Exam

Name___________________________________

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

1)

Price equals the minimum of long–run average cost

1)

A)

along a horizontal long–run supply curve, but not along an upward sloping long–run supply

curve.

B)

whenever average revenue equals marginal cost.

C)

in a short–run equilibrium as well as in a long–run equilibrium.

D)

in a long–run equilibrium.

2)

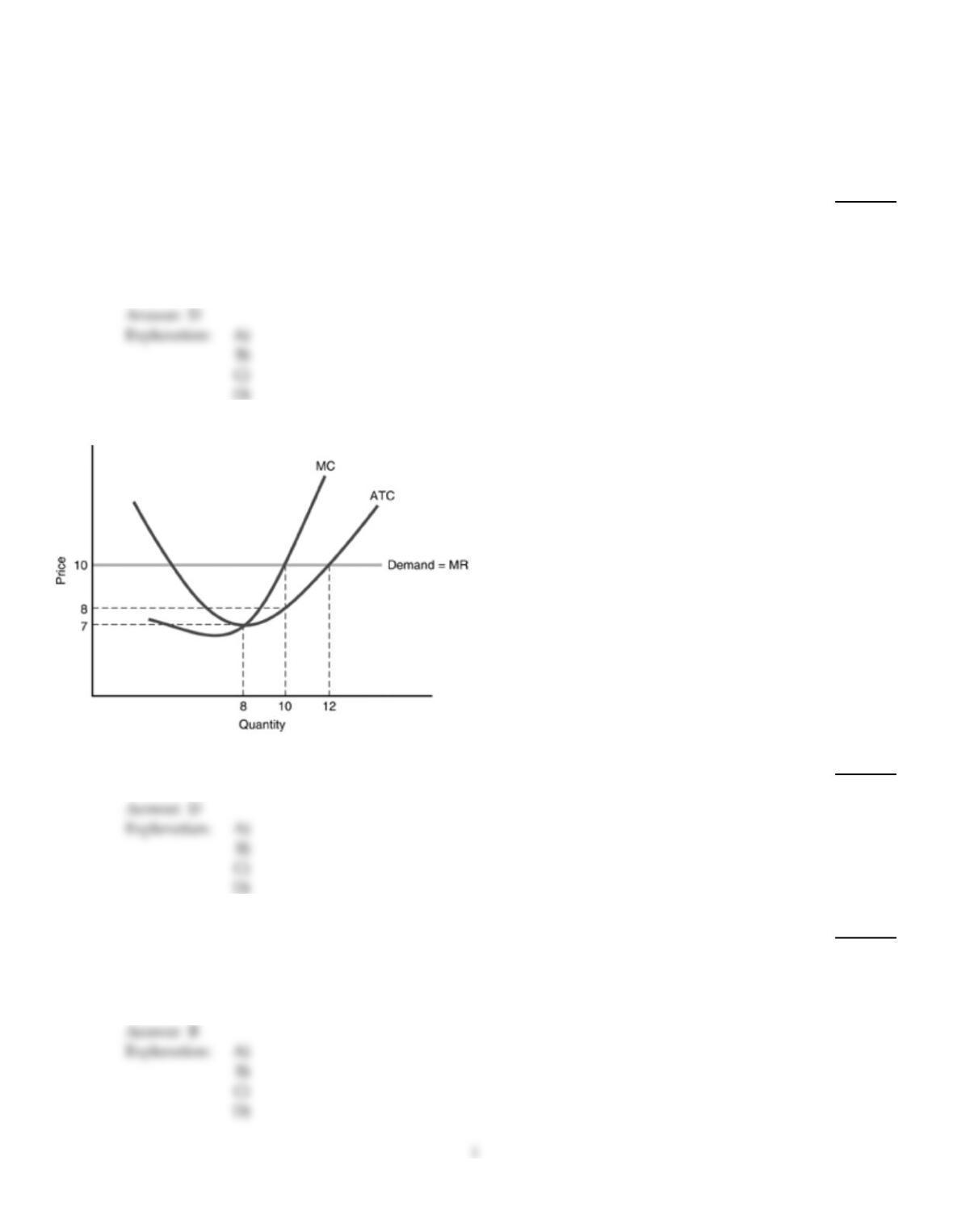

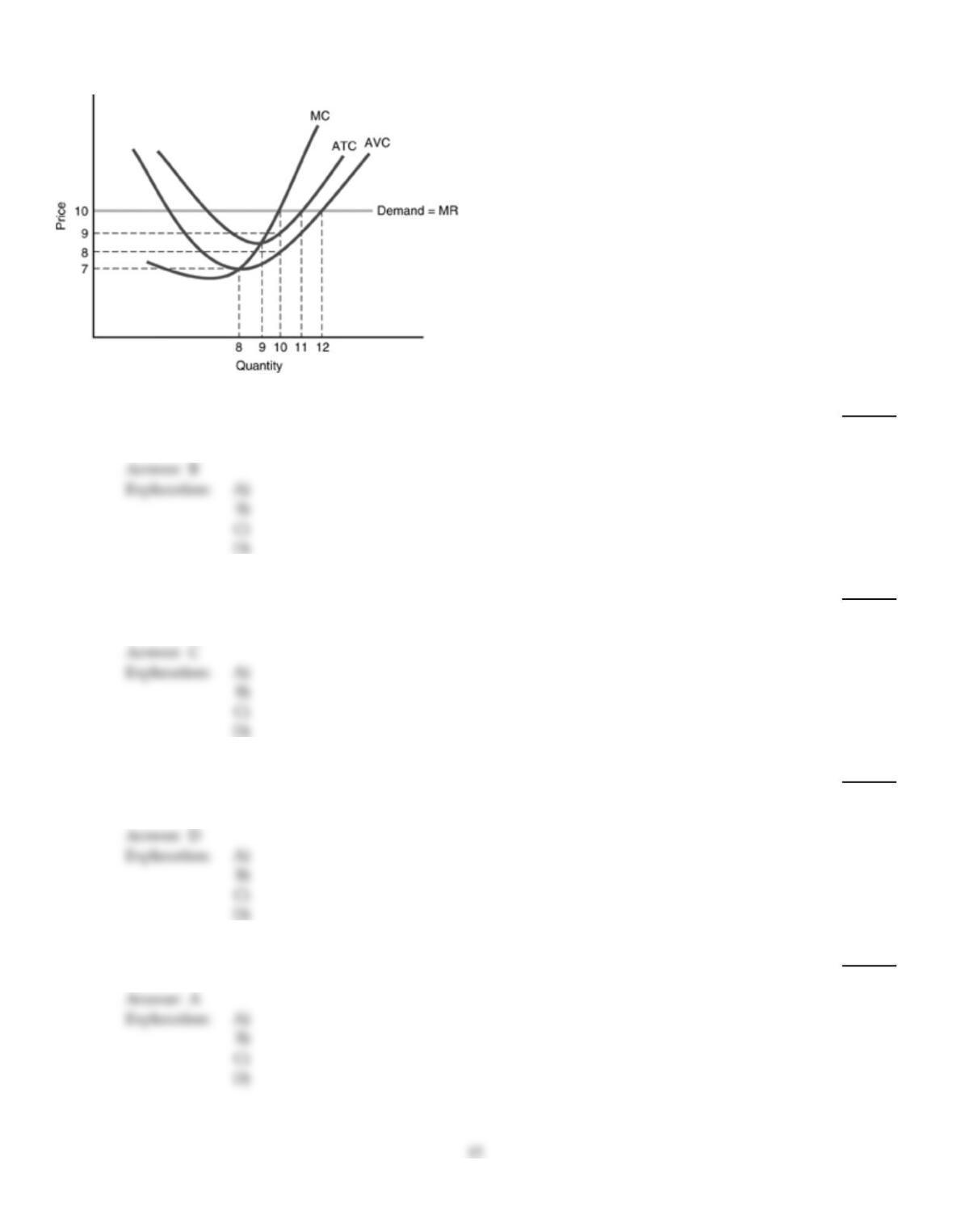

In the above figure, what is the profit–maximizing output and price?

2)

A)

12, $10

B)

8, $7

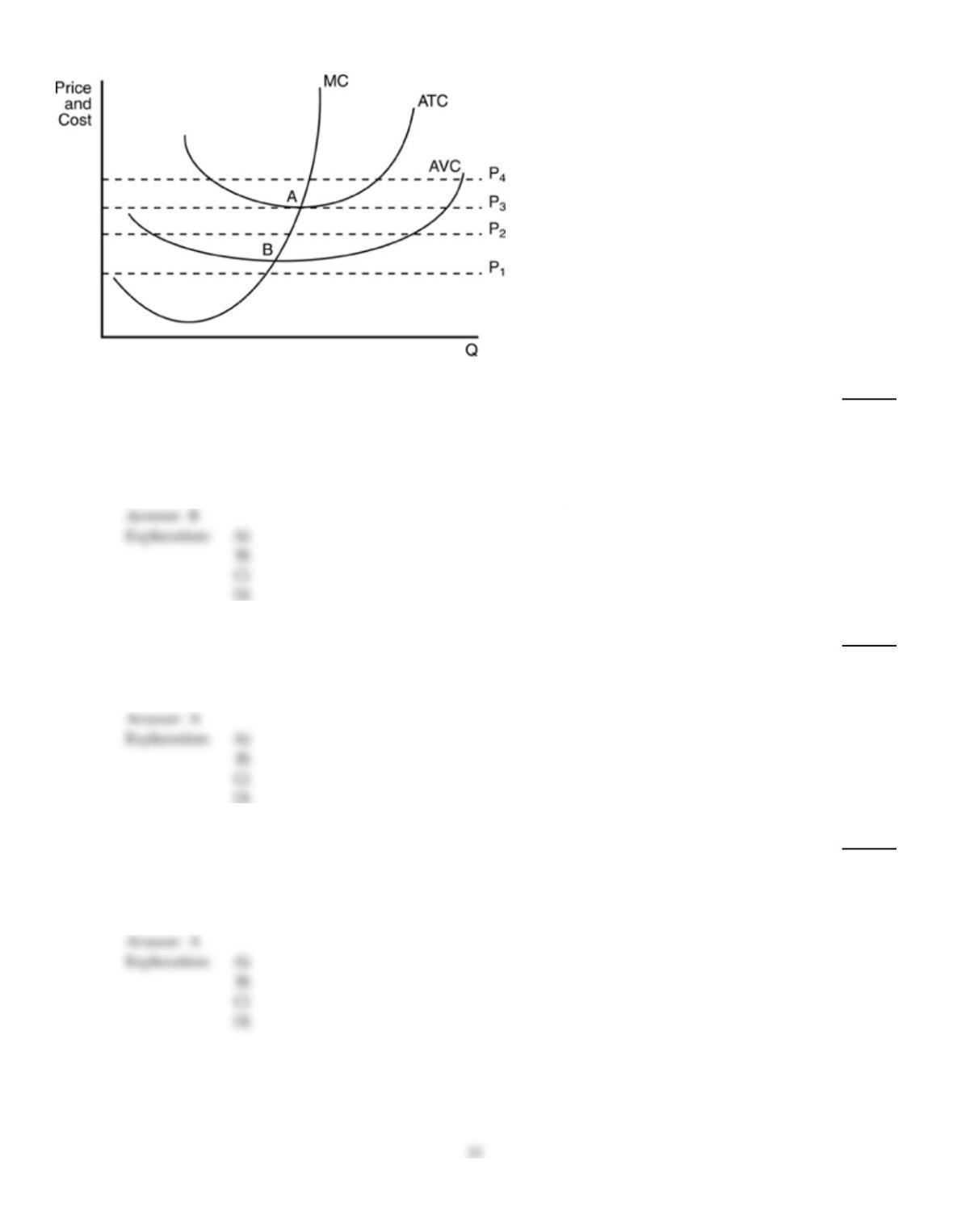

C)

10, $8

D)

10, $10

3)

For a firm in a perfectly competitive industry

3)

A)

the demand curve is unitary elastic throughout.

B)

marginal revenue and product price are equal at every level of output.

C)

more output can be sold only if the firm unilaterally lowers its product price.

D)

the price elasticity of demand is zero.

4)

Which of the following is true for the perfectly competitive firm?

4)

A)

AR is more than price.

B)

Price and MR are always equal.

C)

AR is less than price.

D)

Price elasticity of demand is equal to 1.

5)

The change in total revenues resulting from a change in output of one unit is

5)

A)

quantity revenue.

B)

average revenue.

C)

marginal revenue.

D)

price revenue.

6)

If an industry’s long–run supply curve slopes downward, then the industry is

6)

A)

a fixed–cost industry.

B)

a decreasing–cost industry.

C)

an increasing–cost industry.

D)

a constant–cost industry.

7)

Perfect competition is characterized by

7)

A)

a small number of firms.

B)

many buyers and sellers.

C)

high barriers to entry.

D)

differentiated products of firms in the industry.

8)

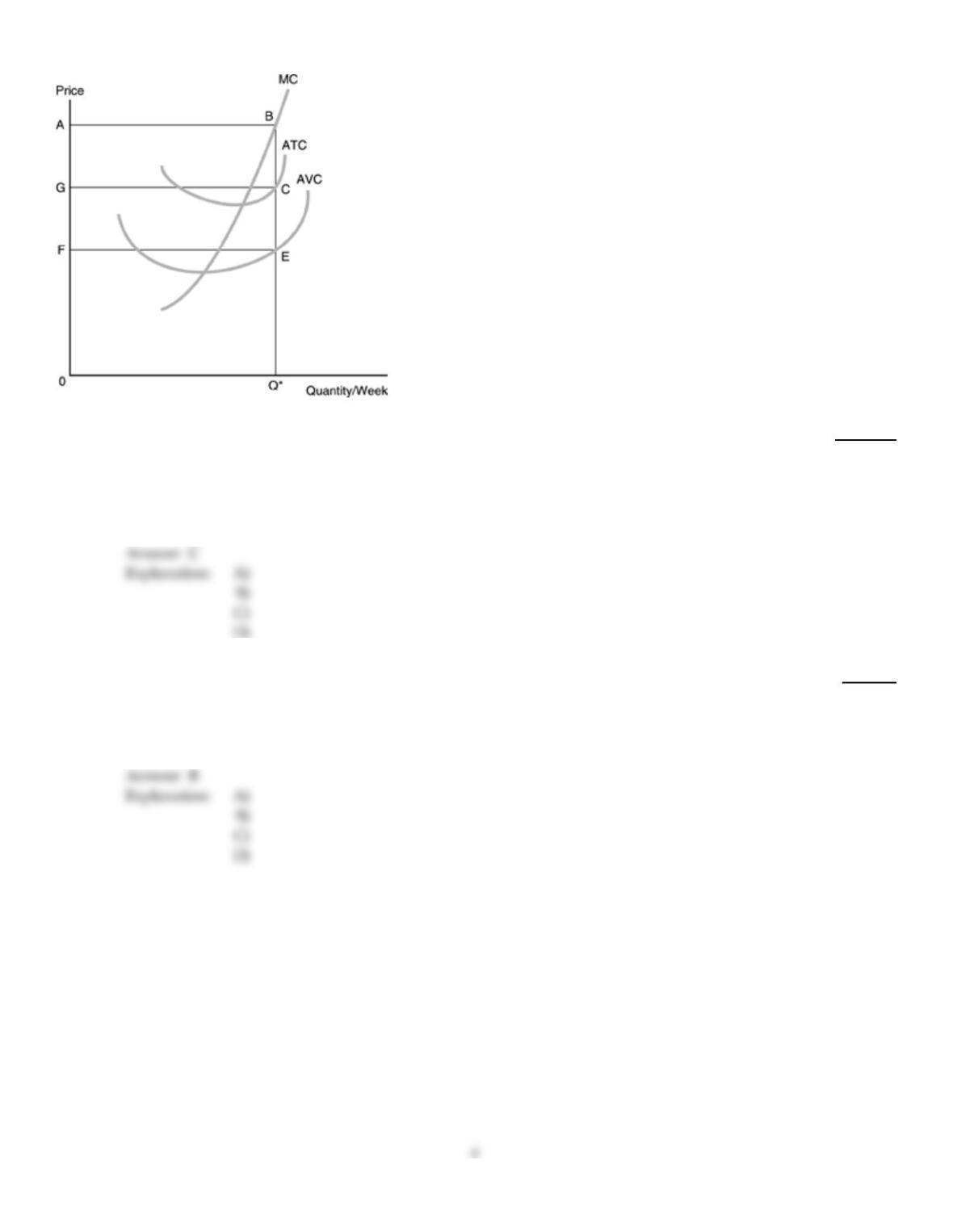

In the above figure, at the profit–maximizing rate of production for the perfectly competitive firm

total cost is

8)

A)

$100.

B)

$30.

C)

$70.

D)

$130.

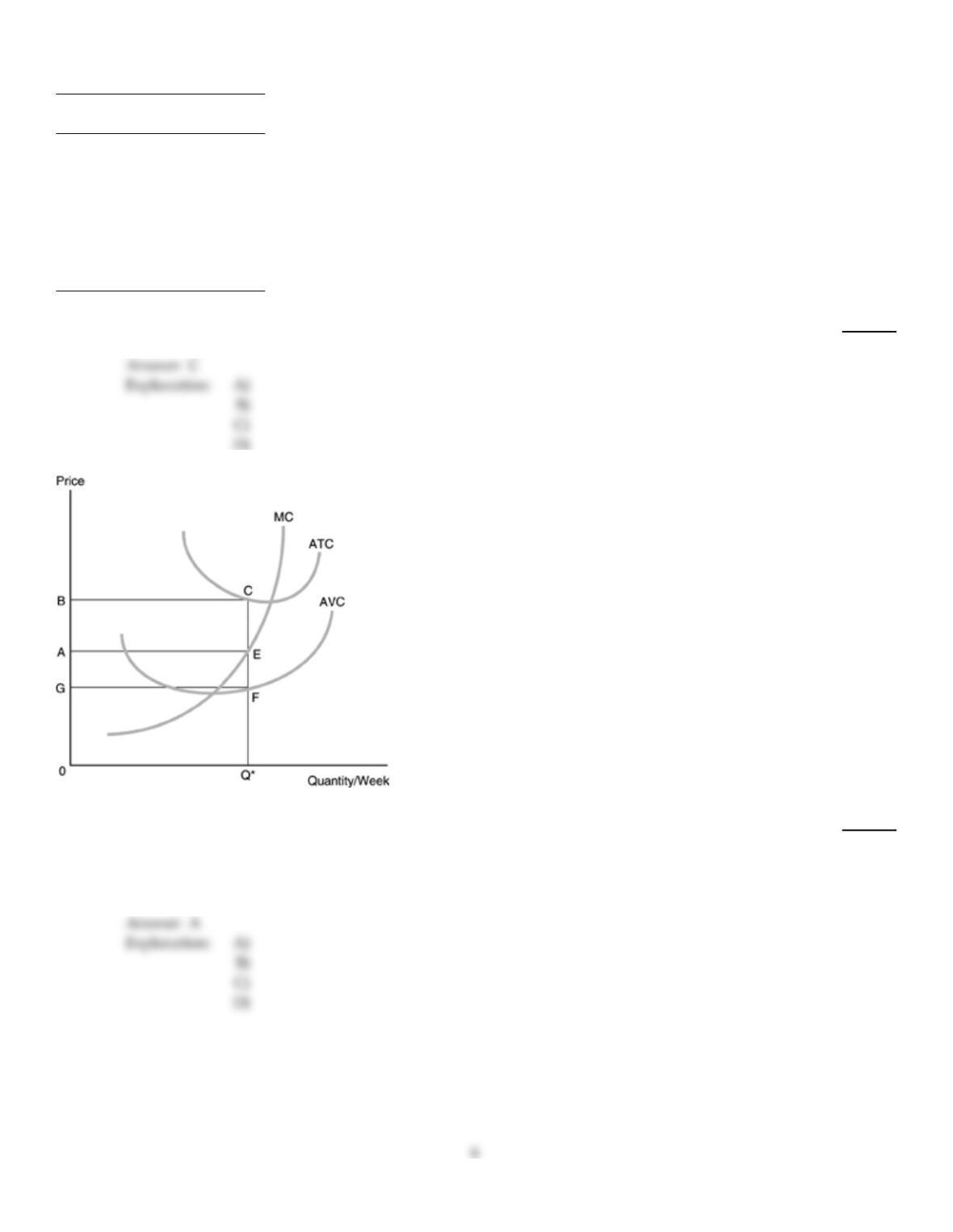

9)

Refer to the above figure. If the market price is equal to A, which statement can be made about

economic profits?

9)

A)

Economic profits are negative and equal to ABQ0.

B)

Economic profits are negative and equal to GCEF.

C)

Economic profits are positive and equal to ABCG.

D)

Economic profits are positive and equal to ABEF.

10)

When marginal cost pricing occurs,

10)

A)

price equals average variable cost but exceeds average total cost.

B)

price equals the additional cost society incurs in producing the next unit of an item.

C)

the firm is at the shutdown point.

D)

the firm can only break even if it does not set price to marginal cost.

11)

Which of the following statements is correct?

11)

A)

The market demand curve of the perfectly competitive industry is downward sloping, so the

demand curves of the individual firms are also downward sloping.

B)

The market demand curve of the perfectly competitive industry is downward sloping while

the demand curve of an individual firm is horizontal with a height equal to the product price.

C)

The demand curve of the perfectly competitive industry is elastic as are the demand curves

facing the individual firms.

D)

The market demand curve of perfect competition is inelastic because the individual

consumers are buying a homogeneous product.

12)

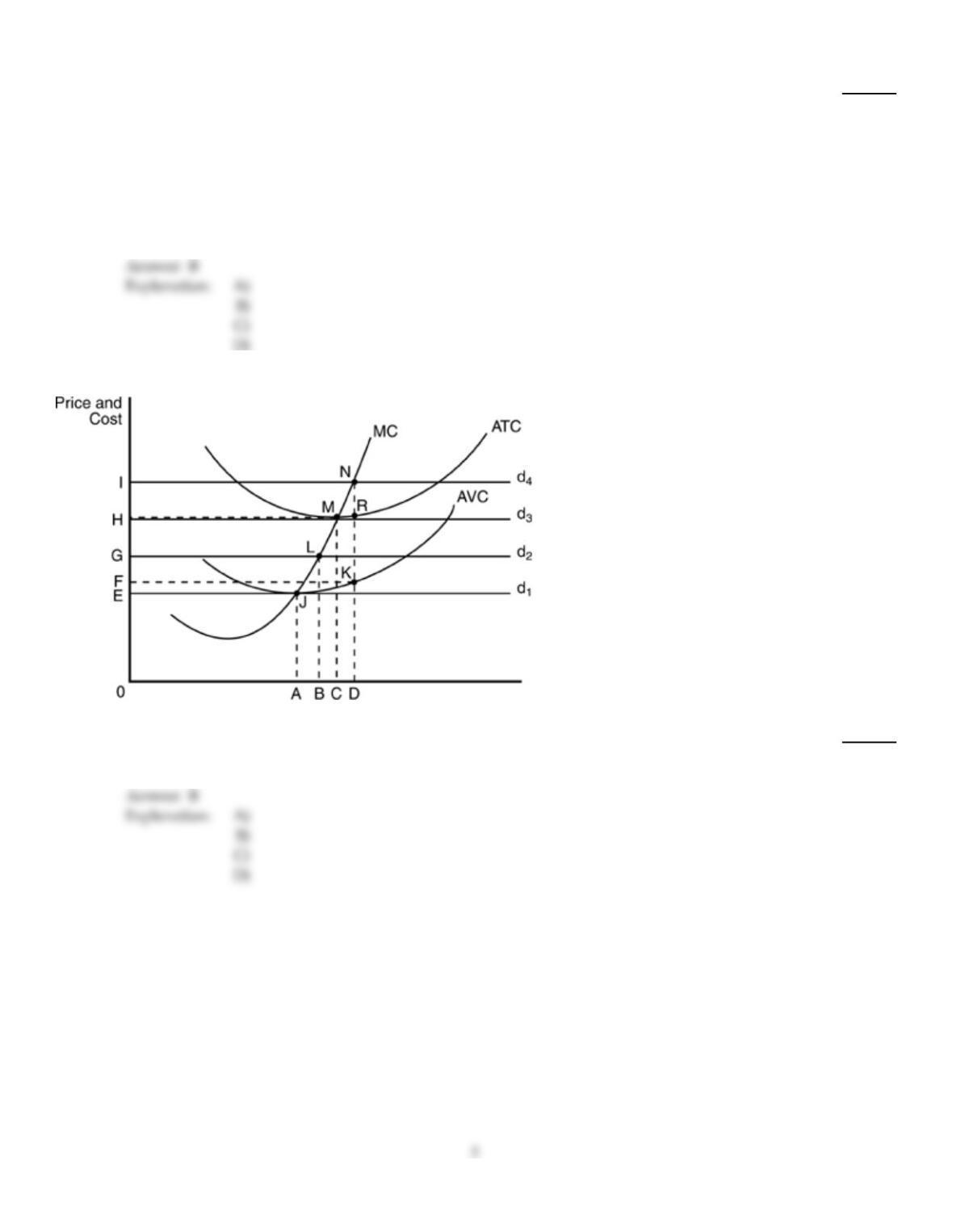

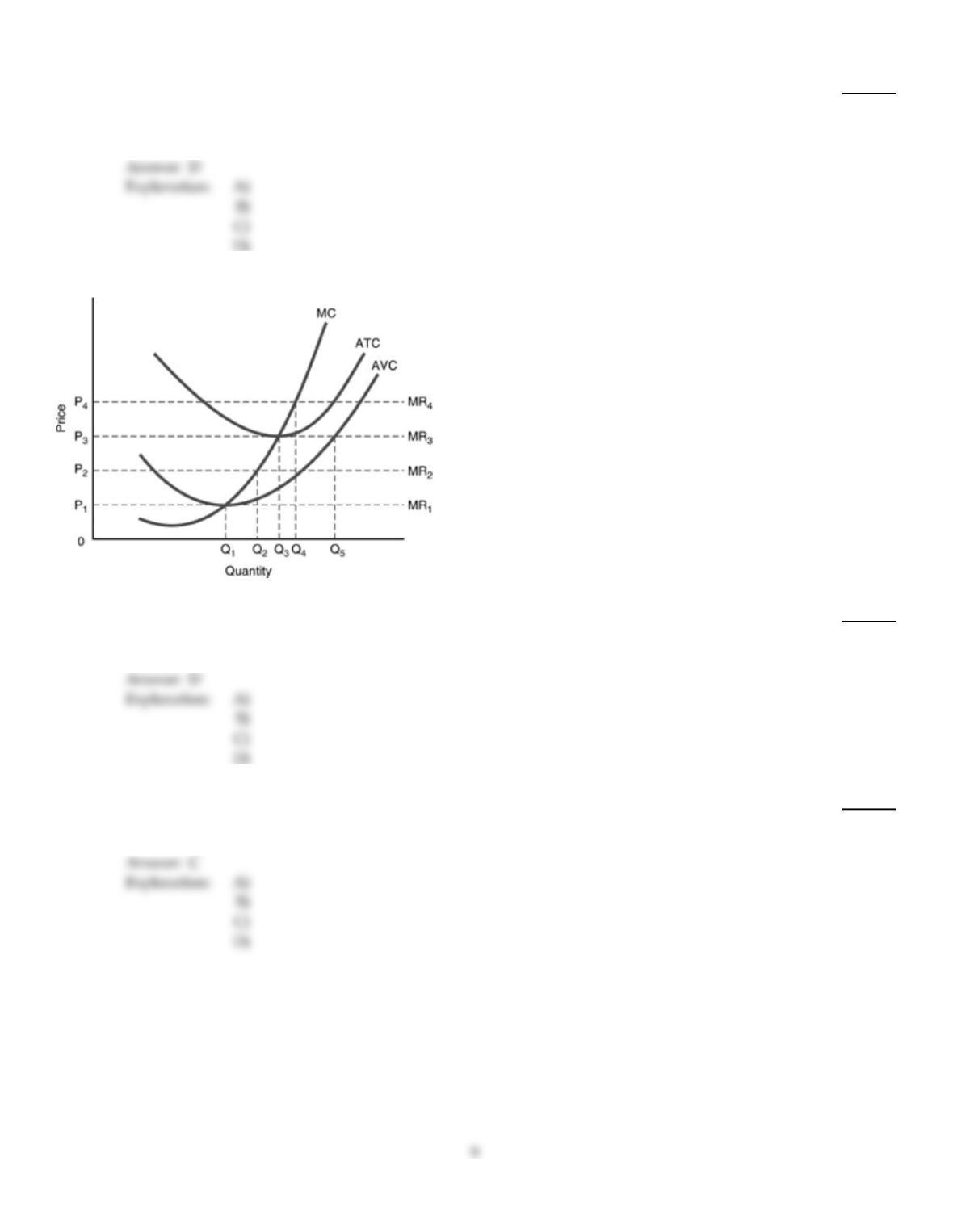

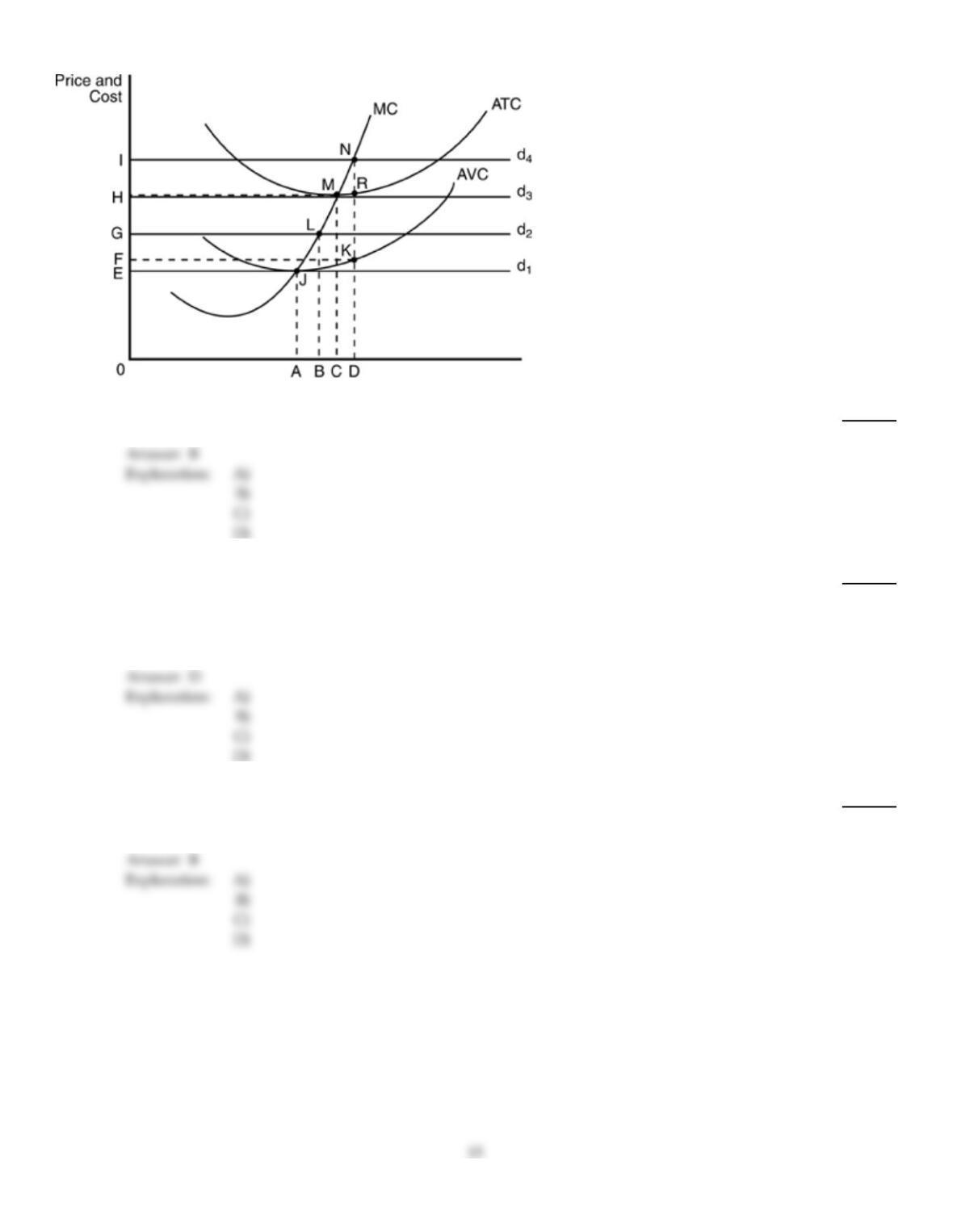

In the above figure, if d4 is the relevant demand curve for this firm, then which level of output will

maximize this firm’s profits or minimize its losses?

12)

A)

A

B)

D

C)

C

D)

B

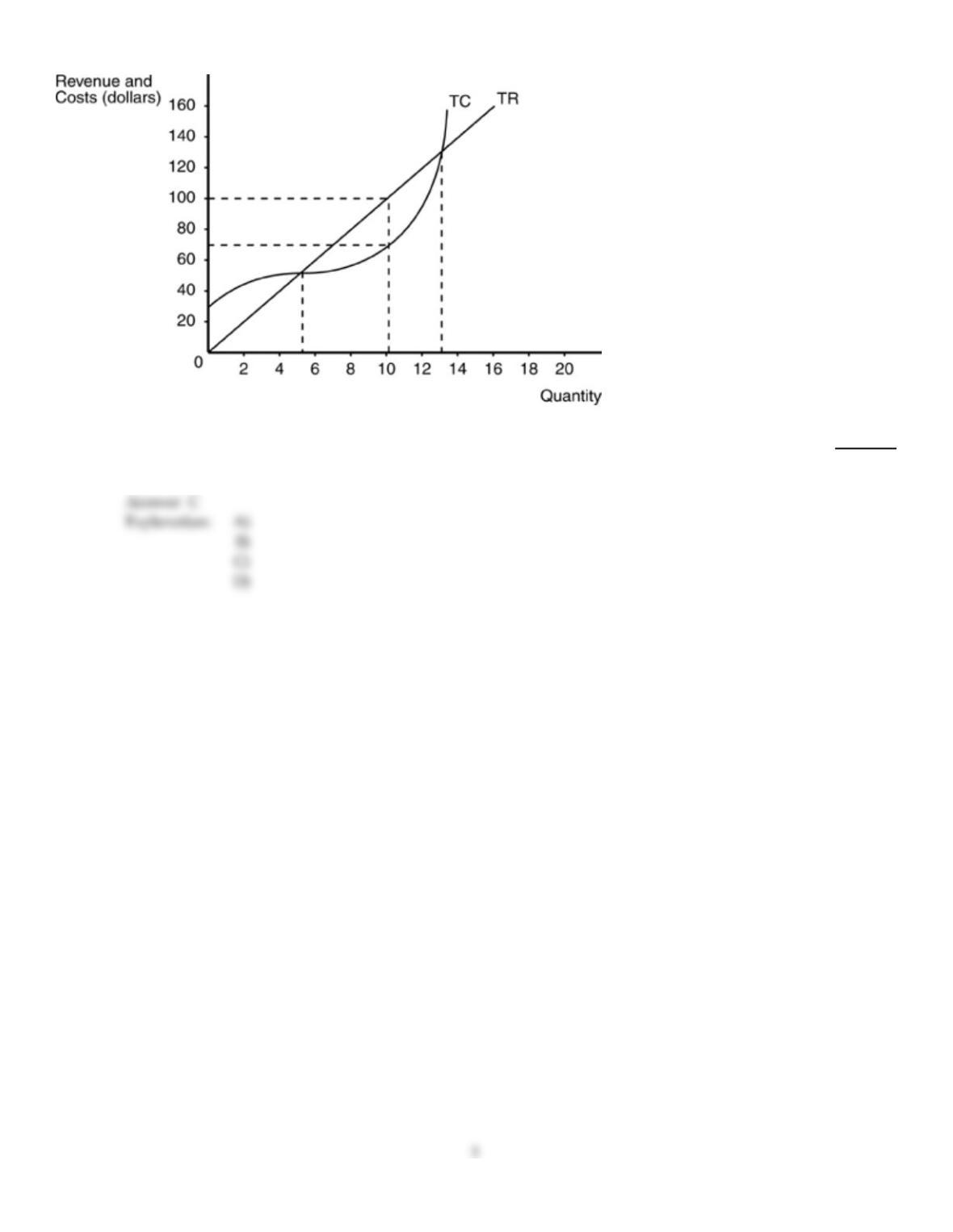

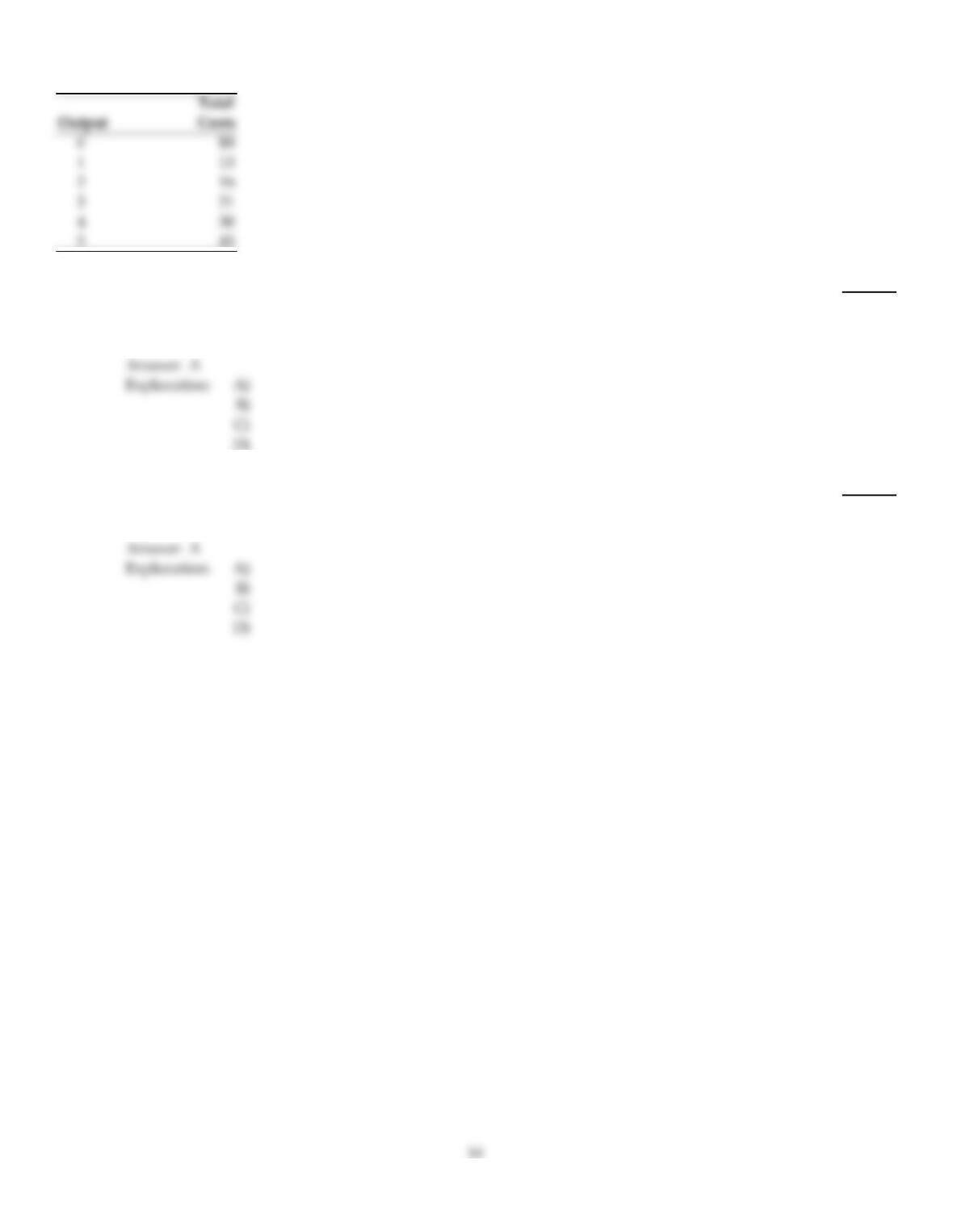

Total

Output Costs

100 $400

101 402

102 405

103 409

104 414

105 420

106 427

107 435

13)

Refer to the above table. If the price is $5, the maximum economic profits this firm could earn is

13)

A)

$520.

B)

$414.

C)

$106.

D)

$420.

14)

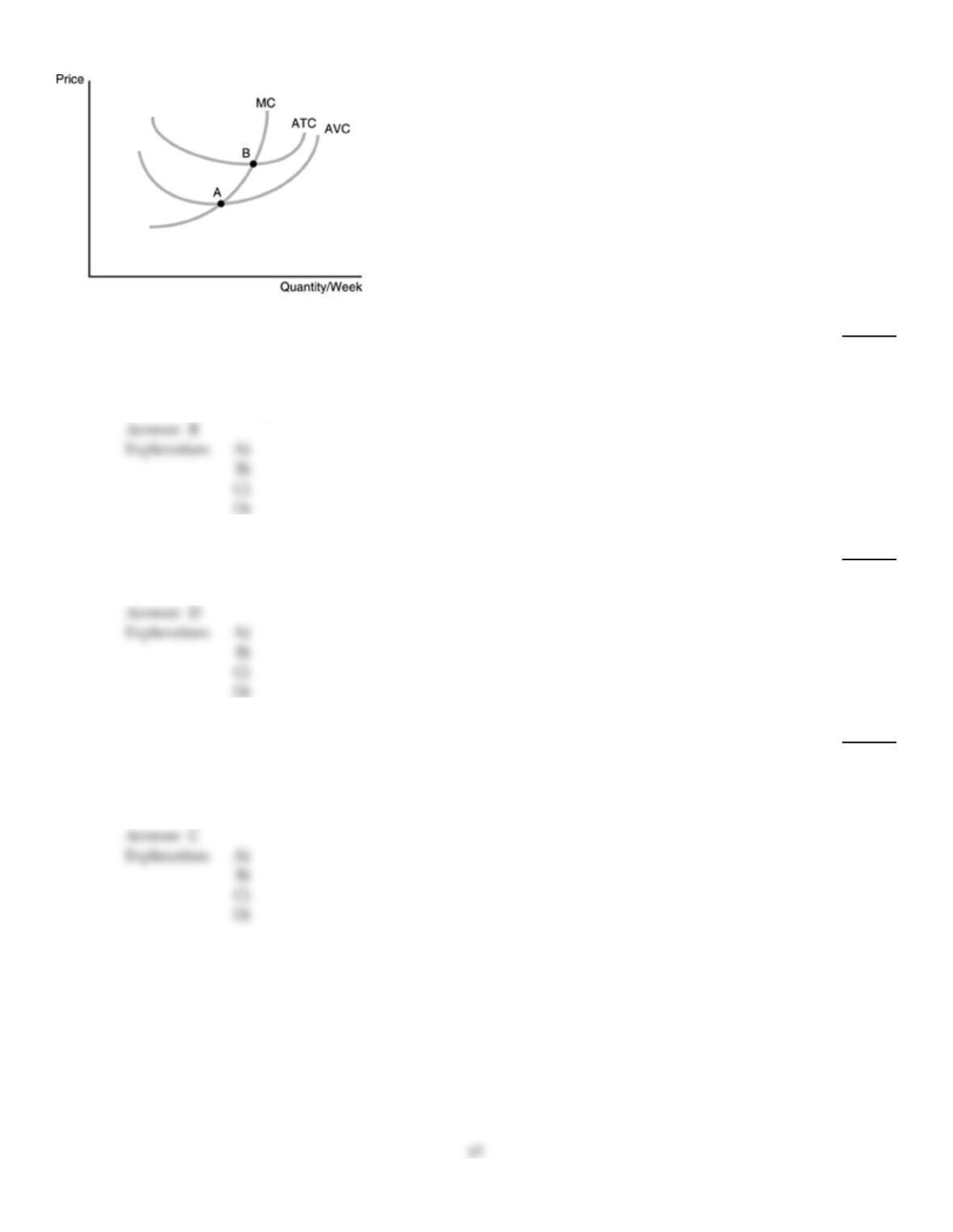

Refer to the above figure. In order to stay open in the short run, this firm must

14)

A)

receive a price equal to or greater than the minimum of its average variable cost.

B)

earn a positive profit.

C)

receive a price exactly equal to its average total cost.

D)

recover its fixed cost.

A

C

15)

The firm in a perfectly competitive industry is a

15)

A)

price maker.

B)

price seeker.

C)

price dealer.

D)

price taker.

16)

For a perfect competitor, price equals

16)

A)

average revenue only.

B)

neither marginal revenue nor average revenue.

C)

both average revenue and marginal revenue.

D)

marginal revenue only.

C

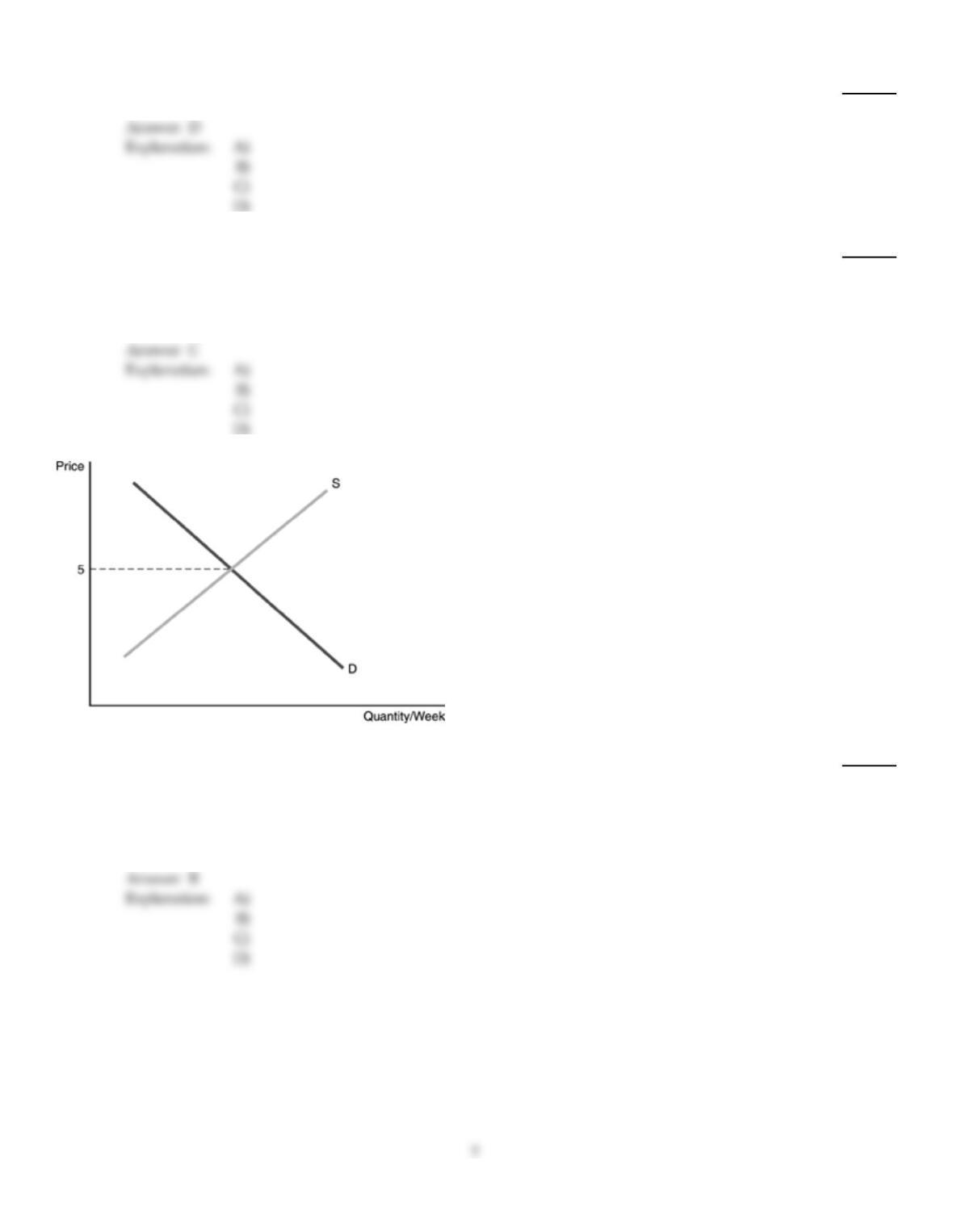

17)

Refer to the above figure. The figure represents the market demand and supply curves for widgets.

What statement can be made about the demand curve for an individual firm in this market?

17)

A)

An individual firm’s demand curve will be a smaller version of the market demand curve.

B)

An individual firm’s demand curve will be horizontal at $5.

C)

An individual firm’s demand curve will be horizontal at a price below $5.

D)

An individual firm’s demand curve cannot be determined from the graph above.

B

D

18)

Refer to the above table. If the price is $3 the maximum profit this firm could earn is

18)

A)

$99.

B)

–$100.

C)

–$99.

D)

$306.

19)

Suppose a perfectly competitive firm faces the following short–run cost and revenue conditions:

ATC = $12.00; AVC = $8.00; MC = $12.00; MR = $10.00. The firm should

19)

A)

change nothing.

B)

decrease output.

C)

increase price.

D)

increase output.

20)

Clothing retailers have faced greater competition in recent years as more firms have entered the

clothing market. Some of the competition has come from foreign competitors, but much of it is

domestic competition. As a result there is much competition in markets for many types of clothing

and

20)

A)

firms have a great degree of flexibility in pricing their products because these products can be

sold at a high profit level.

B)

there are relatively few buyers and sellers in the market, and one individual firm can

determine the market price.

C)

there are no other implications.

D)

individual buyers and sellers cannot affect the market price because it is determined by the

market forces of demand and supply.

21)

In a perfectly competitive market, which of the following is the main factor that affects consumers’

decisions on which firm to purchase a good from?

21)

A)

Customer service

B)

Quality

C)

Reputation

D)

Price

22)

Using the above figure, the perfectly competitive firm should shut down if the market price is

below

22)

A)

P2.

B)

P3.

C)

P4.

D)

P1.

23)

The total amount received from the sale of output is

23)

A)

price revenue.

B)

marginal revenue.

C)

total revenue.

D)

average revenue.

24)

The price per unit times the total quantity sold is

24)

A)

price revenue.

B)

marginal revenue.

C)

total revenue.

D)

average revenue.

25)

A firm earning economic losses should operate in the short run as long as

25)

A)

marginal revenue is at least the price per unit sold.

B)

the price per unit sold is equal to or greater than the marginal cost of production.

C)

the price per unit sold is greater than the average fixed cost per unit produced.

D)

the price per unit sold is greater than the average variable cost per unit produced.

D

26)

The demand curve faced by a perfectly competitive industry

26)

A)

is perfectly inelastic.

B)

slopes downward.

C)

has no slope.

D)

slopes upward.

B

27)

Which of the following is closest to a perfectly competitive market?

27)

A)

the market for automobiles

B)

the market for corn

C)

the market for breakfast cereal

D)

the pizza market

B

28)

A perfectly competitive industry’s short–run supply curve is best described as

28)

A)

horizontal.

B)

perfectly inelastic.

C)

the upward sloping portion of the industry’s marginal cost curve.

D)

the horizontal summation of the individual firms’ supply curves.

D

C

29)

In the above figure, what happens to the firm’s optimal level of output if the price it receives for its

product decreases from P4 to P3?

29)

A)

Output increases.

B)

Output decreases.

C)

Output stays the same.

D)

There is not enough information provided to know what happens to output.

30)

An industry in which an increase in industry output is accompanied by an increase in long–run

per–unit costs is a(n)

30)

A)

increasing–cost industry.

B)

constant–cost industry.

C)

break–even cost industry.

D)

decreasing–cost industry.

31)

If there is no output for which product price is sufficient to cover variable costs,

31)

A)

the firm should shut down in the short run.

B)

the firm earns economic profits by staying open.

C)

the firm should increase production.

D)

the firm should stay open in the short–run.

32)

A firm in a perfectly competitive market maximizes profits when it finds

32)

A)

the quantity at which total revenue is maximized.

B)

the quantity at which total revenue minus total cost is the greatest.

C)

the price at which total revenue minus total cost is the greatest.

D)

the quantity at which total revenue equals total cost.

33)

In a perfectly competitive industry

33)

A)

each firm is a price maker.

B)

firms can never make an economic profit.

C)

no buyer or seller can influence the market price.

D)

there is apt to be a shortage of sellers of output.

34)

At the short–run break–even point, the perfectly competitive firm is

34)

A)

earning positive economic profits.

B)

earning zero economic profits.

C)

just covering its total variable costs.

D)

earning negative economic profits.

35)

The firm in the above figure breaks even when market price is

35)

A)

E.

B)

H.

C)

I.

D)

G.

36)

In a perfectly competitive market, if P > ATC in the short run, there is apt to be

36)

A)

an inward shift in the industry supply curve.

B)

an upward pressure on price.

C)

an accounting loss for existing firms.

D)

entry of new firms into the market.

D

37)

A firm that has positive economic profits has accounting profits that are

37)

A)

zero.

B)

positive.

C)

negative.

D)

indeterminate without more information.

B

B

38)

Refer to the above table. The table represents information on the costs for Ajax Corporation. Ajax

operates in a perfectly competitive market and the price of the product is $7. What will be the value

of total revenue when quantity sold equals 2?

38)

A)

$14

B)

$7

C)

$21

D)

$16

39)

In a decreasing–cost industry, an increase in output will lead to

39)

A)

a reduction in long–run per–unit costs.

B)

an upward shift in the ATC curve.

C)

an increase in long–run per–unit costs.

D)

an upward shift in the MC curve.

40)

In the above figure, if the market price is $10, the firm

40)

A)

produces 11 units.

B)

produces 10 units.

C)

produces 12 units.

D)

shuts down operations.

41)

The short–run supply curve for the perfectly competitive firm is the portion of its

41)

A)

MC curve above the MR curve.

B)

MC curve above the AFC curve.

C)

MC curve above the AVC curve.

D)

MC curve above the ATC curve.

42)

The demand curve for a perfectly competitive industry is

42)

A)

unit elastic.

B)

perfectly elastic.

C)

perfectly inelastic.

D)

downward sloping.

43)

In the short run, the perfectly competitive firm will always earn an economic profit when

43)

A)

P > ATC.

B)

P > AVC.

C)

P = ATC.

D)

P = MC.

44)

A perfectly competitive firm faces a market clearing price of $150 per unit. Average variable costs

are at the minimum value of $200 per unit at an output rate of 100 units. Marginal cost equals $150

per unit at an output rate of 75 units. It can be concluded that the short–run profit–maximizing

output rate is

44)

A)

75 units, at which the firm earns zero economic profits per unit sold.

B)

100 units, because marginal cost equals average variable costs.

C)

75 units, at which the firm earns $50 in economic profits per unit sold.

D)

0 units, because price is less than average variable costs.

45)

Refer to the above table. If the price is $6, the perfectly competitive firm should produce

45)

A)

107 units.

B)

104 units.

C)

105 units.

D)

106 units.

46)

Refer to the above figure. The competitive firm’s short run supply curve

46)

A)

starts at A and goes along the AVC curve as quantity increases.

B)

starts at A and goes along the MC curve as quantity increases.

C)

starts at B and goes along the ATC curve as quantity increases.

D)

starts at B and goes along the MC curve as quantity increases.

47)

If marginal revenue is greater than marginal cost, the firm should

47)

A)

decrease its rate of output.

B)

raise price.

C)

raise marginal revenue.

D)

increase its rate of output.

48)

A constant–cost industry is one in which

48)

A)

each firm has a horizontal long–run average cost curve.

B)

the marginal product of labor is constant.

C)

there is no change in long–run per–unit costs, even as output varies.

D)

output increases lead to productivity gains.

49)

Profits and losses are true signals because they

49)

A)

reward people who make profits with even more profits and punish those who make losses

with even more losses.

B)

convey information about where to place resources and reward people who act on the

information.

C)

convey information about true long–run profits.

D)

cannot be misinterpreted by entrepreneurs.

50)

Each firm in a perfectly competitive industry is

50)

A)

relatively large.

B)

a price setter.

C)

producing a unique product.

D)

a price taker.

51)

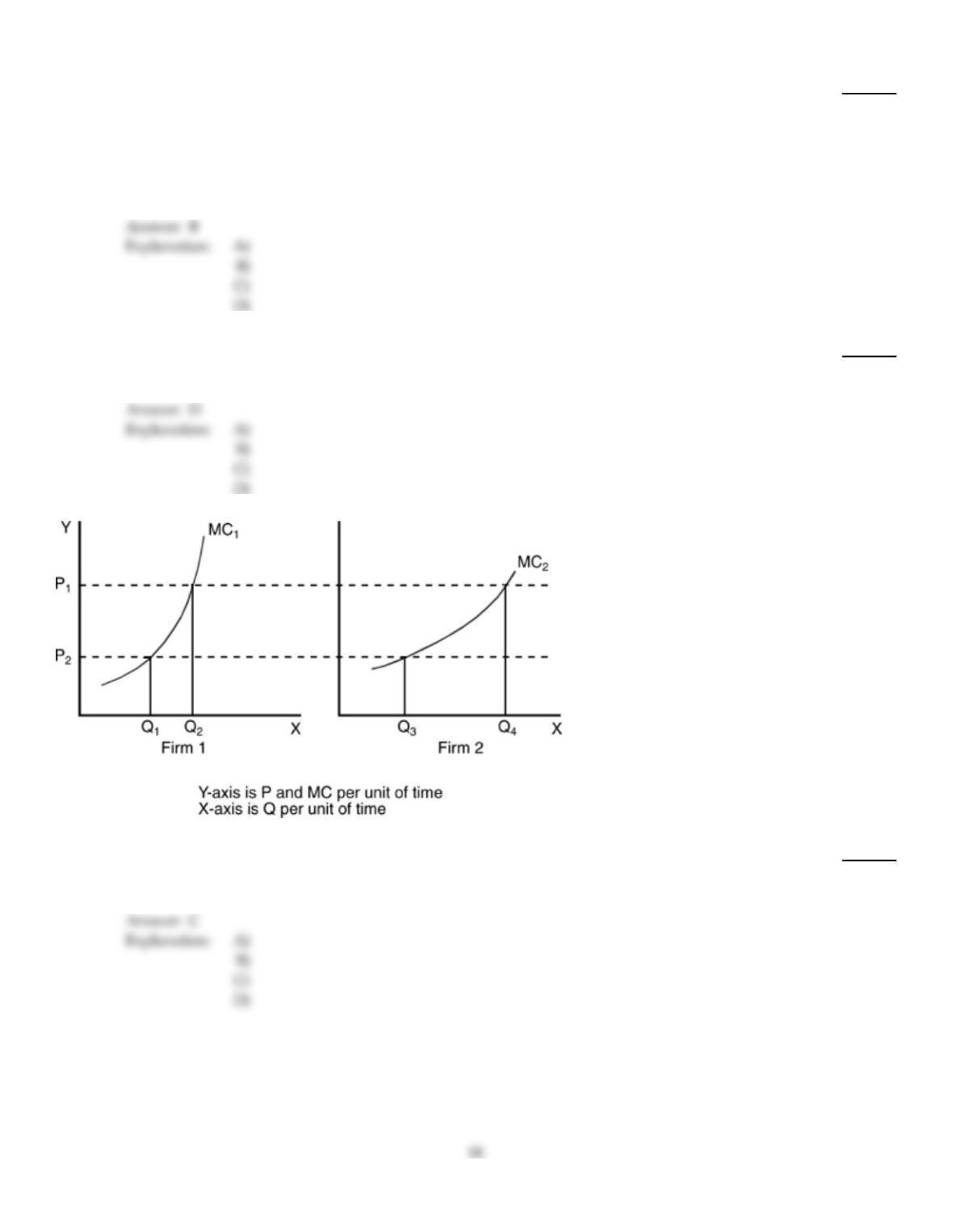

In the above figure, assuming Firm 1 and Firm 2 are the sole producers in the industry, the industry

quantity supplied at price P2 is equal to

51)

A)

Q2+ Q4.

B)

Q4– Q2.

C)

Q1+ Q3.

D)

Q1+ Q2.