101. A business operated at 100% of capacity during its first month, with the following results:

Sales (90 units)

$90,000

Production costs (100 units):

Direct materials

$40,000

Direct labor

20,000

Variable factory overhead

2,000

Fixed factory overhead

7,000

69,000

Operating expenses:

Variable operating expenses

$ 8,000

Fixed operating expenses

1,000

9,000

What is the amount of the contribution margin that would be reported on the variable costing income statement?

102. A business operated at 100% of capacity during its first month, with the following results:

Sales (90 units)

$90,000

Production costs (100 units):

Direct materials

$40,000

Direct labor

20,000

Variable factory overhead

2,000

Fixed factory overhead

7,000

69,000

Operating expenses:

Variable operating expenses

$ 8,000

Fixed operating expenses

1,000

9,000

What is the amount of the income from operations that would be reported on the variable costing income statement?

103. A business operated at 100% of capacity during its first month, with the following results:

Sales (90 units)

$90,000

Production costs (100 units):

Direct materials

$40,000

Direct labor

20,000

Variable factory overhead

2,000

Fixed factory overhead

7,000

69,000

Operating expenses:

Variable operating expenses

$ 8,000

Fixed operating expenses

1,000

9,000

What is the amount of the income from operations that would be reported on the absorption costing income statement?

104. A business operated at 100% of capacity during its first month, with the following results:

Sales (90 units)

$90,000

Production costs (100 units):

Direct materials

$40,000

Direct labor

20,000

Variable factory overhead

2,000

Fixed factory overhead

7,000

69,000

Operating expenses:

Variable operating expenses

$ 8,000

Fixed operating expenses

1,000

9,000

What is the amount of the gross profit that would be reported on the absorption costing income statement?

105. Accountants prefer the variable costing method over absorption costing method for evaluating the

performance of a company because

106. Under which inventory costing method could increases or decreases in income from operations be

misinterpreted to be the result of operating efficiencies or inefficiencies?

107. It would be acceptable to have the selling price of a product just above the variable costs and expenses of

making and selling it in:

108. Costs that can be influenced by management at a specific level of management are called:

109. Which of the following is(are) reason(s) for easy identification and control of variable manufacturing costs

under the variable costing method?

110. Which of the following is not true when determining the selling price for a product?

111. Management will use both variable and absorption costing in all of the following activities except:

112. The relative distribution of sales among various products sold is referred to as the:

113. Management should focus its sales and production efforts on the product or products that will provide

114. The contribution margin ratio is computed as:

115. For a supervisor of a manufacturing department, which of the following costs is controllable?

116. Sales territory profitability analysis can determine profit differences between territories due to

117. Contribution margin reporting can be beneficial for analyzing, which of the following?

118. If sales totaled $200,000 for the current year (10,000 units at $20 each) and planned sales totaled $212,500

(12,500 units at $17 each), the effect of the unit price factor on the change in sales is a:

119. In the contribution margin analysis, the effect of a change in the number of units sold, assuming no change

in unit sales price or unit cost, is referred to as the:

120. In contribution margin analysis, the increase or decrease in unit sales price or unit cost on the number of

units sold is referred to as the:

121. In contribution margin analysis, the quantity factor is computed as:

122. In contribution margin analysis, the unit price or unit cost factor is computed as:

123. If variable cost of goods sold totaled $80,000 for the year (16,000 units at $5.00 each) and the planned

variable cost of goods sold totaled $86,250 (15,000 units at $5.75 each), the effect of the quantity factor on the

change in variable cost of goods sold is:

124. If variable cost of goods sold totaled $80,000 for the year (16,000 units at $5.00 each) and the planned

variable cost of goods sold totaled $86,250 (15,000 units at $5.75 each), the effect of the unit cost factor on the

change in variable cost of goods sold is:

125. If variable selling and administrative expenses totaled $124,000 for the year (80,000 units at $1.55 each)

and the planned variable selling and administrative expenses totaled $136,500 (78,000 units at $1.75 each), the

effect of the quantity factor on the change in variable selling and administrative expenses is:

126. If variable selling and administrative expenses totaled $120,000 for the year (80,000 units at $1.50 each)

and the planned variable selling and administrative expenses totaled $136,500 (78,000 units at $1.75 each), the

effect of the unit cost factor on the change in variable selling and administrative expenses is:

127. If sales totaled $800,000 for the year (80,000 units at $10.00 each) and the planned sales totaled $799,500

(78,000 units at $10.25 each), the effect of the unit price factor on the change in sales is:

128. If sales totaled $800,000 for the year (80,000 units at $10.00 each) and the planned sales totaled $799,500

(78,000 units at $10.25 each), the effect of the quantity factor on the change in sales is:

129. If variable cost of goods sold totaled $90,000 for the year (18,000 units at $5.00 each) and the planned

variable cost of goods sold totaled $86,400 (16,000 units at $5.40 each), the effect of the quantity factor on the

change in variable cost of goods sold is:

130. If variable cost of goods sold totaled $90,000 for the year (18,000 units at $5.00 each) and the planned

variable cost of goods sold totaled $86,400 (16,000 units at $5.40 each), the effect of the unit cost factor on the

change in variable cost of goods sold is:

131. Which of the following causes he difference between the planned and actual contribution margin?

132. The systematic examination of the differences between planned and actual contribution margin is termed

the:

133. Edna’s Chocolates had planned to sell chocolate-covered strawberries for $3.00 each. Due to various

factors, the actual price was $2.75. Edna’s was able to sell 1,000 more strawberries than the anticipated 4,000.

What is (1) the quantity factor and (2) the price factor for sales?

134. On what effects does contribution margin analysis focus?

135. In which of the following types of firms would it be appropriate to prepare contribution margin reporting

and analysis?

136. Which of the following would not be an appropriate activity base for cost analysis in a service firm?

137. Philadelphia Company has the following information for March:

Sales

$450,000

Variable cost of goods sold

240,000

Fixed manufacturing costs

70,000

Variable selling and administrative expenses

52,000

Fixed selling and administrating expenses

35,000

Determine the March (a) manufacturing margin, (b) contribution margin, and (c) income from operations for Philadelphia Company.

138. Cades Company has the following information for March:

Sales

$500,000

Variable cost of goods sold

245,000

Fixed manufacturing costs

85,000

Variable selling and administrative expenses

56,000

Fixed selling and administrating expenses

50,000

Determine the March (a) manufacturing margin, (b) contribution margin, and (c) income from operations for Cades Company.

139. Fixed costs are $10 per unit and variable costs are $25 per unit. Production was 13,000 units, while sales

were 12,000 units. Determine (a) whether variable cost income from operations is less than or greater than

absorption costing income from operations, and (b) the difference in variable costing and absorption costing

income from operations.

(a)

Variable costing income from operations is less than absorption cost income from operations.

(b)

$10,000 ($10 per unit ´ 1,000 units)

140. Fixed costs are $50 per unit and variable costs are $125 per unit. Production was 130,000 units, while

sales were 125,000 units. Determine (a) whether variable cost income from operations is less than or greater

than absorption costing income from operations, and (b) the difference in variable costing and absorption

costing income from operations.

141. The beginning inventory is 10,000 units. All of the units manufactured during the period and 8,000 units

of the beginning inventory were sold. The beginning inventory fixed costs are $50 per unit, and variable costs

are $300 per unit. Determine (a) whether variable costing income from operations is less than or greater than

absorption costing income from operations, and (b) the difference in variable costing and absorption income

from operations.

142. The beginning inventory is 5,000 units. All of the units manufactured during the period and 3,000 units of

the beginning inventory were sold. The beginning inventory fixed costs are $25 per unit, and variable costs are

$55 per unit. Determine (a) whether variable costing income from operations is less than or greater than

absorption costing income from operations, and (b) the difference in variable costing and absorption income

from operations.

143. Variable costs are $80 per unit, and fixed costs are $40,000. Sales are estimated to be 4,000 units. (a) How

much would absorption costing income from operations differ between a plan to produce 4,000 units and a plan

to produce 5,000 units? (b) How much would variable costing income from operations differ between the two

production plans?

144. If variable manufacturing costs are $15 per unit and total fixed manufacturing costs are $200,000, what is

the manufacturing cost per unit if:

(a) 20,000 units are manufactured and the company uses the variable costing concept?

(b) 25,000 units are manufactured and the company uses the variable costing concept?

(c) 20,000 units are manufactured and the company uses the absorption costing concept?

(d) 25,000 units are manufactured and the company used the absorption costing concept?

145. The following data are for Trendy Fashion Apparel:

North

South

Sales volume (units):

Blouses

5,000

5,000

Skirts

4,000

8,000

Sales price per unit:

Blouses

$20.00

$22.00

Skirts

$18.00

$20.00

Variable cost per unit

Blouses

$ 7.00

$ 9.00

Skirts

$ 9.00

$11.00

Determine the contribution margin for (a) Skirts and (b) the South Region.

146. The actual price for a product was $50 per unit, while the planned price was $44 per unit. The volume

increased by 4,000 to 60,000 total units. Determine (a) the quantity factor and (b) the price factor for sales.

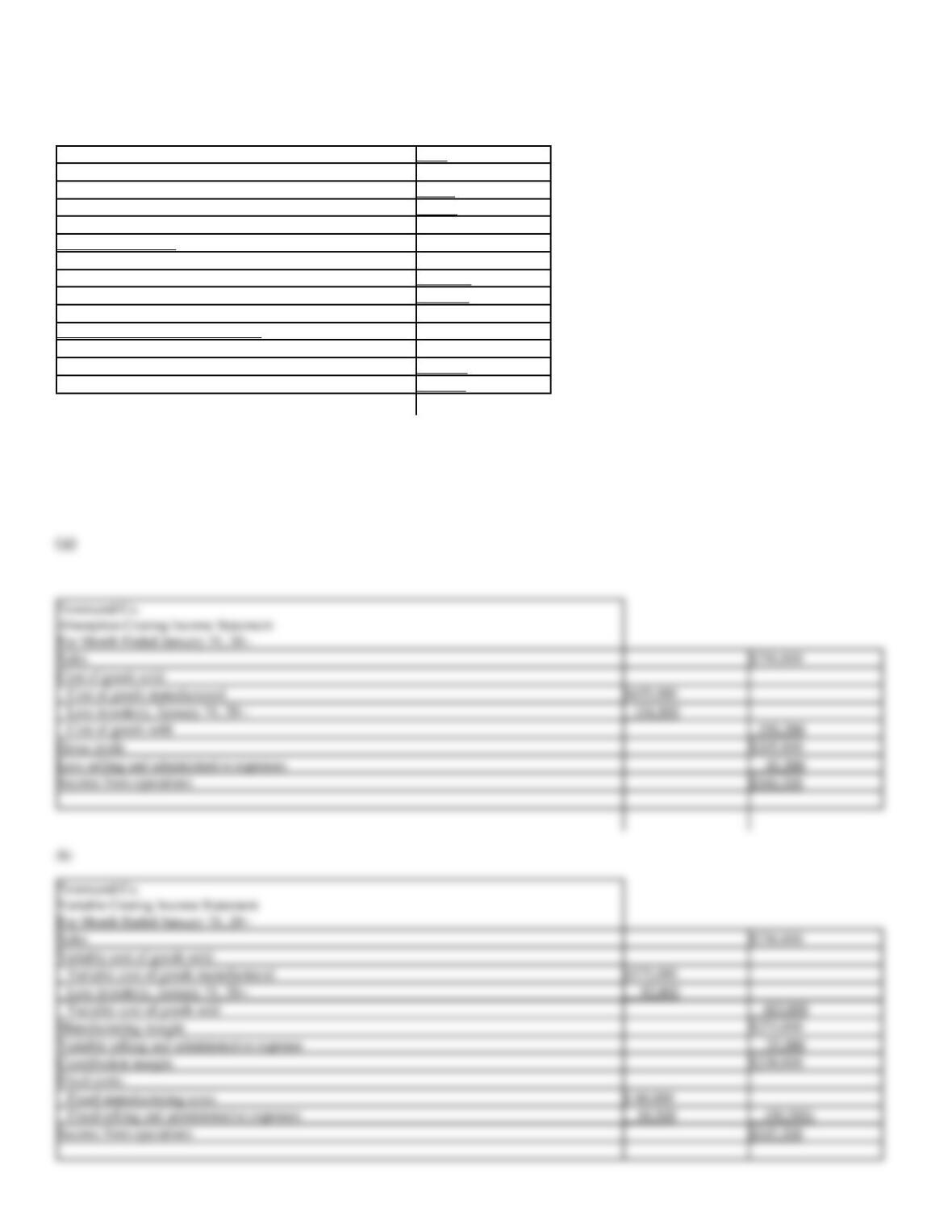

147. On January 1 of the current year, Townsend Co. commenced operations. It operated its plant at 100% of

capacity during January. The following data summarized the results for January:

Units

Production

50,000

Sales ($18 per unit)

42,000

Inventory, January 31

8,000

Manufacturing costs:

Variable

$575,000

Fixed

80,000

Total

$655,000

Selling and administrative expenses:

Variable

$ 35,000

Fixed

10,500

Total

$ 45,500

(a)

Prepare an income statement using absorption costing.

(b)

Prepare an income statement using variable costing.

Sales

$756,000

Cost of goods sold:

Cost of goods manufactured

$655,000

Less inventory, January 31, 20—

104,800

Cost of goods sold

550,200

Gross profit

$205,800

Less selling and administrative expenses

45,500

Income from operations

$160,300

Sales

$756,000

Variable cost of goods sold:

Variable cost of goods manufactured

$575,000

Less inventory, January 31, 20—

92,000

Variable cost of goods sold

483,000

Manufacturing margin

$273,000

Variable selling and administrative expense

35,000

Contribution margin

$238,000

Fixed costs:

Fixed manufacturing costs

$ 80,000

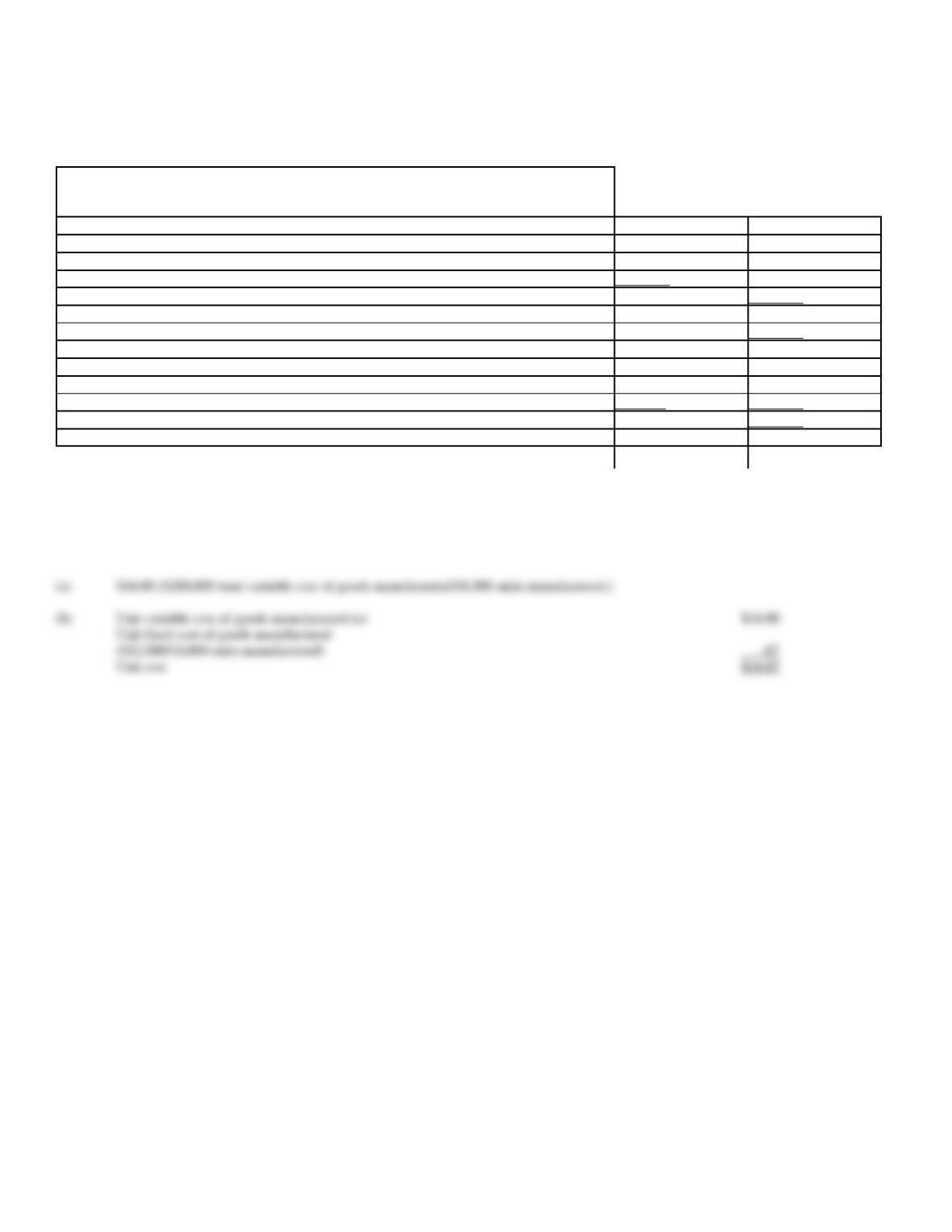

148. On October 31, the end of the first month of operations, Morristown & Co. prepared the following income

statement based on absorption costing:

Morristown & Co.

Absorption Costing Income Statement

For Month Ended October 31, 20-

Sales (2,600 units)

$117,000

Cost of goods sold:

Cost of goods manufactured

$85,500

Less ending inventory (400 units)

11,400

Cost of goods sold

74,100

Gross profit

$ 42,900

Selling and administrative expenses

21,500

Income from operations

$ 21,400

If the fixed manufacturing costs were $42,900 and the variable selling and administrative expenses were $14,600, prepare an income statement using

variable costing.

Morristown & Co.

For Month Ended October 31, 20-

Sales

$117,000

Variable cost of goods sold:

Variable cost of goods manufactured

$42,600

Less ending inventory

(400 units ´ $14.20)

5,680

Variable cost of goods sold

36,920

Manufacturing margin

$ 80,080

Variable selling and administrative expenses

14,600

Contribution margin

$ 65,480

Mixed costs:

Fixed manufacturing costs

$42,900

Fixed selling and administrative expenses

6,900

49,800

Income from operations

$ 15,680

$42,600 variable cost of goods manufactured

= $14.20

3,000 units manufactured

149. Presented below are the major categories or captions that would appear on an income statement prepared in

the variable costing format:

Contribution margin

Fixed costs

Income from operations

Manufacturing margin

Sales

Variable cost of goods sold

Variable selling and administrative expenses

(a)

Arrange the above captions in the proper order in accordance with the variable costing concept.

(b)

Which of the captions represents (1) the difference between sales and the total of all the variable costs and expenses and (2)

the remaining amount of revenue available for fixed manufacturing costs, fixed expenses, and net income?

Variable cost of goods sold

Manufacturing margin

Variable selling and administrative expenses

Fixed costs

Income from operations

(b)

(1)

Contribution margin

150. On August 31, the end of the first year of operations, during which 18,000 units were manufactured and

13,500 units were sold, Olympic Inc. prepared the following income statement based on the variable costing

concept:

Olympic Inc.

Variable Costing Income Statement

For Year Ended August 31, 20—

Sales

$297,000

Variable cost of goods sold:

Variable cost of goods manufactured

$288,000

Less ending inventory

72,000

Variable cost of goods sold

216,000

Manufacturing margin

$ 81,000

Variable selling and administrative expenses

40,500

Contribution margin

$ 40,500

Fixed costs:

Fixed manufacturing costs

$ 12,000

Fixed selling and administrative expenses

10,800

22,800

Income from operations

$ 17,700

Determine the unit cost of goods manufactured, based on (a) the variable costing concept and (b) the absorption costing concept.

(a)

$16.00 ($288,000 total variable cost of goods manufactured/18,000 units manufactured.)

(b)

Unit variable cost of goods manufactured (a)

$16.00

Unit fixed cost of goods manufactured

($12,000/18,000 units manufactured)

.67

Unit cost

$16.67

151. Gyro Company manufactures Products T and W and is operating at full capacity. To manufacture Product

W requires three times the number of machine hours required for Product T. Market research indicates that

1,000 additional units of Product W could be sold. The contribution margin by unit of product is as follows:

Product T

Product W

Sales price

$300

$325

Variable cost of goods sold

235

250

Manufacturing margin

$ 65

$ 75

Variable selling and administrative expenses

25

10

Contribution margin

$ 40

$ 65

Calculate the increase or decrease in total contribution margin if 1,000 additional units of Product W are produced and sold.

Decrease in total contribution margin

$ (55,000)

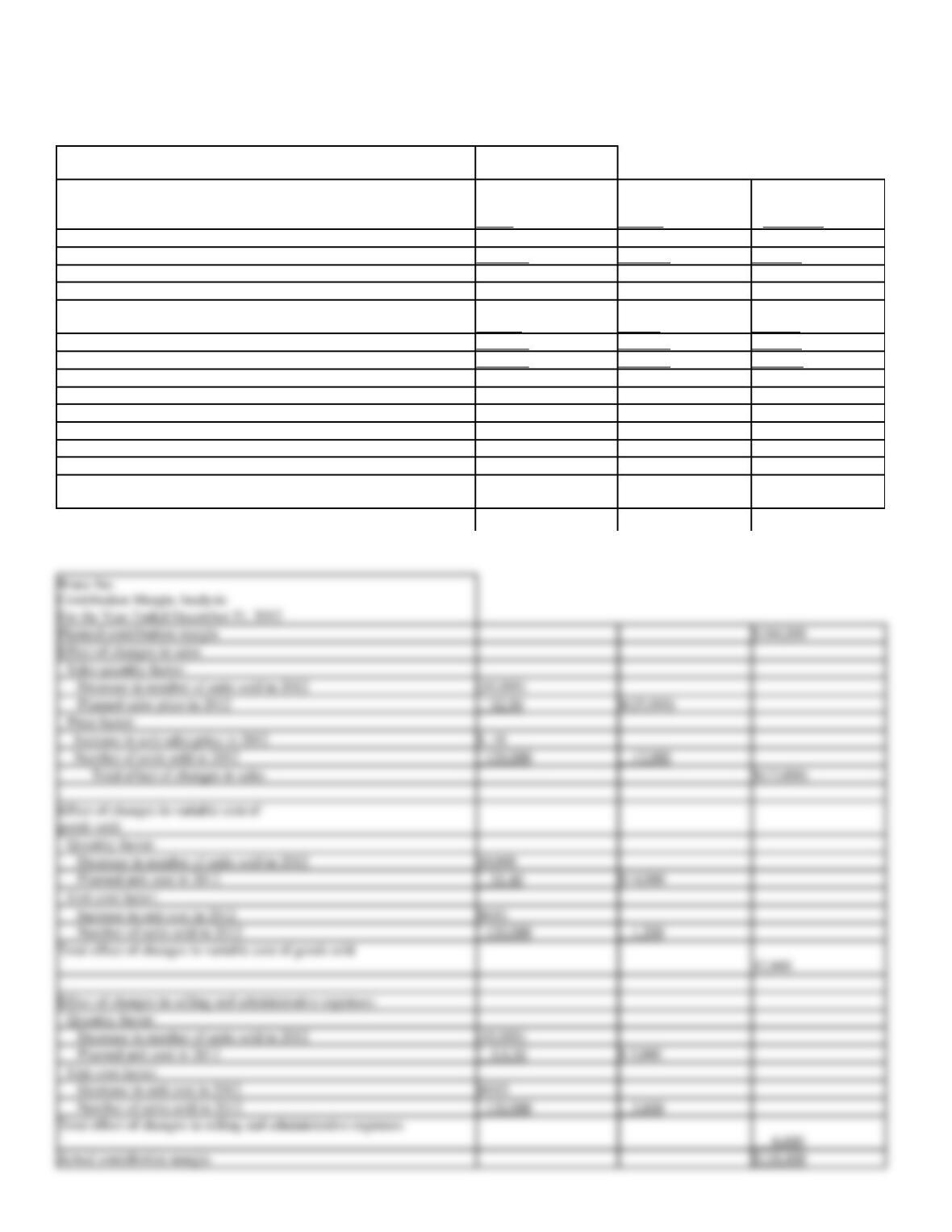

152. Based upon the following data taken from the records of Bruce Inc., prepare a contribution margin analysis

report for the year ended December 31, 2012.

For Year Ended

December 31, 2012

Actual

Planned

Difference

Increase

(Decrease)

Sales

$312,000

$325,000

$(13,000)

Less:

Variable cost of goods sold

$169,200

$182,000

$(12,800)

Variable selling and administrative

expenses

32,400

39,000

(6,600)

Total

$201,600

$221,000

$(19,400)

Contribution margin

$110,400

$104,000

$ 6,400

Number of units sold

120,000

130,000

(10,000)

Per unit:

Sales price

$2.60

$2.50

.10

Variable cost of goods sold

1.41

1.40

.01

Variable selling and administrative

expenses

.27

.30

(.03)

Bruce Inc.

Contribution Margin Analysis

Planned contribution margin

$104,000

Effect of changes in sales

Sales quantity factor:

Decrease in number of units sold in 2012

(10,000)

Planned sales price in 2012

´ $2.50

$(25,000)

Price factor:

Increase in unit sales price in 2012

$ .10

Number of units sold in 2012

´ 120,000

12,000

Total effect of changes in sales

$(13,000)

Effect of changes in variable cost of

goods sold:

Quantity factor:

Decrease in number of units sold in 2012

10,000

Planned unit cost in 2012

´ $1.40

$14,000

Unit cost factor:

Increase in unit cost in 2012

$0.01

Number of units sold in 2012

´ 120,000

1,200

Total effect of changes in variable cost of goods sold

Effect of changes in selling and administrative expenses:

Quantity factor:

Decrease in number of units sold in 2012

(10,000)

Planned unit cost in 2012

´ $ 0.30

$ 3,000

Number of units sold in 2012

´ 120,000

3,600

6,600

153. The Excelsior Company has three salespersons. Average sales price per unit sold, average variable

manufacturing costs per unit, and number of units sold for each salesperson is shown below.

Commissions are according to the following schedule:

Total Sales

Percentage

$0 to 49,999

6%

$50,000 to $52,999

7%

Over $53,000

8%

Salesperson

Mary Q.

John A.

Susan B.

Avg. selling price per unit

$50.00

$65.00

$45.00

Avg. var. mfg. costs per unit

25.00

30.00

35.00

Number of units sold

1,000

750

1,200

Prepare a contribution by salesperson report.

Salesperson

Mary Q.

John A.

Susan B.

Total sales

$50,000

$48,750

$54,000

Variable mfg. cost

25,000

22,500

42,000

Manufacturing margin

$25,000

$26,250

$12,000

Commissions

3,500

2,925

4,320

Contribution margin per salesperson

$21,500

$23,325

$ 7,680

154. The Excelsior Company has three salespersons. Average sales price per unit sold, average variable

manufacturing costs per unit, and number of units sold for each salesperson is shown below.

Commissions are according to the following schedule:

Total Sales

Percentage

$0 to 49,999

6%

$50,000 to $52,999

7%

Over $53,000

8%

Salesperson

Mary Q.

John A.

Susan B.

Avg. selling price per unit

$50.00

$65.00

$45.00

Avg. var. mfg. costs per unit

25.00

30.00

35.00

Number of units sold

1,000

750

1,200

Prepare a contribution by salesperson report.

Salesperson

Mary Q.

John A.

Susan B.

Total sales

$50,000

$48,750

$54,000

Variable mfg. cost

25,000

22,500

42,000

Manufacturing margin

$25,000

$26,250

$12,000

Commissions

3,500

2,925

4,320

Contribution margin per salesperson

$21,500

$23,325

$ 7,680