Test Bank Chapter 2

Chapter 2—Fundamental Economic Concepts

MULTIPLE CHOICE

1. A change in the level of an economic activity is desirable and should be undertaken as long as the

marginal benefits exceed the ____.

a.

marginal returns

b.

total costs

c.

marginal costs

d.

average costs

e.

average benefits

2. The level of an economic activity should be increased to the point where the ____ is zero.

a.

marginal cost

b.

average cost

c.

net marginal cost

d.

net marginal benefit

e.

none of the above

3. The net present value of an investment represents

a.

an index of the desirability of the investment

b.

the expected contribution of that investment to the goal of shareholder wealth

maximization

c.

the rate of return expected from the investment

d.

a and b only

e.

a and c only

4. Generally, investors expect that projects with high expected net present values also will be projects

with

a.

low risk

b.

high risk

c.

certain cash flows

d.

short lives

e.

none of the above

5. An closest example of a risk-free security is

a.

General Motors bonds

b.

AT&T commercial paper

c.

U.S. Government Treasury bills

d.

San Francisco municipal bonds

e.

an I.O.U. that your cousin promises to pay you $100 in 3 months

6. The standard deviation is appropriate to compare the risk between two investments only if

a.

the expected returns from the investments are approximately equal

b.

the investments have similar life spans

c.

objective estimates of each possible outcome is available

d.

the coefficient of variation is equal to 1.0

e.

none of the above

7. The approximate probability of a value occurring that is greater than one standard deviation from the

mean is approximately (assuming a normal distribution)

a.

68.26%

b.

2.28%

c.

34%

d.

15.87%

e.

none of the above

8. Based on risk-return tradeoffs observable in the financial marketplace, which of the following

securities would you expect to offer higher expected returns than corporate bonds?

a.

U.S. Government bonds

b.

municipal bonds

c.

common stock

d.

commercial paper

e.

none of the above

9. The primary difference(s) between the standard deviation and the coefficient of variation as measures

of risk are:

a.

the coefficient of variation is easier to compute

b.

the standard deviation is a measure of relative risk whereas the coefficient of variation is a

measure of absolute risk

c.

the coefficient of variation is a measure of relative risk whereas the standard deviation is a

measure of absolute risk

d.

the standard deviation is rarely used in practice whereas the coefficient of variation is

widely used

e.

c and d

10. The ____ is the ratio of ____ to the ____.

a.

standard deviation; covariance; expected value

b.

coefficient of variation; expected value; standard deviation

c.

correlation coefficient; standard deviation; expected value

d.

coefficient of variation; standard deviation; expected value

e.

none of the above

11. Sources of positive net present value projects include

a.

buyer preferences for established brand names

b.

economies of large-scale production and distribution

c.

patent control of superior product designs or production techniques

d.

a and b only

e.

a, b, and c

12. Receiving $100 at the end of the next three years is worth more to me than receiving $260 right now,

when my required interest rate is 10%.

a. True

b. False

13. The number of standard deviations z that a particular value of r is from the mean ȓ can be computed as

z = (r –

ȓ

)/

Suppose that you work as a commission-only insurance agent earning $1,000 per week

on average. Suppose that your standard deviation of weekly earnings is $500. What is the probability

that you zero in a week? Use the following brief z-table to help with this problem.

Z value Probability

-3 .0013

-2 .0228

-1 .1587

0 .5000

a. 1.3% chance of earning nothing in a week

b. 2.28% chance of earning nothing in a week

c. 15.87% chance of earning nothing in a week

d. 50% chance of earning nothing in a week

e. none of the above

14. Consider an investment with the following payoffs and probabilities:

State of the Economy Probability Return

Stability .50 1,000

Good Growth .50 2,000

Determine the expected return for this investment.

a. 1,300

b. 1,500

c. 1,700

d. 2,000

e. 3,000

15. Consider an investment with the following payoffs and probabilities:

State of the Economy Probability Return

GDP grows slowly .70 1,000

GDP grow fast .30 2,000

Let the expected value in this example be 1,300. How do we find the standard deviation of the

investment?

a. = { (1000-1300)2 + (2000-1300)2 }

b. = { (1000-1300) + (2000-1300) }

c. = { (.5)(1000-1300)2 + (.5)(2000-1300)2 }

d. = { (.7)(1000-1300) + (.3)(2000-1300) }

e. = { (.7)(1000-1300)2 + (.3)(2000-1300)2 }

16. An investment advisor plans a portfolio your 85 year old risk-averse grandmother. Her portfolio

currently consists of 60% bonds and 40% blue chip stocks. This portfolio is estimated to have an ex-

pected return of 6% and with a standard deviation 12%. What is the probability that she makes less

than 0% in a year? [A portion of Appendix B1 is given below, where z = (x – ) with as the mean

and as the standard deviation.]

a. 2.28%

b. 6.68%

c. 15.87%

d. 30.85%

e. 50% Table B1 for Z

Z Prob.

-3 .0013

-2.5 .0062

-2. .0228

-1.5 .0668

-1 .1587

-.5 ..3085

0 .5000

17. Two investments have the following expected returns (net present values) and standard deviations:

PROJECT Expected Value Standard Deviation

Q $100,000 $20,000

X $50,000 $16,000

Based on the Coefficient of Variation, where the C.V. is the standard deviation dividend by the

expected value.

a. All coefficients of variation are always the same.

b. Project Q is riskier than Project X

c. Project X is riskier than Project Q

d. Both projects have the same relative risk profile

e. There is not enough information to find the coefficient of variation.

Test Bank Chapter 2

PROBLEMS

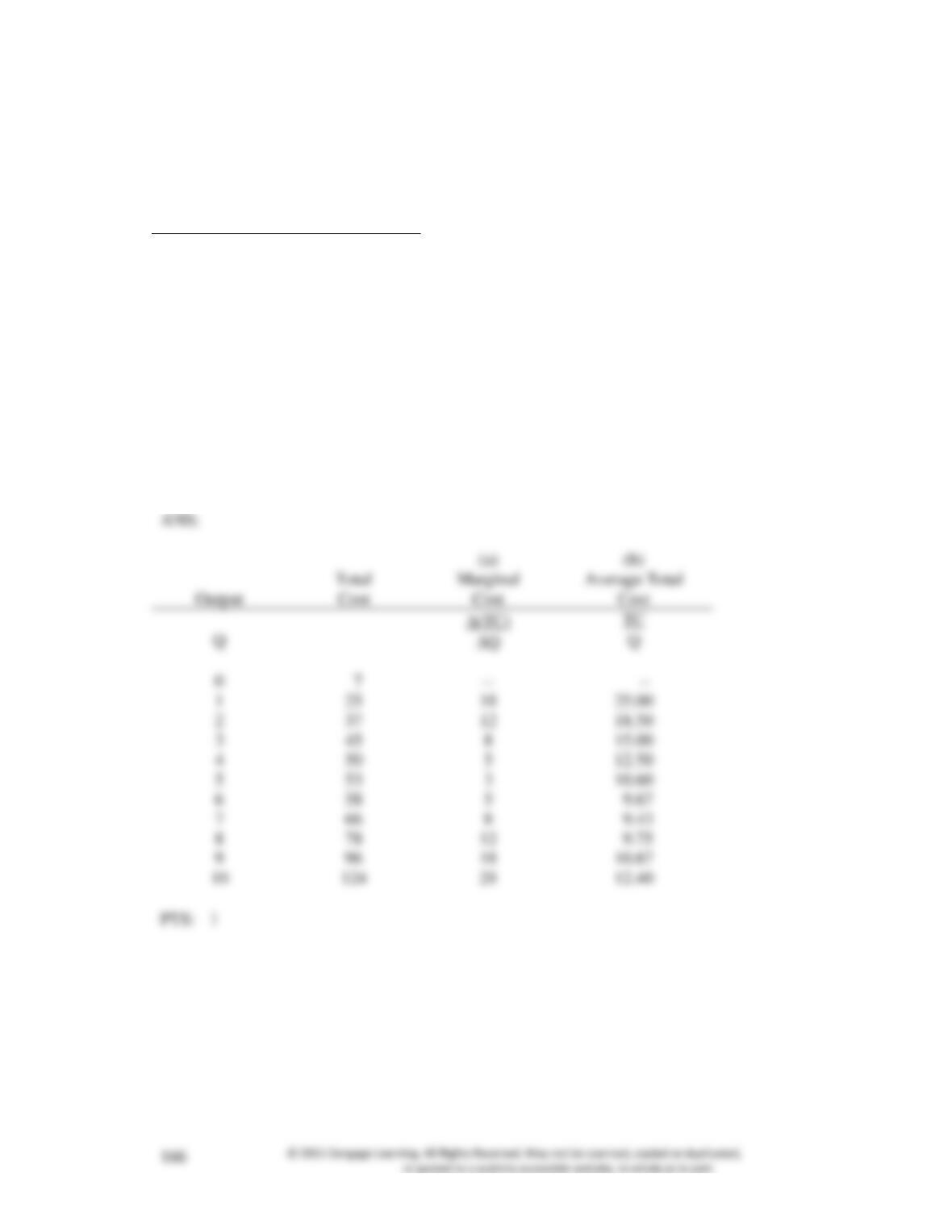

1. Suppose that the firm’s cost function is given in the following schedule (where Q is the level of

output):

Output

Total

Q (units)

Cost

0

7

1

25

2

37

3

45

4

50

5

53

6

58

7

66

8

78

9

96

10

124

(a)

Marginal

Output

Cost

0

7

1

25

18

25.00

2

37

12

18.50

3

45

8

15.00

4

50

5

12.50

5

53

3

10.60

6

58

5

9.67

7

66

8

9.43

8

78

12

9.75

9

96

18

10.67

10

28

12.40

Determine the (a) marginal cost and (b) average total cost schedules

2.Complete the following table.

Total

Marginal

Average

Output

Profit

Profit

Profit

0

−48

0

______

1

−26

______

______

2

−8

______

______

3

6

______

______

4

16

______

______

5

22

______

______

6

24

______

______

7

22

______

______

8

16

______

______

9

6

______

______

10

−8

______

______

Total

Marginal

Average

Output

0

−48

0

—

1

−26

2

−8

18

3

6

14

2.

4

16

10

4.

5

22

6

6

24

2

4.

7

22

−2

8

16

−6

9

6

−10

−14

3. A firm has decided to invest in a piece of land. Management has estimated that the land can be sold in

5 years for the following possible prices:

Price

Probability

10,000

.20

15,000

.30

20,000

.40

25,000

.10

Test Bank Chapter 2

(a)

Determine the expected selling price for the land.

(b)

Determine the standard deviation of the possible sales prices.

(c)

Determine the coefficient of variation.