Page 1

1.

Louis has invested $1,000 in the stock market. At the end of one year, there is a 30%

chance that his stock will be worth only $800 and a 70% chance that it will be worth

$1,200. The expected value of his stock at the end of one year is:

A)

$1,000.

B)

$1,080.

C)

$1,200.

D)

$1,160.

2.

Domingo has a total wealth of $500,000 composed of a house worth $100,000 and

$400,000 in cash. He keeps the cash in a safe deposit box, so that it is completely safe.

However, there is a 10% chance that his house will burn down by the end of the year

and be worth nothing and a 90% chance that nothing will happen to it. Without

insurance, the expected value of his end-of-year wealth is:

A)

$410,000.

B)

$450,000.

C)

$490,000.

D)

$485,000.

3.

Micah is considering turning pro before his senior year basketball season. If he turns

pro, Micah expects a pro contract worth $2 million in present value. If he does not turn

pro, there is a 50% chance an injury will prevent him from playing professionally and a

50% chance he will get a pro contract worth $4 million in present value. What is the

expected present value of Micah’s pro contract if he stays in college for his senior year?

A)

$3.5 million

B)

$5 million

C)

$2 million

D)

$0

4.

Amanda recently graduated from college, and she has a job offer with uncertain income:

there is a 70% probability that she will make $10,000 and a 30% probability that she

will make $70,000. The expected value of Amanda’s income is:

A)

$40,000.

B)

$21,000.

C)

$28,000.

D)

$10,000.

5.

A random variable:

A)

has an uncertain future value.

B)

has a constant value.

C)

doesn’t exist in economics.

D)

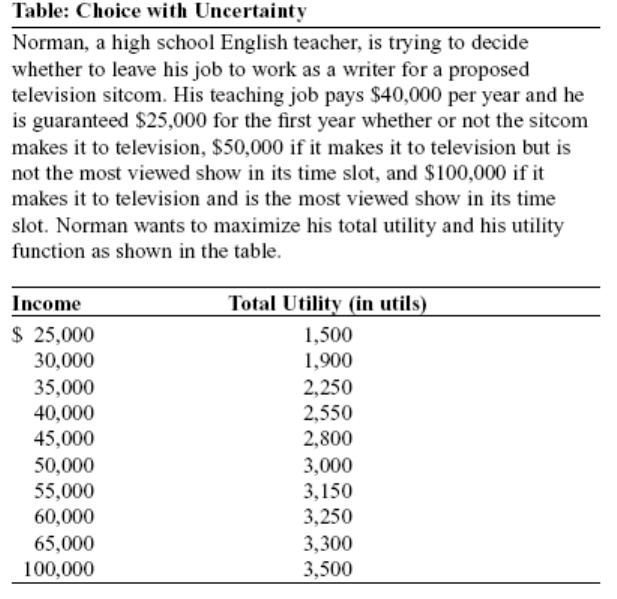

is useless in economic decision making.

Page 2

6.

The expected value of a random variable is:

A)

the most frequently occurring value of that variable.

B)

the most recent value of that variable.

C)

the weighted average of all possible values, where the weights on each possible

value correspond to the probability of that value occurring.

D)

impossible to determine.

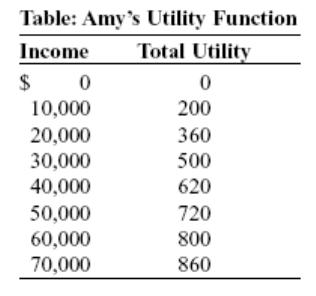

7.

If there is a 25% probability that Joseph will earn $10 per hour at his job today and a

75% probability that he will earn $20 per hour today, his expected pay per hour is:

A)

$10.00.

B)

$15.00.

C)

$17.50.

D)

$20.00.

8.

If there is a 50% probability that Joseph will earn $10 per hour at his job today and a

50% probability that he will earn $20 per hour today, his expected pay per hour is:

A)

$10.00.

B)

$12.50.

C)

$15.00.

D)

$20.00.

9.

If a stock analyst believes there is a 25% probability that the stock price of Dymonatis

will be $30 at the end of the year, a 50% probability that it will be $40, and a 25%

probability that it will be $50, then the expected value of the stock at the end of the year

is:

A)

$30.

B)

$35.

C)

$40.

D)

$50.

10.

If a stock analyst believes there is a 10% probability that the stock price of Dymonatis

will be $30 at the end of the year, a 50% probability that it will be $40, and a 40%

probability that it will be $50, then the expected value of the stock at the end of the year

is:

A)

$32.

B)

$38.

C)

$40.

D)

$43.

Page 3

11.

Uncertainty about monetary outcomes is known as:

A)

financial risk.

B)

monetary risk.

C)

profitability risk.

D)

risk aversion.

12.

A friend of yours owes you $10, and he wants to flip a coin for double or nothing. If the

coin lands heads, he will pay you $20. If the coin lands tails up, he will pay you nothing.

As the coin is in midair, what is your expected value of this wager?

A)

$0

B)

$10

C)

$20

D)

$30

13.

You are about to have a meeting with your manager about a raise in your salary. You

are going to request an increase of $5,000, but you believe the probability of success to

be only 25%. You believe there is a 25% probability your boss will counter with a

$3,000 raise and a 25% probability that your boss will offer a $1,000 raise. Finally,

there is a 25% probability that you will receive no increase in your salary. What is the

expected value of the outcome of your meeting?

A)

$2,250

B)

$9,000

C)

$6,750

D)

$3,000

14.

Darnell pays $7,300 per year to an insurance company in return for its promise to pay

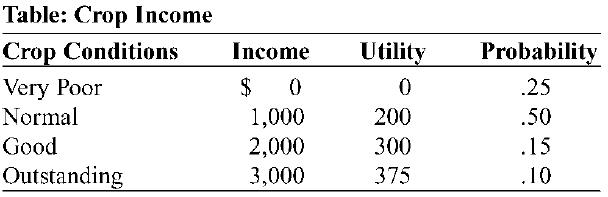

part of his family’s medical bills. The $7,300 is Darnell’s:

A)

risk.

B)

marginal utility.

C)

expected utility.

D)

premium.

15.

A fair insurance policy is one whose premium is _____ the expected value of the claims.

A)

equal to

B)

greater than

C)

less than

D)

unrelated to

Page 4

16.

Suppose that an individual is risk-averse. If this individual’s utility function is depicted

in a graph, with income measured on the horizontal axis and utils on the vertical axis,

the graph will be an upward-sloping:

A)

straight line through the origin.

B)

straight line with a positive vertical intercept.

C)

curve with a steadily increasing slope (i.e., a curve that is convex from below).

D)

curve with a steadily decreasing slope (i.e., a curve that is concave from below).

17.

Amanda recently graduated from college, and she has a job offer with uncertain income.

There is a 70% probability that she will make $10,000 and a 30% probability that she

will make $70,000. Suppose Amanda is offered another job with a certain income. All

else equal, if she has a constant marginal utility of income, she will accept the second

job offer only if it pays more than:

A)

$40,000.

B)

$28,000.

C)

$10,000.

D)

$21,000.

18.

Domingo has total wealth of $500,000 composed of a house worth $100,000 and

$400,000 in cash. He keeps the cash in a safe deposit box, so that it is completely safe.

However, there is a 10% chance that his house will burn down and be worth nothing and

a 90% chance that nothing will happen to it. Domingo buys insurance guaranteeing that

his house will be restored to its original condition should anything happen to it. The

insurance premium is $2,000. Consequently (assuming other things remain unchanged),

his future:

A)

expected wealth is $480,000.

B)

wealth is $500,000 for sure.

C)

expected wealth is $490,000.

D)

wealth is $498,000 for sure.

Page 5

19.

The Conduire family owns three cars and is considering buying insurance to cover the

cost of repairs. They face two possible states: state 1, in which their cars need no repairs

and their income available for purchasing other goods and services is equal to $50,000;

and state 2, in which their cars need $10,000 worth of repairs and their income available

for purchasing other goods and services is reduced to $40,000. The probability of

occurrence is 0.5 for each state. They can buy insurance that will cover the full cost of

repairs for $5,000. If the Conduires are risk-averse and maximize their expected utility:

A)

they will buy the insurance.

B)

they will be indifferent between buying and not buying the insurance, since their

expected income for purchasing other goods and services is $45,000 regardless of

what they do.

C)

they will not buy the insurance, since buying it does not increase their expected

income for purchasing other goods and services.

D)

they will put $10,000 in savings to pay for any required repairs and not buy

insurance.

20.

The total utility of income curve for a risk-averse individual will be _____ with income.

A)

decreasing

B)

increasing at an increasing rate

C)

increasing at a constant rate

D)

increasing at a decreasing rate

21.

Individuals differ in risk aversion because of:

A)

adverse selection.

B)

moral hazard.

C)

differences in income or wealth.

D)

differences in their insurance.

22.

If an individual is risk-averse, then his or her total utility function must display _____

marginal utility.

A)

constant

B)

diminishing

C)

increasing

D)

either constant or diminishing, but not increasing,

23.

The marginal utility of income for a risk-averse individual will be:

A)

constant.

B)

diminishing.

C)

increasing.

D)

unknown; the answer depends on the value of income.

Page 6

24.

For most families, total utility does NOT:

A)

rise as income rises.

B)

rise less quickly as income rises.

C)

show increasing marginal utility.

D)

show diminishing marginal utility.

25.

For most families, the marginal utility of income is:

A)

increasing.

B)

constant.

C)

diminishing.

D)

unknown; the answer depends on the value of income.

26.

A fair insurance policy is one whose premium:

A)

is zero.

B)

allows the insurance company to profit.

C)

equals the expected value of the claims.

D)

is higher as the probability of a claim decreases.

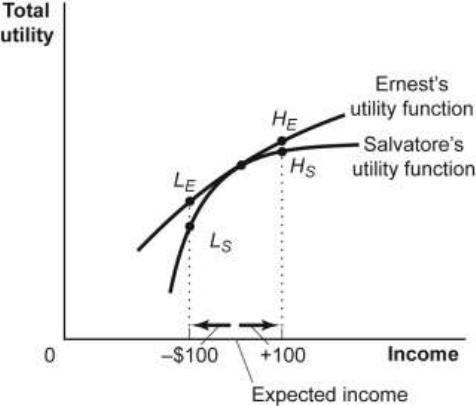

Use the following to answer questions 27-28:

Figure: Differences in Risk Aversion

Page 7

27.

(Figure: Differences in Risk Aversion) Look at the figure Differences in Risk Aversion.

Which of the following statements is CORRECT?

A)

Ernest will gain more utility from insurance than will Salvatore.

B)

Salvatore will gain less utility from an increase in income than Ernest but will lose

more utility than Ernest from a fall in income.

C)

Ernest is more risk-averse than Salvatore.

D)

If either Ernest or Salvatore buys insurance, adverse selection will occur.

28.

(Figure: Differences in Risk Aversion) Look at the figure Differences in Risk Aversion.

An important reason Ernest and Salvatore may differ in their aversion to risk is:

A)

the way their marginal utility is affected by income.

B)

their understanding of risk.

C)

their initial wealth holding or initial income level.

D)

the way their marginal utility is affected by income and their initial wealth holding

or initial income level.

29.

A person who is willing to pay an insurance premium to lessen financial risk is said to

be:

A)

a moral hazard.

B)

risk-loving.

C)

risk-averse.

D)

risk-neutral.

30.

Bikul has just started a great job and plans to buy a fancy car worth $100,000. Bikul is

risk-averse in money matters, but he likes to drive fast, so the probability that he wrecks

the car (a total loss of $100,000) is 0.10. The probability that he has no accidents is 0.90.

If an insurance company offers Bikul a fair insurance policy, the premium will be:

A)

$10,000.

B)

$90,000.

C)

$80,000.

D)

It is impossible to calculate a premium unless we know Bikul’s utility function.

31.

The premium for a(n) _____ insurance policy is equal to the expected value of the

claim.

A)

fair

B)

premium

C)

unfair

D)

diversification

Page 8

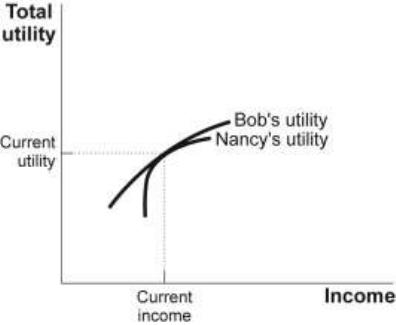

Use the following to answer questions 32-33:

Figure: Risk Aversion

32.

(Figure: Risk Aversion) Look at the figure Risk Aversion. Bob and Nancy have the

same income and the same total utility. Nancy is _____ risk-averse than Bob because

her marginal utility curve is _____ than Bob’s.

A)

more; flatter

B)

more; steeper

C)

less; flatter

D)

less; steeper

33.

(Figure: Risk Aversion) Look at the figure Risk Aversion. Bob and Nancy have the

same income and total utility. Nancy will be willing to pay a ____ insurance premium

than Bob because she is _____ risk-averse.

A)

higher; more

B)

lower; more

C)

lower; less

D)

higher; less

Page 9

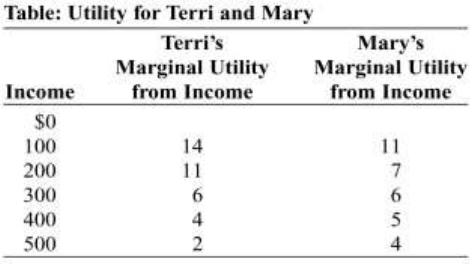

Use the following to answer questions 34-35:

34.

(Table: Utility for Terri and Mary) Look at the table Utility for Terri and Mary. Each

has an income of $300. _____ is more risk-averse because _____ has a _____ drop in

total utility if income were to fall by $100.

A)

Mary; Mary; larger

B)

Terri; Mary; larger

C)

Mary; Terri; smaller

D)

Terri; Terri; larger

35.

(Table: Utility for Terri and Mary) Look at the table Utility for Terri and Mary. Each

has an income of $300. If each were offered insurance to offset the risk of falling

income, _____ would pay a larger premium because she is the consumer with _____

risk aversion.

A)

Terri; more

B)

Terri; less

C)

Mary; more

D)

Mary; less

36.

Risk-averse individuals are willing to pay a premium that is _____ their expected

claims.

A)

less than

B)

greater than or equal to

C)

equal to

D)

dependent on something other than

Page 10

37.

When faced with an insurance policy whose premium exceeds the expected value of the

claim:

A)

no one will buy it.

B)

only risk-tolerant individuals will buy it.

C)

risk-averse individuals will buy it as long as the utility associated with the

insurance is greater than the expected utility without the insurance.

D)

risk-averse individuals will buy it as long as the utility associated with the

insurance is less than the expected utility without the insurance.

38.

Which of the following regarding a warranty is NOT true?

A)

It is a form of consumer insurance.

B)

Consumers may buy one even if the cost of the warranty is greater than the

expected future claim paid by the manufacturer.

C)

It decreases the consumer’s expected utility from an item.

D)

It signals to consumers that the goods are of high quality.

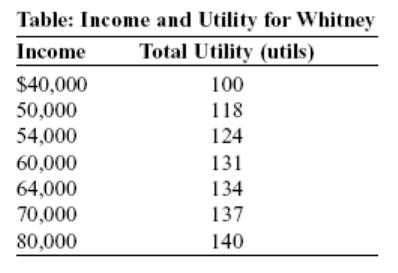

Use the following to answer questions 39-41:

39.

(Table: Income and Utility for Whitney) Look at the table Income and Utility for

Whitney. Whitney’s income next year is uncertain: there is a 40% probability she will

make $40,000 and a 60% probability she will make $80,000. What certain income

leaves Whitney as well off as her uncertain income?

A)

$64,000

B)

$60,000

C)

$54,000

D)

$50,000

Page 11

40.

(Table: Income and Utility for Whitney) Look at the table Income and Utility for

Whitney. Whitney’s income next year is uncertain: there is a 40% probability she will

make $40,000 and a 60% probability she will make $80,000. Whitney’s expected utility

is _____ utils.

A)

135

B)

124

C)

120

D)

130

41.

(Table: Income and Utility for Whitney) Look at the table Income and Utility for

Whitney. Whitney’s income next year is uncertain: there is a 40% probability she will

make $40,000 and a 60% probability she will make $80,000. The expected value of

Whitney’s income is:

A)

$64,000.

B)

$80,000.

C)

$40,000.

D)

$56,000.

Use the following to answer questions 42-43:

42.

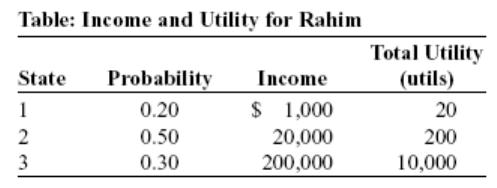

(Table: Income and Utility for Rahim) Look at the table Income and Utility for Rahim.

The expected value of Rahim’s income is:

A)

$221,000.

B)

$20,000.

C)

$110,000.

D)

$70,200.

43.

(Table: Income and Utility for Rahim) Look at the table Income and Utility for Rahim.

Rahim’s expected utility from income is:

A)

3,500 utils.

B)

10,000 utils.

C)

3,104 utils.

D)

Utility cannot be determined from the information given.

Page 12

Use the following to answer questions 44-48:

44.

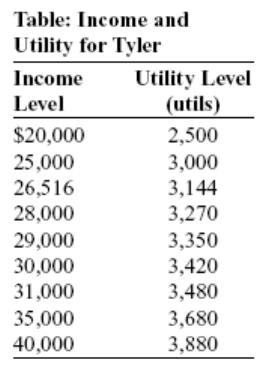

(Table: Income and Utility for Tyler) The table Income and Utility for Tyler shows the

utility Tyler receives at various income levels, but she does not know what her income

will be next year. There is a 40% chance her income will be $20,000, a 40% chance her

income will be $30,000, and a 20% chance her income will be $40,000. We know that

Tyler is risk-averse because:

A)

Tyler would prefer $40,000 but there is a risk she will make only $20,000.

B)

Tyler’s expected income is less than what she may actually earn.

C)

Tyler’s expected income is more than what she may actually earn.

D)

Tyler is subject to diminishing marginal utility from income.

45.

(Table: Income and Utility for Tyler) The table Income and Utility for Tyler shows the

utility Tyler receives at various income levels, but she does not know what her income

will be next year. There is a 40% chance her income will be $20,000, a 40% chance her

income will be $30,000, and a 20% chance her income will be $40,000. What is her

expected income?

A)

$28,000

B)

$29,000

C)

$30,000

D)

$31,000

Page 13

46.

(Table: Income and Utility for Tyler) The table Income and Utility for Tyler shows the

utility Tyler receives at various income levels, but she does not know what her income

will be next year. There is a 40% chance her income will be $20,000, a 40% chance her

income will be $30,000, and a 20% chance her income will be $40,000. What is her

expected utility in utils?

A)

3,270

B)

3,144

C)

3,420

D)

3,480

47.

(Table: Income and Utility for Tyler) The table Income and Utility for Tyler shows the

utility Tyler receives at various income levels, but she does not know what her income

will be next year. There is a 40% chance her income will be $20,000, a 40% chance her

income will be $30,000, and a 20% chance her income will be $40,000. What level of

certain income matches her expected utility, given the uncertainty?

A)

$28,000

B)

$25,000

C)

$26,516

D)

$29,000

48.

(Table: Income and Utility for Tyler) The table Income and Utility for Tyler shows the

utility Tyler receives at various income levels, but she does not know what her income

will be next year. There is a 40% chance her income will be $20,000, a 40% chance her

income will be $30,000, and a 20% chance her income will be $40,000. What is the

maximum amount of insurance Tyler would be willing to pay to guarantee an income of

$28,000?

A)

$0

B)

$1,484

C)

$26,516

D)

$126

Page 14

Use the following to answer questions 49-54:

49.

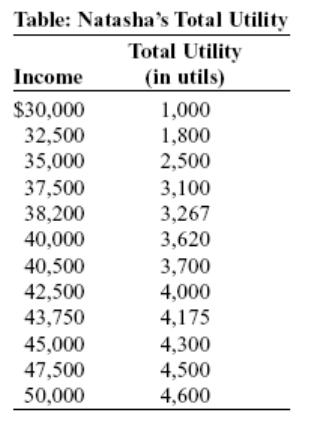

(Table: Natasha’s Total Utility) Look at the table Natasha’s Total Utility. Natasha’s

marginal utility _____ as her income increases. The marginal utility of income between

$30,000 and $32,500 is _____ utils per dollar, while it is _____ utils per dollar between

$47,500 and $50,000.

A)

increases; 0.48; 0.64

B)

increases; 0.12; 0.36

C)

diminishes; 0.50; 0.25

D)

diminishes; 0.32; 0.04

50.

(Table: Natasha’s Total Utility) Look at the table Natasha’s Total Utility. Natasha earns

$50,000 per year but faces losing $20,000 of it if she is late with her work. If there is a

25% probability that Natasha will be late with her work and her income will then equal

$30,000, her expected income is:

A)

$32,500.

B)

$38,200.

C)

$40,500.

D)

$45,000.

Page 15

51.

(Table: Natasha’s Total Utility) Natasha earns $50,000 per year but faces losing $20,000

of it if she is late with her work. If there is a 25% probability that Natasha will be late

with her work and her income will then equal $30,000, her expected total utility is

_____ utils.

A)

4,175

B)

3,700

C)

3,620

D)

3,259

52.

(Table: Natasha’s Total Utility) Look at the table Natasha’s Total Utility. Natasha earns

$50,000 per year but faces losing $20,000 of it if she is late with her work. If there is a

25% probability that Natasha will be late with her work and her income will equal

$30,000, what certain income leaves Natasha just as well off as her uncertain income?

A)

$37,500

B)

$38,200

C)

$40,500

D)

$42,500

53.

(Table: Natasha’s Total Utility) Look at the table Natasha’s Total Utility. Natasha earns

$50,000 per year but faces losing $20,000 of it if she is late with her work. If there is a

25% probability that Natasha will be late with her work and her income will equal

$30,000, To guarantee an income of $50,000, Natasha would be willing to pay _____

for insurance.

A)

$4,000

B)

$5,000

C)

$7,500

D)

$9,500

54.

(Table: Natasha’s Total Utility) Look at the table Natasha’s Total Utility. Natasha earns

$50,000 per year but faces losing $20,000 of it if she is late with her work. If there is a

25% probability that Natasha will be late with her work and her income will equal

$30,000, the premium for a fair insurance policy to eliminate the uncertainty in her

income would equal:

A)

$4,000.

B)

$5,000.

C)

$7,500.

D)

$9,500.

Page 16

Use the following to answer questions 55-61:

55.

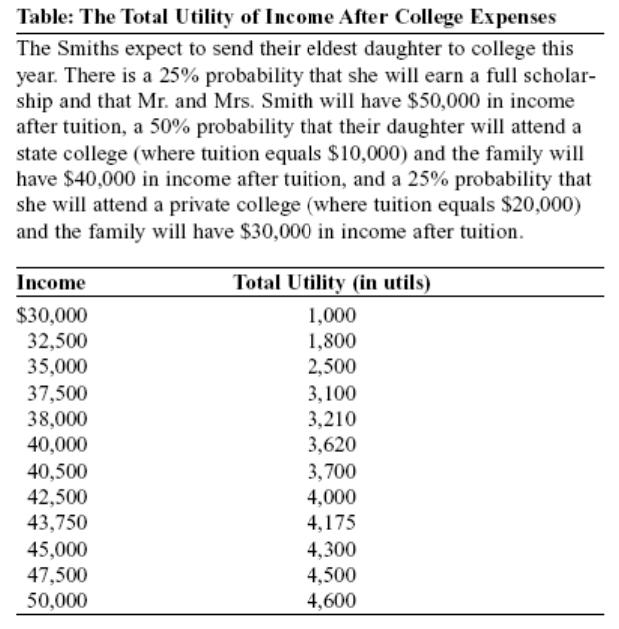

(Table: Total Utility of Income After College Expenses) Look at the table Total Utility

of Income After College Expenses. The Smith family has _____ marginal utility as

income increases. The marginal utility of income between $32,500 and $35,000 is

_____ utils per dollar, while it is _____ utils per dollar between $45,000 and $47,500.

A)

increasing; 0.48; 0.64

B)

increasing; 0.12; 0.36

C)

diminishing; 0.28; 0.08

D)

diminishing; 0.40; 0.10

56.

(Table: Total Utility of Income After College Expenses) Look at the table Total Utility

of Income After College Expenses. The Smith family’s expected income after tuition is:

A)

$32,500.

B)

$38,000.

C)

$40,000.

D)

$45,000.

Page 17

57.

(Table: Total Utility of Income After College Expenses) Look at the table Total Utility

of Income After College Expenses. The Smith family’s expected total utility is _____

utils.

A)

4,175

B)

3,700

C)

3,620

D)

3,210

58.

(Table: Total Utility of Income After College Expenses) Look at the table Total Utility

of Income After College Expenses. What certain income after tuition leaves Mr. and

Mrs. Smith just as well off as their uncertain income after tuition?

A)

$37,500

B)

$38,000

C)

$40,500

D)

$42,500

59.

(Table: Total Utility of Income After College Expenses) Look at the table Total Utility

of Income After College Expenses. Mr. and Mrs. Smith would be willing to pay as

much as _____ for insurance to pay their daughter’s tuition and eliminate the uncertainty

in the family’s income after tuition.

A)

$12,000

B)

$10,000

C)

$8,000

D)

$5,000

60.

(Table: Total Utility of Income After College Expenses) Look at the table Total Utility

of Income After College Expenses. The premium for a fair insurance policy to pay their

daughter’s tuition and eliminate the uncertainty in the Smith family’s income after

tuition would equal:

A)

$12,000.

B)

$10,000.

C)

$8,000.

D)

$5,000.

Page 18

61.

(Table: Total Utility of Income After College Expenses) The Smith family will choose

to purchase insurance:

A)

at any premium.

B)

at a premium for which the reduction in risk leaves the expected value of their

income after tuition the same.

C)

up to but not exceeding the point at which the premium is that of a fair insurance

policy.

D)

at a premium for which the reduction in risk is that of a fair insurance policy.

Use the following to answer questions 62-70:

62.

(Table: Choice with Uncertainty) Look at the table Choice with Uncertainty. Suppose

the probability that the sitcom does not make it to television is 50%, that it makes it to

television but is not the most viewed show in its time slot is 30%, and that it makes it to

television and is the most viewed show in its time slot is 20%. Given this information,

Norman’s expected income is:

A)

$52,500.

B)

$47,500.

C)

$40,000.

D)

$37,500.

Page 19

63.

(Table: Choice with Uncertainty) Look at the table Choice with Uncertainty. Suppose

the probability that the sitcom does not make it to television is 50%, that it makes it to

television but is not the most viewed show in its time slot is 30%, and that it makes it to

television and is the most viewed show in its time slot is 20%. Given this information,

Norman’s expected total utility is _____ utils.

A)

2,000

B)

2,150

C)

2,350

D)

2,650

64.

(Table: Choice with Uncertainty) Look at the table Choice with Uncertainty. Suppose

the probability that the sitcom does not make it to television is 50%, that it makes it to

television but is not the most viewed show in its time slot is 30%, and that it makes it to

television and is the most viewed show in its time slot is 20%. Given this information,

Norman, as a utility maximizer:

A)

should keep his teaching job.

B)

should quit his teaching job and go to Hollywood.

C)

will be indifferent between leaving and staying, because his expected income is the

same whether he stays a teacher or moves to Hollywood.

D)

will be indifferent between leaving and staying, because his expected total utility is

the same whether he stays a teacher or moves to Hollywood.

65.

(Table: Choice with Uncertainty) Look at the table Choice with Uncertainty. Assume

that the probability that the sitcom does not make it to television is 60%, the probability

that it makes it to television but is not the most viewed show in its time slot is 30%, and

the probability that it makes it to television and is the most viewed show in its time slot

is 10%. Norman’s expected income is:

A)

$52,500.

B)

$47,500.

C)

$40,000.

D)

$37,500.

66.

(Table: Choice with Uncertainty) Look at the table Choice with Uncertainty. Suppose

that the probability that the sitcom does not make it to television is 60%, the probability

that it makes it to television but is not the most viewed show in its time slot is 30%, and

that the probability that it makes it to television and is the most viewed show in its time

slot is 10%. Norman’s expected total utility is _____ utils.

A)

2,000

B)

2,150

C)

2,350

D)

2,650

Page 20

67.

(Table: Choice with Uncertainty) Look at the table Choice with Uncertainty. Suppose

the probability that the sitcom does not make it to television is 60%, that it makes it to

television but is not the most viewed show in its time slot is 30%, and that it makes it to

television and is the most viewed show in its time slot is 10%. As a utility maximizer,

Norman:

A)

should keep his teaching job.

B)

should quit his teaching job and go to Hollywood.

C)

will be indifferent between leaving and staying, because his expected income is the

same whether he stays a teacher or moves to Hollywood.

D)

will be indifferent between leaving and staying, because his expected total utility is

the same whether he stays a teacher or moves to Hollywood.

68.

(Table: Choice with Uncertainty) Look at the table Choice with Uncertainty. Suppose

the probability that the sitcom does not make it to television is 30%, that it makes it to

television but is not the most viewed show in its time slot is 50%, and that it makes it to

television and is the most viewed show in its time slot is 20%. Given this information,

Norman’s expected income is:

A)

$52,500.

B)

$47,500.

C)

$40,000.

D)

$37,500.

69.

(Table: Choice with Uncertainty) Look at the table Choice with Uncertainty. Suppose

the probability that the sitcom does not make it to television is 30%, that it makes it to

television but is not the most viewed show in its time slot is 50%, and that it makes it to

television and is the most viewed show in its time slot is 20%. Given this information,

Norman’s expected total utility is _____ utils.

A)

2,000

B)

2,150

C)

2,350

D)

2,650

Page 21

70.

(Table: Choice with Uncertainty) Look at the table Choice with Uncertainty. Suppose

the probability that the sitcom does not make it to television is 30%, that it makes it to

television but is not the most viewed show in its time slot is 50%, and that it makes it to

television and is the most viewed show in its time slot is 20%. Given this information,

Norman, as a utility maximizer:

A)

should keep his teaching job.

B)

should quit his teaching job and go to Hollywood.

C)

will be indifferent between leaving and staying, because his expected income is the

same whether he stays a teacher or moves to Hollywood.

D)

will be indifferent between leaving and staying, because his expected total utility is

the same whether he stays a teacher or moves to Hollywood.

Use the following to answer questions 71-74:

Scenario: Choosing Insurance

The Ramirez family owns three cars and is considering buying insurance to cover the cost of

repairs. They face two possible states: in state 1 their cars need no repairs and their income

available for purchasing other goods and services is $50,000; in state 2 their cars need $10,000

worth of repairs and their income available for purchasing other goods and services is reduced to

$40,000. The probability of repairs is 10%, while the probability of no repairs is 90%.

71.

(Scenario: Choosing Insurance) Refer to the information in the scenario Choosing

Insurance. For $2,000 the Ramirez family can buy insurance that will cover the full cost

of repairs. If family members are risk-averse and want to maximize their expected

utility:

A)

they will buy the insurance.

B)

they will be indifferent between buying and not buying the insurance, since their

expected income for purchasing other goods and services is $48,000 regardless of

what they do.

C)

they will buy the insurance as long as the utility of having a certain income of

$48,000 to buy goods and services other than car repairs is higher than the utility

associated with their expected income without insurance.

D)

they will self-insure.

Page 22

72.

(Scenario: Choosing Insurance) Refer to the information in the scenario Choosing

Insurance. For $1,000 the Ramirez family can buy insurance that will cover the full cost

of repairs. If family members are risk-averse and want to maximize their expected

utility:

A)

they will buy the insurance.

B)

they will be indifferent between buying and not buying the insurance, since their

expected income for purchasing other goods and services is $49,000, regardless of

what they do.

C)

they will buy the insurance as long as the utility of having a certain income of

$48,000 to buy goods and services other than car repairs is higher than the utility

associated with their expected income without insurance.

D)

they will self-insure.

73.

(Scenario: Choosing Insurance) Look at the scenario Choosing Insurance. The premium

on a fair insurance policy for the Ramirez family will be:

A)

$0.

B)

$900.

C)

$1,000.

D)

$2,000.

74.

(Scenario: Choosing Insurance) Refer to the information in the scenario Choosing

Insurance. For $900 the Ramirez family can buy insurance that will cover the full cost

of repairs. If family members are risk-averse and maximize their expected utility:

A)

they will buy the insurance.

B)

they will be indifferent between buying and not buying the insurance, since their

expected income for purchasing other goods and services is $49,100, regardless of

what they do.

C)

they will not buy the insurance, since buying it does not increase their expected

income for purchasing other goods and services.

D)

they will self-insure.

Page 23

Use the following to answer questions 75-77:

75.

(Table: Amy’s Utility Function) Look at the table Amy’s Utility Function. Amy is an

entrepreneur with income of $40,000. Amy is considering development of a new

product. The probability that her new product earns Amy $30,000 in additional income

is 0.5, and the probability that Amy incurs a reduction of $10,000 from her current

income is 0.5. Amy’s expected income after developing her new product is:

A)

$45,000.

B)

$35,000.

C)

$50,000.

D)

$60,000.

76.

(Table: Amy’s Utility Function) Look at the table Amy’s Utility Function. Amy is an

entrepreneur with current income equal to $40,000. Amy is considering development of

a new product. The probability that her new product earns Amy $30,000 in additional

income is 0.5, and the probability that Amy incurs a reduction of $10,000 from her

current income is also 0.5. Amy’s expected utility after developing her new product is

_____ utils.

A)

1,360

B)

860

C)

500

D)

680

Page 24

77.

(Table: Amy’s Utility Function) Look at the table Amy’s Utility Function. Amy is an

entrepreneur with current income equal to $40,000. Amy is considering development of

a new product. The probability that her new product earns Amy $10,000 in additional

income is 0.5, and the probability that Amy incurs a reduction of $10,000 from her

current income is also 0.5. Suppose Amy can buy a fair insurance policy that will

compensate her for any losses. Amy’s premium will be _____, her guaranteed income

will be _____, and her expected utility will be _____ utils.

A)

$5,000; $10,000; 200

B)

$10,000; $30,000; 500

C)

$10,000; $40,000; 620

D)

$30,000; $50,000; 720

78.

Consider the marginal utility of income curves of Hank, Babe, Barry, and Willie. Hank’s

is constant; Babe’s is slightly diminishing; Barry’s is strongly diminishing; and Willie’s

is upward-sloping. All else equal, which of these individuals will be most risk-averse?

A)

Hank

B)

Babe

C)

Barry

D)

Willie

79.

In an efficient allocation of risk:

A)

all risk is eliminated.

B)

those who are most willing to bear risk bear it.

C)

all risk is diversified.

D)

all insurance premiums are equal to the expected value of the claims.

80.

Mary and Bob are trying to decide how much auto insurance to buy. They share the

same expectations of an accident, with the same dollar loss. They also have the same

income levels. However, Mary would rather buy very little insurance, while Bob would

rather buy much more insurance. This suggests that:

A)

Bob is more risk-averse than Mary.

B)

Mary is more risk-averse than Bob.

C)

Bob is risk-averse and Mary is risk-loving.

D)

Mary is risk-averse and Bob is risk-loving.

81.

The total amount of funds that potentially could be paid out by an insurance company is:

A)

the sum of all premiums collected.

B)

the sum of all deductibles received from claims.

C)

the capital at risk.

D)

the company’s liabilities.

Page 25

82.

Suppose the wealth of buyers in the insurance market falls. We would expect insurance

premiums to _____ as the _____ curve shifts _____.

A)

rise; supply; left

B)

fall; supply; right

C)

fall; demand; left

D)

rise; demand; right

83.

Barcelona and Los Angeles are similar, except Barcelona has a good public

transportation system and Los Angeles does not. Auto insurance will probably be more

expensive in _____, since the _____ for insurance is _____.

A)

Barcelona; demand; higher than in Los Angeles

B)

Barcelona; supply; lower than in Los Angeles

C)

Los Angeles; demand; higher than in Barcelona

D)

Los Angeles; supply; lower than in Barcelona

84.

An efficient market for risk, such as an insurance market, is most likely to exist:

A)

when there is a level playing field, so that all participants have approximately the

same wealth and the same degree of risk aversion.

B)

when the sellers of insurance are risk-averse but the purchasers are not.

C)

when there are significant differences between individuals’ wealth levels and

attitudes toward risk.

D)

in the presence of private, or asymmetric, information.

85.

Which of the following is a principle of the insurance industry?

A)

Trade in risk can produce mutual gains.

B)

Diversification can increase risk.

C)

Deductibles add to the problem of moral hazard.

D)

Adverse selection should be used to reduce insurance costs.

86.

People who want to reduce the risk they face may pay other people who are less

sensitive to risk to take on some of their risk. As a result:

A)

a market for risk is illegal.

B)

trade in risk reduces mutual gains.

C)

total risk increases.

D)

people who are willing to accept more risk will purchase from people who are less

willing.

Page 26

87.

The funds that an insurance company may have to pay out are known as the:

A)

fair premium.

B)

capital at risk.

C)

total premium.

D)

deductible.

88.

Which of the following is TRUE if the insurance market is efficient?

A)

The deductibles eliminate moral hazard.

B)

Society as a whole engages in less risky behavior.

C)

It transfers risk from those who most want to get rid of it to those least bothered by

the risk.

D)

Premiums are always kept to the level of a fair insurance policy.

89.

If those who are most willing to bear risk end up bearing it, then we say that the

insurance market is:

A)

experiencing adverse selection.

B)

efficient.

C)

equitable.

D)

showing signs of moral hazard.

90.

As the premium for an insurance policy rises, there is a(n) _____ in the _____

insurance.

A)

decrease; demand for

B)

increase; supply of

C)

decrease; quantity demanded of

D)

decrease; supply of

91.

As the premium for an insurance policy falls, there is an increase in the _____

insurance.

A)

demand for

B)

supply of

C)

quantity demanded of

D)

quantity supplied of

92.

Why might the supply curve of insurance policies shift to the right?

A)

The wealth of the sellers of insurance increases.

B)

Premiums increase.

C)

Risk aversion increases.

D)

Diversification increases.

Page 27

93.

Assume that flood insurance premiums are determined in the competitive market.

Suppose that devastating floods along the Mississippi River have increased the degree

of risk aversion among the insurance investors in this market. The _____ insurance

shifts _____, leading to a(n) _____ in equilibrium premiums and a(n) _____ in the

quantity of insurance bought and sold.

A)

supply of; rightward; decrease; increase

B)

demand for; leftward; decrease; decrease

C)

supply of; leftward; increase; decrease

D)

demand for; rightward; increase; increase

94.

We would consider a tornado and a CEO scandal that hit a construction company on the

same day as _____ events.

A)

independent

B)

dependent

C)

premium

D)

probable

95.

Suppose the probability of a major theft at a hotel is 1%, while the probability of an

earthquake hitting the hotel is 2.3%. The probability that both would occur on the same

day is therefore:

A)

0.00023%.

B)

0.0023%.

C)

0.023%.

D)

2.3%.

Use the following to answer questions 96-97:

Scenario: Buying Shares

Geordie is considering buying shares in two companies, Apple and Microsoft. If he invests

$1,000 in Apple, there is a 40% probability that his investment will be worth only $800 and a

60% probability that it will be worth $1,200 at the end of a year. If he invests $500 in Apple,

there is a 40% probability that his investment will be worth $400 and a 60% probability that it

will be worth $600 at the end of a year. The corresponding numbers for investment in Microsoft

are identical.

Page 28

96.

(Scenario: Buying Shares) Look at the scenario Buying Shares. The probability that

Geordie will sustain a loss (i.e., that his investment at the end of the year will be worth

less than $1,000) is _____ if he invests $1,000 in either Apple or Microsoft and is _____

if he invests $500 apiece in Apple and in Microsoft.

A)

40%; 40%

B)

40%; 16%

C)

80%; 20%

D)

40%; 80%

97.

(Scenario: Buying Shares) Look at the scenario Buying Shares. The probability that

Geordie will make a gain is _____ if he invests $1,000 in either Apple or Microsoft. The

probability that he will make a gain is _____ if he invests $500 apiece in Apple and in

Microsoft.

A)

60%; 60%

B)

60%; 84%

C)

76%; 24%

D)

60%; 36%

98.

The strategy of reducing or eliminating risks by taking a small share in many

independent events or by taking advantage of the predictability associated with large

numbers of independent events is known as:

A)

floating.

B)

specializing.

C)

pooling.

D)

screening.

99.

Which pair of events is NOT independent?

A)

You forget your umbrella; it rains.

B)

There is a heat wave; demand for ice increases.

C)

You didn’t study last night; there is a quiz in your economics class.

D)

You don’t clean your apartment; you have unexpected company.

100.

On any particular day, the probability that it will rain is 25% and that you will be sick is

10%. The probability that both happen on the same day is:

A)

0.25%.

B)

1%.

C)

2.5%.

D)

17.5%.

Page 29

Use the following to answer questions 101-104:

Scenario: Diversification

Morris is considering investing $10,000 in a sunglass company or a rain poncho company. If it is

a rainy year and he invests only in the sunglass company, he will lose $5,000. However, if it is a

rainy year and he invests only in the rain poncho company, he will earn $10,000. If it is a sunny

year and he invests only in the sunglass company, he will earn $10,000; if he invests only in the

rain poncho company, he will lose $5,000 in a sunny year. There is a 50% chance of a sunny

year and a 50% chance of a rainy year.

101.

(Scenario: Diversification) Look at the scenario Diversification. If Morris invests all of

his money in the sunglass company, what is his expected gain or loss?

A)

a loss of $2,500

B)

to break even

C)

a gain of $2,500

D)

a gain of $10,000

102.

(Scenario: Diversification) Look at the scenario Diversification. If Morris invests all of

his money in the rain poncho company, what is his expected gain or loss?

A)

a loss of $2,500

B)

to break even

C)

a gain of $2,500

D)

a gain of $10,000

103.

(Scenario: Diversification) Look at the scenario Diversification. If Morris invests half of

his money in the sunglass company and half in the rain poncho company, what is his

expected gain or loss?

A)

a loss of $2,500

B)

to break even

C)

a gain of $2,500

D)

a gain of $10,000

104.

(Scenario: Diversification) Look at the scenario Diversification. If Morris invests half of

his money in the sunglass company and half in the rain poncho company, he will earn

_____ in a sunny year and _____ in a rainy year.

A)

$2,500; $0

B)

$1,250; $1,250

C)

–$2,500; $2,500

D)

$2,500; $2,500

Page 30

105.

If an insurance company insured 100,000 cars across the state against theft, which of the

following would NOT be true?

A)

The insurance company would be fairly certain of the number of cars that will be

stolen.

B)

The insurance company would be pooling risks.

C)

The insurance company would know with a fair amount of certainty the expected

payoff on the insurance policies.

D)

The insurance company must assume that very few cars will be stolen.

106.

An individual can almost eliminate risk by taking a small share in many independent

events or by taking advantage of the predictability associated with large numbers of

independent events. This is known as:

A)

specializing.

B)

floating.

C)

pooling.

D)

insuring.

107.

The strategy of investing in several assets so that any possible losses are independent

events is:

A)

diversification.

B)

private information.

C)

moral hazard.

D)

adverse selection.

108.

Which pair of events is likely to be positively correlated?

A)

stock prices of computer companies and of tire companies

B)

hurricane damage in Florida and earthquake damage in California

C)

sales of ice cream and cars on a hot summer day

D)

a week-long power outage due to a large hurricane and battery sales

109.

Investors in agricultural corporations face many correlated financial risks. Which of the

following are NOT correlated risks for the agricultural industry?

A)

losses due to drought and changes in the exchange rate with the euro

B)

political events that can lead to fewer crop subsidies and fewer milk supports

C)

recessions and changes in availability of credit

D)

the spread of genetically modified crops and the presence of locusts

Page 31

110.

If relevant events are _____, diversification will NOT reduce risk.

A)

positively correlated

B)

negatively correlated

C)

dependent

D)

independent

111.

Which of the following is a limit to the ability of diversification to reduce risk?

A)

losses due to bad decision making

B)

key raw materials

C)

industrial life cycles

D)

economic losses from bad weather

112.

At the end of the 1980s, Lloyd’s of London was in severe financial trouble because of:

A)

a major recession in Western Europe and the United States.

B)

terror attacks by the IRA.

C)

asbestos claims.

D)

the war in Iraq.

113.

The opportunity to engage in pooling shifts the _____ curve of insurance to the right;

insurance companies will take on _____ risk and charge a _____ premium than without

pooling.

A)

supply; more; lower

B)

demand; more; lower

C)

supply; less; higher

D)

demand; less; higher

114.

Asymmetric, or private, information:

A)

is an important explanation of the variation (or asymmetric performance) of

individuals on standardized tests.

B)

refers to personal information (e.g., regarding gender or ethnicity) that a person is

not obligated to reveal on a job application.

C)

is relevant for an economic transaction and is known only by some of the people

involved in the transaction.

D)

is protected by patents or copyrights.

Page 32

115.

When some people know things that other people don’t know, there is _____; it can

_____ economic decisions.

A)

risk aversion; facilitate

B)

blind strategy; delay

C)

private information; distort

D)

blind trust; diversify

116.

A life insurance company will often require an applicant to submit to a brief physical

exam to assess that person’s basic level of health. This practice is a form of _____ to

lessen the problem of _____.

A)

diversification; moral hazard

B)

signaling; deductibles

C)

reputation; adverse selection

D)

screening; adverse selection

117.

The problem of adverse selection:

A)

occurs when sellers (who know more than buyers about the quality of the product)

deliberately select inferior products to sell.

B)

is also referred to as the moral hazard problem.

C)

can result in an overall increase in the gains from trade.

D)

occurs when an employer fires the wrong person.

118.

In which of the following situations is adverse selection most likely to be a problem?

A)

buying tomatoes at the local farmers’ market

B)

hiring a new manager to work the night shift

C)

buying a new lawnmower

D)

buying a house directly from the previous owner

119.

People faced with adverse selection use _____ to deal with it.

A)

screening

B)

signals

C)

reputation

D)

screening, signals, and reputation

120.

_____ is (are) a strategy(ies) for dealing with adverse selection in the labor market.

A)

Careful screening of an applicant

B)

Examination of signals from an applicant

C)

Obtaining reference letters from an applicant’s previous place of employment

D)

Careful screening of an applicant, examination of signals from an applicant, and

obtaining reference letters from an applicant’s previous place of employment

Page 33

121.

Companies offering life insurance often require a drug test to determine whether the

buyer is a smoker. A smoker must pay a higher premium. This is an example of:

A)

providing the buyer with a personal stake, a way of dealing with moral hazard.

B)

screening to deal with adverse selection.

C)

the demand curve shifting right because of an increase in risk.

D)

pooling of risk with others.

122.

In practice, insurance companies faced with adverse selection use _____ to deal with it.

A)

moral hazard

B)

deductibles

C)

signals

D)

co-pays

123.

Private information leads _____ to expect hidden problems in items offered for sale,

leading to _____ prices and to the best items being kept off the market.

A)

buyers; high

B)

buyers; low

C)

sellers; high

D)

sellers; low

124.

Rhonda would like a better bicycle, and she considers selling her old one by advertising

on the bulletin board in the student center. She decides against it because the used

bicycles listed on the board are underpriced. This describes the problem of:

A)

adverse selection.

B)

moral hazard.

C)

positive correlation.

D)

risk aversion.

125.

Sellers of used cars may have private information to which buyers are not privy. This

leads to all of the following EXCEPT:

A)

lower prices for the cars.

B)

a shortage of used cars on the market.

C)

many mutually beneficial transactions not taking place.

D)

potential sellers willing to sell only at high prices.

Page 34

126.

Used-car dealers will often advertise how long they have been in business as a means of

_____ their long-term _____.

A)

signaling; reputation

B)

screening; customers

C)

insuring; capital at risk

D)

revealing; moral hazard

127.

Moral hazard occurs when individuals:

A)

do not do what is in their own best interest.

B)

know more about acceptable business behavior than other people do.

C)

have an incentive to violate their morals.

D)

know more about their actions than other people do.

128.

Many people smoke and continue poor eating habits because they have health insurance.

This is an example of:

A)

moral hazard.

B)

signaling.

C)

reputation.

D)

adverse selection.

129.

Moral hazard:

A)

occurs when incentives are distorted because an individual knows more about his

or her own actions than other people do.

B)

is a term used to describe the bonuses paid for particularly hazardous jobs (such as

firefighting).

C)

is a term used synonymously with value judgment.

D)

refers to the questionable morality of price gouging in hazardous times (e.g., in the

presence of famines or floods).

130.

Solutions to moral hazard include:

A)

offering salespeople in stores a straight salary rather than a commission on sales.

B)

setting up many stores and restaurants that are part of a national chain as

franchises, with the owner undertaking quite a lot of risk.

C)

allowing property owners to overinsure their buildings.

D)

diversification.

Page 35

131.

Insurance companies deal with the problems of moral hazard by:

A)

always insuring buildings for their full replacement value.

B)

refusing to insure commercial properties against losses caused by fire.

C)

requiring a deductible to provide an incentive for insured individuals to take

reasonable precautions to avoid losses.

D)

charging extra in cases of adverse selection.

132.

Health insurance policies include deductibles:

A)

to minimize moral hazard.

B)

because when it comes to health, most people are risk-averse.

C)

to minimize adverse selection.

D)

because many health insurance companies own hospitals.

133.

You insure your car against theft. Consequently, you rarely lock the car. This describes

the problem of:

A)

adverse selection.

B)

moral hazard.

C)

positive correlation.

D)

risk aversion.

134.

The premium on insurance is often _____ to the deductible, allowing insurance

companies to _____ their customers.

A)

equal; pool

B)

directly related; signal

C)

equal; offer a fair premium to

D)

inversely related; screen

135.

Fire insurance policies include deductibles:

A)

because when it comes to fire, most people are risk-averse.

B)

because it is too expensive to fully insure something against fire.

C)

to minimize moral hazard.

D)

to minimize adverse selection.

136.

Insurance companies attempt to minimize moral hazard by imposing:

A)

premiums.

B)

capital at risk.

C)

adverse selection.

D)

deductibles.

Page 36

137.

McDonald’s and other fast-food chains rely mainly on franchisees to operate the

restaurants to avoid the problem of:

A)

adverse selection.

B)

moral hazard.

C)

insurance.

D)

deductibles.

138.

By offering a menu of policies with different premiums and deductibles, insurance

companies can _____ their customers; for example, a low-risk customer will often buy

insurance with a lower _____ but a higher _____ than a high-risk customer.

A)

signal; deductible; premium

B)

signal; premium; deductible

C)

screen; deductible; premium

D)

screen; premium; deductible

139.

A random variable has a certain future value.

A)

True

B)

False

140.

The future price of one share of General Motors stock is a random variable.

A)

True

B)

False

141.

You go into a grocery store to buy a soft drink. You find that different brands or

varieties have different prices: for a one-liter bottle, Coke costs $1, Pepsi costs $0.95,

and ginger ale costs $1.05. The price of a one-liter bottle of a soft drink at your grocery

store is therefore a random variable.

A)

True

B)

False

142.

The Baker family is faced with two possible states. In state 1, they remain healthy and

incur no medical expenses. In state 2, their medical expenses will be $8,000. There is a

30% chance that state 1 will occur and a 70% chance that state 2 will occur. An

insurance company offers to pay all of their medical expenses for a premium of $6,000.

From the Bakers’ point of view, this is a fair insurance policy.

A)

True

B)

False

Page 37

143.

Jill is a risk-averse expected-utility maximizer. Jack offers her the following bet: he will

toss a coin and pay her $5 if it comes down heads, but if it comes down tails, Jill will

have to pay him $5. Even though heads and tails are equally likely, Jill will not take the

bet.

A)

True

B)

False

144.

A fair insurance policy is one in which the premium equals the expected value of the

claim.

A)

True

B)

False

145.

Risk-averse individuals are willing to make deals that reduce their income to reduce

their risk.

A)

True

B)

False

146.

The wealthy are generally more risk-averse than the poor, since the wealthy have more

to lose.

A)

True

B)

False

147.

A person who has a constant marginal utility of income will be risk-averse.

A)

True

B)

False

148.

The existence of a large and growing gambling industry clearly shows that many people

are risk-loving.

A)

True

B)

False

149.

Through insurance and other devices, the modern economy offers many ways for

individuals to reduce their exposure to risk.

A)

True

B)

False

Page 38

150.

Risk-averse individuals will always buy insurance, regardless of the premiums charged.

A)

True

B)

False

151.

Buying a warranty on a new television is an example of paying to avoid risk.

A)

True

B)

False

152.

An efficient allocation of risk occurs when those most willing to bear risk insure those

who are least willing to bear risk.

A)

True

B)

False

153.

Two possible events are independent if they happen at different times and in different

places.

A)

True

B)

False

154.

The easiest risks to reduce by diversification are those associated with positively

correlated events.

A)

True

B)

False

155.

Private information can cause economic inefficiency by preventing mutually beneficial

transactions.

A)

True

B)

False

156.

Common strategies to deal with the problem of adverse selection include screening

(using observable information to make inferences about private information), signaling

(engaging in actions that reveal one’s private information), and establishing a good

reputation.

A)

True

B)

False

157.

Moral hazard occurs only when people fail to do what is in their best interest.

A)

True

B)

False

Page 39

158.

Adverse selection and moral hazard do not affect the efficiency of the market.

A)

True

B)

False

159.

You have one ticket for a raffle with a grand prize of $1,000. There are two prizes worth

$100 and five prizes worth $20. If only 100 tickets have been distributed, what is the

expected value of your winnings?

160.

You are risk-neutral. You are considering the purchase of a $10 ticket for a raffle with a

grand prize of $1,000. There are two prizes worth $100 and five prizes worth $20. If

you know that only 100 tickets will be sold, should you purchase the ticket?

161.

You are considering the purchase of one ticket for a raffle with a grand prize of $1,000.

There are two prizes worth $100 and five prizes worth $20. If you know that only 100

tickets will be sold, what is the most you would pay for one raffle ticket?

162.

Jaleh has just landed a great job and plans to buy a fancy car worth $100,000. Jaleh is

otherwise risk-averse, but she likes to drive fast, so the probability that she wrecks the

car (a total loss of $100,000) is 0.1. The probability that she has no accidents is 0.9. If

an insurance company were to offer Jaleh a fair insurance policy that completely

replaced her car, how much would she pay? What is the most she would pay for an

insurance policy that would completely replace her car if she totaled it?

Use the following to answer question 163:

163.

(Table: Crop Income) Look at the table Crop Income. Brent is a farmer, and his income

depends on the weather.

A) Calculate Brent’s expected income.

B) Calculate Brent’s expected utility.

Page 40

164.

Most college-bound high school seniors apply for admission to several colleges of

varying reputations and admission standards. Explain how this behavior is similar to

diversification of assets discussed in the chapter.

165.

The seller of a product will sometimes offer a warranty that if the product is defective,

the seller will repair or replace it free of charge within a specified time. What is the role

of product warranties in lessening the problem of asymmetric information (or private

information) and increasing the number of transactions that are made?

166.

Two consumers go to the insurance company to purchase life insurance. James is a

smoker and a police officer who races motorcycles in his spare time. Kathy is a

nonsmoker and a librarian who likes to make quilts in her spare time. The insurance

company knows that both consumers are 40 years old, but the company has no

information about occupations or hobbies. How does the private information in this

situation set up an adverse-selection problem? How could the insurance company lessen

this problem?

167.

You own a shoe store and need a new sales associate. You have a large stack of

applications, but unfortunately you have no idea who is a strong salesperson and who is

a weak one. What kind of problem are you facing and how can you solve it?

168.

Newman has decided to take a road trip in a rental car. He has the minimum amount of

personal car insurance to rent the car, but he decides to pay a little extra to the rental car

company to completely insure himself against any damage to the rental car. How is

there a potential moral hazard due to Newman’s purchase of the additional insurance?

Use the following to answer questions 169-171:

Scenario: Health Costs

Alan is hoping for a healthy year, meaning that he would have zero health costs. Given his

habits, there is a 40% chance that Alan will develop a health issue resulting in $50,000 in health

costs. Assume these are the only two conditions that could exist for Alan in the coming year.

Page 41

169.

(Scenario: Health Costs) Look at the scenario Health Costs. Given the fact that Alan has

a 40% chance of developing a health problem, what is the expected value of Alan’s

health care costs for the coming year?

A)

$0

B)

$50,000

C)

$20,000

D)

$16,000

170.

(Scenario: Health Costs) Look at the scenario Health Costs. Suppose that Alan decides

to change his habits dramatically and as a result decreases the probability of his

developing a health problem such that he now has a 20% chance of becoming ill. What

is the expected value of Alan’s health costs now?

A)

$0

B)

$10,000

C)

$20,000

D)

$2,000

171.

(Scenario: Health Costs) Look at the scenario Health Costs. When Alan’s probability of

developing a health problem decreases, holding everything else constant, Alan’s

expected value of health care costs:

A)

increases.

B)

decreases.

C)

stays constant.

D)

increases, decreases, or stays constant.

172.

If the probability that one person will develop a health problem is greater than that of

another person and if they buy insurance from the same provider, most likely the person

with a higher probability will pay:

A)

the same as the other person.

B)

more than the person with the lower probability.

C)

less than the person with the lower probability.

D)

All people, regardless of probabilities, pay the same amount for insurance.

173.

An individual finds that as his income increases, his total utility also increases but at a

decreasing rate. This can be attributed to:

A)

diminishing marginal utility.

B)

being risk-neutral.

C)

expected values.

D)

efficient allocation of risk.

Page 42

174.

Given uncertainty, individuals attempt to maximize their:

A)

adverse selection.

B)

expected utility.

C)

risk aversion.

D)

consumption.

175.

Suppose for the coming year a family has calculated its expected value for car repairs to

be $3,000. The family decides to buy a car insurance policy that would cover such

claims. This insurance policy would cost a total of $3,000 for the household. This

insurance policy is:

A)

overcharging the family and is not fair.

B)

an example of a fair insurance policy.

C)

undercharging the family.

D)

not appropriate for the family, and they should not buy it.

176.

Organized-gambling venues such as those at Las Vegas tend to attract:

A)

risk-loving individuals only.

B)

even risk-averse people because they are designed to allow individuals to win.

C)

people who may be irrational in their choice of gambling and are often risk-averse.

D)

only professional gamblers.

177.

Lucy decides to buy car insurance because:

A)

she wishes to increase her exposure to risk.

B)

she wants to decrease her exposure to risk.

C)

she is not risk-averse.

D)

her marginal utility is not strongly dependent upon her income.

178.

Risk-averse individuals:

A)

will not gamble at casinos such as those found in Las Vegas.

B)

will pay higher insurance premiums based on their risk aversion.

C)

are a minority of the population.

D)

have upward-sloping marginal utility functions.

179.

Warranties that cover the cost of a repair or replacement will:

A)

decrease the consumer’s expected utility from consuming the good.

B)

increase the consumer’s expected utility from consuming the good.

C)

have no impact on the consumer’s expected utility from consuming the good.

D)

reverse the consumer’s diminishing marginal utility.

Page 43

180.

When Lloyd’s of London offered to provide insurance to merchant ships in the

eighteenth century, Lloyd’s was:

A)

exhibiting risk-averse behavior.

B)

less sensitive to risk than those who requested insurance.

C)

attempting to decrease its exposure to risk.

D)

not very rational in its behavior.

181.

_____ of insurance are often risk-averse, and _____ of insurance are interested in

reducing their exposure to risk.

A)

Demanders; suppliers

B)

Demanders; demanders

C)

Suppliers; demanders

D)

Suppliers; suppliers

Use the following to answer questions 182-183:

Scenario: Flood Area

Suppose you own a home that is estimated to be worth $250,000. You live in a flood plain; as a

result, the probability that you will lose your home to a flood is 30%.

182.

(Scenario: Flood Area) Look at the scenario Flood Area. A flood may occur, causing

you to lose your entire home. In this case, your expected loss resulting from the flood

would be:

A)

$250,000.

B)

$75,000.

C)

$15,000.

D)

$100,000.

183.

(Scenario: Flood Area) Look at the scenario Flood Area. Suppose an insurance company

offers you flood insurance. Most likely this insurance would require a premium

payment:

A)

greater than $250,000.

B)

greater than $75,000.

C)

less than $15,000.

D)

equal to $100,000.

Page 44

184.

In a particular insurance market, there is a decrease in the degree of risk aversion among

buyers. Holding everything else constant, the equilibrium premium will _____ and the

equilibrium quantity of insurance will _____.

A)

increase; increase

B)

decrease; decrease

C)

increase; decrease

D)

decrease; increase

185.

In a particular insurance market, there is a decrease in the degree of risk aversion among

suppliers. Holding everything else constant, the equilibrium premium will _____ and

the equilibrium quantity of insurance will _____.

A)

increase; increase

B)

decrease; decrease

C)

increase; decrease

D)

decrease; increase

186.

As a result of frequent flooding, the insurance market has noted a positive correlation

between flooding and the amount of insurance monies paid out for such floods. Holding

demand for insurance constant, if flooding is expected to continue to be a problem,

flood insurance premiums will most likely:

A)

rise.

B)

fall.

C)

stay the same.

D)

rise, fall, or stay the same.

187.

Suppose a person rolls a typical six-sided die. What is the probability that the die will

come up with a 1 two times in a row?

A)

1 in 6

B)

1 in 3

C)

1 in 36

D)

1 in 12

188.

Suppose a person rolls a typical six-sided die. What is the probability that the die will

come up with a 1 and then a 2?

A)

1 in 3

B)

1 in 36

C)

1 in 6

D)

2 in 5

Page 45

189.

Two individuals make up the auto insurance market. Bonnie drives well, and the

probability of her having an accident is 10% this year. Lisa also drives carefully, and her

probability of having an accident is 5%. What is the probability that Bonnie and Lisa

will both have accidents this year?

A)

0.15%

B)

0.75%

C)

0.005%

D)

0.5%

190.

The pooling of risk is a _____ form of diversification that produces a payoff with a very

_____ risk.

A)

weak; large

B)

weak; small

C)

strong; large

D)

strong; small

191.

Economic growth that is not industry-specific is most likely to:

A)

have no effect on most businesses.

B)

result in many businesses doing well.

C)

result in many businesses not doing well.

D)

affect only a few select businesses.

192.

As a result of frequent flooding, the insurance market has noted a positive correlation

between flooding and the amount of insurance monies paid out for such floods. Holding

demand for insurance constant, if flooding is expected to continue to be a problem:

A)

flood insurance providers will reap greater profits.

B)

more insurance companies will provide such insurance.

C)

flood insurance markets may eventually collapse, since the risks of damage cannot

be offset by diversification.

D)

flood insurance premiums will decrease.

193.

As a result of frequent flooding, the insurance market has noted a positive correlation

between flooding and the amount of insurance monies paid out for such floods.

Moreover, the probability of such flooding has been increasing. As a result,

homeowners in flood plains will find flood insurance:

A)

easy to acquire and relatively inexpensive.

B)

very costly and relatively difficult to find.

C)

premiums have not changed, since the insurance continues to offer the same

coverage.

D)

relatively expensive but easy to acquire.

Page 46

194.

The insurance industry operates on the principles of:

A)

risk trading and diversification.

B)

exploitation and capital accumulation.

C)

moral hazard and irrationality.

D)

adverse selection and diminishing marginal utility.

195.

Toyotas are known for their quality and durability. As a result, compared to other used

car markets, adverse selection in the used Toyota market is:

A)

equally likely.

B)

relatively unlikely.

C)

more likely.

D)

not expected.

196.

When an individual knows more about his or her own actions than other people do,

incentives are distorted, which causes:

A)

moral hazard.

B)

adverse selection.

C)

screening.

D)

signaling.

197.

Moral hazard:

A)

increases the ability of markets to allocate risk efficiently.

B)

decreases the ability of markets to allocate risk efficiently.

C)

has no impact on the ability of markets to allocate risk efficiently.

D)

encourages the provision of 100% insurance coverage.

198.

Moral hazard can be reduced by:

A)

the use of 100% insurance coverage.

B)

imposing a deductible on insurance coverage.

C)

taking away personal stakes for people with private information.

D)

offering fewer incentives to people with private information to act in a less risky

manner.

199.

Insurance premiums often fall substantially if a buyer purchases a policy with a high

deductible, and such a policy is often purchased by individuals who self-identify as:

A)

low-risk drivers.

B)

high-risk drivers.

C)

drivers who do not care what their premium costs are.

D)