat

on the collusive agreement.

b.

oligopolistic firms are always worse off when they collude.

c.

oligopolistic firms never have an incentive to cheat on collusive agreements, unlike

prisoners.

d.

students who cheat on economics exams end up in jail.

106. Monopolists may be able to earn profit, even in the long run, as the result of

a.

consumer ignorance.

b.

an inelastic demand for its product.

c.

product differentiation.

d.

high barriers to entry.

107. Which of the following is true of pure monopoly?

a.

Monopoly expands the options available to consumers.

b.

Monopoly results in allocative inefficiency.

c.

Profits and losses induce firms to enter and exit from industries.

d.

Monopoly works well when governments regulate prices.

108. Which of the following is true under unregulated monopoly?

a.

Monopoly results in more output than under pure competition.

b.

Monopoly results in a more efficient allocation of resources than competition.

c.

Monopoly expands the choices available to consumers.

d.

Monopoly results in lower output and higher prices than competition.

109. Which of the following is a valid criticism of unregulated monopoly?

a.

Monopoly limits the options available to consumers.

b.

Relative to a competitive market, a monopolist generally will produce too great an output.

c.

Profit-maximizing monopolists will fail to produce at the lowest possible cost.

d.

A monopoly’s output will often be more than if the market were competitive.

110. Assuming that firms maximize profits, how will the price and output policy of an unregulated

monopolist compare with ideal market efficiency?

a.

The output of the monopolist will be too large and the price too high.

b.

The output of the monopolist will be too large and the price too low.

c.

The output of the monopolist will be too small and the price too high.

d.

The output of the monopolist will be too small and the price too low.

111. Economists generally criticize high barriers to market entry because

a.

the ability of consumers to discipline producers is weakened.

b.

unregulated monopolists and oligopolists can often gain by increasing output and raising

price.

c.

legal barriers to entry will encourage firms to “invest” resources in developing highly

desired products that consumers are willing to pay more for.

d.

entry barriers are popular with consumers but not businesses.

112. When the government imposes a barrier to entry in a market,

a.

more resources will be wasted by firms attempting to secure and maintain market power.

b.

the options available to consumers will increase in the protected market.

c.

allocative efficiency will be improved by the reduction of wasteful competition.

d.

consumers will be better able to direct the smaller number of producers to serve their

interests.

113. Which of the following is an important side effect of government licensing and other grants of

monopoly power?

a.

The number of options available to consumers is increased.

b.

Competition is enhanced.

c.

Firms will produce more efficiently.

d.

Rent-seeking is encouraged.

114. In the area of business, rent-seeking often involves

a.

the use of resources to construct high-priced rental housing.

b.

the use of resources to secure and maintain a grant of monopoly power from the

government.

c.

an agreement between firms to raise prices and limit entry.

d.

an agreement between a firm and a customer that makes both parties better off.

115. A natural monopoly is defined as an industry in which one firm

a.

can produce the entire industry output at a lower average cost than a larger number of

firms could.

b.

can produce the entire industry output at a lower marginal cost than a larger number of

firms could.

c.

is very large relative to other firms that could enter the industry.

d.

can earn higher profits if it is the only firm in the industry rather than if other firms also

enter the industry.

116. To be a natural monopoly, a firm must

a.

control an essential natural resource input.

b.

be very large.

c.

have a continuously falling average cost curve as output rises.

d.

have falling average costs over a substantial range of total market demand.

117. If government officials break a natural monopoly up into several smaller firms, then

a.

competition will force firms to attain economic profits rather than accounting profits.

b.

competition will force firms to produce surplus output, which drives up price.

c.

the average costs of production will increase.

d.

the average costs of production will decrease.

118. A natural monopoly is a market where

a.

a single firm has control over a vital natural resource.

b.

many smaller firms can produce the entire market output at the same per-unit cost as could

one large firm.

c.

a single large firm can produce the entire market output at a lower per-unit cost than a

group of smaller firms.

d.

many smaller firms can produce the entire market output at a lower per-unit cost than

could one large firm.

119. An industry is said to be a natural monopoly when

a.

legal barriers limit entry into the market.

b.

diseconomies of scale are present in the market.

c.

the market demand for the product supplied by a firm is inelastic.

d.

long-run ATC continues to decline as firm size increases.

e.

larger firms have higher per-unit costs than their smaller rivals.

120. Which of the following is true under natural monopoly?

a.

The marginal cost curve will be above the average cost curve.

b.

The monopolist will set price equal to marginal cost and will earn economic profits.

c.

Economies of scale will be present.

d.

Output is produced under conditions of constant cost.

121. In the case where a natural monopoly exists in an industry,

a.

a competitive market structure will be costly and difficult to maintain.

b.

a competitive market structure will be more efficient and more equitable.

c.

government regulations will always improve efficiency in this industry.

d.

economies of scale will not be a consideration when analyzing the proper structure of the

industry.

122. Antitrust action restructures a previously monopolized industry into a competitive industry. If

economies of scale are unimportant in the industry, the expected result of this movement from

monopoly to competition is

a.

a reduction in output and an increase in price in the industry.

b.

a reduction in both price and output in the industry.

c.

an increase in both price and output in the industry.

d.

an increase in output and a reduction in price in the industry.

123. Which of the following are illegal under the antitrust laws of the United States?

a.

charging prices that exceed average total costs

b.

charging some consumers different prices than others

c.

mergers that unnecessarily create excessively large firms

d.

collusive behavior or other actions designed to create a monopoly or cartel

124. When economies of scale are important, imposing competition by splitting a monopolistic firm into

many rival units will

a.

lead to an increase in the per-unit cost of production in the industry.

b.

not affect per-unit costs but will affect demand conditions.

c.

generally increase the social efficiency of production.

d.

cause the industry demand curve to increase (shift to the right).

125. Breaking a monopoly firm into several rival firms will be unlikely to improve economic efficiency

when economies of scale are important because

a.

several smaller firms will have higher per-unit costs than a single larger firm.

b.

a single firm will have higher per-unit costs than several smaller firms.

c.

it is harder to regulate many smaller firms than it is one large firm.

d.

consumers will find it harder to choose among the products of many alternative sellers.

126. Regulating “natural monopolies” according to the “rate of return” criterion is likely to

a.

increase the monopolist’s incentive to minimize cost.

b.

increase output compared to the situation where the firm is unregulated.

c.

completely eliminate the “welfare loss” due to monopoly.

d.

do all of the above

127. Regulating natural monopolies according to the “rate of return” criterion is likely to

a.

reduce the incentive of firms to minimize cost.

b.

result in a smaller quantity of output than when the natural monopolist is unregulated.

c.

discourage the firms from investing resources in an effort to influence the decisions of the

regulatory agency.

d.

increase the number of firms in the industry.

128. A regulatory agency that imposes a price ceiling in order to limit monopoly profits to a “fair rate of

return” is forcing the monopolist to sell at a price equal to

a.

average fixed cost.

b.

average total cost.

c.

marginal cost.

d.

average variable cost.

129. If the government wants a natural monopoly to earn a “fair return” or zero economic profit, it will set

a.

price equal to marginal cost.

b.

price equal to average total cost.

c.

price equal to average revenue.

d.

marginal cost equal to marginal revenue.

e.

marginal cost equal to average total cost.

130. Compared to the profit-maximizing outcome, average cost pricing in natural monopoly leads to

a.

a higher price.

b.

decreased consumer surplus.

c.

the elimination of economic profit.

d.

less output.

131. Because of the rise of global competition and free trade,

a.

antitrust policy may be less necessary than previously thought.

b.

U.S. industrial concentration poses more of a threat to consumers.

c.

U.S. markets are becoming less competitive.

d.

U.S. manufacturers are seeking fewer trade barriers.

132. Which of the following is a major shortcoming of government regulation of business monopoly?

a.

The regulators often estimate production costs incorrectly and thus force firms into loss

positions.

b.

The regulators often come to represent the interests of the established firms and use their

power to limit competition.

c.

The regulators usually permit firms to make unusually high accounting profits.

d.

The regulators, acting in consumers’ interests, often force prices so low that even with

efficient production techniques the regulated firms lose money.

133. When a regulatory agency uses marginal cost pricing to regulate a monopolist,

a.

price will exceed marginal cost.

b.

production costs will probably exceed the total revenues of the monopolist.

c.

marginal cost will equal average total cost.

d.

social welfare could be improved if average cost pricing was used instead

134. Which of the following is a problem that arises when regulations force “natural monopolies,” like

electric utilities, to charge a price that is equal to their marginal cost (MC)?

a.

This price will force the firms out of business in the long run.

b.

The firms have an incentive to pad their fixed costs.

c.

When price is equal to MC, new firms will enter the industry and drive up the costs of

production.

d.

Both b and c are correct.

135. What problem does the government have that makes price regulation less than an ideal solution?

a.

There is no effective way to enforce price regulation.

b.

The government cannot tell what price a firm is charging.

c.

Regulators frequently will not have the information they need to set prices.

d.

Regulation often will lead to lower costs.

136. Government-operated firms with monopoly power

a.

will necessarily meet the criteria of economic efficiency, as long as price equals average

total cost.

b.

will always be more efficient than private firms because they do not have to make a profit.

c.

are likely to be inefficient since some of the monopoly power is likely to serve the

interests of the governmental managers and employees.

d.

are highly responsive to changes in the preferences of individual consumers since

consumers are also voters.

137. The incentive for managers of a government-operated firm (for example, a state university or the U.S.

Post Office) to operate efficiently will be

a.

low because all government workers are lazy.

b.

low because there are no residual claimants to monitor and institute cost-reducing

measures.

c.

high because government employees and officials will be less concerned with personal

gain.

d.

high because voters can easily detect those who are to blame for inefficiencies and replace

them.

138. Which of the following has tended to increase the competitiveness of markets in the United States

during the last couple of decades?

a.

increases in transport costs

b.

development of the Internet

c.

decreased competition from imports

d.

more government regulation of product quality

139. Which of the following is true?

a.

Competitive forces are present even in markets with high barriers to entry.

b.

Quality competition is an unimportant element of the competitive process.

c.

Profitability and high prices discourage technological change and the development of

substitute products.

d.

Government regulations have substantially increased the quality of American

manufacturing products in recent years.

140. Which of the following is true?

a.

Competitive forces are stronger in markets with high entry barriers than in those where

entry barriers are low.

b.

Quality competition is an important element of the competitive process.

c.

If the production of a good is highly profitable, the development of substitute products

will be discouraged.

d.

High barriers to entry are only the result of natural factors not artificial factors like

government regulations.

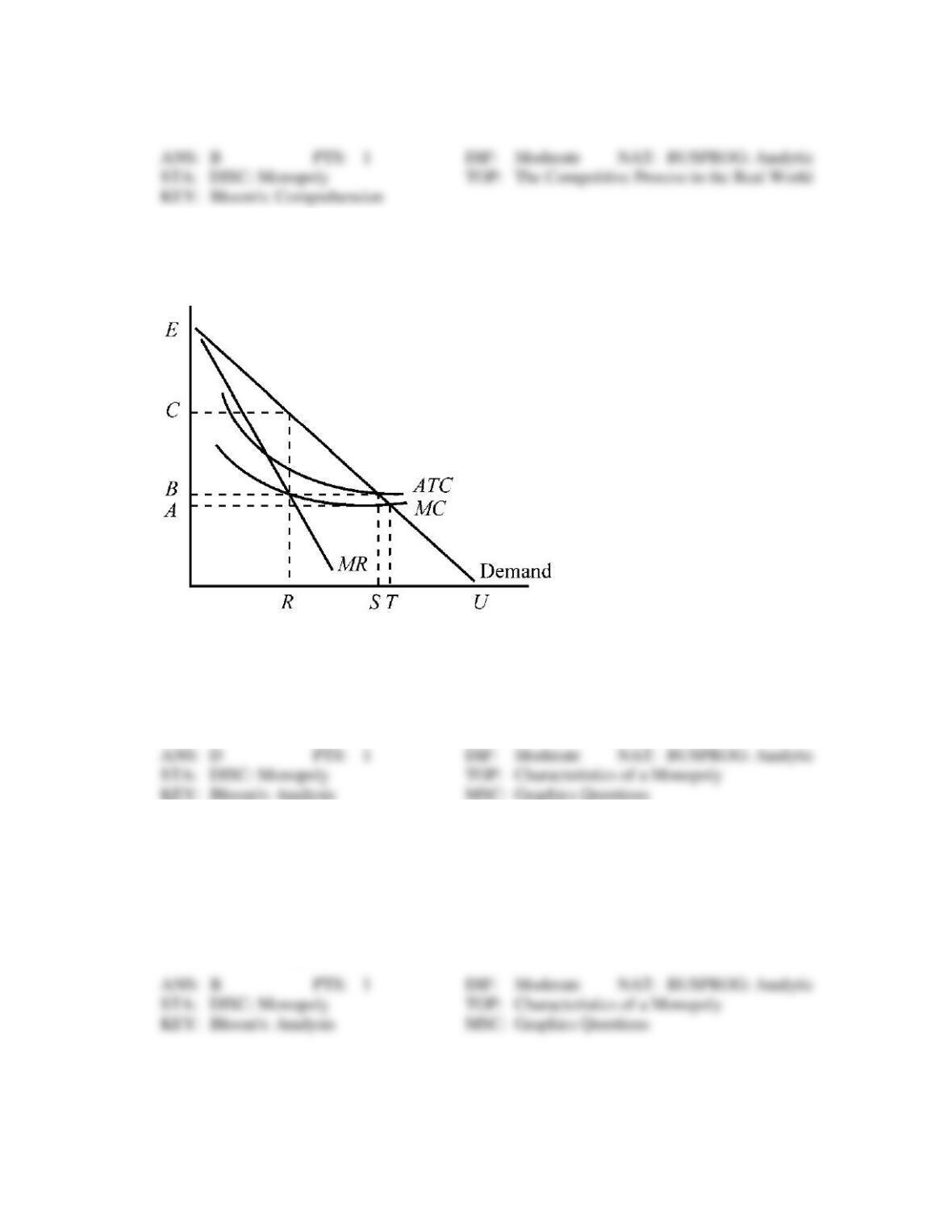

Use the figure to answer the following question(s).

Figure 11-1

141. What price and output in Figure 11-1 would an unregulated profit-maximizing monopolist choose?

a.

price A and output T

b.

price B and output S

c.

price B and output R

d.

price C and output R

142. If a regulatory agency were using the “normal return” (zero economic profit) criteria to impose a price

on a monopolist with the cost and demand conditions depicted in Figure 11-1, what price would the

regulators set, and what output would the monopolist produce?

a.

price A and output T

b.

price B and output S

c.

price B and output R

d.

price C and output R

Use the figure to answer the following question(s).

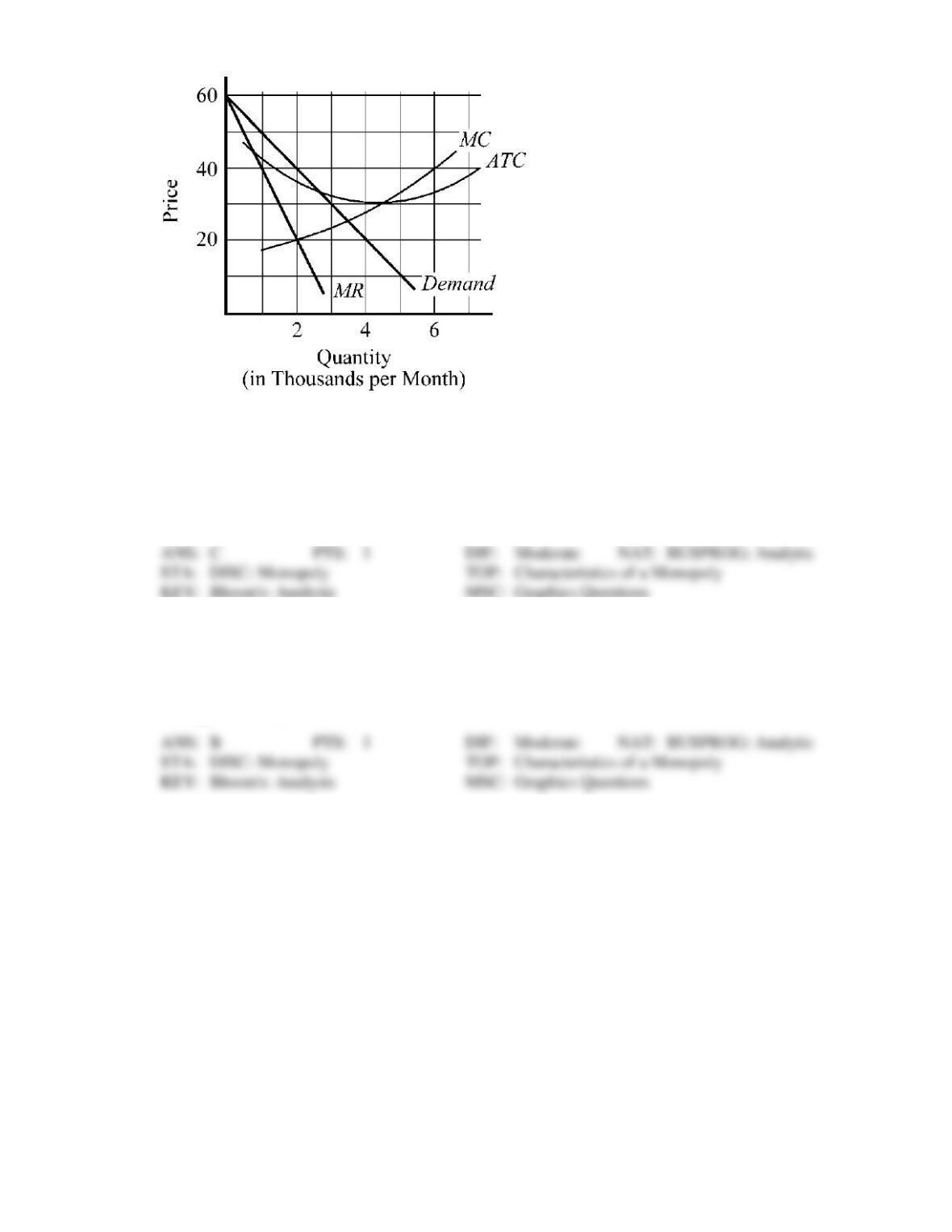

Figure 11-2

143. The cost and demand conditions for a monopolist are depicted in Figure 11-2. If the monopolist is

maximizing profit, it will charge a price of

a.

$30 and produce an output of 4,000.

b.

$40 and produce an output of 4,000.

c.

$40 and produce an output of 2,000.

d.

more than $40.

144. What is the maximum profit per month that the monopolist will be able to earn in Figure 11-2?

a.

zero

b.

approximately $10,000

c.

approximately $20,000

d.

approximately $40,000

Use the figure to answer the following question(s).

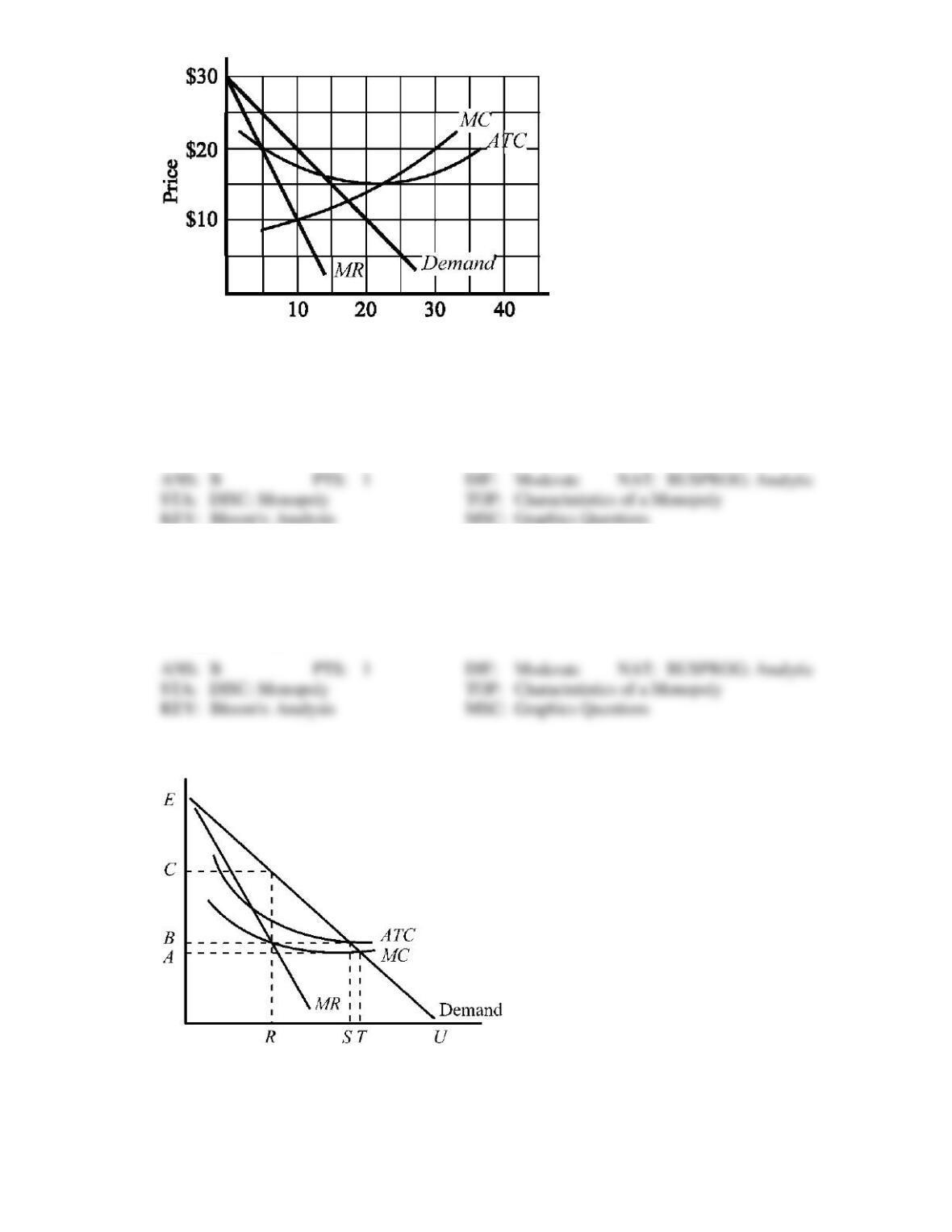

Figure 11-3

145. The cost and demand conditions for a monopolist are depicted in Figure 11-3. If the monopolist is

maximizing profit, it will charge a price of

a.

$10 and produce an output of 20,000.

b.

$20 and produce an output of 10,000.

c.

$20 and produce an output of 20,000.

d.

more than $20.

146. What is the maximum profit per month that the monopolist will be able to earn in Figure 11-3?

a.

zero

b.

approximately $20,000

c.

approximately $50,000

d.

approximately $100,000

Figure 11-4

147. What output would a monopolist with the demand and cost conditions depicted in Figure 11-4 produce

if ordered by regulators to serve the entire market at average cost?

a.

R

b.

S

c.

T

d.

U

Figure 11-5

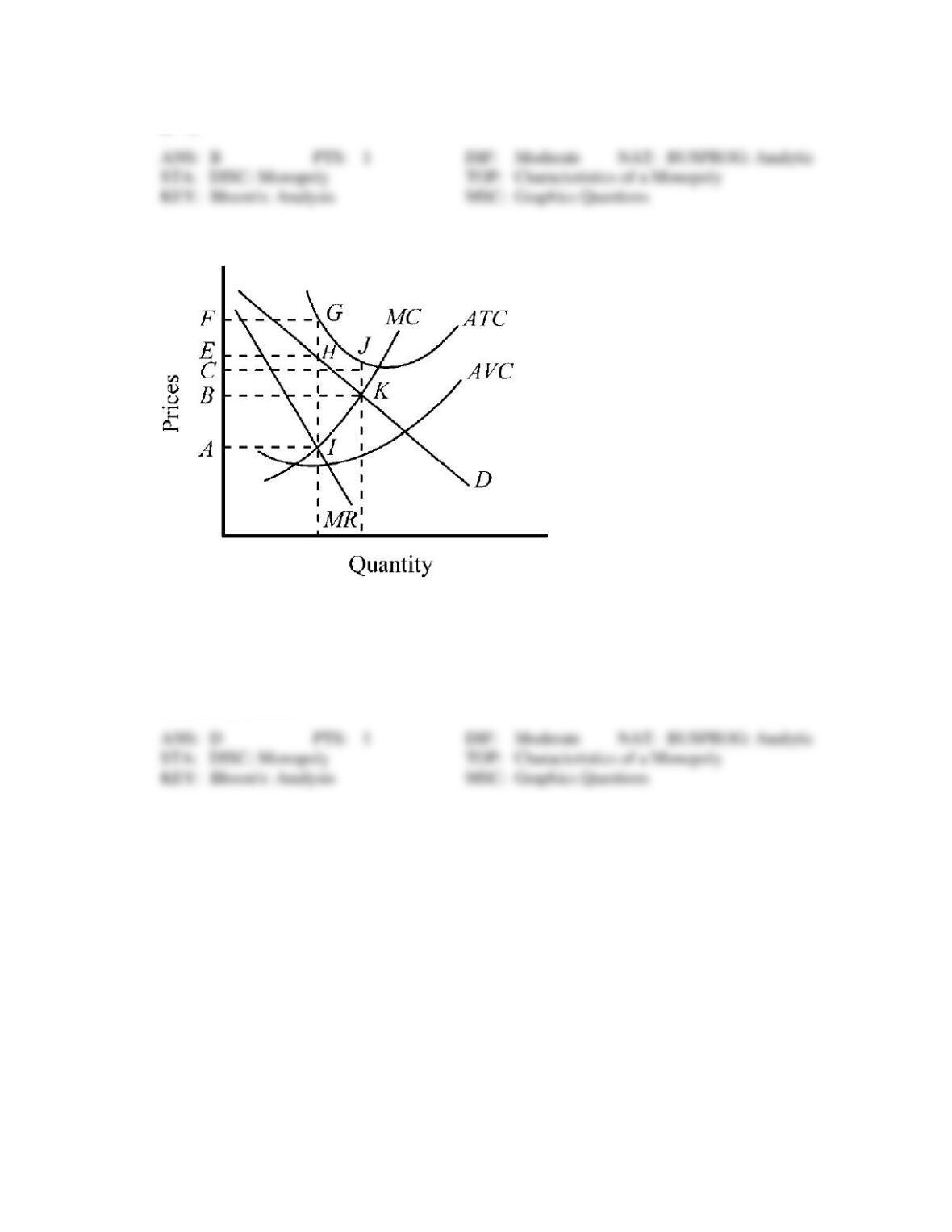

148. Indicate the maximum profit (or minimum loss) a pure monopolist with the cost and demand

conditions depicted in Figure 11-5 would be able to achieve.

a.

profit of AIHE

b.

profit of BKJC

c.

losses of BKJC

d.

losses of EHGF

Use the figure to answer the following question(s).

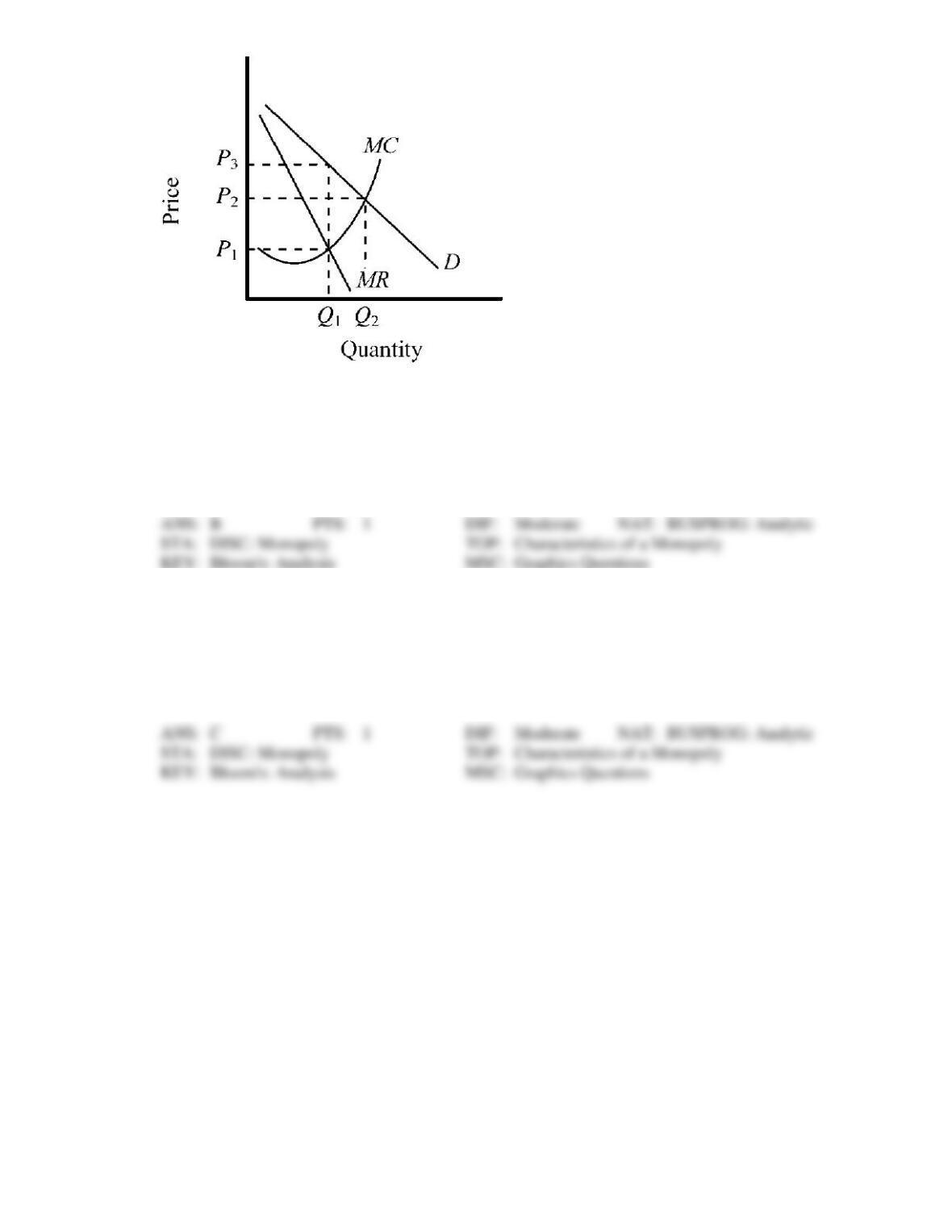

Figure 11-6

149. The demand and cost conditions in an industry are as depicted in Figure 11-6. In the viewpoint of

economic efficiency, what would the ideal price and output be?

a.

price, P1; quantity produced, Q1

b.

price, P2; quantity produced, Q2

c.

price, P3; quantity produced, Q1

d.

price, P1; quantity produced, Q2

150. If the output in the industry is produced by a monopolist, at what price will the good sell and what

quantity will be produced in Figure 11-6?

a.

price, P1; quantity produced, Q1

b.

price, P2; quantity produced, Q2

c.

price, P3; quantity produced, Q1

d.

price, P3; quantity produced, Q2

Use the figure to answer the following question(s).

Figure 11-7