Chapter 22 – Performance Management and Evaluation

TRUE/FALSE

1. The balanced scorecard links the perspectives of an organization’s stakeholders with the organization’s

mission and vision, performance measures, strategic plan, and resources.

2. An organization’s four basic stakeholder groups include investors, employees, external business

processes, and customers.

3. To succeed, an organization must add value for all of its stakeholders in the long term only.

4. The alignment of an organization’s strategy with all the perspectives of the balanced scorecard results

in performance objectives that benefit all stakeholders.

5. It is not necessary for managers to fully understand the causal relationship between their actions and

the organization’s overall performance to get results.

6. A performance management and evaluation system is mainly utilized to account for and report on

financial performance.

7. A performance management and evaluation system allows a company to identify how well it is doing,

where it is going, and what improvements will make it more profitable.

8. What is being measured by managers is the same as the actual measures used to monitor performance.

9. Performance measurement is the use of both quantitative and qualitative tools to gauge an

organization’s performance in relation to a specific goal or an expected outcome.

10. Most organizations use very similar performance measures in their day–to-day business operations.

11. When developing performance measures, management must consider a number of different issues

besides what to measure and how to measure.

12. Managers at all levels are evaluated in terms of their ability to manage their areas of responsibility in

keeping with organizational goals.

13. Responsibility accounting is more concerned with performance evaluation than performance

management.

14. Manufacturing companies rarely utilize responsibility accounting.

15. A responsibility center whose manager is held accountable for both revenues and costs and for the

resulting operating income is called a profit center.

16. An organization chart assists in management control.

17. A report for a responsibility center includes costs and revenues that are both controllable and

uncontrollable by a manager.

18. Performance reports allow comparisons between actual performance and budget expectations.

19. If a performance report contains items that are out of a manager’s control, the entire responsibility

accounting system can be called into question.

20. Both flexible budgeting and variable costing can be utilized to evaluate cost center performance.

21. A flexible budget is derived by multiplying actual unit output by the standard unit costs.

22. Variable costing is a method of reporting that deals only with a manager’s controllable, variable costs.

23. A variable costing income statement is essentially the same as a traditional income statement.

24. In evaluating investment center performance, ROI proves to be such a comprehensive performance

measure that other performance measures are rarely needed.

25. Residual income is the amount of profit left after subtracting expenses of a particular investment

center.

26. When calculating ROI, assets invested represent the average of the beginning and ending asset

balances for a given period.

27. ROI is a performance measure mainly connected with a company’s income statement.

28. Like ROI, residual income is a performance measure displayed as a ratio.

29. For residual income figures to be comparable on a companywide basis, all investment centers must

have equal access to resources and similar asset investment bases.

30. ROI, residual income, and economic value added all represent performance measures that can be

utilized to determine investment center performance.

31. Economic value added is synonymous with shareholder wealth created by an investment center.

32. Cost of capital is the maximum desired rate of return on a particular investment.

33. The equation for economic value added includes pretax operating income as well as current liabilities.

34. A manager can improve the economic value of an investment center by decreasing assets.

35. The economic value added performance measure focuses on long-term financial performance.

36. How effective a performance management and evaluation system is depends on how well the goals of

the entire company are coordinated rather than on how well the goals of individual responsibility

centers and managers are coordinated.

37. The logical linking of goals to measurable objectives and targets and the tying of appropriate

compensation incentives to the achievement of such objectives and targets are critical to the successful

coordination of goals.

38. Tying compensation incentives to performance targets decreases the likelihood that the goals of

responsibility centers, managers, and the entire organization will be well coordinated.

39. Employer-provided health insurance is a common type of incentive compensation.

40. Incentive awards are utilized mainly to encourage long-term performance.

41. The causal links between an organization’s goals, objectives, measures, performance targets need not

be apparent.

MULTIPLE CHOICE

1. The balanced scorecard was developed by

a.

Robert S. Kaplan.

b.

David R. Norton.

c.

David R. Norton and Robert S. Princeton.

d.

Robert S. Kaplan and David R. Norton.

2. Which of the following represents a basic stakeholder of an organization?

a.

The account receivable clerk of the organization

b.

A vice president of the organization

c.

A line supervisor of the organization

d.

All of these choices

3. By balancing all stakeholders’ needs, managers are more likely to achieve their objectives in

a.

the long term.

b.

the short term.

c.

the short term as well as the long term.

d.

all areas of the organization.

4. One of the overall goals of the Pancake House Restaurant is customer satisfaction. In the light of that

goal, match the learning and growth perspective with the appropriate objective.

a.

Customer satisfaction means that the chefs engage in culinary continuing education.

b.

Customer satisfaction means that customers receive their food within 10 minutes of

placing an order.

c.

Customer satisfaction means that the customer appreciation program is successful.

d.

Customer satisfaction means that the restaurant is profitable.

5. One of the overall goals of the Pancake House Restaurant is customer satisfaction. In the light of that

goal, match the internal business processes perspective with the appropriate objective.

a.

Customer satisfaction means that the chefs engage in culinary continuing education.

b.

Customer satisfaction means that customers receive their food within 10 minutes of

placing an order.

c.

Customer satisfaction means that the customer appreciation program is successful.

d.

Customer satisfaction means that the restaurant is profitable.

6. The balanced scorecard links the perspectives of an organization’s stakeholders with the organization’s

a.

goals and vision, performance goals, strategic plan, and financial resources.

b.

mission and overall plan, performance measures, departmental plans, and resources.

c.

mission and vision, performance measures, strategic plan, and resources.

d.

mission and vision, performance goals, overall plan, and resources.

7. A performance management and evaluation system is a set of procedures that account for and report on

a.

qualitative performance.

b.

quantitative performance.

c.

employee performance.

d.

quantitative and qualitative performance.

8. The use of quantitative tools to gauge an organization’s performance in relation to a specific goal or an

expected outcome is known as

a.

responsibility accounting.

b.

an asset turnover.

c.

a performance management and evaluation system.

d.

a performance measurement.

9. Which of the following is an example of a performance measurement?

a.

Product quality

b.

Number of customer complaints

c.

Customer satisfaction

d.

All of these choices

10. In developing performance measures, management must consider which of the following?

a.

How should we measure?

b.

How can managers monitor financial performance?

c.

What should we measure?

d.

All of these choices

11. A performance management and evaluation system is utilized so that a company can identify which of

the following?

a.

How well it is doing and where it is going

b.

How satisfied investors are with their return on investment

c.

How satisfied both customers and employees are

d.

How well it is doing, where it is going, and what improvements will bring in more profit

12. The manager of Center A is responsible for generating cash inflows and incurring costs with the goal

of making money for the company. The manager has no responsibility for assets. What type of

responsibility center is Center A?

a.

Cost center

b.

Discretionary cost center

c.

Profit center

d.

Revenue center

13. The manager of Center B produces a product that is not sold to an external party. What type of

responsibility center is Center B?

a.

Cost center

b.

Discretionary cost center

c.

Profit center

d.

Revenue center

14. The manager of Center C is responsible for the online order operations of a large retailer. What type of

responsibility center is Center C?

a.

Discretionary cost center

b.

Profit center

c.

Revenue center

d.

Investment center

15. The manager of Center D designs, produces, and sells products to external parties. The manager makes

both long-term and short-term decisions. What type of responsibility center is Center D?

a.

Cost center

b.

Profit center

c.

Revenue center

d.

Investment center

16. The manager of Center E provides human resource support for the other centers in the company. What

type of responsibility center is Center E?

a.

Cost center

b.

Discretionary cost center

c.

Revenue center

d.

Investment center

17. Many organizations utilize responsibility accounting

a.

to assist in building performance measures for the organization.

b.

to assist in performance management and evaluation.

c.

solely to evaluate how well employees are handling their responsibilities.

d.

as an alternative to generally accepted accounting principles.

18. How many different types of responsibility centers exist?

a.

2

b.

5

c.

10

d.

3

19. The way in which the performance of a cost center is evaluated is similar to

a.

job order costing.

b.

standard costing.

c.

process costing.

d.

none of these choices.

20. A responsibility center in which the relationship between resources and products or services produced

is not well defined is known as a(n)

a.

investment center.

b.

profit center.

c.

cost center.

d.

discretionary cost center.

21. A good example of a profit center would be

a.

a car manufacturer’s assembly line.

b.

a local Home Depot store.

c.

Avis Car Rental’s national reservation center.

d.

a manufacturer’s human resources department.

22. A responsibility accounting system ensures that

a.

generally accepted accounting principles reporting requirements are met.

b.

managers will not be held responsible for items they cannot change.

c.

99 percent of businesses utilizing such a system will be profitable.

d.

easy correlations between revenues and costs can be drawn.

23. Performance reports should include

a.

controllable costs and revenues for a specific responsibility center.

b.

all costs, revenues, and resources for a specific responsibility center.

c.

controllable costs for a specific responsibility center.

d.

controllable costs, revenues, and resources for a specific responsibility center.

24. Standard costing would most often require which type of performance evaluation?

a.

Flexible budgeting

b.

Zero-based budgeting

c.

Variable costing

d.

Any of these choices

25. Variable costing allows a manager to classify controllable costs as

a.

either variable or fixed.

b.

variable only.

c.

fixed only.

d.

either short-term variable or long-term variable.

26. A variable costing income statement is the same as

a.

a contribution margin income statement.

b.

a traditional income statement.

c.

a cost-volume-profit income statement.

d.

none of these choices.

27. Variable costing is utilized to evaluate the performance of

a.

investment centers.

b.

revenue centers.

c.

discretionary cost centers.

d.

profit centers.

28. How is the contribution margin calculated when utilizing variable costing?

a.

Sales less variable cost of goods sold

b.

Sales less variable cost of goods sold, less variable selling and administrative expenses

c.

Sales less cost of goods sold

d.

Sales less variable cost of goods sold, less variable selling and administrative expenses,

less fixed cost of goods sold, less fixed selling and administrative expenses

29. Dana Klammer is the manager of the Cutting Department in the Northwest Division of Steel Products.

Which of the following costs is a controllable cost?

a.

Salaries of cutting machine workers

b.

Cost of electricity for the Northwest Division

c.

Lumber Department hauling costs

d.

Vice president’s salary

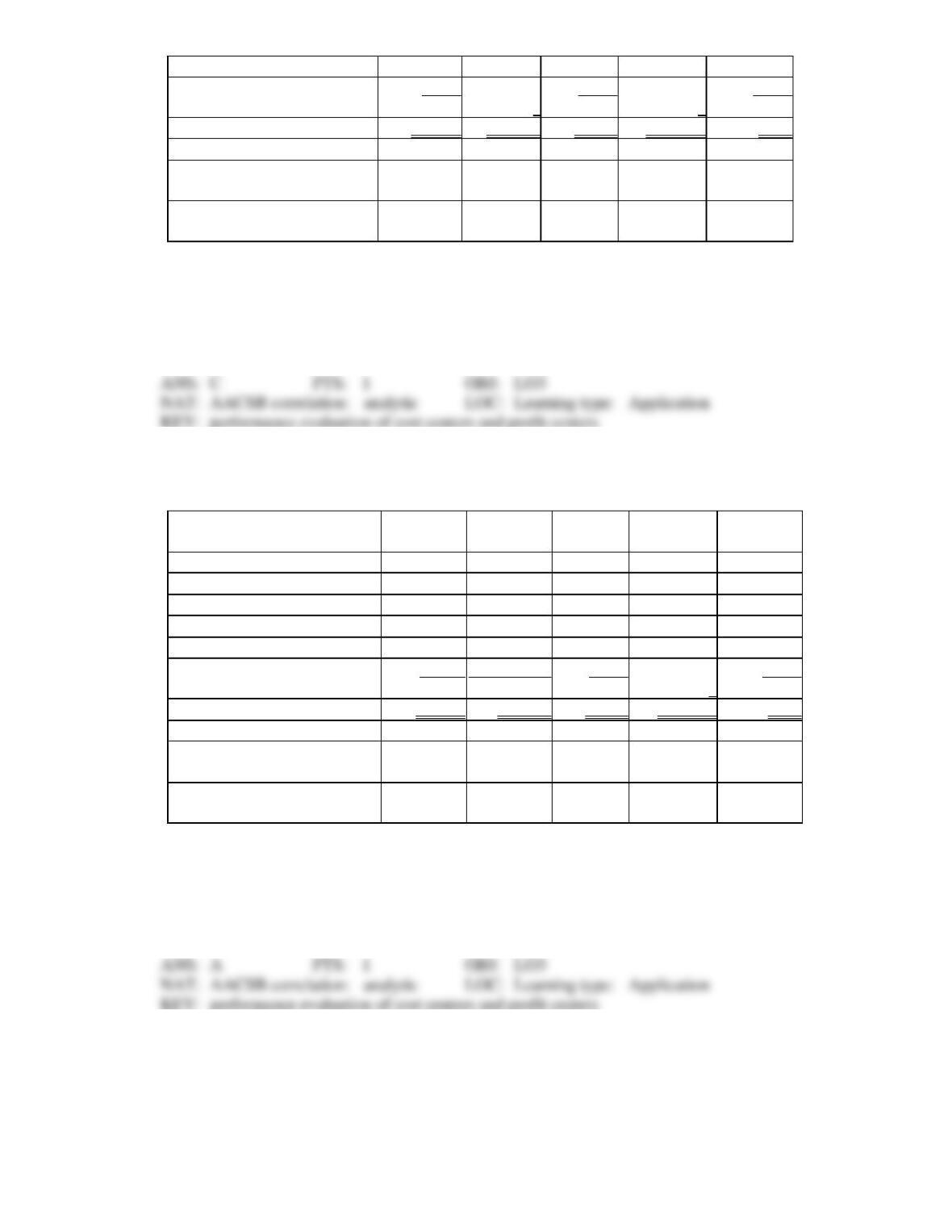

30. Use the following performance report for a cost center of the Dry Cat Food Division for the month

ended December 31 to answer the question below.

Actual

Results

Variance

Flexible

Budget

Variance

Master

Budget

Units produced

70

0

?

30 (U)

100

Center costs

Direct materials

$ 84

$ ?

$ 70

$ ?

$100

Direct labor

150

?

?

60 (F)

200

Variable overhead

?

20 (U)

210

?

300

Fixed overhead

280

?

250

?

250

Total cost

$ ?

$74 (U)

$ ?

$255 (F)

$850

Performance measures

Defect-free units to total

produced

80%

?

N/A

N/A

90%

Average throughput

time per unit

12 minutes

?

N/A

N/A

10 minutes

The flexible budget is based on how many units produced?

a.

0 units

b.

30 units

c.

70 units

d.

100 units

31. Use the following performance report for a cost center of the Dry Cat Food Division for the month

ended December 31 to answer the question below.

Actual

Results

Variance

Flexible

Budget

Variance

Master

Budget

Units produced

70

0

?

30 (U)

100

Center costs

Direct materials

$ 84

$ ?

$ 70

$ ?

$100

Direct labor

150

?

?

60 (F)

200

Variable overhead

?

20 (U)

210

?

300

Fixed overhead

280

?

250

?

250

Total cost

$ ?

$74 (U)

$ ?

$255 (F)

$850

Performance measures

Defect-free units to total

produced

80%

?

N/A

N/A

90%

Average throughput

time per unit

12 minutes

?

N/A

N/A

10 minutes

What is the direct materials variance between the actual results and the flexible budget?

a.

$14 (U)

b.

$14 (F)

c.

$30 (U)

d.

$30 (F)

32. Use the following performance report for a cost center of the Dry Cat Food Division for the month

ended December 31 to answer the question below.

Actual

Results

Variance

Flexible

Budget

Variance

Master

Budget

Units produced

70

0

?

30 (U)

100

Center costs

Direct materials

$ 84

$ ?

$ 70

$

?

$100

Direct labor

150

?

?

60 (F)

200

Variable overhead

?

20 (U)

210

?

300

Fixed overhead

280

?

250

?

250

Total cost

$ ?

$74 (U)

$ ?

$255 (F)

$850

Performance measures

Defect-free units to total

produced

80%

?

N/A

N/A

90%

Average throughput

time per unit

12 minutes

?

N/A

N/A

10 minutes

What is the actual total cost?

a.

$521

b.

$595

c.

$744

d.

$1,031

33. Use the following performance report for a cost center of the Dry Cat Food Division for the month

ended December 31 to answer the question below.

Actual

Results

Variance

Flexible

Budget

Variance

Master

Budget

Units produced

70

0

?

30 (U)

100

Center costs

Direct materials

$ 84

$ ?

$ 70

$ ?

$100

Direct labor

150

?

?

60 (F)

200

Variable overhead

?

20 (U)

210

?

300

Fixed overhead

280

?

250

?

250

Total cost

$ ?

$74 (U)

$ ?

$255 (F)

$850

Performance measures

Defect-free units to total

produced

80%

?

N/A

N/A

90%

Average throughput

time per unit

12 minutes

?

N/A

N/A

10 minutes

What is the direct labor variance between the actual results and the flexible budget?

a.

$10 (U)

b.

$10 (F)

c.

$60 (U)

d.

$60 (F)

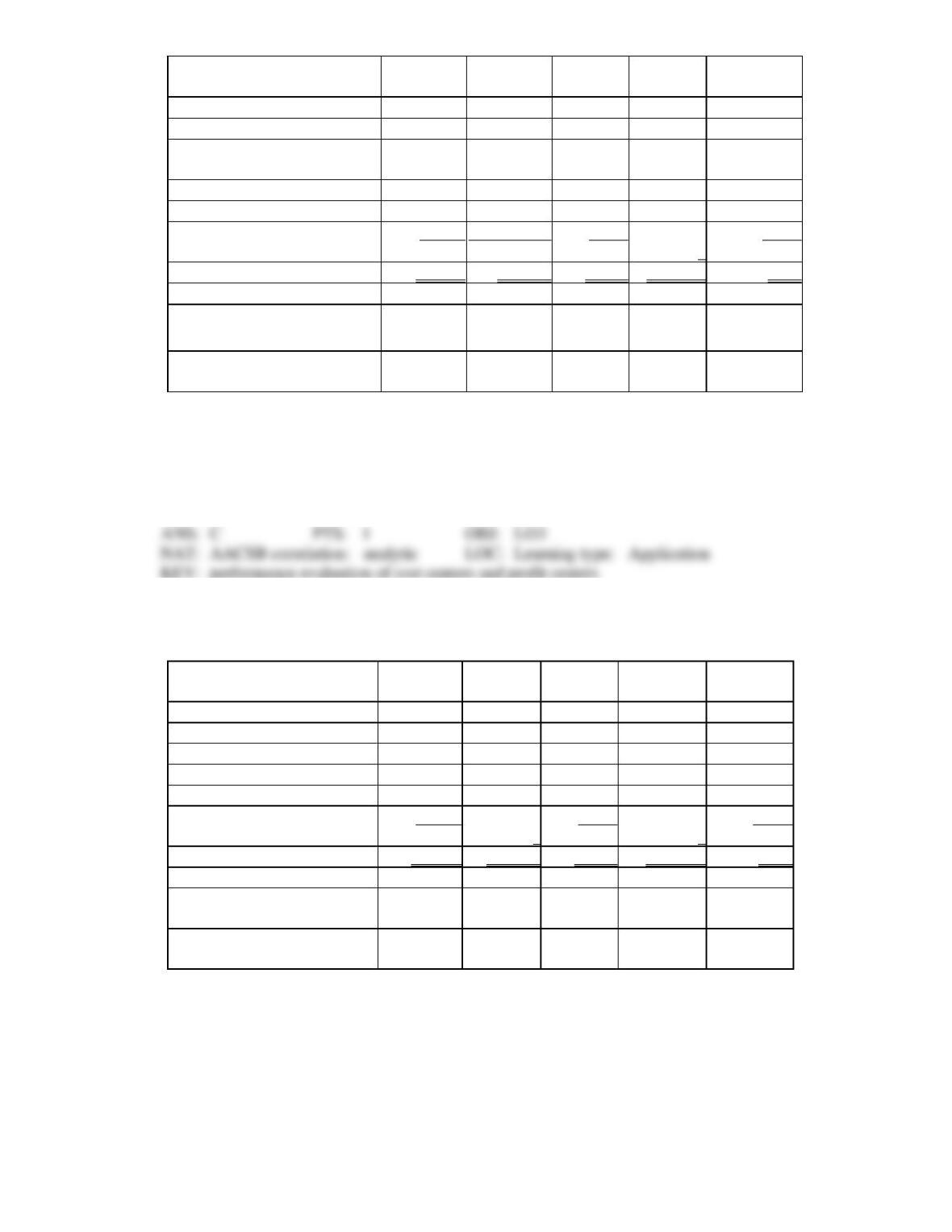

34. Use the following performance report for a profit center of the Wet Cat Food Company for the month

ended December 31 to answer the question below.

Actual

Results

Variance

Master

Budget

Sales

$ ?

$20 (F)

$ 200

Controllable variable costs

Variable cost of goods sold

$ 125

$10 (U)

$ ?

Variable selling and administrative

expenses

15

?

5

Contribution margin

$ 80

$ ?

$ 80

Controllable fixed costs

?

10 (F)

60

Profit center income

$ ?

$10 (F)

$ ?

Performance measures

Number of orders processed

50

20 (F)

?

Average daily sales

$?

0.66 (F)

$4.00

Number of units sold

100

40 (F)

?

What were the actual sales?

a.

$180

b.

$200

c.

$220

d.

$240

35. Use the following performance report for a profit center of the Wet Cat Food Company for the month

ended December 31 to answer the question below.

Actual

Results

Variance

Master

Budget

Sales

$ ?

$20 (F)

$ 200

Controllable variable costs

Variable cost of goods sold

$ 125

$10 (U)

$ ?

Variable selling and administrative

expenses

15

?

5

Contribution margin

$ 80

$ ?

$ 80

Controllable fixed costs

?

10 (F)

60

Profit center income

$ ?

$10 (F)

$ ?

Performance measures

Number of orders processed

50

20 (F)

?

Average daily sales

$?

0.66 (F)

$4.00

Number of units sold

100

40 (F)

?

What was the actual profit center income?

a.

$10

b.

$20