Chapter 2: Financial Statements and the Annual Report

88. Which one of the following is a financing activity of a business?

a. Paying for purchases of inventory

b. Issuing stock for cash

c. Paying salaries

d. Purchasing a manufacturing plant

89. Which one of the following is an operating activity of a business?

a. Paying for purchases of inventory

b. Issuing stock for cash

c. Borrowing money from a bank

d. Purchasing a manufacturing plant

90. Which of the following represents the correct sequence of the three business activities on the Statement of

Cash Flows?

a. Financing – Operating – Investing

b. Investing – Operating – Financing

c. Operating – Investing – Financing

d. Financing – Investing – Operating

91. Business entities generally carry on:

a. Operating, investing, and financing activities

b. Operating activities, but only corporations engage in financing and investing activities

c. Investing and operating activities, but only corporations engage in financing activities

d. Either investing or financing activities, but not both

92. Although businesses engage in a wide variety of activities, all of these activities can be categorized into three

types. Which of the following choices best reflects these three types of business activities?

a. Operating, financing, reporting

b. Investing, reporting, financing

c. Operating, financing, investing

d. Investing, reporting, operating

Chapter 2: Financial Statements and the Annual Report

93. As used in accounting, the “Notes to the Financial Statements” should be:

a. Listed with the liabilities on the balance sheet

b. Omitted at the option of the company

c. Included as an integral part of the financial statements

d. Reported as expenses on the Income Statement

94. Which of the following items will be found in a corporate annual report?

a. Company budgets

b. Notes to the financial statements

c. Selected financial data from competitor companies

d. Management’s statement that the auditors are responsible for the financial statements

95. Which one of the following sections is least likely to be found in a corporate annual report?

a. Notes to the Financial Statements

b. Forecasts of Cash Flows and Earnings

c. Report of the Independent Accountants

d. Management’s Discussion and Analysis

96. Supplementary disclosures required by GAAP that help explain detail behind the accounting treatment of

certain items in the financial statements is most likely found in which of the following sections of a corporate

annual report?

a. Report of the Independent Accountants

b. Notes to the Financial Statements

c. Management’s Discussion and Analysis

d. Balance Sheet

97. An investor found the following in an annual report: “The financial statements, in our opinion, present fairly

the financial position, operating results, and cash flows, in conformity with accounting principles generally

accepted in the United States.” In which section of the annual report did the investor find this?

a. Balance Sheet

b. Notes to the Financial Statements

c. Management’s Discussion and Analysis

d. Report of the Independent Accountants

Chapter 2: Financial Statements and the Annual Report

98. Which of the following represents one of the purposes of the notes to financial statements?

a. To provide a place for management to justify questionable items in the statements

b. To provide comparative ratios for the company’s financial data

c. To provide the CPA‘s opinion of the fairness of the financial statements

d. To satisfy the need for full disclosure of all the facts relevant to a company’s results and financial position

99. Financial statements are intended to tell the reader the value of a company.

a. True

b. False

100. Accountants are the main reason financial statements are prepared.

a. True

b. False

101. The Financial Accounting Standards Board created the objectives of financial reporting.

a. True

b. False

102. The purpose of financial reporting is to provide economic information to external decision makers only.

a. True

b. False

103. An objective of financial reporting is to reflect economic information concerning a company’s cash flows.

a. True

b. False

104. The concept of conservatism is the capacity of information to make a difference in a decision.

a. True

b. False

105. Materiality deals with the size of an error in accounting information.

a. True

b. False

Chapter 2: Financial Statements and the Annual Report

106. Most businesses have an operating cycle of less than one year.

a. True

b. False

107. Current assets, other than cash, are expected to be sold or consumed are during a company’s normal operating

cycle.

a. True

b. False

108. Obligations related to operating activities that will be paid within the company‘s operating cycle must be

reported as current liabilities on a classified balance sheet.

a. True

b. False

109. The operating cycle for all businesses is one year.

a. True

b. False

110. A construction company that builds skyscrapers is likely to have an operating cycle longer than one year.

a. True

b. False

111. Three common categories of long-term assets are: 1) property, plant, and equipment, 2) investments,

and 3) intangibles.

a. True

b. False

112. In the stockholders’ equity section of a classified balance sheet, a distinction is made between amounts

invested by owners and amounts accumulated from business earnings.

a. True

b. False

Chapter 2: Financial Statements and the Annual Report

113. One primary purpose of a classified balance sheet is to help users evaluate the liquidity of a company.

a. True

b. False

114. Companies prepare classified financial statements because they are required by international accounting

principles.

a. True

b. False

115. The current ratio is irrelevant in liquidity analysis for service companies because they do not have

inventories among their current assets

a. True

b. False

116. An advantage of the current ratio is that it considers the makeup of the current assets.

a. True

b. False

117. The excess of current assets over current liabilities is referred to as working capital.

a. True

b. False

118. A balance sheet shows cash, $75,000; marketable securities, $115,000; accounts receivable, $150,000 and

$222,500 of inventories. Current liabilities are $225,000. The current ratio is 2.5 to 1.

a. True

b. False

119. If a firm has a current ratio of 2, the subsequent receipt of a 60-day note receivable to settle an open account

will cause the ratio to decrease.

a. True

b. False

120. The purchase of inventory for cash will cause the current ratio to decrease.

a. True

b. False

Chapter 2: Financial Statements and the Annual Report

121. Income from operations does not include interest revenue and interest expense because these items are

considered to be non–operating in nature.

a. True

b. False

122. A 12% change in sales will result in a 12% change in net income.

a. True

b. False

123. Some analysts properly refer to a company’s profit margin as its return on assets.

a. True

b. False

124. Dividends declared and paid reduce a company’s retained earnings balance.

a. True

b. False

125. Dividends paid appears on both the income statement and the statement of retained earnings.

a. True

b. False

126. Investing activities are needed to provide the funds to start a business.

a. True

b. False

127. The statement of cash flows, like the income statement, reports only operating activities of a company.

a. True

b. False

128. Funds raised from financing activities should be invested in assets that can be used to carry on business

operations.

a. True

b. False

Chapter 2: Financial Statements and the Annual Report

129. The primary responsibility for the preparation and integrity of the financial statements in an annual report

belongs to the company’s independent accountants (CPAs).

a. True

b. False

130. Independent auditors (CPAs) render an opinion that the financial statements do or do not fairly

present a company‘s financial position, operating results, and cash flows.

a. True

b. False

131. An independent auditor’s (CPA’s) report is a guarantee that the financial statements are free from fraud or

material error

a. True

b. False

132. In the independent auditors’ report included with the annual report, management discusses the financial

statements and provides the shareholders with explanations for certain amounts reported in the statements.

a. True

b. False

133. ____________________ and ____________________ have claims to an entity’s economic resources.

134. is the magnitude of an omission or misstatement in accounting information that

will affect the judgment of someone relying on the information.

135. is the capacity of information to make a difference in a decision.

136. ____________________ is the practice of using the least optimistic estimate when two estimates of

amounts are about equally likely.

137. is the quality of accounting information that makes it comprehensible to those

willing to spend the necessary time.

Chapter 2: Financial Statements and the Annual Report

138. is the quality of accounting information that makes it dependable in representing

the events that it purports to represent.

139. is the quality of accounting information that allows a user to analyze two or

more companies and look for similarities and differences.

140. is the quality of accounting information that allows a user to compare two or

more accounting periods for a single company.

141. have claims to an entity’s economic resources.

142. are cash and other assets that are reasonably expected to be realized in

cash during the normal operating cycle of the business.

143. Property, plant and equipment is classified as assets on the balance sheet.

144. ____________________ is the process of writing off the cost of tangible assets and

____________________ is the process of writing off the cost of intangible assets.

145. is a liquidity measure that is calculated by subtracting current assets

from current liabilities.

146. The ability of a company to pay its debt as it comes due relates to .

147. In a -step income statement, all expenses and losses are added together, then

deducted from the sum of all revenues and gains.

148. The statement of explains changes in the components of owners’ equity during the

period.

Chapter 2: Financial Statements and the Annual Report

149. On the statement of cash flows, the section involves the

acquisition and sale of long-term assets.

150. On the statement of cash flows, the section involves the purchase

and sale of products and services.

151. On the statement of cash flows, the section involves the issuance

and repayment of long term liabilities and stock transactions.

Cargo Corporation

Listed below is information from the financial records of Cargo Corporation at December 31, 2015:

Retained earnings

$37,000

Notes payable—Due July 1, 2018

$12,000

Accumulated depreciation

13,000

Interest payable

1,000

Income taxes payable

24,000

Office supplies

2,000

Buildings

48,000

Accounts payable

36,000

Cash

11,000

Inventory

33,000

Accounts receivable

35,000

Land

50,000

Capital stock

60,000

Prepaid rent

4,000

152. Read the information about Cargo Corporation.

Required:

Prepare the current liabilities section of the balance sheet for Cargo Corp. at December 31, 2015. You may

omit the heading. If the amount of current liabilities were larger, what effect would this have on the current

ratio?

Chapter 2: Financial Statements and the Annual Report

153. Read the information about Cargo Corporation.

Required:

Prepare the long-term asset section of Cargo Corp.’s balance sheet at December 31, 2015. You may omit the

heading. Why are these amounts classified as “long-term”?

154. Read the information about Cargo Corporation.

Required:

Prepare the current assets section of the balance sheet for Cargo Corp. at December 31, 2015. You may omit

the heading. How does the concept of liquidity apply?

155. Read the information about Cargo Corporation.

Required:

Calculate Cargo’s current ratio at December 31, 2015. What does this ratio tell you about the “composition” of

the current assets?

Chapter 2: Financial Statements and the Annual Report

156. Read the information below about Cargo Corporation.

Required:

Calculate the amount of working capital at December 31, 2015 for Cargo Corp. What can you learn from the

current ratio that you cannot learn from the amount of working capital?

157. Harrison Company calculated the following amounts concerning its financial information for the years

ending December 31, 2015 and 2014:

2015

2014

Current ratio

3.1 to 1

2.0 to 1

Profit margin

22 %

18%

Required:

Examine Harrison’s ratios. Is the change in the current ratio favorable or not? Explain.

Chapter 2: Financial Statements and the Annual Report

158. Read the information about Fasoli, Inc.

Required:

Prepare the Liabilities section of the classified balance sheet, including total liabilities balance.

Chapter 2: Financial Statements and the Annual Report

Fasoli, Inc.

The following balance sheet items from Fasoli, Inc. are listed for December 31, 2015:

Accounts payable

$ 32,650

Interest payable

2,200

Accounts receivable

26,500

Land

250,000

Accumulated depreciation—buildings

40,000

Marketable securities

15,000

Merchandise inventory

112,900

Accumulated depreciation—equipment

12,500

Notes payable, due April 15, 2016

6,500

Office supplies

200

Notes payable, due December 31, 2019

251,630

Paid-in capital in excess of par value

75,000

Buildings

150,000

Patents

45,000

Capital stock, $1 par value

200,000

Prepaid rent

3,800

Cash

60,990

Retained earnings

113,510

Equipment

84,500

Salaries payable

7,400

Income taxes payable

7,500

159. Read the information about Fasoli, Inc.

Required:

Present the Current Assets section (including the total) of a classified balance sheet.

Chapter 2: Financial Statements and the Annual Report

160. Read the information about Fasoli, Inc.

Required:

Prepare the Stockholders’ Equity section of the classified balance sheet, including the total stockholders’

equity amount.

161. Read the information about Fasoli, Inc.

Required:

Present the current liabilities section (including the total) of a classified balance sheet.

162. Read the information about Fasoli, Inc.

Required:

Compute Fasoli’s current ratio. On the basis of your answer, does Fasoli appear to be liquid? What other

information do you need to fully answer that question?

Chapter 2: Financial Statements and the Annual Report

163. Read the information about Fasoli, Inc.

Required:

Prepare the Assets section of the classified balance sheet.

Chapter 2: Financial Statements and the Annual Report

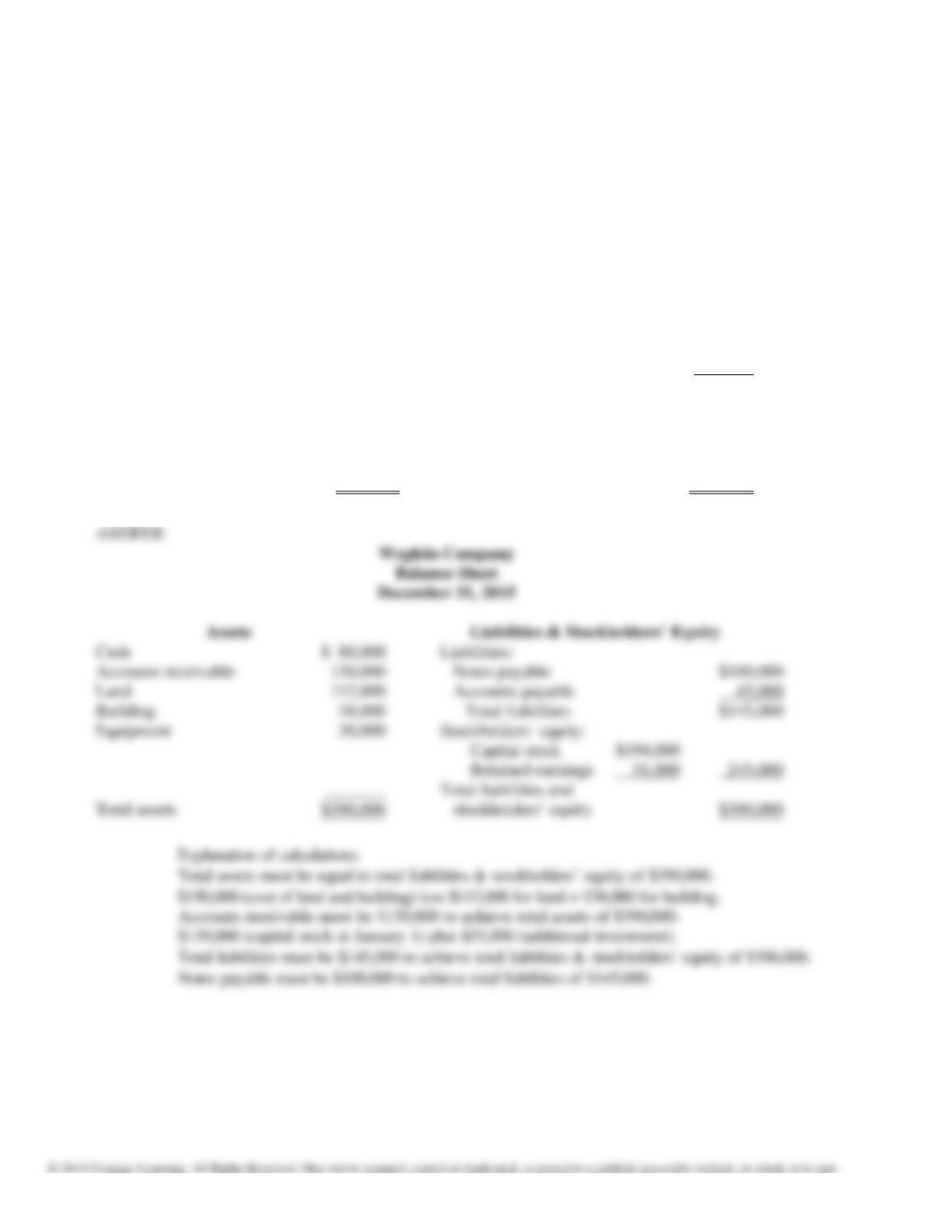

164. Complete the December 31, 2015 (first year of operation) Balance sheet for Weglein Company using the

following information:

(a) Retained earnings at December 31, 2015 was $51,000.

(b) Total stockholders’ equity at January 1, 2015 was $139,000.

(c) On December 30, 2015, additional capital stock was sold for cash, $55,000

(d) The land and building were purchased on December 30, 2015 for $150,000.

Weglein Company

Balance Sheet

December 31, 2015

Assets

Liabilities & Stockholders’ Equity

Cash

$ 80,000

Liabilities:

Accounts receivable

Notes payable

$

Land

112,000

Accounts payable

45,000

Buildings

Total liabilities

$

Equipment

30,000

Stockholders’ equity:

Capital Stock

$

Retained earnings

_______

_______

Total liabilities and

Total assets

$

stockholders’ equity

$390,000

Cash

Liabilities:

Accounts receivable

Notes payable

Land

Accounts payable

45,000

Building

Total liabilities

Equipment

Capital stock

$194,000

Retained earnings

51,000

245,000

Total liabilities and

Total assets

stockholders’ equity

Chapter 2: Financial Statements and the Annual Report

165. Harrison Company calculated the following amounts concerning its financial information for the years

ending December 31, 2015 and 2014:

2015

2014

Current ratio

3.1 to 1

2.0 to 1

Profit margin

22 %

18%

Required:

Suppose Harrison Company had a decrease in its cash account from 2014 to 2015. Would the other current

asset amounts have increased or decreased? Explain.

Fellsmere Corporation

Presented below are the condensed balance sheets of Fellsmere Corporation at December 31, 2014 and 2013.

Net income for the years ending December 31, 2014 and 2013 is $346, 000 and $109,000, respectively.

December 31, 2014

December 31, 2013

Current assets

$2,228,186

$2,544,683

Property, plant, & equipment (net)

530,589

376,647

Intangibles and other assets

131,206

118,121

Total assets

$2,889,981

$3,039,451

Current liabilities

$1,429,674

$1,003,906

Long-term obligations

3,360

7,240

Warranty and other liabilities

112,971

98,081

Total liabilities

$1,546,605

$1,109,227

Stockholders’ equity:

Common stock

$ 1,566

$ 501,631

Additional paid-in capital

365,986

799,483

Retained earnings

980,509

634,509

Accumulated other comprehensive loss

(4,085)

(5,489)

Total stockholders’ equity

$1,343,976

$1,930,224

Total liabilities and stockholders’ equity

$2,889,981

$3,039,451

Chapter 2: Financial Statements and the Annual Report

166. Read the information about Fellsmere Corporation.

Required:

(A) Did Fellsmere’s current ratio increase or decrease from 2013 to 2014? Make any necessary calculations

and explain your answer. Which financial statement users are most concerned with this ratio?

(B) The balance sheets show a large increase in retained earnings during 2014. Identify the possible

reason(s) for this increase.

167. Read the information about Fellsmere Corporation.

Required:

(A) Explain the change in Fellsmere’s working capital from 2013 to 2014. Why do users believe the current

ratio provides more information than the dollar amount of working capital? Explain.

(B) Fellsmere Corporation‘s creditors need to know whether its working capital position improved during the

year. How would you evaluate this?

Chapter 2: Financial Statements and the Annual Report

Crystal, Inc.

Crystal, Inc. reported $52,000 of net income for 2014. Crystal’s balance sheet at December 31, 2014 includes

the following amounts:

Wages payable

$ 1,000

Inventory

$26,000

Prepaid rent

3,000

Land

40,000

Cash

15,000

Accounts receivable

22,000

Accounts payable

25,000

Capital stock

40,000

Retained earnings

29,000

Income taxes payable

11,000

168. Read the information about Crystal, Inc. Which item is most “liquid“? Why is liquidity important?

169. Read the information about Crystal, Inc. Has Crystal been profitable since it began operations? How do you

know?

Chapter 2: Financial Statements and the Annual Report

170. The balance sheet of Evanston Inc. includes the following items:

Cash

$ 21,500

Accounts receivable

12,400

Inventory

45,300

Prepaid insurance

1,800

Land

80,000

Accounts payable

49,000

Salaries payable

1,625

Capital stock

105,100

Retained earnings

5,700

Required:

(1) Determine the current ratio and working capital.

(2) What does the composition of the current assets tell you about Evanston’s liquidity?

(3) What other information do you need to fully assess Evanston’s liquidity?