69)

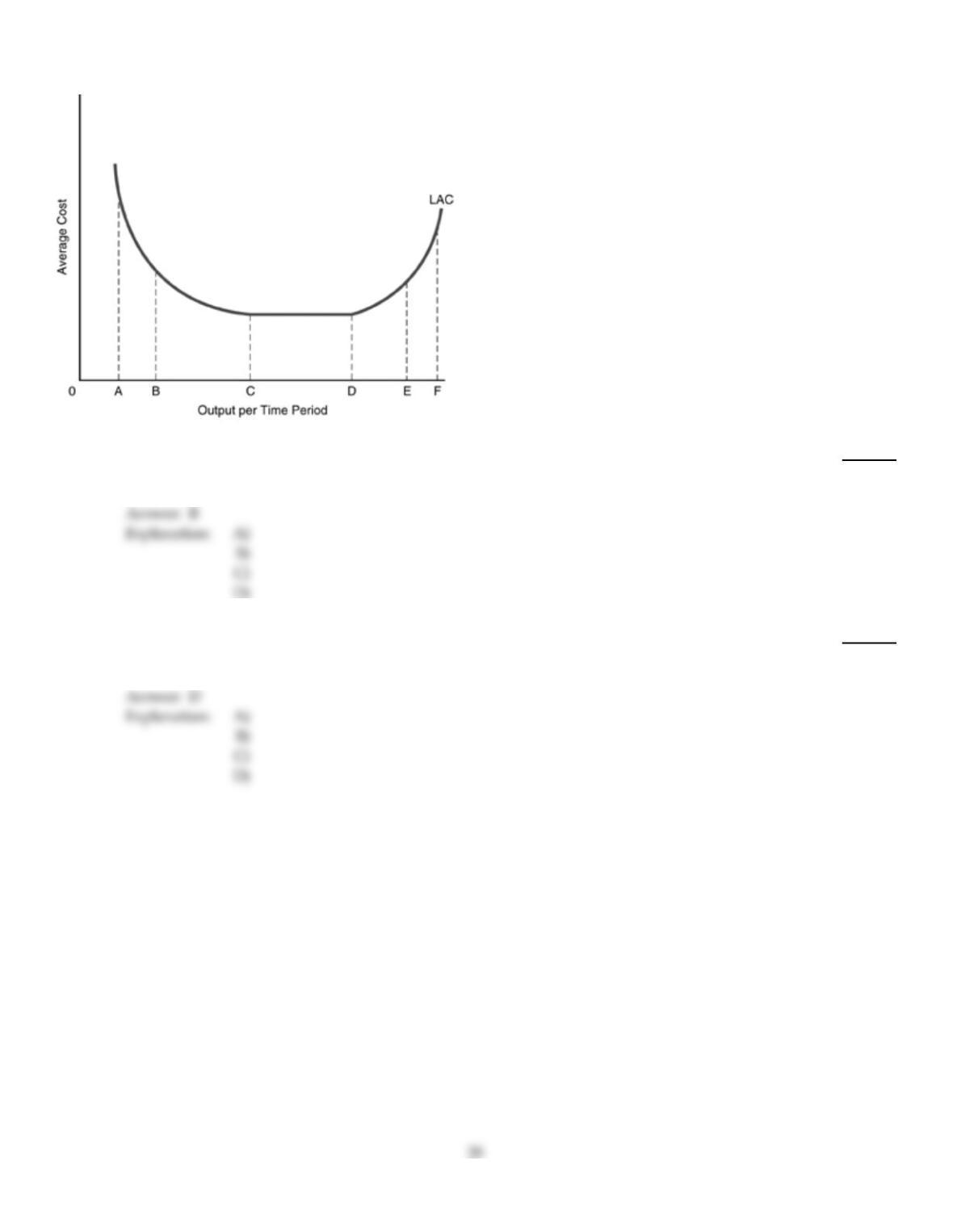

In the above figure, the long–run cost curve between points A and B illustrates

69)

A)

diseconomies of scale.

B)

economies of scale.

C)

diminishing marginal product.

D)

constant returns to scale.

70)

The planning curve is the

70)

A)

short–run average cost curve.

B)

short–run marginal cost curve.

C)

production function.

D)

long–run average cost curve.

Explanation:

Explanation:

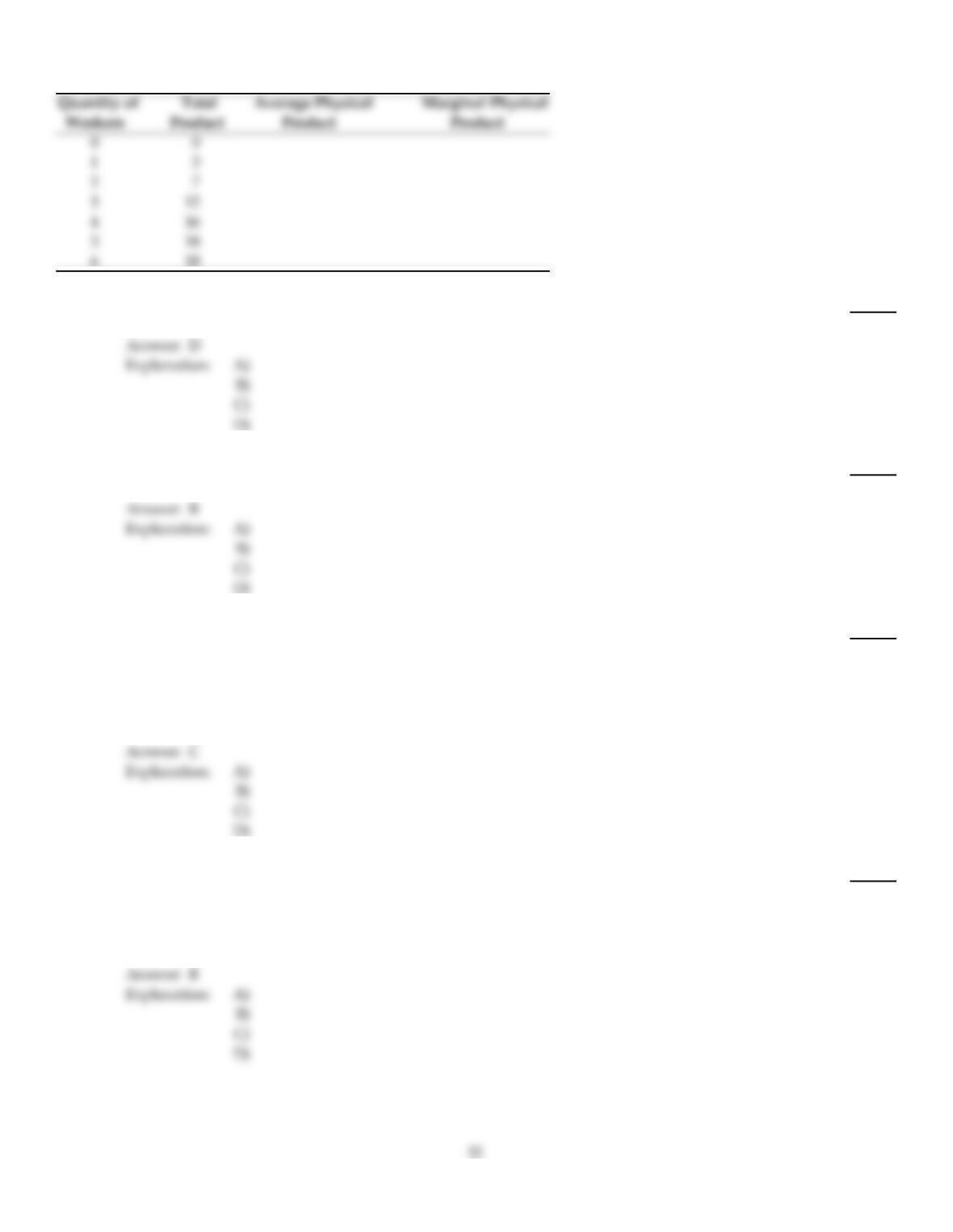

71)

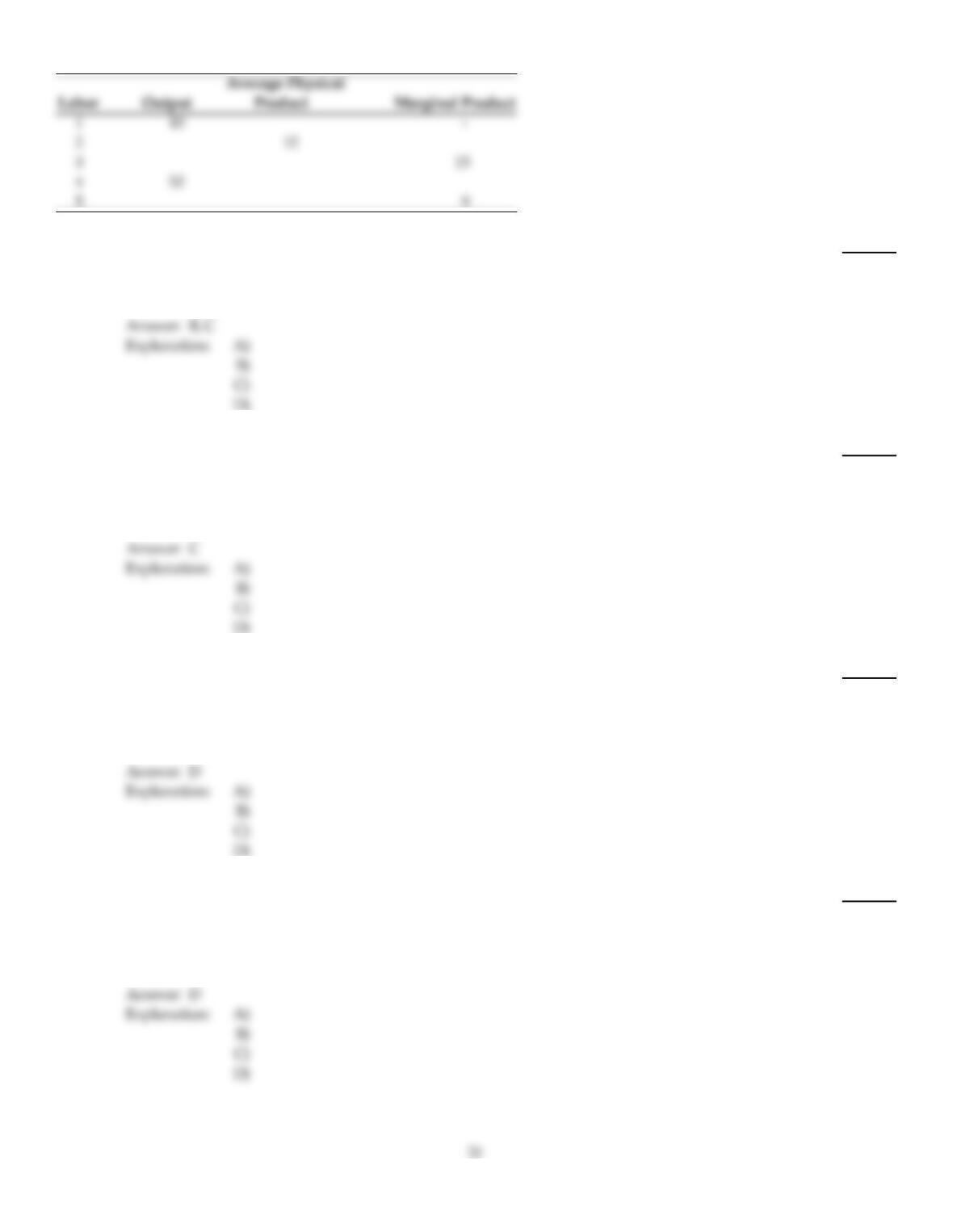

Using the above table, the average physical product and marginal physical w hen 4 workers are

employed are

71)

A)

13 and 9, respectively.

B)

14 and 13, respectively.

C)

13 and 13, respectively.

D)

13 and 14, respectively.

72)

Total fixed cost is

72)

A)

the cost of buying and installing new machinery.

B)

the expenditure on imported raw materials.

C)

the cost that does not change as output changes.

D)

the wages paid to consultants.

73)

If we add successive laborers to work a given amount of land on a wheat farm, eventually

73)

A)

the increases in wheat harvested will rise at a constant rate.

B)

the increases in wheat harvested will get larger and larger.

C)

average total cost will fall to zero.

D)

the increases in wheat harvested will get smaller and smaller.

74)

If average variable costs are increasing while average total costs are decreasing, then

74)

A)

marginal cost must equal average total cost.

B)

fixed costs must be zero.

C)

marginal cost must equal average variable cost.

D)

marginal cost must lie between average variable and average total costs.

75)

When the average physical product is rising,

75)

A)

total cost is falling.

B)

average variable cost is falling.

C)

marginal cost is always rising.

D)

average total cost is increasing.

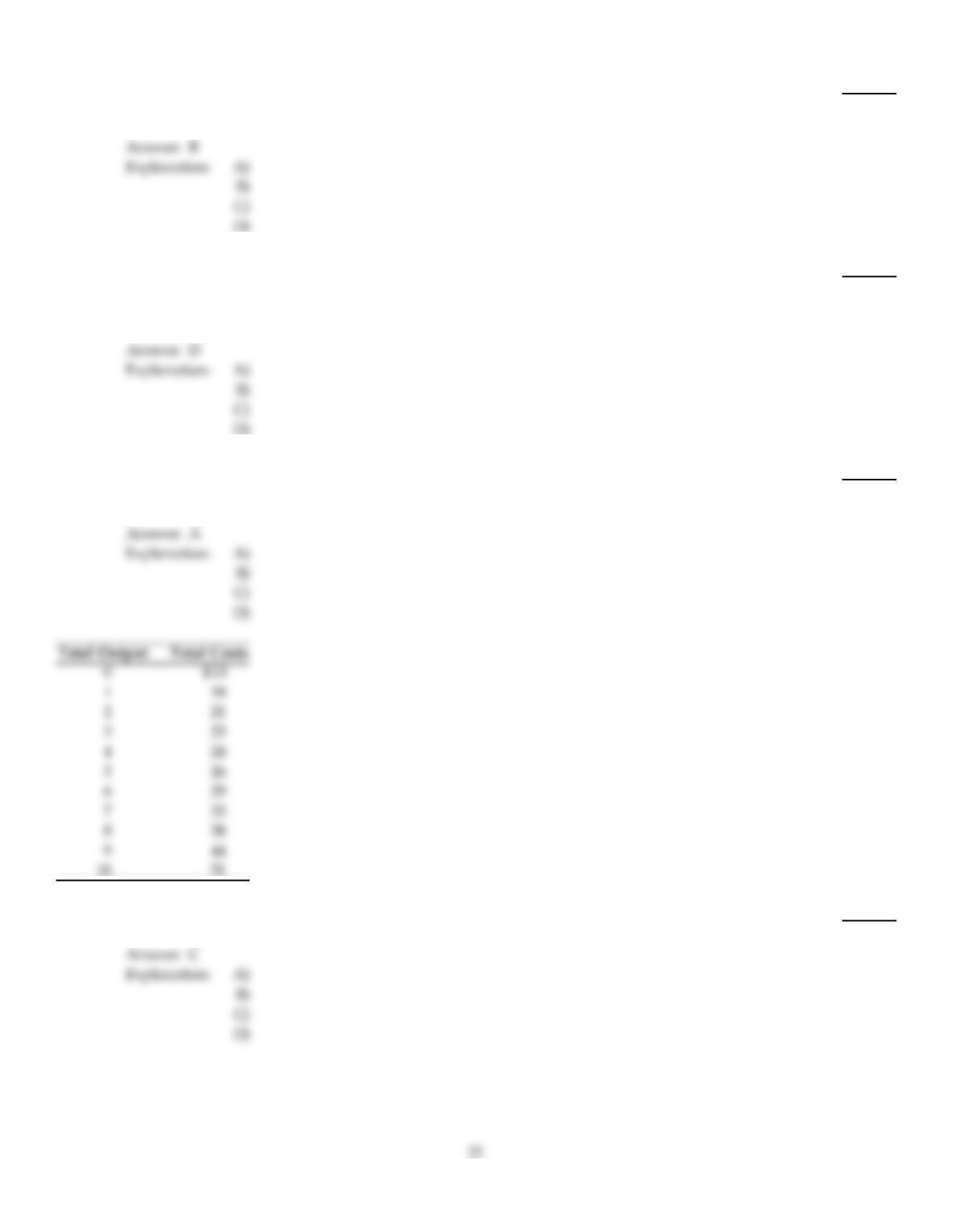

76)

When total product is rising,

76)

A)

marginal product must be positive.

B)

marginal product must be negative.

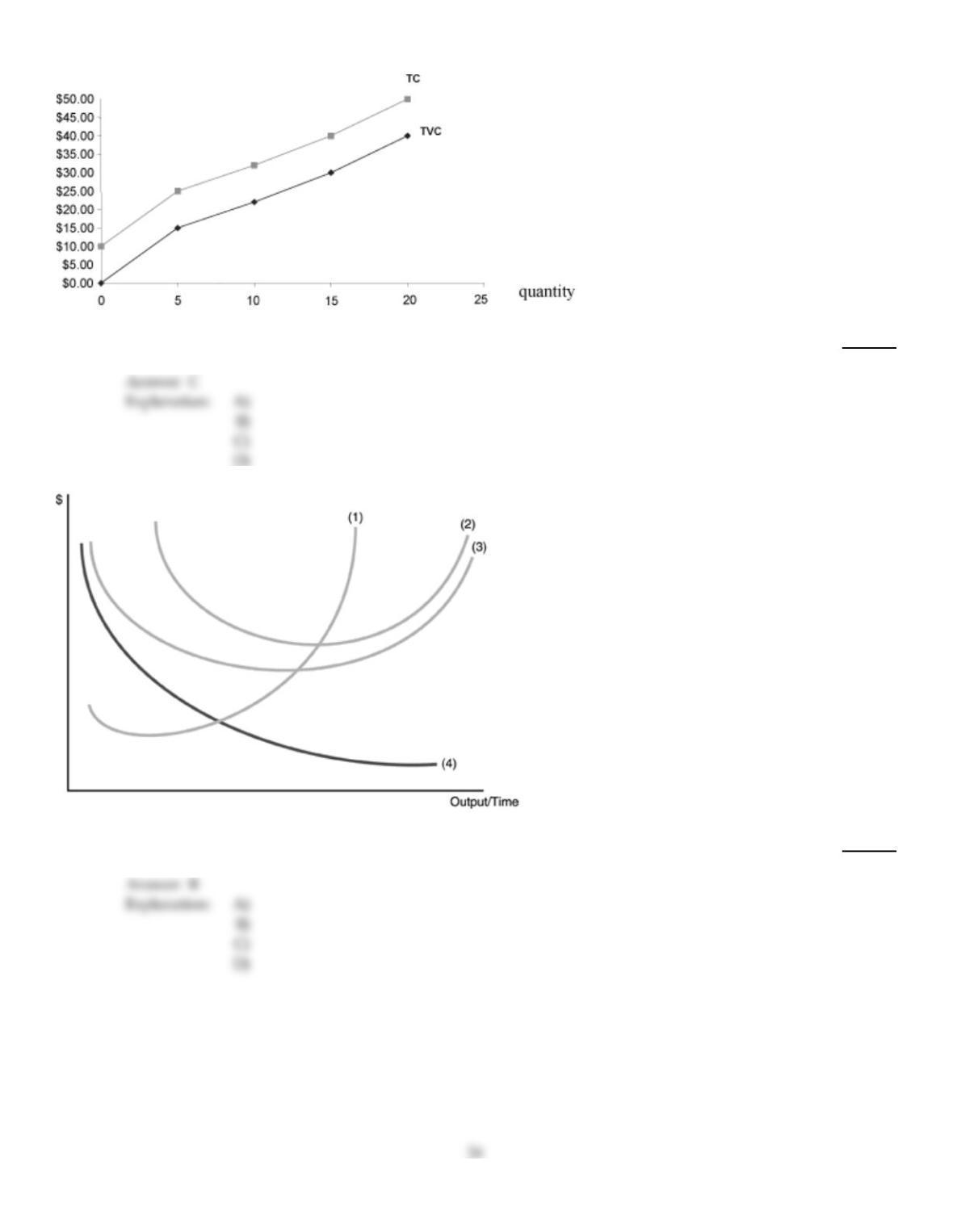

C)

variable cost must be declining.

D)

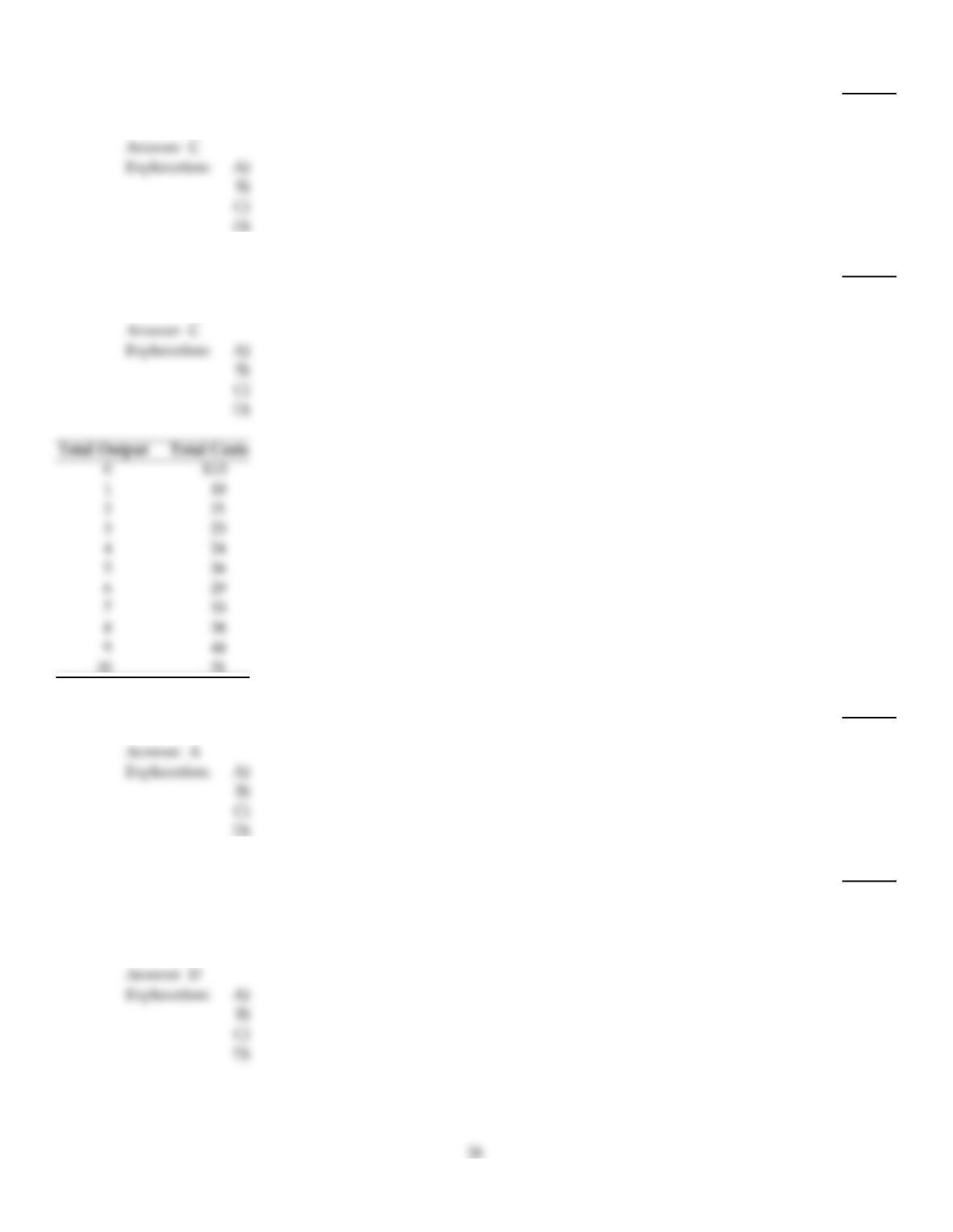

fixed cost must be rising.

77)

If Microsoft is determining whether to build a new plant in Southern California or in New Mexico,

it is making a(n) ________ decision.

77)

A)

immediate–run

B)

variable–input

C)

short–run

D)

long–run

78)

As successive equal increases in a variable factor of production are added to fixed factors of

production, there will be a point beyond which the extra product that can be attributed to each

additional unit of the variable factor of production will decline. This is known as the law of

78)

A)

decreasing product.

B)

diminishing average product.

C)

diminishing marginal product.

D)

diminishing total product.

79)

If the price of labor is constant and a firm experiences diminishing marginal product, then its

79)

A)

total costs decrease.

B)

marginal costs decrease.

C)

average variable cost increases.

D)

fixed costs increase.

80)

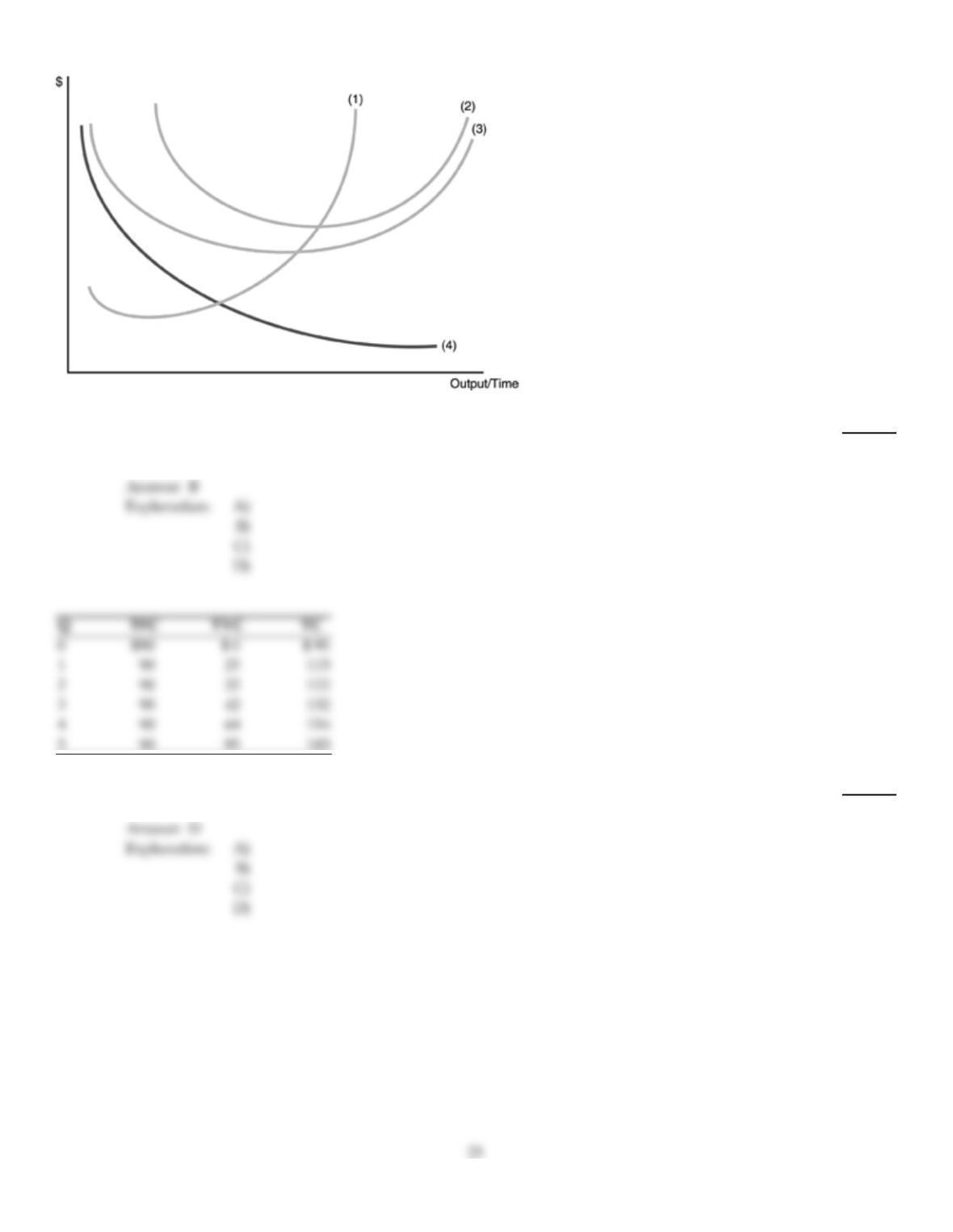

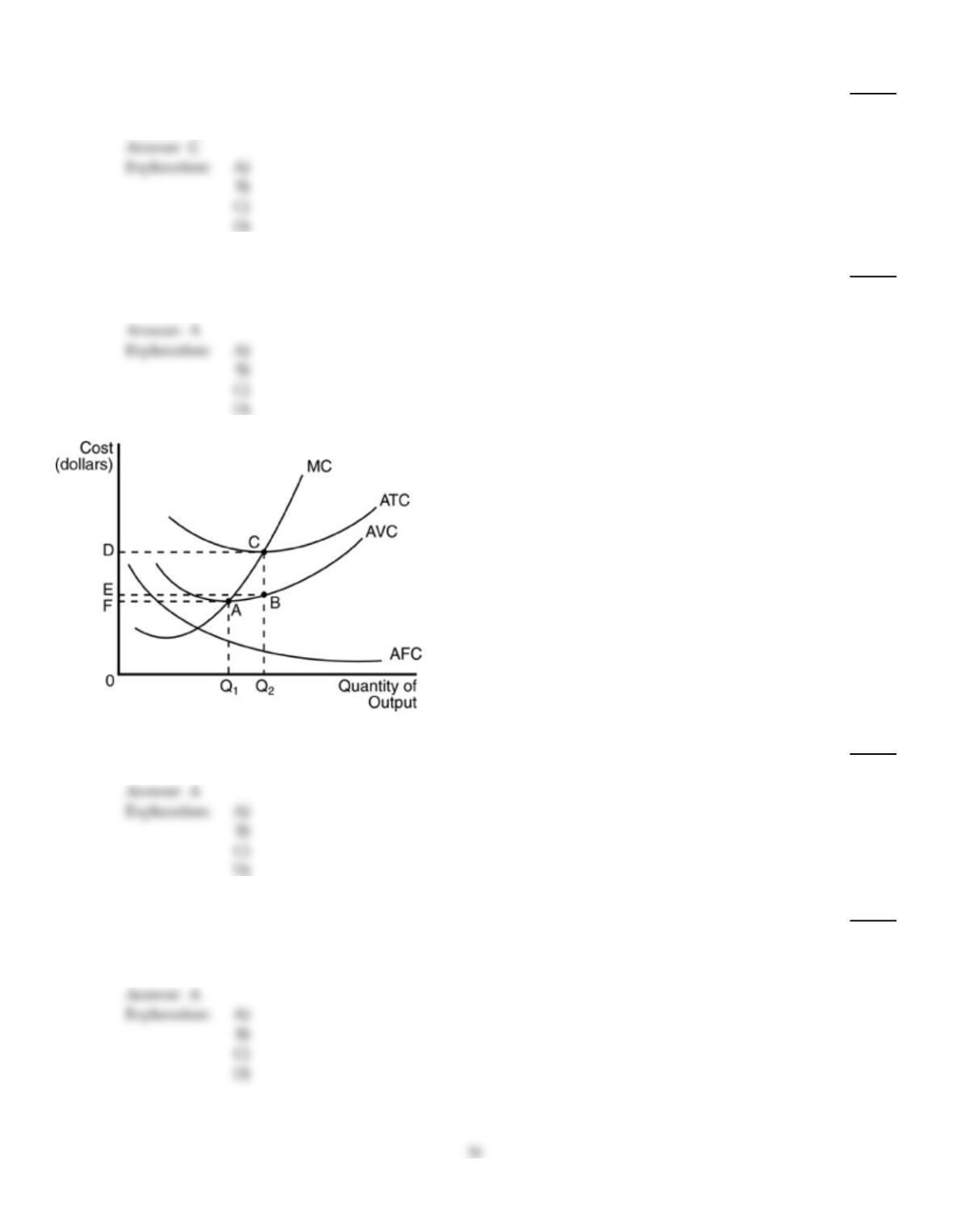

Refer to the above figure. Curve (4) is the

80)

A)

average variable cost curve.

B)

average fixed cost curve.

C)

marginal product curve.

D)

total fixed cost curve.

81)

Refer to the above table. When output rises from 2 units to 3 units, marginal costs are

81)

A)

$22.

B)

$41.

C)

$7.

D)

$10.

82)

Use the above figure. The ATC at output 5 is

82)

A)

$3.00.

B)

$2.00.

C)

$5.00.

D)

$25.00.

83)

Refer to the above figure. Average total costs are represented by curve

83)

A)

1.

B)

2.

C)

3.

D)

4.

84)

For a wheat farmer in the middle of harvesting system, a fixed input would be

84)

A)

combines rented.

B)

the land that had been planted.

C)

workers hired.

D)

trucks rented to haul the wheat.

85)

Suppose that one worker can produce 15 cookies, two workers can produce 35 cookies together,

and three workers can produce 65 cookies together. What is the marginal product of the 2nd

worker?

85)

A)

35 cookies

B)

15 cookies

C)

30 cookies

D)

20 cookies

86)

During the short run, a firm cannot

86)

A)

change its plant size.

B)

purchase more raw materials.

C)

change its variable costs.

D)

increase its use of labor.

87)

In the above table, total fixed costs are

87)

A)

$8.00.

B)

$18.00.

C)

$10.00.

D)

$5.00.

88)

The focus of firm decisions in the short run is primarily on

88)

A)

economies of scale.

B)

plant size.

C)

variable inputs.

D)

capital investment.

89)

Marginal cost equals

89)

A)

TC/Q.

B)

TFC/Q.

C)

change in total cost/change in output.

D)

TVC/Q.

90)

In the above table, the marginal cost of the ninth unit is

90)

A)

$6.00.

B)

$7.00.

C)

$4.00.

D)

$5.00.

91)

Marginal physical product and average physical product are measured in

91)

A)

the same units as marginal cost and average total cost.

B)

profit terms.

C)

dollars.

D)

units of production.

92)

The marginal physical product of labor is calculated assuming other factor inputs

92)

A)

decrease.

B)

remain constant.

C)

increase less than proportionately.

D)

increase more than proportionately.

93)

Economies of scale exist where the long–run average cost curve is

93)

A)

upward sloping.

B)

downward sloping.

C)

tangent to the marginal cost curve.

D)

horizontal.

94)

If the marginal product of an input is falling, then

94)

A)

average total cost is constant.

B)

average fixed cost is constant.

C)

marginal cost is falling.

D)

marginal cost is rising.

95)

Which of the following would NOT be a short–run decision for the firm?

95)

A)

Build another wing on the plant in order to add a new assembly line

B)

Recall workers who were previously laid–off

C)

Have labor work two hours overtime each day in order to expand output

D)

Place an order with a supplier for additional raw materials

96)

Suppose that one worker can produce 15 cookies, two workers can produce 35 cookies together,

and three workers can produce 65 cookies together. What is the average product of the first two

workers?

96)

A)

15 cookies

B)

20 cookies

C)

35 cookies

D)

17.5 cookies

97)

The marginal cost curve always intersects the average total cost curve at the point at which the

average total cost curve

97)

A)

is at its minimum.

B)

is zero.

C)

is at its maximum.

D)

has a vertical slope.

98)

Which of the following would NOT be considered a fixed cost of production?

98)

A)

The opportunity cost of capital

B)

Insurance payments on plant and equipment

C)

Wages paid to labor

D)

Interest payments on a loan

C

99)

In the above table, what is the average variable cost to produce 2 units of output?

99)

A)

$20

B)

$30

C)

$55

D)

$60

B

A

100)

In the above table, the average product of the fifth worker is

100)

A)

–5.

B)

135.

C)

27.

D)

35.

101)

Marginal cost is equal to average variable cost

101)

A)

when average variable cost is at its minimum value.

B)

when average variable cost is getting larger.

C)

when average variable cost is getting smaller.

D)

when marginal cost is at its minimum value.

102)

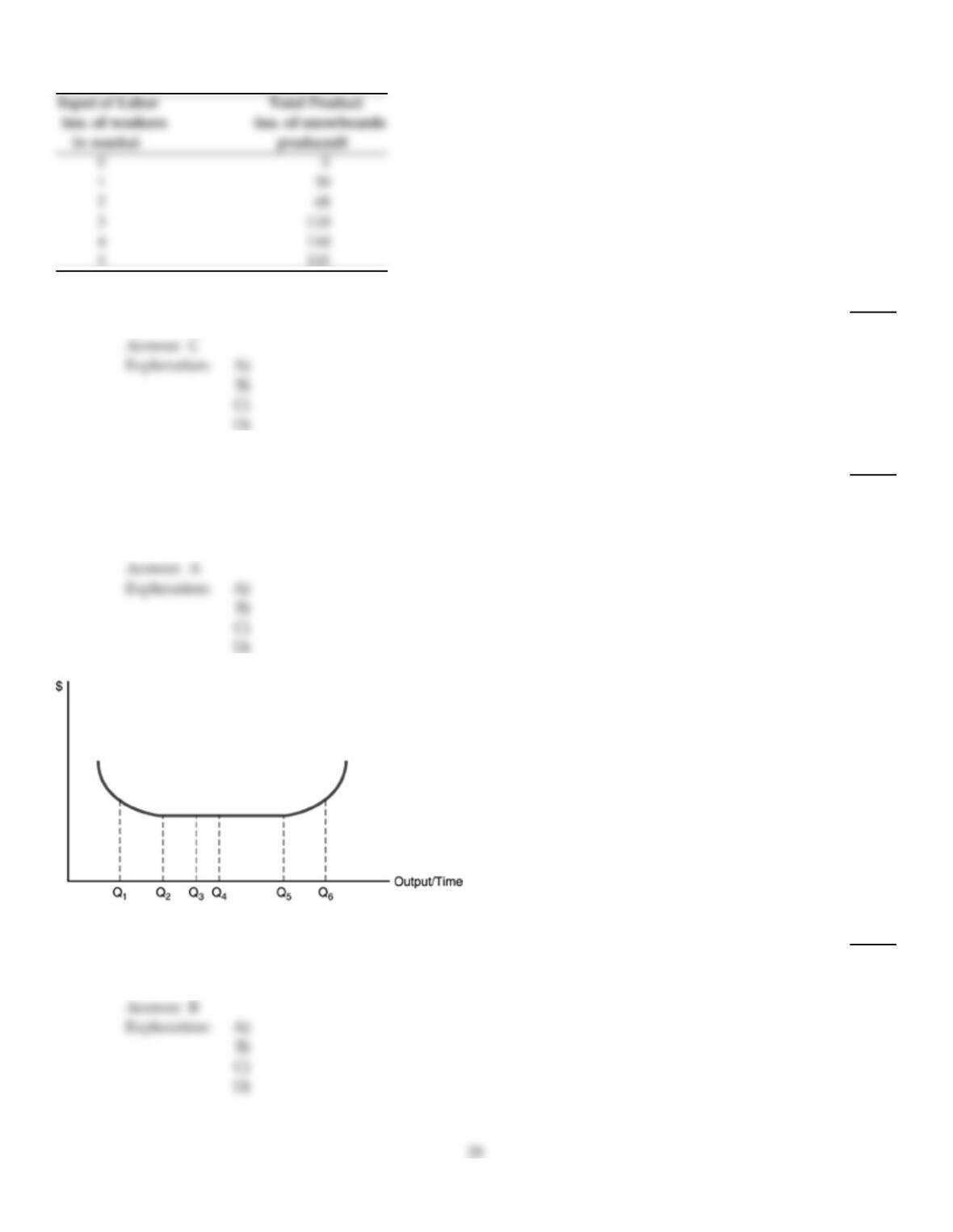

Refer to the above figure. Diseconomies of scale exist

102)

A)

up to output Q2.

B)

after output Q5.

C)

over the entire range of output.

D)

from output Q2 to Q5.

103)

An increase in output would result in a rise in long–run average costs when there are

103)

A)

constant returns to scale.

B)

diseconomies to scale.

C)

economies of scale.

D)

the law of diminishing marginal product.

104)

Assume it takes 10 units of labor to produce 4 units of output. When the price of labor is $6 per unit

and fixed costs equal $60, what is the total cost of those 4 units of output?

104)

A)

$84

B)

$70

C)

$120

D)

$60

105)

In the above table, the marginal physical product of the 3rd worker is

105)

A)

12.

B)

4.

C)

5.

D)

3.

106)

The time frame in which all factors of production can vary is

106)

A)

indeterminate.

B)

the short run.

C)

the intermediate run.

D)

the long run.

107)

When Super Stuff Corporation produces 5,000 units, total costs equal $150,000 and total variable

costs equal $75,000. At this level of output, what is Super Stuff’s average fixed cost?

107)

A)

$30

B)

$225,000

C)

$15

D)

$75,000

108)

As long as output increases,

108)

A)

average fixed costs decrease.

B)

average total costs decrease.

C)

average variable costs decrease.

D)

marginal costs decrease.

109)

In the above figure, if this firm produces output level Q2, it has average variable costs of

109)

A)

OE.

B)

OD.

C)

OF.

D)

OC.

110)

The change in total product occurring when a variable input is increased and all other inputs are

held constant is

110)

A)

marginal physical product.

B)

average physical product.

C)

marginal cost.

D)

average total cost.

111)

In the above table, the average physical product of the 3rd worker is

111)

A)

3.

B)

12.

C)

5.

D)

4.

112)

Costs that do not vary with output are

112)

A)

variable costs.

B)

fixed costs.

C)

marginal costs.

D)

total costs.

113)

Which of the following statements is true?

113)

A)

Diseconomies of scale is a short–run concept, while economies of scale is a long–run concept.

B)

No firm would ever operate at a level of output for which it experiences diseconomies of

scale.

C)

A firm can experience diminishing marginal product and economies of scale at the same time.

D)

If a firm is experiencing economies of scale, diminishing marginal product has not set in yet.

114)

Which of the following is a long–run adjustment?

114)

A)

A bank hires a new CEO.

B)

A company builds a new manufacturing plant.

C)

A company hires ten new management trainees.

D)

A restaurant hires a new chef.

115)

Another term for the total quantity of output is

115)

A)

marginal physical product.

B)

total product.

C)

average variable product.

D)

average physical product.

116)

Which of the following is NOT correct?

116)

A)

MC = change in TC/change in Q

B)

ATC = TC/Q

C)

ATC + AVC = AFC

D)

AVC = TVC/Q

117)

If a firm gets so large that management of employees and other resources becomes a costly

problem, it will be experiencing

117)

A)

diseconomies of scale.

B)

constant returns to scale.

C)

diminishing marginal product.

D)

economies of scale.

118)

After some point successive equal increases in a variable factor of production, when added to a

fixed amount of inputs, will result in smaller increases in output. This is known as

118)

A)

marginal physical product.

B)

the law of diminishing marginal product.

C)

the long run.

D)

short run average cost.

119)

Short–run total cost is defined as

119)

A)

total capital cost only.

B)

the sum of marginal cost and total variable cost.

C)

total fixed cost plus total variable cost.

D)

price of labor per unit multiplied by the number of labor units.

120)

If a farmer seeks to buy one–hundred more acres for her kiwi fruit farm, she is making a

120)

A)

long–run decision.

B)

short–run decision.

C)

variable–input decision.

D)

immediate–run decision.

SHORT ANSWER. Write the word or phrase that best completes each statement or answers the question.

121)

“The short–run average total cost curve and the long–run average cost curve are both

U–shaped for the same reasons.” Do you agree or disagree? Why?

121)

Explanation:

122)

What is the difference between the short run and the long run? What is the appropriate

time dimension of the long run?

122)

Explanation:

123)

“All average costs have a U–shaped curve.” Do you agree or disagree? Explain why?

123)

Explanation:

124)

What is the relationship between the marginal cost curve and marginal product? Explain.

124)

Explanation:

125)

What are the relationships between the marginal cost curve and the average cost curves?

Explain in words.

125)

Explanation:

Explanation:

126)

“In the short run, a firm cannot change any of its inputs.” Do you agree or disagree?

Explain.

126)

127)

Explain how the long–run average cost curve is constructed graphically.

127)

128)

“In economics, the short run commonly refers to a period within one year and the long run

is a period longer than one year.” Do you agree or disagree? Explain your answer.

128)

129)

Graphically, what happens to the production function if a firm uses automation to raise the

amount of output per worker? Explain.

129)

130)

Graphically, what does the marginal product curve for a labor input look like? Explain in

words.

130)

Answer Key

Testname: C22

36

Answer Key

Testname: C22

Answer Key

Testname: C22