Exam

Name___________________________________

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

1)

Which of the following statements is false?

1)

A)

You can think of the debt holders as owning the firm and having sold a call option with a

strike price equal to the required debt payment.

B)

If the value of the firm’s assets exceeds the required debt payment, debt holders are fully

repaid.

C)

Viewing debt as an option portfolio is useful as it provides insight into how credit spreads for

risky debt are determined.

D)

Another way to view corporate debt: as a portfolio of riskless debt and a short position in a

call option on the firm‘s assets with a strike price equal to the required debt payment.

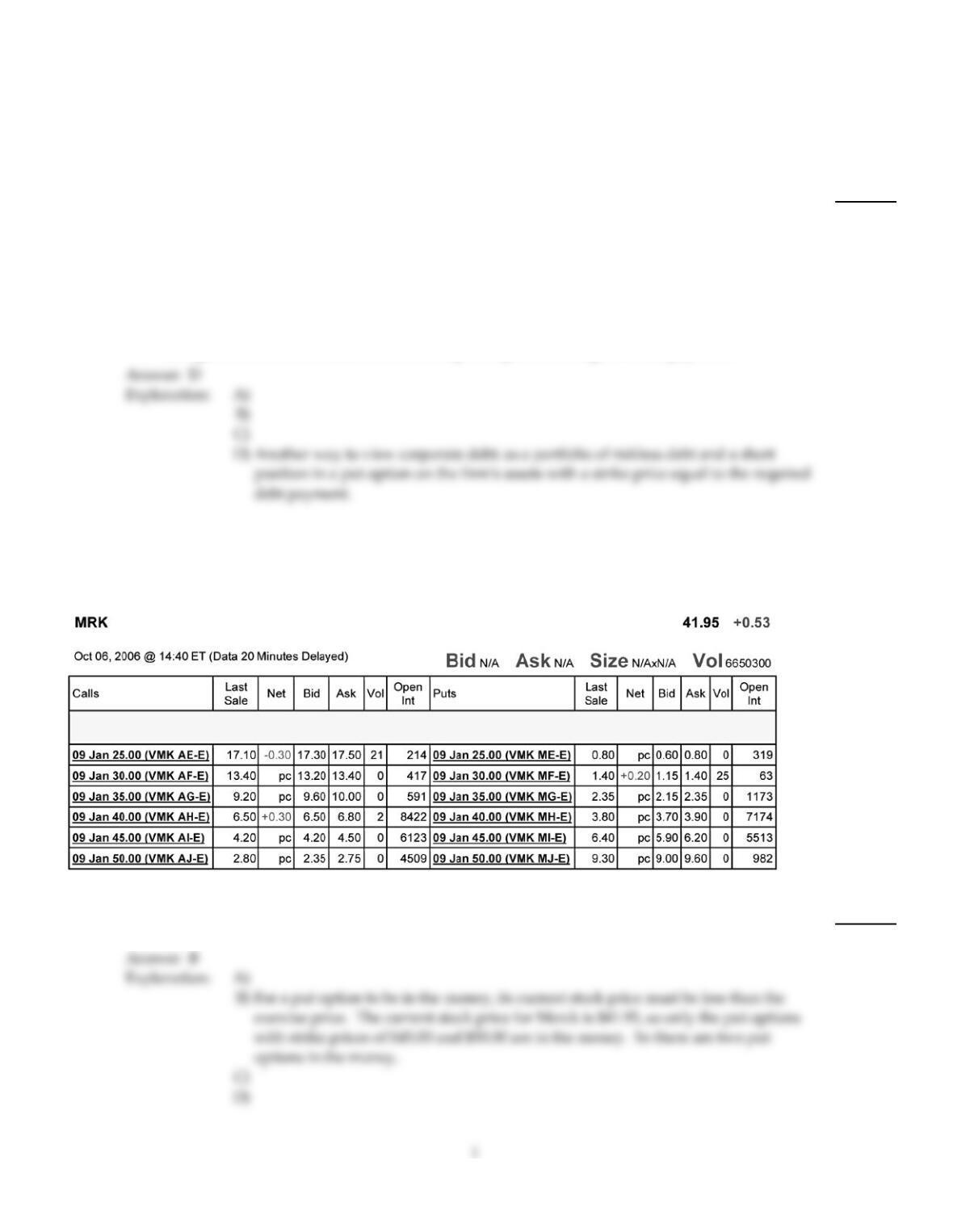

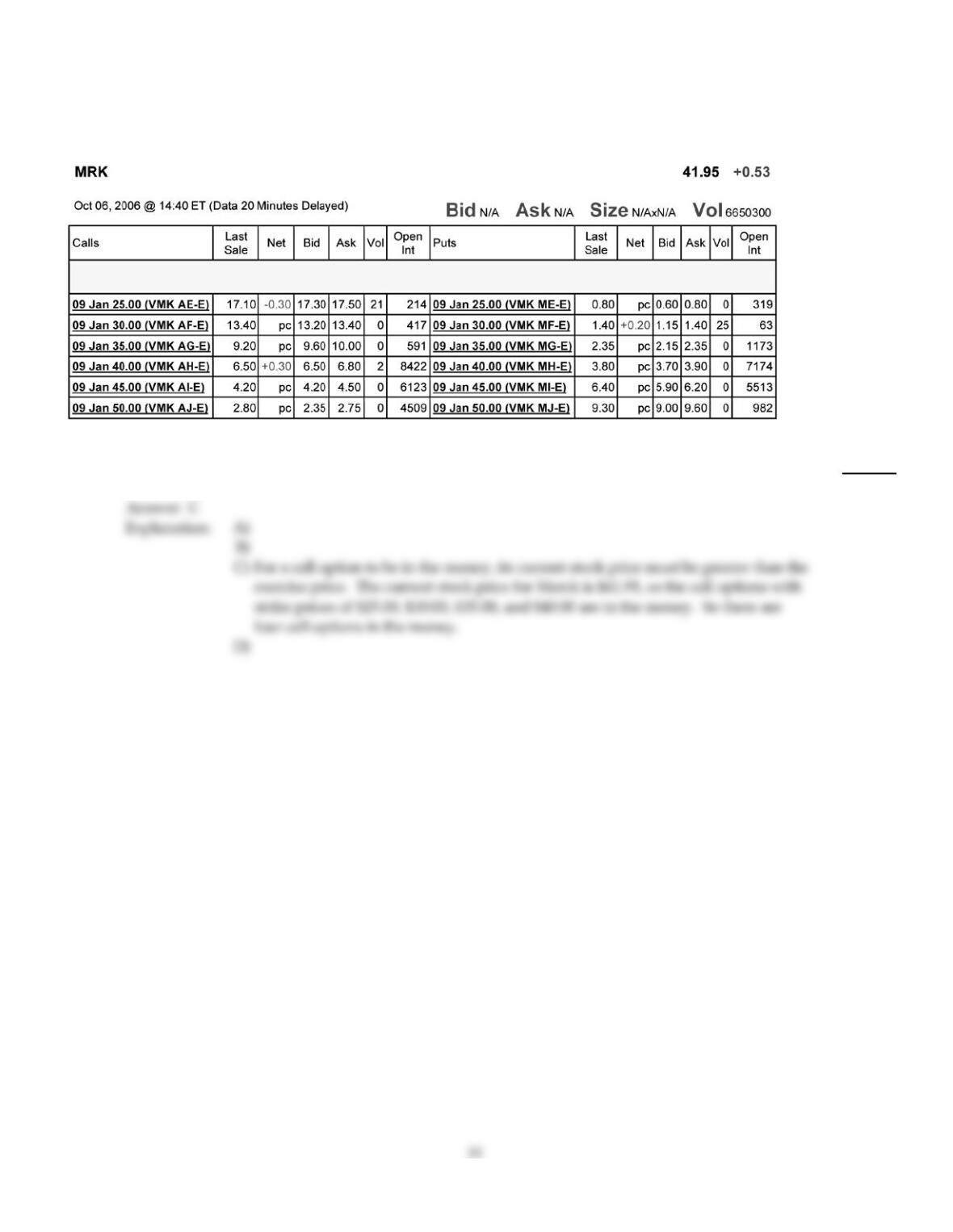

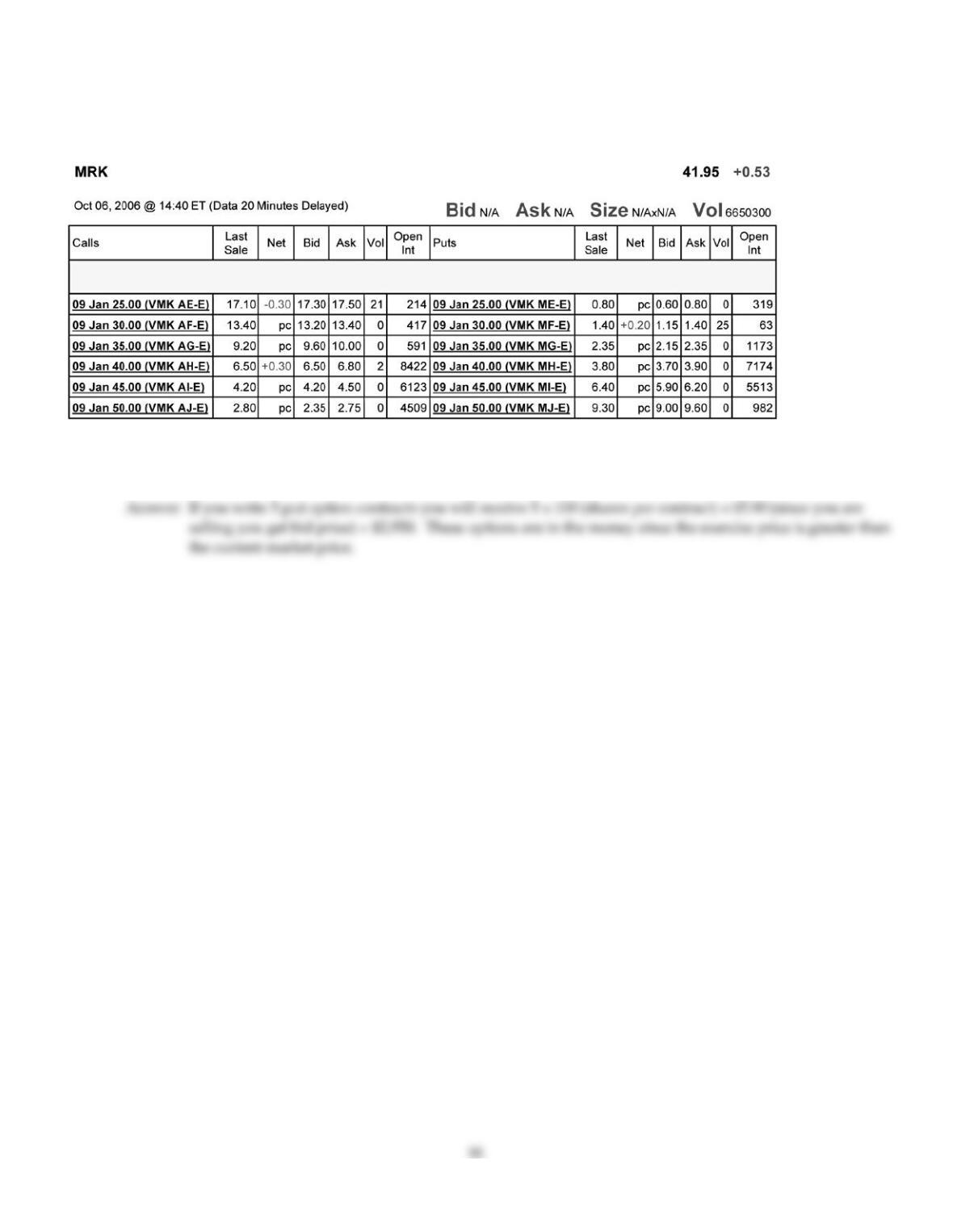

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

2)

How many of the January 2009 put options are in the money?

2)

A)

1

B)

2

C)

3

D)

4

3)

Which of the following statements is false?

3)

A)

When the exercise price of an option is equal to the current price of the stock, the option is

said to be at–the–money.

B)

A holder would not exercise an in–the–money option.

C)

Because the long side has the option to exercise, the short side has an obligation to fulfill the

contract.

D)

The option seller, also called the option writer, sells (or writes) the option and has a short

position in the contract.

4)

The payoff to the holder of a put option is given by:

4)

A)

P=max(K, 0)

B)

P=min(S–K, 0)

C)

P=max(K–S, 0)

D)

P=max(S–K, 0)

5)

Using options to reduce risk is called?

5)

A)

Speculation.

B)

A covered position.

C)

A naked position.

D)

Hedging.

6)

You pay $3.25 for a call option on Luther Industries that expires in three months with a strike price

of $40.00. Three months later, at expiration, Luther Industries is trading at $41.00 per share. Your

profit per share on this transaction is closest to?

6)

A)

–$2.25

B)

$1.00

C)

–$1.00

D)

$2.25

7)

Which of the following statements is false?

7)

A)

The market price of the option is also called the exercise price.

B)

As with other financial assets, options can be bought and sold. Standard stock options are

traded on organized exchanges, while more specialized options are sold through dealers.

C)

If the payoff from exercising an option immediately is positive, the option is said to be

in–the–money.

D)

The option buyer, also called the option holder, holds the right to exercise the option and has

a long position in the contract.

8)

Consider the following equation:

C = S – K + dis(K)+ P – PV(Div)

In this equation, dis(K) +P–PV(Div) tells us

8)

A)

the difference in the price of an American option over a European option because of dividend

capture.

B)

the time value of the option.

C)

the market value of the option.

D)

the intrinsic value of the option.

9)

Which of the following statements is false?

9)

A)

Options also allow investors to speculate, or place a bet on the direction in which they believe

the market is likely to move.

B)

European options allow their holders to exercise the option only on the expiration date

–holders cannot exercise before the expiration date.

C)

Options where the strike price and the stock price are very far apart are referred to as deep

in–the–money or deep out of–the–money.

D)

Call options with strike prices above the current stock price are in–the money, as are put

options with strike prices below the current stock price.

10)

Luther Industries is currently trading for $27 per share. The stock pays no dividends. A one–year

European put option on Luther with a strike price of $30 is currently trading for $2.60. If the

risk–free interest rate is 6% per year, then the price of a one–year European call option on Luther

with a strike price of $30 will be closest to:

10)

A)

$1.95

B)

$2.60

C)

$1.30

D)

$7.10

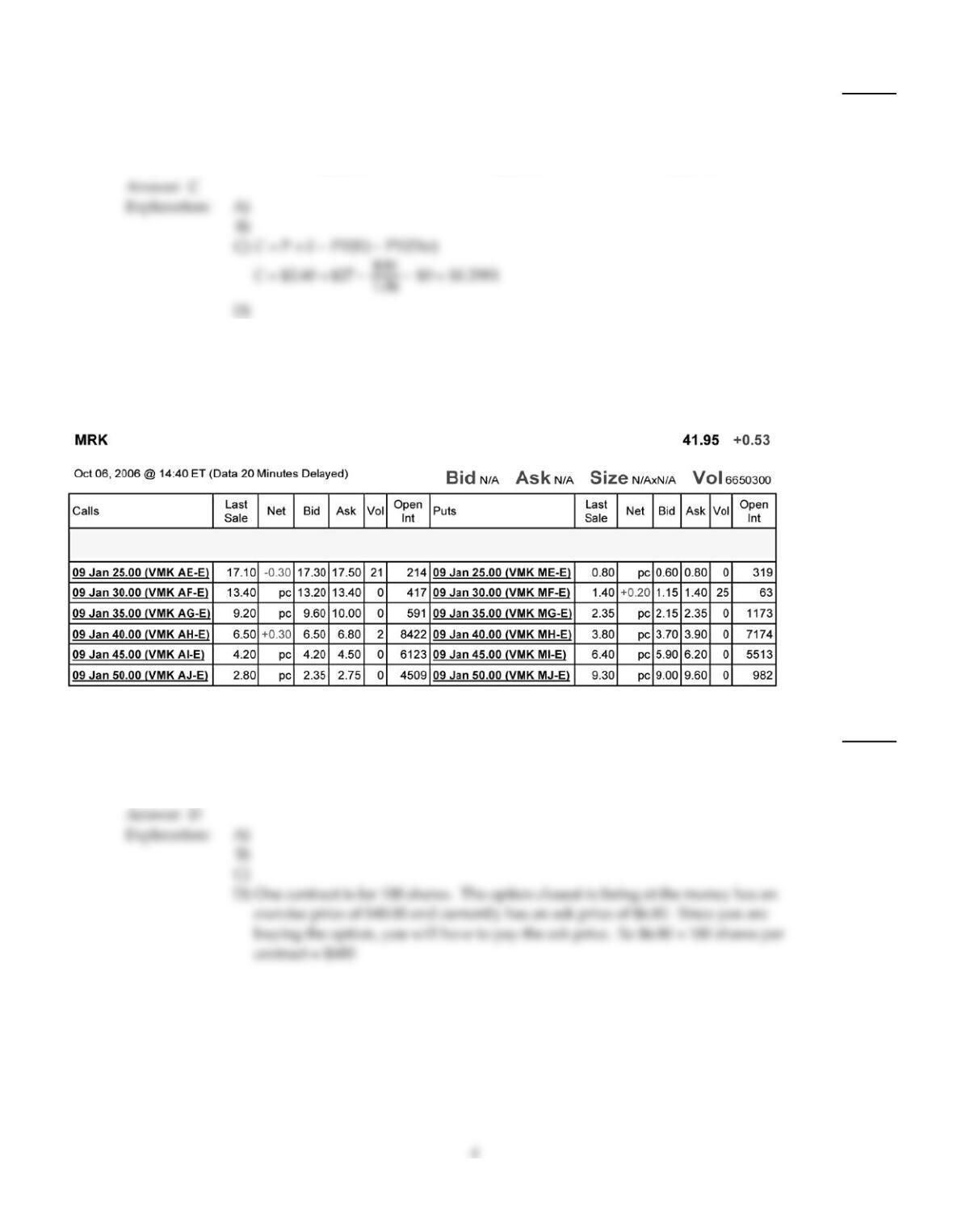

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

11)

Assume you want to buy one option contract that with an exercise price closest to being

at–the–money and that expires January 2009. The current price that you would have to pay for

such a contract is:

11)

A)

$650

B)

$420

C)

$380

D)

$680

12)

An option strategy in which you hold a long position in both a put and a call option with the same

strike price is called

12)

A)

portfolio insurance.

B)

a straddle.

C)

a butterfly spread.

D)

a strangle.

13)

KD Industries stock is currently trading at $32 per share. Consider a put option on KD stock with a

strike price of $30. The intrinsic value of this put option is:

13)

A)

$2

B)

$30

C)

–$2

D)

$0

14)

The holder of a put option has

14)

A)

the right to buy a security for a given price.

B)

the obligation to sell a security for a given price.

C)

the right to sell a security for a given price.

D)

the obligation to buy a security for a given price.

15)

Which of the following statements is false?

15)

A)

Because an option is a contract between two parties, for every owner of a financial option,

there is also an option writer, the person who takes the other side of the contract.

B)

The price at which the holder buys or sells the share of stock when the option is exercised is

called the strike price or exercise price.

C)

When a holder of an option enforces the agreement and buys or sells a share of stock at the

agreed–upon price, he is exercising the option.

D)

There are two kinds of options. European options allow their holders to exercise the option on

any date up to and including a final date called the expiration date.

16)

Which of the following statements is false?

16)

A)

If present value of the dividend payment is large enough, the time value of a European call

option can be negative, implying that its price could be less than its intrinsic value.

B)

It is never optimal to exercise a call option on a dividend paying stock early–you are always

better off just selling the option.

C)

An American call on a non–dividend paying stock has the same price as its European

counterpart.

D)

The price of any call option on a non–dividend–paying stock always exceeds its intrinsic

value.

17)

Which of the following statements is false?

17)

A)

An American option with a later exercise date cannot be worth less than an otherwise

identical American option with an earlier exercise date.

B)

Because an American option cannot be worth less than its intrinsic value, it cannot have a

negative time value.

C)

The value of an option generally decreases with the volatility of the stock.

D)

The intrinsic value is the amount by which the option is currently in–the money or 0 if the

option is out–of–the–money.

18)

Consider the following equation:

C = P + S – PV(K)– PV(Div)

In this equation the term K refers to?

18)

A)

the strike price of the option.

B)

the value of the call option.

C)

the price of a zero coupon bond.

D)

the stocks current price.

It is never optimal to exercise a call option on a non–dividend paying stock early

19)

Which of the following statements is false?

19)

A)

For a given strike price, the value of a call option is higher if the current price of the stock is

higher, as there is a greater likelihood the option will end up in–the–money.

B)

Put–call parity gives the price of a European call option in terms of the price of a European

put, the underlying stock, and a zero–coupon bond.

C)

The value of an otherwise identical call option is higher if the strike price the holder must pay

to buy the stock is higher.

D)

Because a put is the right to sell the stock, puts with a lower strike price are less valuable.

20)

Consider the following equation:

C = P + S – PV(K)– PV(Div)

In this equation the term C refers to

20)

A)

the strike price of the option.

B)

the value of the call option.

C)

the stocks current price.

D)

the payoff of a zero coupon bond.

21)

Which of the following statements is false?

21)

A)

A put option gives the owner the right to sell the asset.

B)

A financial option contract gives the writer the right (but not the obligation) to purchase or

sell an asset at a fixed price at some future date.

C)

A stock option gives the holder the option to buy or sell a share of stock on or before a given

date for a given price.

D)

A call option gives the owner the right to buy the asset.

A financial option contract gives the owner the right (but not the obligation) to

22)

Which of the following will not increase the value of a put option?

22)

A)

An increase in the exercise price

B)

An increase in the time to maturity

C)

A decrease in the stocks volatility

D)

A decrease in the stock price

23)

The writer of a call option has

23)

A)

the obligation to buy a security for a given price.

B)

the right to buy a security for a given price.

C)

the obligation to sell a security for a given price.

D)

the right to sell a security for a given price.

24)

KD Industries stock is currently trading at $32 per share. Consider a put option on KD stock with a

strike price of $30. The maximum value of this put option is:

24)

A)

$30

B)

$0

C)

$32

D)

$2

25)

Using options to place a bet on the direction in which you believe the market is likely to move is

called?

25)

A)

Speculation.

B)

Hedging.

C)

A naked position.

D)

A covered position.

26)

Which of the following statements is false?

26)

A)

The deeper out–of–the–money the put option is, the less negative its beta, and the higher is its

expected return.

B)

The put position has a higher return in states with low stock prices; that is, if the stock has a

positive beta, the put has a negative beta.

C)

Although payouts on a long position in an option contract are never negative, the profit from

purchasing an option and holding it to expiration could well be negative because the payout

at expiration might be less than the initial cost of the option.

D)

Because a short position in an option is the other side of a long position, the profits from a

short position in an option are just the negative of the profits of a long position.

The deeper out–of–the–money the put option is, the less negative its beta, and the

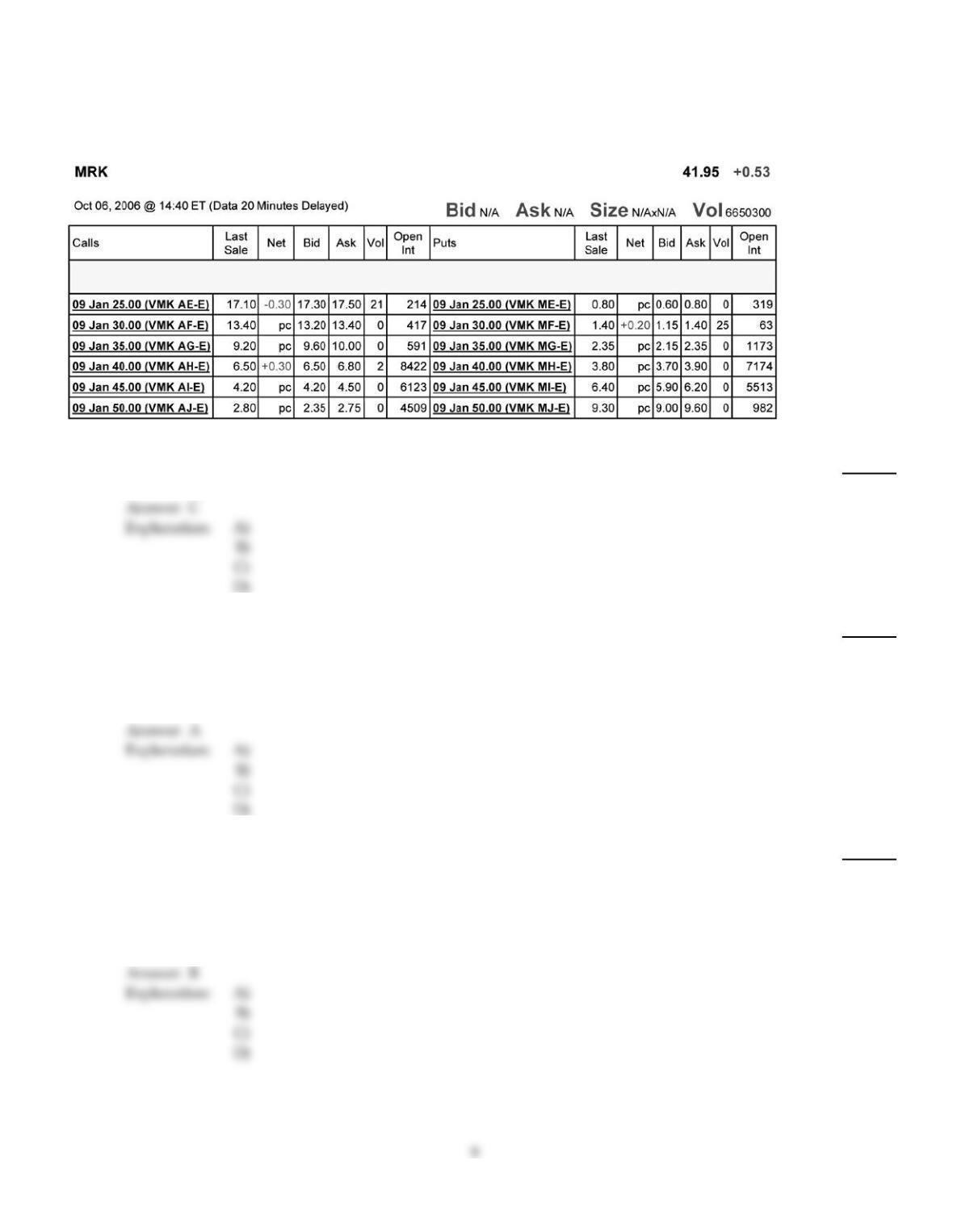

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

27)

The open interest for January 2009 put option that is closest to being at–the–money is:

27)

A)

982

B)

8422

C)

7174

D)

319

28)

Which of the following statements is false?

28)

A)

A European option cannot be worth less than its American counterpart.

B)

The intrinsic value of an option is the value it would have if it expired immediately.

C)

A put option cannot be worth more than its strike price.

D)

Put options increase in value as the stock price falls.

29)

Consider the following equation:

C = S – K + dis(K) +P

In this equation, S – K tells us

29)

A)

the market value of the option.

B)

the intrinsic value of the option.

C)

the option spread.

D)

the time value of the option.

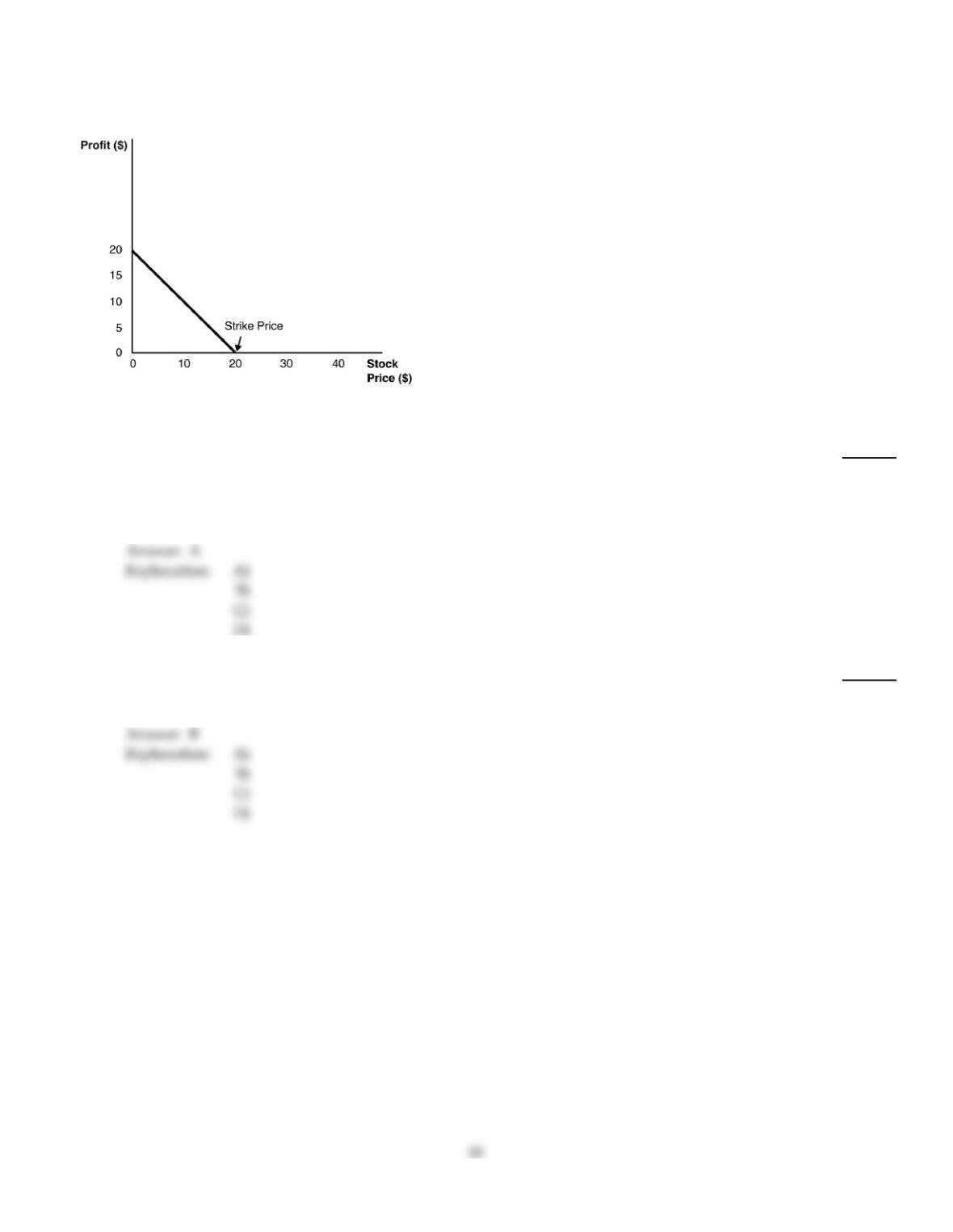

Use the figure for the question(s) below.

30)

This graph depicts the payoffs of a

30)

A)

a long position in a put option at expiration.

B)

a short position in a put option at expiration.

C)

a long position in a call option at expiration.

D)

short position in a call option at expiration.

31)

The payoff to the holder of a call option is given by:

31)

A)

C=max(K–S, 0)

B)

C=max(S–K, 0)

C)

C=min(K– S, 0)

D)

C=min(K, 0)

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

32)

How many of the January 2009 call options are in the money?

32)

A)

2

B)

3

C)

4

D)

1

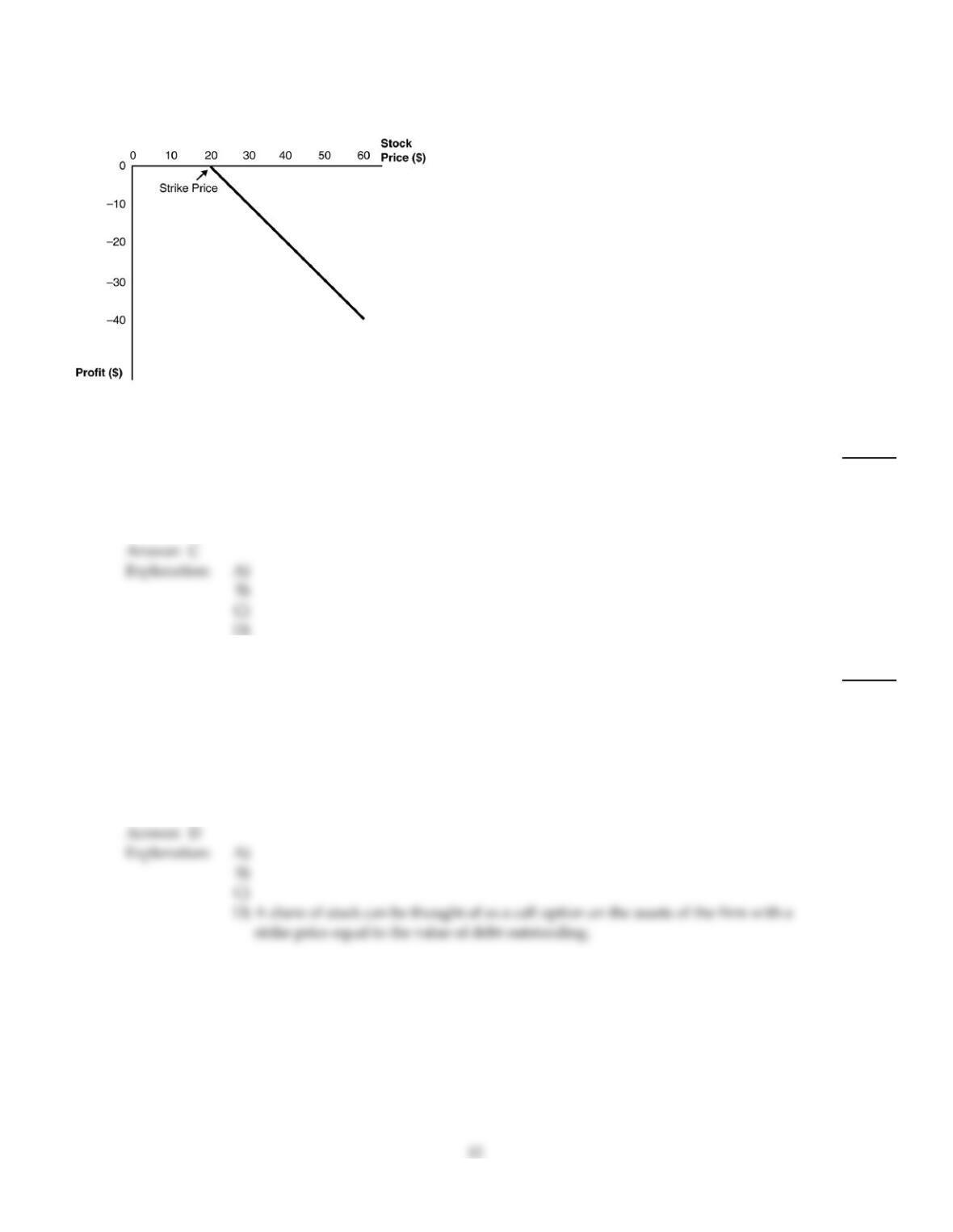

Use the figure for the question(s) below.

33)

This graph depicts the payoffs of a

33)

A)

a long position in a call option at expiration.

B)

a long position in a put option at expiration.

C)

short position in a call option at expiration.

D)

a short position in a put option at expiration.

34)

Which of the following statements is false?

34)

A)

In the context of corporate finance, equity is at–the money when a firm is close to bankruptcy.

B)

Because the price of equity is increasing with the volatility of the firm’s assets, equity holders

benefit from a zero–NPV project that increases the volatility of the firm’s assets.

C)

The option price is more sensitive to changes in volatility for at–the–money options than it is

for in–the–money options.

D)

A share of stock can be thought of as a put option on the assets of the firm with a strike price

equal to the value of debt outstanding.

35)

Consider the following equation:

C = P + S – PV(K)– PV(Div)

In this equation the term S refers to

35)

A)

the payoff of a zero coupon bond.

B)

the value of the call option.

C)

the strike price of the option.

D)

the stocks current price.

ESSAY. Write your answer in the space provided or on a separate sheet of paper.

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

36)

You have decided to buy 10 January 2009 call options on Merck with an exercise price of $45 per share. How

much will this transaction cost you and are these contracts in or out of the money?

37)

You are long both a put option and a call option on Rockwood stock with the same expiration date. The exercise

price of the call option is $40 and the exercise price of the put option is $30. Graph the payoff of the combination

of options at expiration.

38)

Describe the conditions when it would be optimal to exercise an American Call and an American Put option

prior to their expiration.

39)

Rose Industries is currently trading for $47 per share. The stock pays no dividends. A one–year European call

option on Luther with a strike price of $45 is currently trading for $7.45. If the risk–free interest rate is 6% per

year, then calculate the price of a one–year European put option on Luther with a strike price of $45.

40)

Graph the payoff at expiration of a short position in a put option with a strike price of $20.

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

41)

You have decided to sell (write) 5 January 2009 put options on Merck with an exercise price of $45 per share.

How much money will you receive and are these contracts in or out of the money?

Answer Key

Testname: C20

17

Answer Key

Testname: C20

18

Answer Key

Testname: C20

19

Answer Key

Testname: C20