Corporate Finance, 3e (Berk/DeMarzo)

Chapter 20 Financial Options

20.1 Option Basics

1) Which of the following statements is FALSE?

A) A call option gives the owner the right to buy the asset.

B) A put option gives the owner the right to sell the asset.

C) A financial option contract gives the writer the right (but not the obligation) to purchase or

sell an asset at a fixed price at some future date.

D) A stock option gives the holder the option to buy or sell a share of stock on or before a given

date for a given price.

2) Which of the following statements is FALSE?

A) When a holder of an option enforces the agreement and buys or sells a share of stock at the

agreed-upon price, he is exercising the option.

B) There are two kinds of options. European options allow their holders to exercise the option on

any date up to and including a final date called the expiration date.

C) Because an option is a contract between two parties, for every owner of a financial option,

there is also an option writer, the person who takes the other side of the contract.

D) The price at which the holder buys or sells the share of stock when the option is exercised is

called the strike price or exercise price.

3) Which of the following statements is FALSE?

A) The option buyer, also called the option holder, holds the right to exercise the option and has

a long position in the contract.

B) The market price of the option is also called the exercise price.

C) If the payoff from exercising an option immediately is positive, the option is said to be in-the-

money.

D) As with other financial assets, options can be bought and sold. Standard stock options are

traded on organized exchanges, while more specialized options are sold through dealers.

4) Which of the following statements is FALSE?

A) A holder would not exercise an in-the-money option.

B) The option seller, also called the option writer, sells (or writes) the option and has a short

position in the contract.

C) Because the long side has the option to exercise, the short side has an obligation to fulfill the

contract.

D) When the exercise price of an option is equal to the current price of the stock, the option is

said to be at-the-money.

5) Which of the following statements is FALSE?

A) Options also allow investors to speculate, or place a bet on the direction in which they believe

the market is likely to move.

B) Options where the strike price and the stock price are very far apart are referred to as deep in-

the-money or deep out of-the-money.

C) Call options with strike prices above the current stock price are in-the-money, as are put

options with strike prices below the current stock price.

D) European options allow their holders to exercise the option only on the expiration date—

holders cannot exercise before the expiration date.

6) The writer of a call option has:

A) the obligation to sell a security for a given price.

B) the obligation to buy a security for a given price.

C) the right to sell a security for a given price.

D) the right to buy a security for a given price.

7) The holder of a put option has:

A) the obligation to sell a security for a given price.

B) the right to buy a security for a given price.

C) the right to sell a security for a given price.

D) the obligation to buy a security for a given price.

8) Using options to reduce risk is called:

A) speculation.

B) a naked position.

C) hedging.

D) a covered position.

9) Using options to place a bet on the direction in which you believe the market is likely to move

is called:

A) speculation.

B) hedging.

C) a covered position.

D) a naked position.

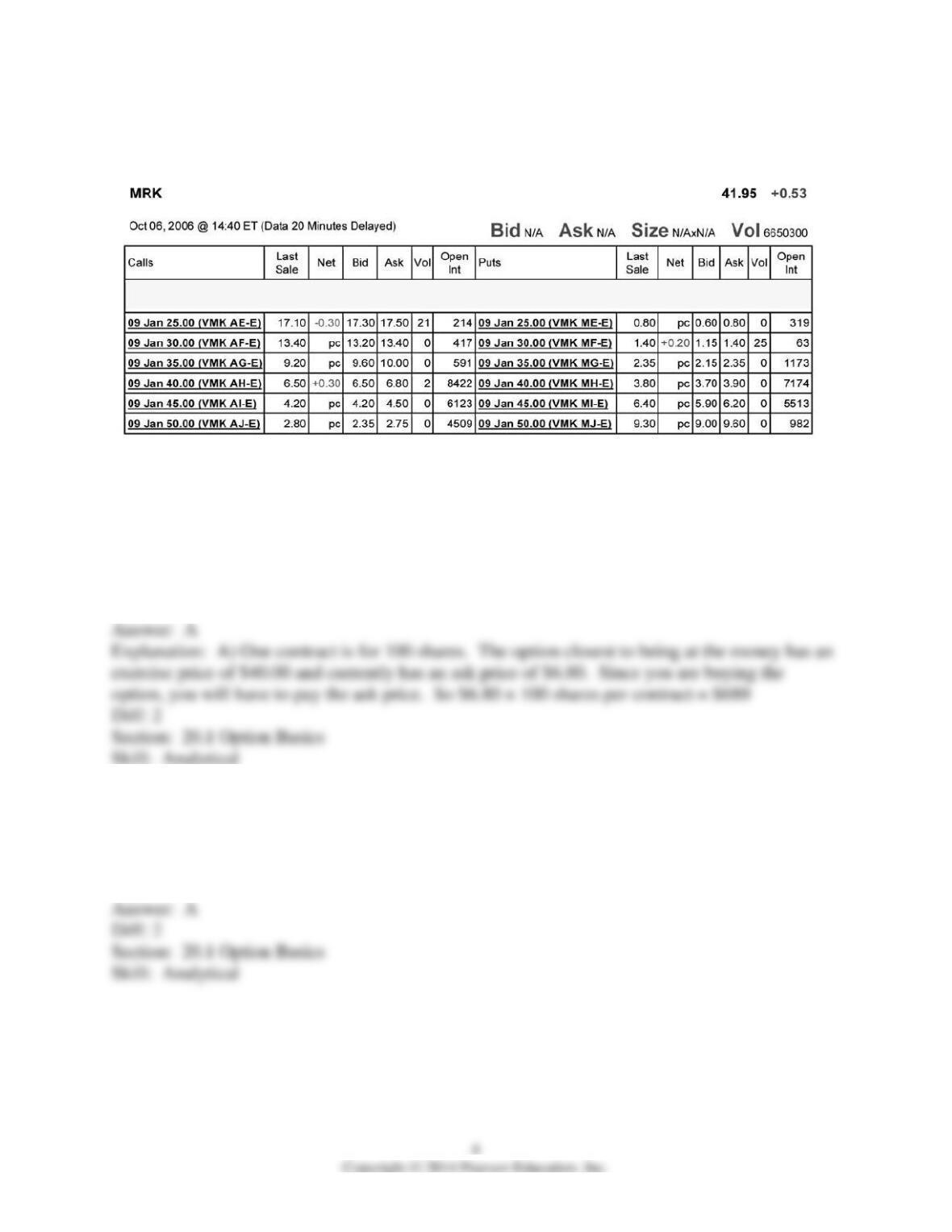

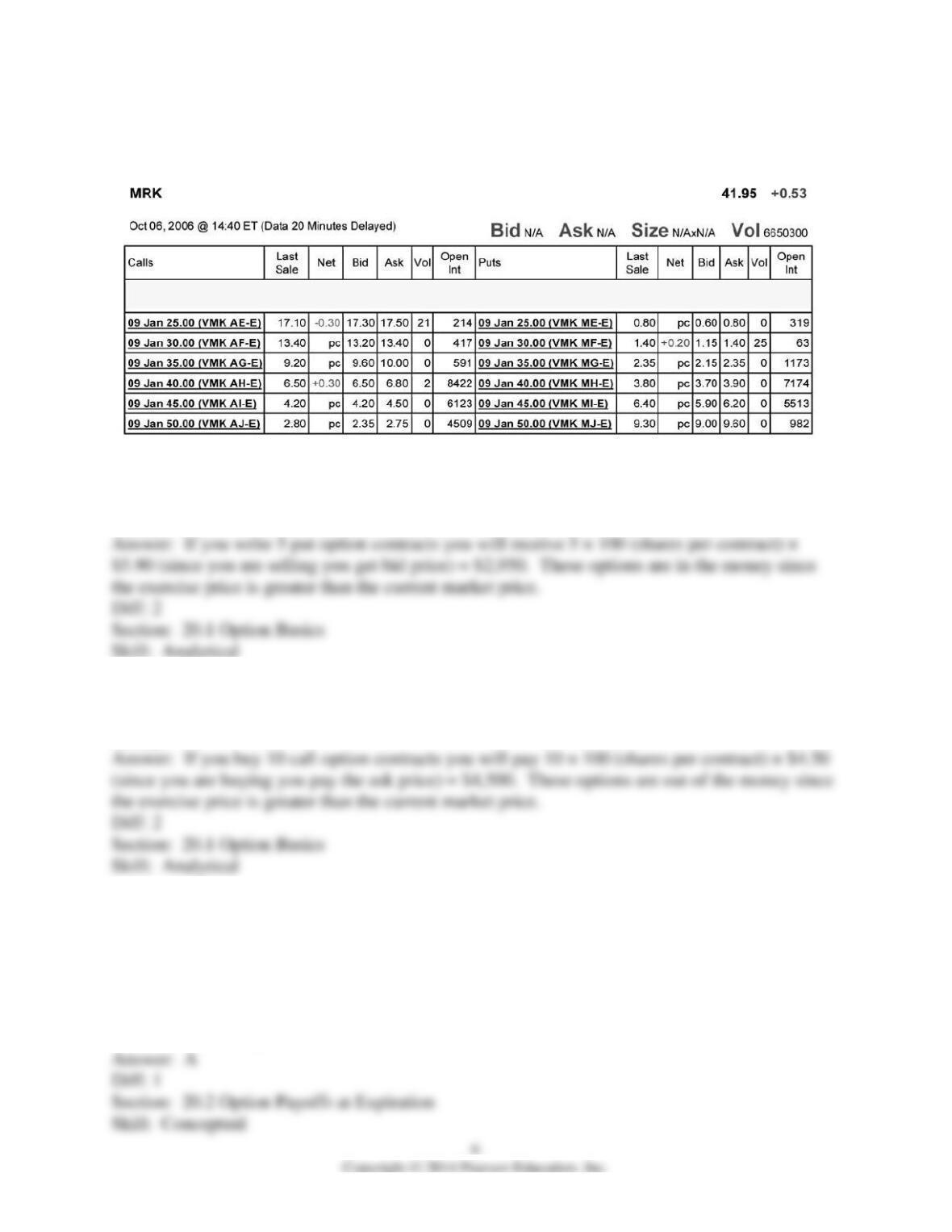

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

10) Assume you want to buy one option contract that with an exercise price closest to being at-

the-money and that expires January 2009. The current price that you would have to pay for such

a contract is:

A) $680

B) $380

C) $650

D) $420

11) The open interest for January 2009 put option that is closest to being at-the-money is:

A) 7174

B) 982

C) 319

D) 8422

12) How many of the January 2009 put options are in the money?

A) 1

B) 3

C) 2

D) 4

13) How many of the January 2009 call options are in the money?

A) 2

B) 4

C) 1

D) 3

14) The market price of an option is called the:

A) American premium.

B) European premium.

C) option premium.

D) exercising premium.

15) As the seller of an option, you receive the:

A) exercise price.

B) strike price.

C) risk premium.

D) option premium.

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

16) You have decided to sell (write) 5 January 2009 put options on Merck with an exercise price

of $45 per share. How much money will you receive and are these contracts in or out of the

money?

17) You have decided to buy 10 January 2009 call options on Merck with an exercise price of

$45 per share. How much will this transaction cost you and are these contracts in or out of the

money?

20.2 Option Payoffs at Expiration

1) The payoff to the holder of a call option is given by:

A) C = max(S – K, 0)

B) C = min(K, 0)

C) C = max(K – S, 0)

D) C = min(K – S, 0)

2) The payoff to the holder of a put option is given by:

A) P = max(K – S, 0)

B) P= max(S – K, 0)

C) P = min(S – K, 0)

D) P = max(K, 0)

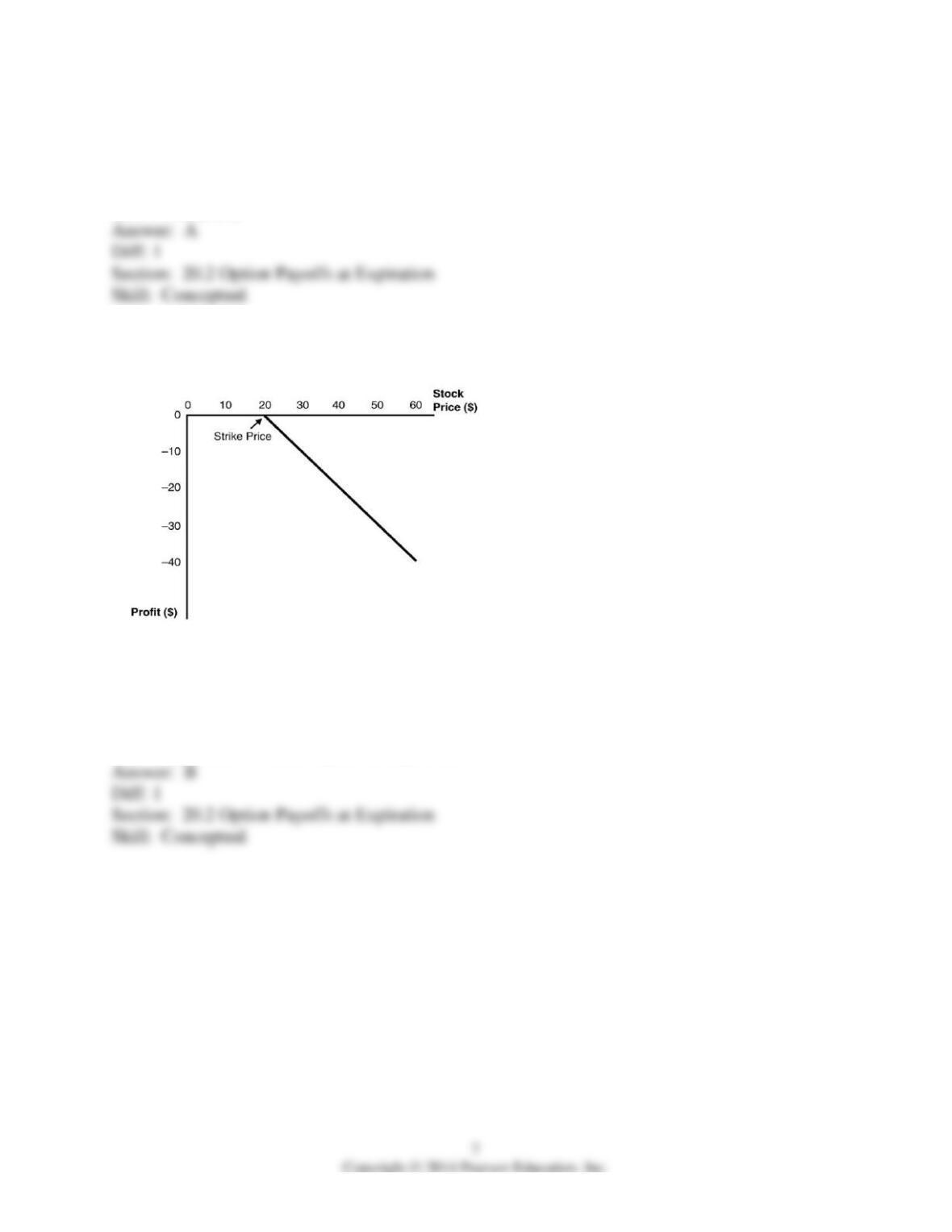

Use the figure for the question(s) below.

3) This graph depicts the payoffs of:

A) a short position in a put option at expiration.

B) a short position in a call option at expiration.

C) a long position in a put option at expiration.

D) a long position in a call option at expiration.

Use the figure for the question(s) below.

4) This graph depicts the payoffs of:

A) a long position in a put option at expiration.

B) a short position in a call option at expiration.

C) a short position in a put option at expiration.

D) a long position in a call option at expiration.

5) An option strategy in which you hold a long position in both a put and a call option with the

same strike price is called:

A) a strangle.

B) portfolio insurance.

C) a butterfly spread.

D) a straddle.

6) Which of the following statements is FALSE?

A) Because a short position in an option is the other side of a long position, the profits from a

short position in an option are just the negative of the profits of a long position.

B) The deeper out-of-the-money the put option is, the less negative its beta, and the higher is its

expected return.

C) Although payouts on a long position in an option contract are never negative, the profit from

purchasing an option and holding it to expiration could well be negative because the payout at

expiration might be less than the initial cost of the option.

D) The put position has a higher return in states with low stock prices; that is, if the stock has a

positive beta, the put has a negative beta.

7) You pay $3.25 for a call option on Luther Industries that expires in three months with a strike

price of $40.00. Three months later, at expiration, Luther Industries is trading at $41.00 per

share. Your profit per share on this transaction is closest to:

A) -$1.00

B) $1.00

C) -$2.25

D) $2.25

8) Graph the payoff at expiration of a short position in a put option with a strike price of $20.

9) You are long both a put option and a call option on Rockwood stock with the same expiration

date. The exercise price of the call option is $40 and the exercise price of the put option is $30.

Graph the payoff of the combination of options at expiration.

20.3 Put-Call Parity

1) Consider the following equation:

C = P + S – PV(K) – PV(Div)

In this equation the term S refers to:

A) the payoff of a zero coupon bond.

B) the strike price of the option.

C) the value of the call option.

D) the stock’s current price.

2) Consider the following equation:

C = P + S – PV(K) – PV(Div)

In this equation the term C refers to:

A) the value of the call option.

B) the stock’s current price.

C) the payoff of a zero coupon bond.

D) the strike price of the option.

3) Consider the following equation:

C = P + S – PV(K) – PV(Div)

In this equation the term K refers to:

A) the value of the call option.

B) the strike price of the option.

C) the price of a zero coupon bond.

D) the stock’s current price.