2-1: Fixed, Variable, and Average Costs

Midstate University is trying to decide whether to allow 100 more students into the

university. Tuition is $5000 per year. The controller has determined the following schedule of

costs to educate students:

Number of Students Total Costs

4000 $30,000,000

4100 30,300,000

4200 30,600,000

4300 30,900,000

The current enrollment is 4200 students. The president of the university has calculated the cost

per student in the following manner: $30,600,000/4200 students = $7286 per student. The

president was wondering why the university should accept more students if the tuition is only

$5000.

Required:

a. What is wrong with the president’s calculation?

b. What are the fixed and variable costs of operating the university?

2-1: Solution to Fixed, Variable, and Average Costs (15 minutes)

2-2: The Elements of Cost Volume Profit

The M Company’s variable costs are 75% of the sales price per unit and their fixed costs

are $240,000. If the company earned $60,000 in selling 150,000 units, what was the sales price

per unit?

2-2: Solution Cost Volume Profit (5 minutes)

2-3: Opportunity Costs

The First Church has been asked to operate a homeless shelter in part of the church. To

operate a homeless shelter the church would have to hire a full time employee for $1,200/month

to manage the shelter. In addition, the church would have to purchase $400 of supplies/month for

the people using the shelter. The space that would be used by the shelter is rented for wedding

parties. The church averages about 5 wedding parties a month that pay rent of $200 per party.

Utilities are normally $1,000 per month. With the homeless shelter, the utilities will increase to

$1,300 per month.

What is the opportunity cost to the church of operating a homeless shelter in the church?

2-3: Solution to Opportunity Costs (10 minutes)

2-4: Fixed and Variable Costs

The university athletic department has been asked to host a professional basketball game

at the campus sports center. The athletic director must estimate the opportunity cost of holding

the event at the sports center. The only other event scheduled for the sports center that evening is

a fencing match that would not have generated any additional costs or revenues. The fencing

match can be held at the local high school, but the rental cost of the high school gym would be

$200. The athletic director estimates that the professional basketball game will require 20 hours

of labor to prepare the building. Clean-up depends on the number of spectators. The athletic

director estimates the time of clean-up to be equal to 2 minutes per spectator. The labor would be

hired especially for the basketball game and would cost $8 per hour. Utilities will be $500 greater

if the basketball game is held at the sports center. All other costs would be covered by the

professional basketball team.

Required:

a. What is the variable cost of having one more spectator?

b. What is the opportunity cost of allowing the professional basketball team to use the sports

center if 10,000 spectators are expected?

c. What is the opportunity cost of allowing the professional basketball team to use the sports

center if 12,000 spectators are expected?

2-4: Solution to Fixed and Variable Costs (15 minutes)

2-5: Opportunity Cost of Attracting Industry

The Itagi Computer Company From Japan is looking to build a factory for making DVD

burners in the United States. The company is concerned about the safety and well-being of its

employees and wants to locate in a community with good schools. The company also wants the

factory to be profitable and is looking for subsidies from potential communities. Encouraging new

business to create jobs for citizens is important for communities, especially communities with high

unemployment.

Wellville has not been very well since the shoe factory left town. The city officials have

been working on a deal with Itagi to get the company to locate in Wellville. Itagi officials have

identified a 20 acre undeveloped site. The city has tentatively agreed to buy the site for $50,000

for Itagi and not require any payment of property taxes on the factory by Itagi for the first five

years of operation. The property tax deal will save Itagi $3,000,000 in taxes over the five years.

This deal was leaked to the local newspaper. The headlines the next day were: “Wellville Gives

Away $3,000,000+ to Japanese Company”.

Required:

a. Do the headlines accurately describe the deal with Itagi?

b. What are the relevant costs and benefits to the citizens of Wellville of making this deal?

2-5: Solution to Opportunity Cost of Attracting Industry (15 minutes)

2-6: Cost, Volume, Profit Analysis

With the possibility of the US Congress relaxing restrictions on cutting old growth, a local

lumber company is considering an expansion of its facilities. The company believes it can sell

lumber for $0.18/board foot. A board foot is a measure of lumber. The tax rate for the company

is 30 percent. The company has the following two opportunities:

• Build Factory A with annual fixed costs of $20 million and variable costs of $0.10/board

foot. This factory has an annual capacity of 500 million board feet.

• Build Factory B with annual fixed costs of $10 million and variable costs of $0.12/board

foot. This factory has an annual capacity of 300 million board feet.

Required:

a. What is the break-even point in board feet for Factory A?

b. If the company wants to generate an after tax profit of $2 million with Factory B, how

many board feet would the company have to process and sell?

c. If demand for lumber is uncertain, which factory is riskier?

d. At what level of board feet would the after-tax profit of the two factories be the same?

2-6: Solution to Cost, Volume, Profit Analysis (20 minutes)

2-7: Cost, Volume, Profit Analysis

Leslie Mittelberg is considering the wholesaling of a leather handbag from Kenya. She

must travel to Kenya to check on quality and transportation. The trip will cost $3000. The cost of

the handbag is $10 and shipping to the United States can occur through the postal system for $2

per handbag or through a freight company which will ship a container that can hold up to a 1000

handbags at a cost of $1000. The freight company will charge $1000 even if less than 1000

handbags are shipped. Leslie will try to sell the handbags to retailers for $20. Assume there are

no other costs and benefits.

Required:

a. What is the break-even point if shipping is through the postal system?

b. How many units must be sold if Leslie uses the freight company and she wants to have a

profit of $1000?

c. At what output level would the two shipping methods yield the same profit?

d. Suppose a large discount store asks to buy an additional 1000 handbags beyond normal

sales. Which shipping method should be used and what is the minimum sales price Leslie

should consider in selling those 1000 handbags?

2-7: Solution to Cost, Volume, Profit Analysis (20 minutes)

2-8: Multiple Product Cost Volume Profit

A company sells three products as shown below:

Product X

Product Y

Product Z

Total

Units

60,000

140,000

50,000

250,000

Sales

$90,000

$150,000

$60,000

$300,000

Variable Costs

$63,000

$93,000

$19,000

$175,000

Contribution

Margin

$125,000

Fixed Costs

$100,000

Required:

a. How many units of each product need to be sold to breakeven?

b. How many units must of each product must be sold if the company wants to have a profit

of $50,000?

2-8: Solution to Multiple Product Cost Volume Profit (10 minutes)

2-9: Make Buy

A company has needs 10,000 units of a component used in producing one of its products.

The latest internal accounting reports show that the per unit manufacturing cost to be $150.00. The

manufacturing cost per component broken down into type of costs is as follows: Variable

manufacturing costs = $110.00 and fixed manufacturing overhead = $40. The company recently

received an offer from another manufacturer to produce the component for $144.00. If they buy the

component on the outside 40% of the fixed overhead can be avoided.

Required:

a. If the company decides to have the component made by the outside supplier at $144.00,

what is the impact on income?

b. What price would make the company indifferent between making the component internally

and having the outside supplier make it?

2-9: Solution to Make-Buy (10 minutes)

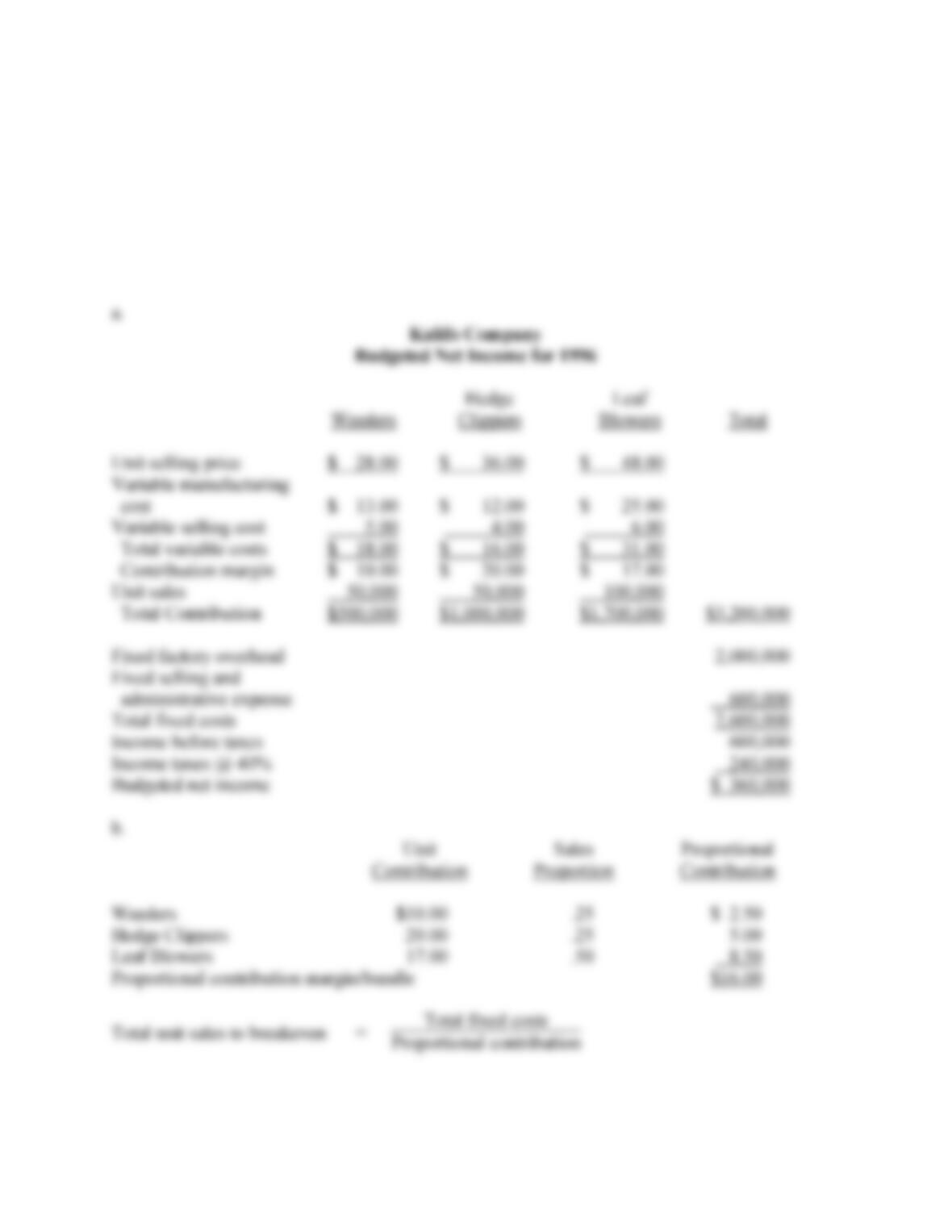

2-10: Cost, Volume, Profit Analysis

Kalifo Company manufactures a line of electric garden tools that are sold in general

hardware stores. The company’s controller, Sylvia Harlow, has just received the sales forecast for

the coming year for Kalifo’s three products: weeders, hedge clippers, and leaf blowers. Kalifo has

experienced considerable variations in sales volumes and variable costs over the past two years,

and Harlow believes the forecast should be carefully evaluated from a cost-volume-profit

viewpoint. The preliminary budget information for 1996 is presented below.

Weeders

Hedge Clippers

Leaf

Blowers

Unit sales

50,000

50,000

100,000

Unit selling price

$28.00

$36.00

$48.00

Variable manufacturing cost per unit

13.00

12.00

25.00

Variable selling cost per unit

5.00

4.00

6.00

For 1996, Kalifo’s fixed factory overhead is budgeted at $2 million, and the company’s

fixed selling and administrative expenses are forecast to be $600,000. Kalifo has a tax rate of 40

percent.

Required:

a. Determine Kalifo Co.’s budgeted net income for 1996.

b. Assuming that the sales mix remains as budgeted, determine how many units of each

product Kalifo must sell in order to break even in 1996.

c. Determine the total dollar sales Kalifo must sell in 1996 in order to earn an after-tax net

income of $450,000.

d. After preparing the original estimates, Kalifo determines that its variable manufacturing

cost of leaf blowers will increase 20 percent and the variable selling cost of hedge clippers

can be expected to increase $1 per unit. However, Kalifo has decided not to change the

selling price of either product. In addition, Kalifo learns that its leaf blower is perceived

as the best value on the market, and it can expect to sell three times as many leaf blowers

as any other product. Under these circumstances, determine how many units of each

product Kalifo will have to sell to break even in 1996.

e. Explain the limitations of cost-volume-profit analysis that Sylvia Harlow should consider

when evaluating Kalifo’s 1996 budget.

Source: CMA adapted.

2-10: Solution to Cost, Volume, Profit Analysis (CMA adapted) (45 minutes)

2-11: Breakeven and Cost-Volume-Profit with Taxes

DisKing Company is a retailer for video disks. The projected after-tax net income for the

current year is $120,000 based on a sales volume of 200,000 video disks. DisKing has been selling

the disks at $16 each. The variable costs consist of the $10 unit purchase price of the disks and a

handling cost of $2 per disk. DisKing’s annual fixed costs are $600,000 and DisKing is subject to

a 40 percent income tax rate.

Management is planning for the coming year, when it expects that the unit purchase price

of the video disks will increase 30 percent.

Required:

a. Calculate DisKing Company’s break-even point for the current year in number of video

disks.

b. Calculate the increased after-tax income for the current year from an increase of 10 percent

in projected unit sales volume.

c. If the unit selling price remains at $16, calculate the volume of sales in dollars that DisKing

Company must achieve in the coming year to maintain the same after-tax net income as

projected for the current year.

Source: CMA adapted

2-11: Solution to Breakeven and Cost Volume Profit with Taxes (CMA adapted) (15 minutes)

2-12: Cost-volume-profit of a Make/buy Decision

Elly Industries is a multiproduct company that currently manufactures 30,000 units of Part

MR24 each month for use in production. The facilities now being used to produce Part MR24

have affixed monthly cost of $150,000 and a capacity to produce 84,000 units per month. If Elly

were to buy Part MR24 from an outside supplier, the facilities would be idle, but its fixed costs

would continue at 40 percent of its present amount. The variable production costs of Part MR24

are $11 per unit.

Required:

a. If Elly Industries continues to use 30,000 units of Part MR24 each month, it would realize

a net benefit by purchasing Part MR24 from an outside supplier only if the supplier’s unit

price is less than how much?

b. If Elly Industries can obtain Part MR24 from an outside supplier at a unit purchase price

of $12.875, what is the monthly usage at which it will be indifferent between purchasing

and making Part MR24?

Source: CMA adapted

2-12: Solution to Cost-Volume-Profit of a Make/Buy Decision (CMA adapted) (15 minutes)

2-13: Opportunity Cost of Purchase Discounts and Lost Sales

Winter Company is a medium-size manufacturer of hard drives that are sold to computer

manufacturers. At the beginning of 2012 Winter began shipping a much-improved hard drive,

Model W899. The W899 was an immediate success and accounted for $5 million in revenues for

Winter in 2012.

While the W899 was in the development stage, Winter planned to price it at $130. In

preliminary discussions with customers about the W899 design, no resistance was detected to

suggestions that the price might be $130. The $130 price was considerably higher than the

estimated variable cost of $70 per unit to produce the W899, and it would provide Winter with

ample profits.

Shortly before setting the price of the W899, Winter discovered that a competitor was

reading a product very similar to the W899 and was no more than 60 days behind Winter’s own

schedule. No information could be obtained on the competitor’s planned price, although it had a

reputation for aggressive pricing. Worried about the competitor, and unsure of the market size,

Winter lowered the price of the W899 to $100. It maintained the price although, to Winter’s

surprise, the competitor announced a price of $130 for its product.

After reviewing the 2012 sales of the W899, Winter’s management concluded that unit

sales would have been the same if the product had been marketed at the original price of $130

each. Management has predicted that 2013 sales of the W899 would be either 85,000 units at $100

each or 60,000 units at $130 each. Winter has decided to raise the price of the disk drive to $130

effective immediately.

Having supported the higher price from the beginning, Sharon Daley, Winter’s marketing

director, believes that the opportunity cost of selling the W899 for $100 during 2012 should be

reflected in the company’s internal records and reports. In support of her recommendation, Daley

explained that the company has booked these types of costs on other occasions when purchase

discounts not taken for early payment have been recorded.

Required:

a. Define opportunity cost and explain why opportunity costs are not usually recorded.

b. What is the 2012 opportunity cost?

c. Explain the impact of Winter Company’s selection of the $130 selling price for the W899

on 2013 operating income. Support your answer with appropriate calculations.

Source: CMA adapted

2-13: Solution to Opportunity Cost of Purchase Discounts and Lost Sales (CMA adapted)

(20 minutes)

2-14: Make/Buy and the Opportunity Cost of Freed Capacity

Leland Manufacturing uses 10 units of part KJ37 each month in the production of radar

equipment. The cost to manufacture one unit of KJ37 is presented in the accompanying table.

Direct materials

$ 1,000

Materials handling (20% of direct material cost)

200

Direct labor

8,000

Manufacturing overhead

12,000

Total manufacturing cost

$21,200

Materials handling represents the direct variable costs of the receiving department and is applied

to direct materials and purchased components on the basis of their cost. This is a separate charge

in addition to manufacturing overhead. Leland’s annual manufacturing overhead budget is one-

third variable and two-third fixed. Scott Supply, one of Leland’s reliable vendors, has offered to

supply part KJ37 at a unit price of $15,000. The fixed cost of producing KJ37 is the cost of a

special piece of testing equipment that ensures the quality of each part manufactured. This testing

equipment is under a long-term, noncancelable lease. If Leland were to purchase part KJ37,

materials handling costs would not be incurred.

Required:

a. If Leland purchases the KJ37 units from Scott, the capacity Leland was using to

manufacture these parts would be idle. Should Leland purchase the parts from Scott?

Make explicit any key assumptions.

b. Assume Leland Manufacturing is able to rent all idle capacity for $25,000 per month.

Should Leland purchase from Scott Supply? Make explicit any key assumptions.

c. Assume that Leland Manufacturing does not wish to commit to a rental agreement but

could use idle capacity to manufacture another product that would contribute $52,000 per

month. Should Leland manufacture KJ37? Make explicit any key assumptions.

Source: CMA adapted

2-14: Solution to Make/Buy and the Opportunity Cost of Freed Capacity (CMA adapted)

(20 minutes)