Chapter 2 – Analyzing Transactions

206. On December 1, JumpStart Company provides $2,800 in services to clients.

(a) Journalize this event as if the clients had paid cash at the time the services were rendered.

(b)(1) Journalize this event as if the clients had been rendered the services on account.

(b)(2) Assume that the clients paid $1,200 of the amount on account on December 30. Journalize this transaction.

Chapter 2 – Analyzing Transactions

207. Analyze the effect of the following transactions on the accounting equation.

(a)

The company paid $725 to a vendor for supplies purchased previously on account.

(b)

The company performed $850 of services and billed the customer.

(c)

The company received a utility bill for $395 and will pay it next month.

(d)

The company paid dividends of $145.

(e)

The company paid $315 in salaries to its employees.

(f)

The company collected $730 of cash from its customers on account.

Some of the possible effects of a transaction on the accounting equation are listed below:

(1)

Assets, Dr.; Assets, Cr.

(2)

Assets, Dr.; Stockholders’ Equity, Cr.

(3)

Assets, Dr.; Liabilities, Cr.

(4)

Assets, Dr.; Revenues, Cr.

(5)

Liabilities, Dr.; Assets, Cr.

(6)

Dividends, Dr.; Assets, Cr.

(7)

Expenses, Dr.; Assets, Cr.

(8)

Expenses, Dr.; Liabilities, Cr.

Put the appropriate letter next to each transaction.

Chapter 2 – Analyzing Transactions

208. Prepare a journal entry on October 12 for the fees earned on account, $14,600. Omit explanation.

Oct. 12

Accounts Receivable

209. State for each account whether it is likely to have (a) debit entries only, (b) credit entries only, or (c) both debit and

credit entries when recording business transactions during the month. Also, indicate the normal balance of each account.

1.

Fees Earned

4.

Supplies

2.

Utilities Expense

5.

Cash

3.

Accounts Payable

6.

Accounts Receivable

6. Both debit and credit entries, normal debit balance

Chapter 2 – Analyzing Transactions

210. The bookkeeper for Brockton Industries prepared the following journal entries and posted the entries to the general

ledger as indicated in the T accounts presented. Assume that the dollar amounts and the descriptions of the entries are

correct.

July

3

Accounts Receivable

1,000

Service Revenue

1,000

Customers were billed for services

completed.

11

Cash

500

Accounts Receivable

500

Payment is received from a customer

billed for services on July 3.

12

Office Supplies

600

Accounts Payable

600

Purchased office supplies on account;

payment is due in 30 days.

25

Office Furniture

700

Cash

700

Payment is made for office furniture

received on July 25.

ACCOUNTS RECEIVABLE

SERVICE REVENUE

7/3

1,000

7/3

1,000

7/11

500

CASH

ACCOUNTS PAYABLE

7/11

500

7/25

700

7/12

600

OFFICE SUPPLIES

OFFICE FURNITURE

7/12

600

7/25

700

Required: If you assume that all journal entries have been recorded correctly, use the above information to:

(1) Identify the postings to the general ledger that were made incorrectly.

(2) Describe how each incorrect posting should have been made.

Chapter 2 – Analyzing Transactions

211. Journalize the entries to correct the following errors:

(a)

A purchase of supplies for $500 on account was recorded and posted as a debit to

Supplies for $200 and as a credit to Accounts Receivable for $200.

(b)

A receipt of $2,500 from fees earned was recorded and posted as a debit to Fees

Earned for $2,500 and a credit to Cash for $2,500.

Accounts Receivable

212. On November 30, the company accountant discovers that $550 of a transaction recording the purchase of office

supplies was really office equipment. Prepare the journal entry to correct this situation.

Nov. 30

Office Equipment

213. The following errors took place in journalizing and posting transactions:

a.

Dividends were recorded as a debit to Office Expense and a credit to Cash.

b.

Accounts receivable payment for $7,800 was recorded as a debit to Cash and a

credit to Fees Earned.

Journalize the entries to correct the errors. Omit the explanations.

Chapter 2 – Analyzing Transactions

Fees Earned

214. For each of the following errors, considered individually, indicate whether the error would cause the trial balance

totals to be unequal. If the error would cause the trial balance totals to be unequal, indicate whether the debit or credit

total is higher and by how much.

A.

Payment of a cash dividend $6,800 was journalized and posted as a debit of

$8,600 to Salaries Expense and a credit of $8,600 to Cash.

B.

A fee of $9,780 earned was debited to Accounts Receivable for $7,980 and

credited to Fees Earned for $9,780.

C.

A payment of $3,000 to a creditor was posted as a credit of $3,000 to Accounts

Payable and a credit of $3,000 to Cash.

The totals are equal.

The totals are unequal. The credit total is higher by $1,800.

The totals are unequal. The credit total is higher by $6,000.

Chapter 2 – Analyzing Transactions

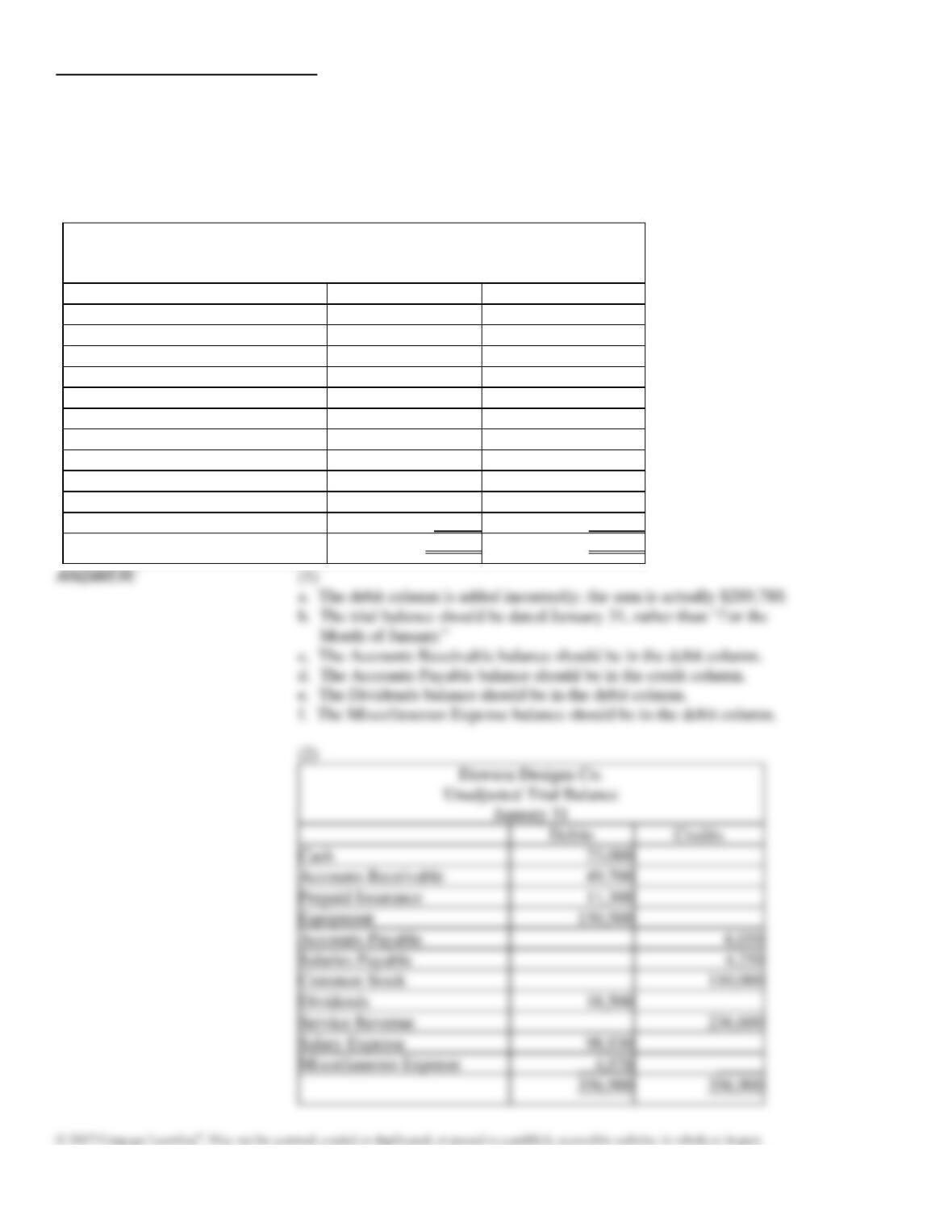

215. Below is the unadjusted trial balance for Dawson Designs.

REQUIRED:

(1) Identify the errors in the trial balance. All accounts have normal balances.

(2) Prepare a corrected trial balance.

Dawson Designs Co.

Unadjusted Trial Balance

For the Month of January

Debits

Credits

Cash

23,000

Accounts Receivable

49,700

Prepaid Insurance

11,300

Equipment

150,500

Accounts Payable

6,050

Salaries Payable

4,250

Common Stock

110,000

Dividends

18,500

Service Revenue

236,600

Salary Expense

98,930

Miscellaneous Expense

4,970

424,020

424,020

Cash

Accounts Receivable

Prepaid Insurance

Equipment

Accounts Payable

Salaries Payable

Common Stock

Dividends

Service Revenue

Salary Expense

Miscellaneous Expense

Chapter 2 – Analyzing Transactions

216. Prepare a trial balance, listing the following accounts in proper sequence. The accounts (all normal balances) were

taken from the ledger of Sophie Designs Co. on April 30.

Accounts Payable

$ 4,100

Rent Expense

$11,500

Accounts Receivable

3,450

Salary Expense

14,000

Cash

6,700

Fees Earned

45,425

Common Stock

17,800

Supplies

3,125

Dividends

7,500

Supplies Expense

1,700

Equipment

14,500

Utilities Expense

4,000

Miscellaneous Expense

850

Cash

Accounts Receivable

Supplies

Equipment

Accounts Payable

Common Stock

Dividends

Fees Earned

Salary Expense

Rent Expense

Utilities Expense

Supplies Expense

Miscellaneous Expense

Chapter 2 – Analyzing Transactions

217.

(a)

List the errors in the following trial balance. All accounts have normal

balances.

(b)

What would be the new totals of the trial balance after errors are corrected?

What would be the balance of Accounts Receivable?

Winslow’s Auto Body

Trial Balance

For Month Ending April 30

Cash

19,475

Accounts Receivable

?

Supplies

1,000

Equipment

15,000

Prepaid Insurance

500

Accounts Payable

2,500

Common Stock

17,000

Dividends

1,000

Fees Earned

49,600

Salary Expense

14,500

Rent Expense

9,000

Utilities Expense

1,400

Supplies Expense

3,900

Miscellaneous Expense

250

55,000

81,575

(a)

(1)

(2)

The Cash balance should be a debit.

(3)

The Accounts Receivable balance is missing.

(4)

The Supplies balance should be a debit.

(5)

The Prepaid Insurance balance should be a debit and this account should

follow Supplies.

(6)

The Common Stock balance should be a credit.

(7)

The Dividends balance should be a debit.

(8)

Rent Expense should be a debit.

(9)

Utilities Expense should appear after Supplies Expense.

(10)

The trial balance does not balance.

($69,100 total credits − $66,025 corrected debits).

Chapter 2 – Analyzing Transactions

218. Answer the following questions for each of the errors listed below, considered individually:

(a)

Did the error cause the trial balance totals to be unequal?

(b)

What is the amount of the difference between the trial balance totals (where

applicable)?

(c)

Which of the trial balance totals, debit or credit, is the larger (where

applicable)?

Present your answers in columnar form, using the following headings:

Error

Totals

Difference in Totals

Larger of Totals

(identifying number)

(equal or unequal)

(amount)

(debit or credit)

Errors:

(1)

A dividend of $3,000 cash to shareholders was recorded by a debit of $3,000 to

Salary Expense and a credit of $3,000 to Cash.

(2)

A $650 purchase of supplies on account was recorded as a debit of $1,650 to

Equipment and a credit of $1,650 to Accounts Payable.

(3)

A purchase of equipment for $3,450 on account was not recorded.

(4)

A $870 receipt on account was recorded as a $870 debit to Cash and a $780

credit to Accounts Receivable.

(5)

A payment of $1,530 cash on account was recorded only as a credit to Cash.

(6)

Cash sales of $8,500 were recorded as a credit of $8,500 to Cash and a credit

of $8,500 to Fees Earned.

(7)

The debit to record a $4,000 cash receipt on account was posted twice; the

credit was posted once.

(8)

The credit to record a $300 cash payment on account was posted twice; the

debit was posted once.

(9)

The debit balance of $7,400 in Accounts Receivable was recorded in the trial

balance as a debit of $7,200.

Difference in Totals

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

Chapter 2 – Analyzing Transactions

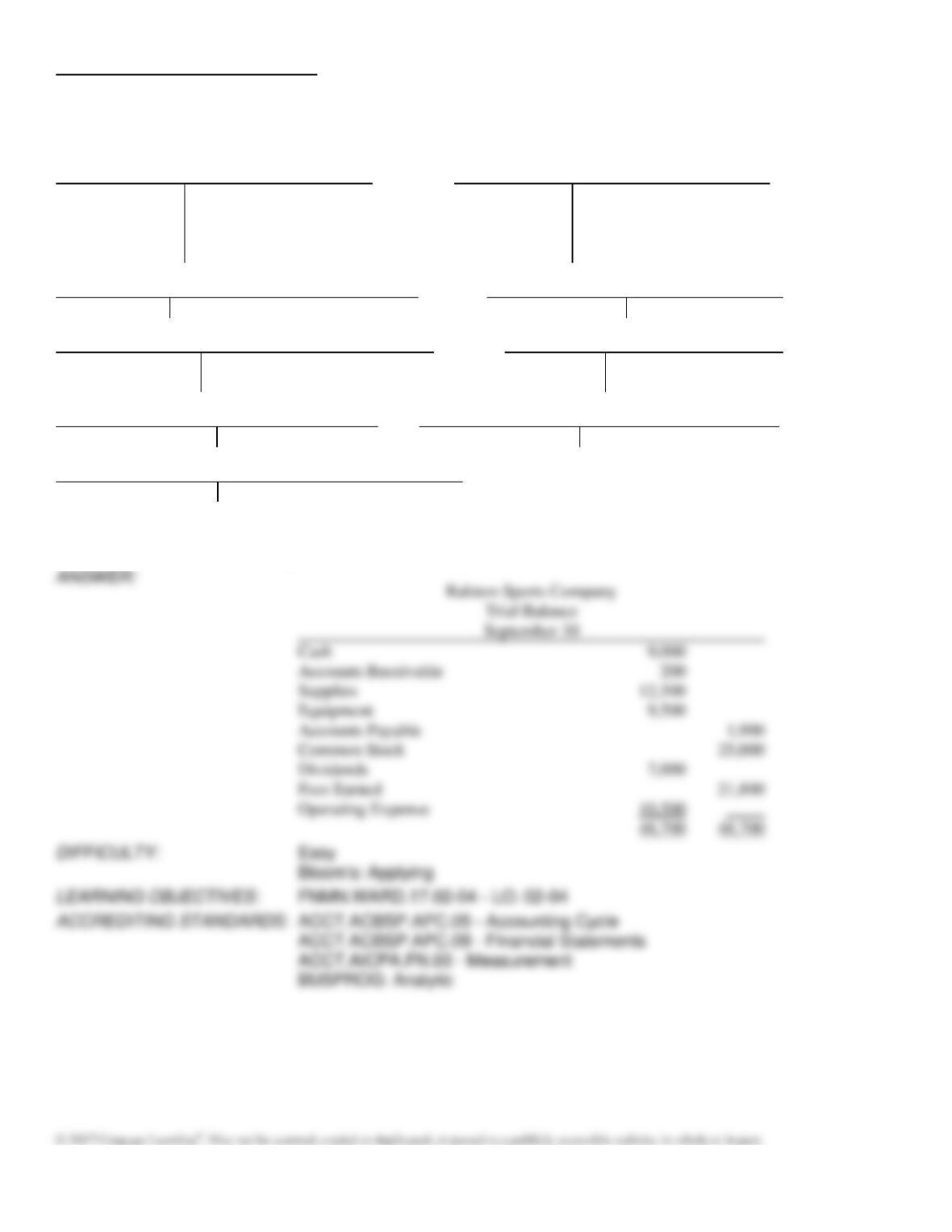

Use the information below to answer the question that follows.

All nine transactions for Ralston Sports Co. for September, the first month of operations, are recorded in the following T

accounts:

Cash

Common Stock

(1)

25,000

(3)

12,500

(1)

25,000

(7)

11,900

(5)

7,600

(9)

9,700

(6)

10,500

(8)

7,000

Accounts Receivable

Dividends

(4)

9,900

(9)

9,700

(8)

7,000

Supplies

Fees Earned

(3)

12,500

(4)

9,900

(7)

11,900

Equipment

Operating Expense

(2)

9,500

(6)

10,500

Accounts Payable

(5)

7,600

(2)

9,500

219. Prepare a trial balance, listing the accounts in their proper order.

Cash

Accounts Receivable

Supplies

Equipment

Accounts Payable

Common Stock

Dividends

Fees Earned

Operating Expense

Chapter 2 – Analyzing Transactions

220. Lewis Company has a condensed income statement as shown:

Year 2

Year 1

Sales

$178,400

$162,500

Wage expenses

$100,000

$ 92,500

Rent expenses

33,000

30,000

Utilities expenses

30,000

25,000

Total operating expenses

$163,000

$147,500

Net income

$ 15,400

$ 15,000

REQUIRED:

Prepare a horizontal analysis of Lewis Company’s income statements. Comment on the trends, both favorable and

unfavorable.

Sales

Wage expenses

Rent expenses

Utilities expenses

Total operating expenses

expenses, resulting in a small increase in net income.

221. Nebraska Technologies has a condensed income statement as shown:

Year 2

Year 1

Sales

$158,400

$162,500

Wage expenses

$ 80,000

$ 92,500

Rent expenses

28,000

30,000

Utilities expenses

30,000

25,000

Total operating expenses

$138,000

$147,500

Net income

$ 20,400

$ 15,000

REQUIRED:

Prepare a horizontal analysis of Nebraska Technologies’ income statements. Comment on the trends, both favorable and

unfavorable.

Chapter 2 – Analyzing Transactions

Match each of the following accounts with its proper account group from groups listed below.

a.

Assets

b.

Liabilities

c.

Stockholders’ Equity

d.

Revenue

e.

Expenses

DIFFICULTY:

Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.02-01 – LO: 02–01

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.02 – GAAP

ACCT.ACBSP.APC.09 – Financial Statements

ACCT.ACBSP.APC.13 – Long–term Assets Reporting

ACCT.ACBSP.APC.15 – Current Assets Reporting

ACCT.ACBSP.APC.16 – Current Liabilities Reporting

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

222. Unearned Rent

223. Prepaid Insurance

224. Fees Earned

Sales

DIFFICULTY:

Bloom’s: Applying

LEARNING OBJECTIVES:

225. Patents

226. Dividends

For each of the following accounts, indicate whether its normal balance is on the credit side or the debit side of the T

account.

a.

Credit side

b.

Debit side

DIFFICULTY:

Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.02-02 – LO: 02–02

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.02 – GAAP

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

227. Common Stock

228. Accounts Receivable

229. Accounts Payable

230. Interest Revenue

231. Copyrights

Several types of errors can be made during the journalizing and posting process. Match the following with their best

description.

a.

Trial balance preparation errors

b.

Account balance errors

c.

Posting errors

DIFFICULTY:

Challenging

Bloom’s: Remembering

LEARNING OBJECTIVES:

FNMN.WARD.17.02-04 – LO: 02–04

ACCREDITING STANDARDS:

ACCT.ACBSP.APC.02 – GAAP

ACCT.ACBSP.APC.06 – Recording Transactions

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

Chapter 2 – Analyzing Transactions

232. Balance incorrectly computed.

233. Debit or credit posting omitted.

234. Wrong amount posted to an account.

235. Trial balance column incorrectly added.

236. Balance entered on wrong side of account.

237. Amount incorrectly entered on trial balance.

238. Balance entered in wrong trial balance column or omitted.

239. Debit posted as credit, or vice versa.