93. The supply curve of a price-taker firm in the short run is the

a.

firm’s average variable cost curve.

b.

portion of the firm’s average total cost curve that lies above average variable cost curve.

c.

portion of the firm’s marginal cost curve that lies above average variable cost curve.

d.

firm’s marginal revenue curve.

94. In a price-taker market, the short-run market supply curve is the

a.

vertical sum of the marginal cost curves of all firms in the market.

b.

vertical sum of the average variable cost curves of all firms.

c.

horizontal sum of the marginal cost curves of all firms so long as price exceeds average

variable cost.

d.

horizontal sum of the average total cost curves of all the firms in the market so long as

average total cost exceeds the market price.

95. A competitive price-taker firm would be willing to remain in the industry in the long run at zero

economic profit because

a.

it would find it too difficult to exit from the industry in the long run.

b.

accounting profit would be negative.

c.

it is covering all costs, including the opportunity cost of capital and labor.

d.

its sunk costs would prevent it from leaving the industry.

96. The market for a competitive price-taker market clears at a price of $3, and the minimum average cost

for all firms is $2.50. In the long run, we would expect an increase in

a.

each firm’s output.

b.

the number of firms.

c.

each firm’s profit.

d.

each firm’s average cost.

97. Regardless of quantity in long-run equilibrium, the competitive price-taker market price cannot exceed

the

a.

long-run average cost of supplying that quantity.

b.

total variable cost of supplying that quantity.

c.

long-run total cost of supplying that quantity.

d.

minimum long-run marginal cost of supplying that quantity.

98. A competitive price-taker market in long-run equilibrium is described as efficient because firms

a.

produce at the low point on their average cost curve.

b.

produce where marginal cost yields a profit.

c.

earn no more than the cost of capital.

d.

are not profitable.

99. When new firms have an incentive to enter a competitive price-taker market, their entry will

a.

increase the price of the product.

b.

drive down profits of existing firms in the market.

c.

shift the market supply curve to the left.

d.

increase demand for the product.

100. When firms have an incentive to exit a competitive price-taker market, their exit will

a.

lower market price.

b.

necessarily raise the costs of firms that remain in the market.

c.

raise profits for firms that remain in the market.

d.

reduce demand for the product.

101. When new firms enter a competitive price-taker market,

a.

economic profits of existing firms will continue to be zero.

b.

entering firms will earn zero economic profit upon entry into the market.

c.

existing firms may see their costs rise as more firms compete for limited resources.

d.

prices will rise as existing firms raise prices to keep new firms out of the market.

102. The entry of new firms into a competitive market will

a.

increase market supply and increase market prices.

b.

increase market supply and decrease market prices.

c.

decrease market supply and increase market prices.

d.

decrease market supply and decrease market prices.

103. The exit of existing firms from a competitive market will

a.

increase market supply and increase market prices.

b.

increase market supply and decrease market prices.

c.

decrease market supply and increase market prices.

d.

decrease market supply and decrease market prices.

104. The motivating force behind an increase in supply in a long-run adjustment to equilibrium is

a.

lower prices.

b.

economic profits that are present in the short run.

c.

higher profit expectations among owners of firms in the industry, triggered by increased

prices.

d.

normal profits witnessed by individuals outside the industry that trigger entry.

e.

the decreases in average cost that can be obtained through economies of scale.

105. If a competitive price-taking firm is operating in long-run equilibrium and market demand suddenly

falls, the short-run result will be

a.

greater economic profit.

b.

a normal profit.

c.

lower average total cost.

d.

lower average variable cost.

e.

economic losses.

106. When a firm in a price-taker industry is in long-run equilibrium, the market price equals

a.

marginal cost but may be greater or less than average total cost.

b.

both average total cost and marginal cost.

c.

average total cost but may be greater or less than marginal cost.

d.

marginal revenue but may be greater or less than both average total cost and marginal cost.

107. If long-run equilibrium is present in a competitive market, the typical firm in the market will be

a.

making economic losses.

b.

making zero economic profit.

c.

making economic profit.

d.

making a rate of return that is higher than the rate earned in other industries.

e.

both c and d are correct.

108. When entry barriers into a market are low, firms will tend to earn zero economic profit in the long run

because

a.

low entry barriers lead to rising costs.

b.

profit-seeking entrepreneurs will not enter a market when entry barriers are low.

c.

short-run profit attracts additional suppliers and drives down the market price.

d.

consumers will refuse to pay more than the cost of producing a good once they find out the

producer’s per-unit costs.

109. If a price-taker industry is in long-run equilibrium, the market price in the industry will be just

sufficient to cover the firm’s average

a.

total costs.

b.

fixed costs.

c.

variable costs.

d.

variable costs plus a 10 percent accounting profit.

110. Which of the following conditions will be present when a price-taker market is in long-run

equilibrium?

a.

Price will exceed marginal revenue.

b.

Firms will earn economic profit.

c.

Marginal revenue will exceed marginal cost.

d.

Average total cost will be at a minimum.

111. There are 1,000 identical firms in a price-taker industry. In the short run, total revenues of each firm

exceed total costs. What will happen in the long run?

a.

Nothing, because each firm is already maximizing its profits.

b.

Many firms will enter the market and each firm will eventually operate at a loss.

c.

Additional firms will enter the market, and price will be driven down to where each firm

will be making just enough to stay in business.

d.

Additional firms will enter the market, but the price will remain the same because the

existing firms will not allow price to decrease.

112. There are 1,000 identical firms in a price-taker industry. In the short run, the total revenues of each

firm are less than total costs. What will happen in the long run?

a.

Nothing, because each firm is already maximizing its profits.

b.

Additional firms will enter the market, and price will be driven down to where each firm

will be making just enough to stay in business (cover its variable costs).

c.

Additional firms will enter the market, but the price will remain the same because the

existing firms will not allow it to decrease.

d.

Firms will exit the market, and the product price will rise.

113. In the long run, in a price-taker market, the price of a good is determined primarily by the

a.

average total cost of producing it.

b.

decision of buyers in determining how much they are willing to pay for the good.

c.

elasticity of supply.

d.

number of firms in the industry.

114. Suppose sharply higher coffee prices lead to an increase in demand for tea. As tea prices increase, tea

producers experience short-run economic profits. If the tea industry is a price-taker industry and if

sufficient time is allowed for the market to adjust fully to the increase in demand for tea, one would

expect the tea industry’s output to

a.

increase, and economic profits to increase as well.

b.

increase, and economic profits to disappear.

c.

decline, and economic profits to increase.

d.

decline, and economic profits to disappear.

115. Several producers in industry A developed an improved technology that reduces the quantity of

resources used to produce a given output. Which of the following would be expected?

a.

The per-unit costs of production of the firms adopting the technology would increase.

b.

In the short run, economic profits would be earned by the earliest firms adopting the

technology.

c.

Product price would immediately fall to the minimum average total cost of the firms

quickly adopting the technology, thus retarding the rate at which firms enter the industry.

d.

Producers who adopt the technology will have short-run economic losses.

116. Suppose the demand for large (and therefore high-gasoline consumption) cars decreases sharply during

an energy crisis. The most likely market adjustment would be

a.

a sharp rise in the price of large cars in the short run as people rush to purchase these

vehicles before producers cut back on manufacturing them.

b.

a moderate increase in short-run prices, followed by a larger long-run price increase as the

supply of large cars is depleted.

c.

lower short-run prices, which will lead to an expansion in the number of large cars sold.

d.

a decrease in the price of large cars in the short run, leading to a reduction in output, which

will moderate the price decline in the long run.

117. Suppose that sharply lower coffee prices lead to a decrease in the demand for tea. Tea price decreases,

and the tea producers experience short-run economic losses. If the tea industry is a price-taker market,

after sufficient time is allowed for the market to adjust fully to the decrease in the demand for tea, one

would expect the tea industry’s output to

a.

increase and economic losses to persist.

b.

decline and economic losses to persist.

c.

decline and economic losses to disappear.

d.

increase and economic losses to disappear

118. If the ice cream industry is a competitive price-taker market and all ice cream producers are earning

zero economic profit, what will be the impact of an increase in the demand for ice cream?

a.

Firms will exit the ice cream industry in the long run since they are earning zero economic

profit.

b.

The firms will now be able to earn long-run economic profit assuming that barriers to

entry remain low and new firms can enter the market.

c.

A shortage of ice cream will develop.

d.

The price of ice cream will rise initially, inducing the existing firms to expand output and

new firms to enter the industry.

119. Other things constant, if wheat production is a price-taker industry, a decrease in the price of fertilizer

used to grow wheat will

a.

increase the supply of wheat.

b.

increase the demand for wheat.

c.

decrease the supply of wheat.

d.

do both a and b.

120. If factor prices rise as demand increases and the firms expand output, the long-run market supply curve

will be upward sloping. In terms of economics, this describes

a.

an oligopolistic industry.

b.

a constant cost industry.

c.

an increasing cost industry.

d.

a decreasing cost industry.

121. The textile industry is composed of a large number of small firms. In recent years, these firms have

suffered economic losses, and many sellers have left the industry. Economic theory suggests that if

technology, imports, and other factors remain constant, these conditions will

a.

shift the market demand curve outward so that price will rise to the level of production

cost.

b.

cause the remaining firms to collude so they can produce more efficiently.

c.

cause the market supply to decline and the price of textiles to rise.

d.

cause firms in the textile industry to suffer long-run economic losses.

122. If a decrease in the demand for corn leads to economic losses for corn farmers,

a.

some existing corn farmers will exit the industry.

b.

the price of corn will remain low in the long run due to the economic losses.

c.

the suppliers of corn will suffer long-run economic losses.

d.

all of the above are correct.

123. In a constant cost industry,

a.

a natural monopoly is likely to occur.

b.

total cost is the same, no matter how much a firm produces.

c.

the long-run supply curve will be perfectly elastic.

d.

entry of new firms in the industry will lead to a reduction in the cost of inputs.

124. In a constant-cost industry, an increase in output that increases the demand for resources used by the

industry

a.

is likely to result in higher prices for at least some resources.

b.

causes the firm’s cost curves to shift downward.

c.

causes the demand curve for the industry to rise.

d.

is not likely to result in higher prices for resources.

125. A perfectly elastic, long-run market supply curve is most likely to be achieved in

a.

a price-taker industry.

b.

a constant cost industry.

c.

an increasing cost industry.

d.

a price searcher industry.

126. If the expansion of output in an industry leads to unchanged resource prices, the industry is most likely

to be

a.

a decreasing cost industry.

b.

an increasing cost industry.

c.

a constant cost industry.

d.

an industry characterized by economies of scale.

127. Which of the following is true for a constant cost industry?

a.

The total cost of producing 500 units will be the same as the total cost of producing 250

units.

b.

If 100 units can be produced for $500, then 200 units can be produced for $1,000.

c.

The demand curve and, therefore, the unit price in the industry are constant.

d.

Firms in the industry will hold output constant if the price of the product increases.

128. If a product is manufactured under conditions of constant cost, an increase in the demand for the

product will increase

a.

both equilibrium quantity and equilibrium price in the long run.

b.

equilibrium price, but equilibrium quantity will be unchanged in the long run.

c.

equilibrium price but reduce equilibrium quantity in the long run.

d.

equilibrium quantity, but equilibrium price will be unchanged in the long run.

129. If a product is manufactured under conditions of constant cost, an increase in the demand for the

product will increase

a.

both equilibrium quantity and equilibrium price in the long run.

b.

equilibrium price, but equilibrium quantity will be unchanged in the long run.

c.

equilibrium quantity, but equilibrium price will be unchanged in the long run.

d.

equilibrium quantity but reduce equilibrium price in the long run.

130. Suppose the demand curve for aluminum cans is downward sloping, and the cans are produced in a

constant cost industry where the firms are price takers. A $.25-per-can tax is levied on aluminum cans.

How much will the price of aluminum cans increase in the short run and the long run?

a.

short run, $.25; long run, more than $.25

b.

short run, less than $.25; long run, $.25

c.

short run, less than $.25; long run, more than $.25

d.

short run, $.25; long run, less than $.25

131. If resource prices rise and the average total cost of producing a product increases as the firms in an

industry expand output in response to an increase in demand, the long-run market supply curve for the

product will

a.

be perfectly elastic (a horizontal line).

b.

be perfectly inelastic (a vertical line).

c.

slope upward to the right.

d.

be more inelastic than the short-run supply curve for the product.

132. If the demand for a product increases in an increasing cost industry, as the market adjusts in the long

run,

a.

price will rise.

b.

the firm’s per-unit costs will increase.

c.

the firm’s per-unit costs will fall.

d.

the market price will return to its initial position.

133. Why will the long-run market supply curve for most products slope upward to the right?

a.

The firms producing the product will be unable to expand the size of their plant and

equipment in the long run.

b.

Economies of scale are present in most industries.

c.

Most products are produced under conditions of constant cost.

d.

Resource prices will rise and push costs upward as the output of the industry expands.

134. Suppose antitheft auto alarms are produced in a price-taker market that is initially in long-run

equilibrium. It is estimated that only 23 percent of all autos have alarms. Due to rising auto theft,

Congress mandates alarms in every vehicle. Assume complete compliance. If the industry is an

increasing cost industry, price will

a.

increase in both the short run and long run.

b.

decrease in both the short run and long run.

c.

increase in the short run but not in the long run.

d.

decrease in the short run but not in the long run.

135. The long-run supply curve for a product differs from the short-run supply curve in that the long-run

supply curve is usually

a.

vertical.

b.

more inelastic.

c.

more elastic.

d.

of unitary elasticity.

136. As the period for firms to expand output is lengthened, the elasticity of the market supply curve will

a.

approach zero.

b.

increase.

c.

decrease.

d.

remain the same since time does not affect the elasticity of market supply.

137. Which of the following is a residual reward that accrues to business decision makers who use

resources so as to increase their value?

a.

opportunity cost

b.

earnings of employees

c.

economic profit

d.

interest earnings of corporate bondholders

138. In a price-taker market, profits are

a.

the result of consumers being charged arbitrarily high prices.

b.

a reward for creating value.

c.

the result of barriers to entry into the market.

d.

a signal that fewer resources are needed in a market.

139. When profits occur in a competitive market, this indicates that

a.

consumers value the goods more than the resources used to produce them.

b.

producers value the goods more than the resources used to produce them.

c.

producers value the goods more than consumers value the goods.

d.

consumers value the goods less than the resources used to produce them.

140. When a firm in a competitive market is earning profits, this indicates that the firm is

a.

exploiting consumers.

b.

increasing the value of resources.

c.

blocking the entry of competing firms.

d.

reducing overall wealth in the market.

141. Suppose the development of new drought-resistant hybrid seed corn leads to a 50-percent increase in

the average yield per acre without increasing the cost to the farmers who use the new technology. If

the conditions in the corn production industry are approximated by the price-taker model, which of the

following is most likely to occur?

a.

The price of corn will increase.

b.

The price of soybeans (a substitute for corn) will increase.

c.

The profits of corn farmers who quickly adopt the new technology will increase.

d.

The profits of corn farmers who do not adopt the new technology will increase.

142. The owners of a firm are earning economic profit if

a.

return on their capital is lower than the opportunity cost of employing that capital in their

industry.

b.

their total revenues exceed the monetary payments to labor and other resources in the long

run after all plant size adjustments are made.

c.

price exceeds average variable costs at the shutdown point.

d.

they are earning a return on their capital that is higher than what can generally be earned in

other markets.

143. Suppose a typical firm in a particular industry is making positive economic profits. These economic

profits

a.

reflect a waste of society’s scarce resources and reflect inefficient production.

b.

signal owners of factors of production to move their resources out of that industry.

c.

imply that accounting costs are greater than economic costs in this industry.

d.

signal owners of factors of production to move resources into this industry.

144. If a firm is losing money, this implies that

a.

consumers do not understand the value of the product.

b.

the value of the resources used to make the product is being reduced.

c.

the firm must go out of business immediately.

d.

this product cannot be produced profitably in the long run.

145. In a price-taker market, economic losses indicate that

a.

some firms are using unfair tactics to harm others.

b.

some firms have miscalculated, producing goods that are less valuable than the resources

used to make them.

c.

the situation is normal and firms need to make no adjustments.

d.

the firms in the industry are not minimizing their cost; they should expand output in order

to fully realize the economies of scale in the industry.

146. If profit-seeking entrepreneurs are going to be successful, they must

a.

produce a product that the consumers value more than the resources required for its

production.

b.

produce the product more cheaply than their rivals regardless of quality.

c.

maximize the salaries of high-level management so they will be able to attract people who

will work hard.

d.

charge a higher price than their competitors so they can make economic profits in the long

run.

147. When competition is present, self-interested business decision makers have a strong incentive to

a.

produce efficiently.

b.

ignore the wishes of customers who are also self-interested.

c.

adopt technological improvements slowly in order to avoid making wrong decisions

d.

maximize price in order to maximize profits.

148. The ability of price-taker firms to freely expand or contract their businesses and to enter or exit the

market means that

a.

prices will always be high enough to generate positive economic profit.

b.

resources that would be more valuable elsewhere will be trapped, unproductively, in a

particular industry.

c.

resource owners cannot move their resources to other areas where they would be more

highly valued.

d.

resources that would be more valuable elsewhere will not be trapped, unproductively, in a

particular industry.

149. If a price taker in a competitive market is going to maximize profits, he must

a.

increase the price of his product.

b.

minimize his fixed costs of production.

c.

minimize the per-unit cost of producing the good.

d.

use the highest valued set of resources to produce his product.

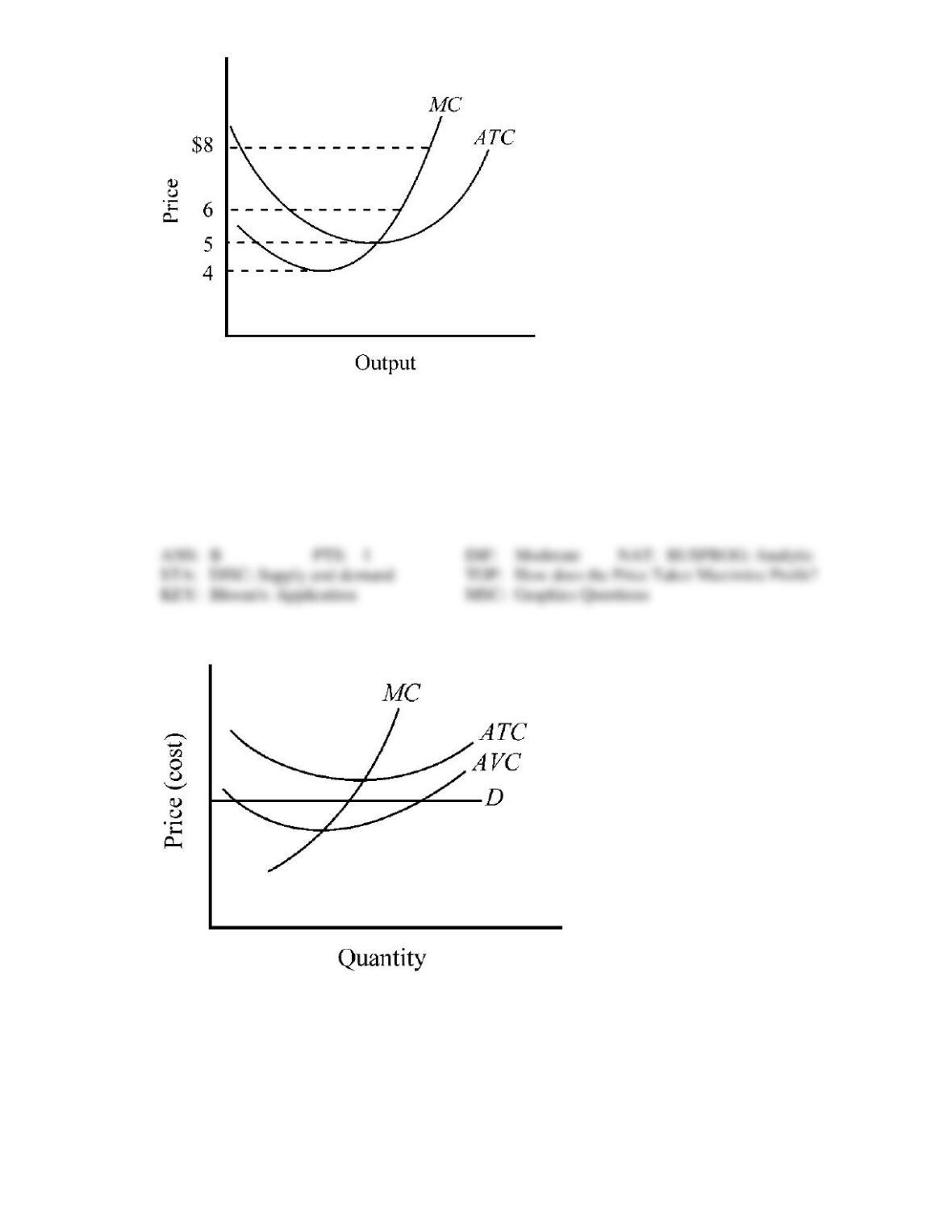

Figure 9-1

150. Figure 9-1 shows the marginal and average total cost curves for a firm producing product A. What

would be the minimum price this firm could charge and still continue to supply A to the market in the

long run?

a.

$4

b.

$5

c.

$6

d.

$8

Figure 9-2

151. Figure 9-2 illustrates a firm

a.

capable of earning economic profit.

b.

that is only able to break even when it maximizes profit.

c.

taking economic losses.

d.

that should shut down immediately.