CHAPTER 18

COST-VOLUME-PROFIT

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

True-False Statements

1.

1

K

9.

2

C

17.

4

K

25.

6

K

sg33.

3

K

2.

1

K

10.

3

K

18.

5

K

26.

6

AP

sg34.

5

C

3.

1

K

11.

3

K

19.

5

K

27.

7

K

sg35.

6

K

4.

1

C

12.

3

C

20.

5

K

28.

7

K

sg36.

7

AP

5.

1

C

13.

3

K

21.

5

K

29.

8

K

sg37.

8

K

6.

1

C

14.

3

C

22.

5

K

30.

8

K

7.

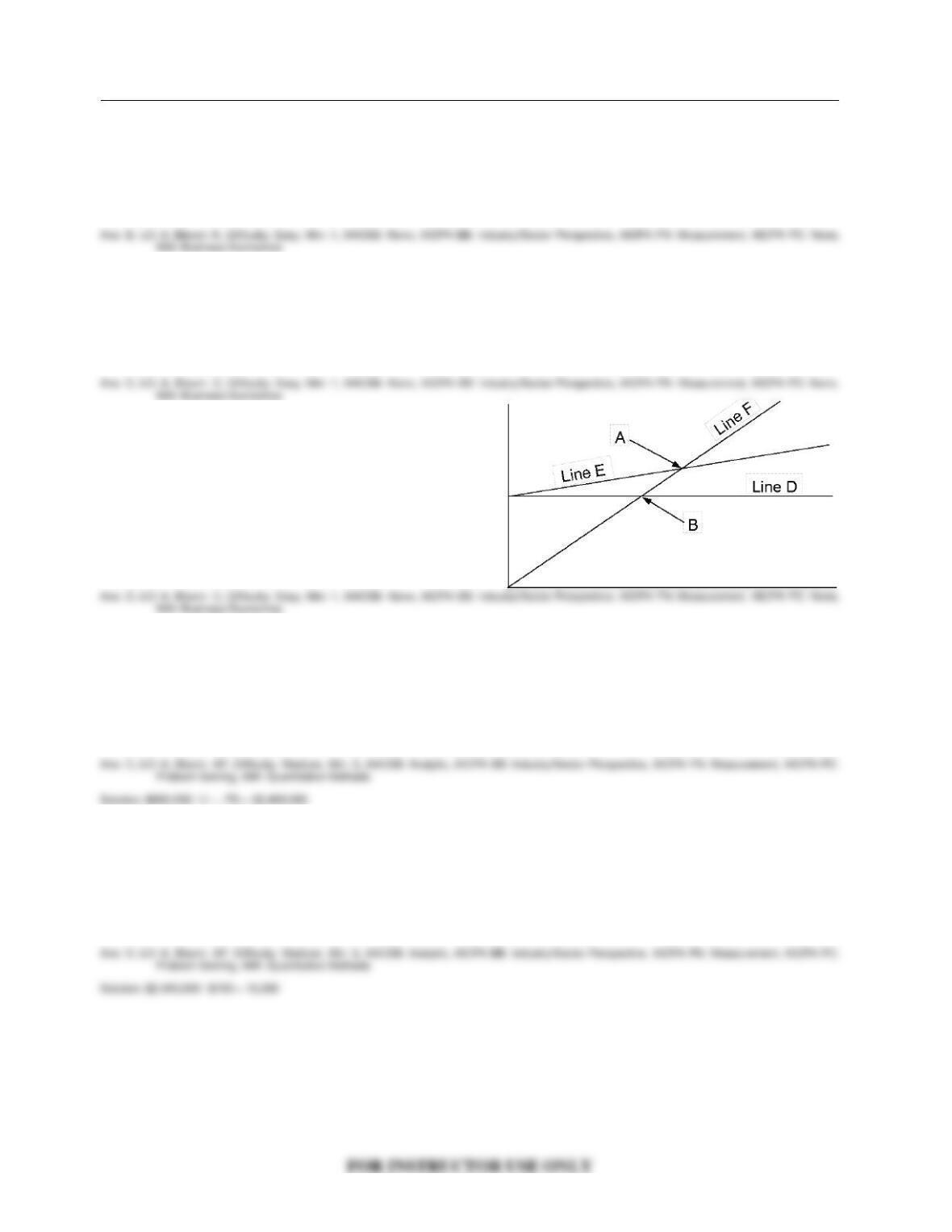

2

K

15.

3

K

23.

6

K

sg31.

1

K

8.

2

K

16.

4

K

24.

6

K

sg32.

1

K

Multiple Choice Questions

38.

1

C

62.

2

C

86.

5

AP

110.

6

C

134.

7

AP

39.

1

K

63.

2

C

87.

5

K

111.

6

K

135.

7

AP

40.

1

K

64.

3

AP

88.

5

AP

112.

6

AP

136.

7

AP

41.

1

C

65.

3

K

89.

5

C

113.

6

AP

137.

7

AP

42.

1

C

66.

3

AP

90.

5

AP

114.

6

AP

138.

7

AP

43.

1

K

67.

3

AP

91.

5

AP

115.

6

AP

139.

7

AP

44.

1

C

68.

3

C

92.

5

AP

116.

6

AP

140.

8

AP

45.

1

C

69.

3

C

93.

5

AP

117.

6

AP

141.

8

AP

46.

1

K

70.

3

K

94.

5

AP

118.

6

AP

142.

8

AP

47.

1

C

71.

3

C

95.

5

AP

119.

6

AP

143.

8

K

48.

1

C

72.

3

AP

96.

5

AP

120.

6

AP

144.

8

C

49.

1

K

73.

3

AP

97.

5

AP

121.

6

AP

sg145.

2

K

50.

1

C

74.

3

AP

98.

5

AP

122.

6

AP

st146.

3

K

51.

1

K

75.

3

K

99.

5

C

123.

6

C

sg147.

3

AP

52.

1

C

76.

3

K

100.

5

K

124.

7

AP

st148.

4

K

53.

1

C

77.

3

C

101.

5

K

125.

7

AP

sg149.

5

C

54.

1

C

78.

3

AP

102.

5

AP

126.

7

AP

st150.

5

K

55.

1

C

79.

3

AP

103.

6

AP

127.

7

AP

sg151.

5

AP

56.

2

C

80.

4

K

104.

6

AP

128.

7

AP

st152.

6

AP

57.

2

K

81.

4

K

105.

6

K

129.

7

AP

sg153.

6

K

58.

2

C

82.

4

C

106.

6

C

130.

7

AP

st154.

7

AP

59.

2

C

83.

4

K

107.

6

C

131.

7

AP

sg155.

7

K

60.

2

C

84.

4

C

108.

6

AP

132.

7

AP

sg156.

8

AP

61.

2

K

85.

4

C

109.

6

AP

133.

7

AP

Brief Exercises

157.

3

AP

159.

5

AP

161.

6

AP

163.

6

AP

165.

8

AP

158.

5

AP

160.

5

AP

162.

6

AP

164.

8

AP

166.

8

AP

sg This question also appears in the Study Guide.

st This question also appears in a self-test at the student companion website.

a This question covers a topic in an appendix to the chapter.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 2

SUMMARY OF QUESTIONS BY LEARNING OBJECTIVES AND BLOOM’S TAXONOMY

Exercises

16

7.

1,3

AP

173.

4

AN

179.

5,6,7

AN

185.

5,7

AP

191.

6,7

AP

16

8.

1,3,6,8,

AP

174.

4

E

180.

5,6

AP

186.

6

AP

192.

7

AP

16

9.

1,3,5,6,

AN

175.

4,6,7

AN

181.

5,6,8

AP

187.

6,7,8

AP

193.

8

AP

17

0.

3

AP

176.

5

AP

182.

5,6

AP

188.

6,7

AP

17

1.

3

AP

177.

5

AP

183.

5,6,8

AP

189.

6,7

C

17

2.

3

AP

178.

5,6,7

AN

184.

5,6,8

AP

190.

6,7

AP

Completion Statements

19 4

.

1

K

197.

1

K

199.

2

K

201.

5

K

203.

6

K

19 5

.

1

K

198.

1

K

200.

3

K

202.

6

K

204.

8

K

19 6

.

1

K

Matching Statements

20 5

.

1

K

Short-Answer Essay

20 6

.

4

S

208.

1

S

210.

3

S

20 7

.

5

S

209.

3

S

211.

1

S

SUMMARY OF LEARNING OBJECTIVES BY QUESTION TYPE

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Learning Objective 1

1.

TF

31.

TF

42.

MC

48.

MC

54.

MC

195.

C

211.

SA

2.

TF

32.

TF

43.

MC

49.

MC

55.

MC

196.

C

3.

TF

38.

MC

44.

MC

50.

MC

167.

Ex

197.

C

4.

TF

39.

MC

45.

MC

51.

MC

168.

Ex

198.

C

5.

TF

40.

MC

46.

MC

52.

MC

169.

Ex

205.

MA

6.

TF

41.

MC

47.

MC

53.

MC

194.

C

208.

SA

Learning Objective 2

7.

TF

9.

TF

57.

MC

59.

MC

61.

MC

63.

MC

199.

C

8.

TF

56.

MC

58.

MC

60.

MC

62.

MC

145.

MC

Learning Objective 3

10.

TF

15.

TF

67.

MC

72.

MC

77.

MC

157.

BE

171.

Ex

11.

TF

33.

TF

68.

MC

73.

MC

78.

MC

167.

Ex

172.

Ex

12.

TF

64.

MC

69.

MC

74.

MC

79.

MC

168.

Ex

200.

C

13.

TF

65.

MC

70.

MC

75.

MC

146.

MC

169.

Ex

209.

SA

14.

TF

66.

MC

71.

MC

76.

MC

147.

MC

170.

Ex

210.

SA

Learning Objective 4

16.

TF

80.

MC

82.

MC

84.

MC

148.

MC

174.

Ex

206.

SA

17.

TF

81.

MC

83.

MC

85.

MC

173.

Ex

175.

Ex

Learning Objective 5

18.

TF

86.

MC

92.

MC

98.

MC

150.

MC

177.

Ex

183.

Ex

19.

TF

87.

MC

93.

MC

99.

MC

151.

MC

178.

Ex

184.

Ex

20.

TF

88.

MC

94.

MC

100.

MC

158.

BE

179.

Ex

185.

Ex

21.

TF

89.

MC

95.

MC

101.

MC

159.

BE

180.

Ex

201.

C

22.

TF

90.

MC

96.

MC

102.

MC

160.

BE

181.

Ex

207.

SA

34.

TF

91.

MC

97.

MC

149.

MC

176.

Ex

182.

Ex

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 3

Learning Objective 6

22.

TF

100.

MC

108.

MC

116.

MC

152.

MC

178.

Ex

187.

Ex

23.

TF

101.

MC

109.

MC

117.

MC

153.

MC

179.

Ex

188.

Ex

24.

TF

102.

MC

110.

MC

118.

MC

161.

BE

180.

Ex

189.

Ex

25.

TF

103.

MC

111.

MC

119.

MC

162.

BE

181.

Ex

190.

Ex

26.

TF

104.

MC

112.

MC

120.

MC

163.

BE

182.

Ex

191.

Ex

35.

TF

105.

MC

113.

MC

121.

MC

168.

Ex

183.

Ex

202.

C

98.

MC

106.

MC

114.

MC

122.

MC

169.

Ex

184.

Ex

203.

C

99.

MC

107.

MC

115.

MC

123.

MC

175.

Ex

186.

Ex

Learning Objective 7

27.

TF

126.

MC

131.

MC

136.

MC

155.

MC

187.

Ex

192.

Ex

28.

TF

127.

MC

132.

MC

137.

MC

175.

Ex

188.

Ex

36.

TF

128.

MC

133.

MC

138.

MC

178.

Ex

189.

Ex

124.

MC

129.

MC

134.

MC

139.

MC

179.

Ex

190.

Ex

125.

MC

130.

MC

135.

MC

154.

MC

185.

Ex

191.

Ex

Learning Objective 8

29.

TF

140.

MC

143.

MC

164.

BE

168.

Ex

184.

Ex

204.

C

30.

TF

141.

MC

144.

MC

165.

BE

181.

Ex

187.

Ex

37.

TF

142.

MC

156.

MC

166.

BE

183.

Ex

193.

Ex

Note: TF = True-False BE = Brief Exercise C = Completion

MC = Multiple Choice Ex = Exercise MA = Matching

SA = Short-Answer Essay

CHAPTER LEARNING OBJECTIVES

1. Distinguish between variable and fixed costs. Variable costs are costs that vary in total

directly and proportionately with changes in the activity index. Fixed costs are costs that

remain the same in total regardless of changes in the activity index.

2. Explain the significance of the relevant range. The relevant range is the range of activity

in which a company expects to operate during a year. It is important in CVP analysis

because the behavior of costs is assumed to be linear throughout the relevant range.

3. Explain the concept of mixed costs. Mixed costs increase in total but not proportionately

with changes in the activity level. For purposes of CVP analysis, mixed costs must be

classified into their fixed and variable elements. One method that management may use to

classify these costs is the high-low method.

4. List the five components of cost-volume-profit analysis. The five components of CVP

analysis are (a) volume or level of activity, (b) unit selling prices, (c) variable cost per unit,

(d) total fixed costs, and (e) sales mix.

5. Indicate what contribution margin is and how it can be expressed. Contribution margin

is the amount of revenue remaining after deducting variable costs. It is identified in a CVP

income statement, which classifies costs as variable or fixed. It can be expressed as a total

amount, as a per unit amount, or as a ratio.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 4

6. Identify the three ways to determine the break-even point. The break-even point can be

(a) computed from a mathematical equation, (b) computed by using a contribution margin

technique, and (c) derived from a CVP graph.

7. Give the formulas for determining sales required to earn target net income. The

general formula for required sales is: Required sales = Variable costs + Fixed costs +

Target net income. Two other formulas are: Required sales in units = (Fixed costs + Target

net income) ÷ Contribution margin per unit, and Required sales in dollars = (Fixed costs +

Target net income) ÷ Contribution margin ratio.

8. Define margin of safety, and give the formulas for computing it. Margin of safety is the

difference between actual or expected sales and sales at the break-even point. The

formulas for margin of safety are: Actual (expected) sales – Break-even sales = Margin of

safety in dollars; Margin of safety in dollars ÷ Actual (expected) sales = Margin of safety

ratio.

TRUE-FALSE STATEMENTS

1. An activity index identifies the activity that has a causal relationship with a particular cost.

2. A variable cost remains constant per unit at various levels of activity.

3. A fixed cost remains constant in total and on a per unit basis at various levels of activity.

4. If volume increases, all costs will increase.

5. If the activity index decreases, total variable costs will decrease proportionately.

6. Changes in the level of activity will cause unit variable and unit fixed costs to change in

opposite directions.

7. For CVP analysis, both variable and fixed costs are assumed to have a linear relationship

within the relevant range of activity.

8. The relevant range of activity is the activity level where the firm will earn income.

9. Costs will not change in total within the relevant range of activity.

Cost-Volume-Profit

18 – 5

10. The high-low method is used in classifying a mixed cost into its variable and fixed

elements.

11. A mixed cost has both selling and administrative cost elements.

12. The fixed cost element of a mixed cost is the cost of having a service available.

13. For planning purposes, mixed costs are generally grouped with fixed costs.

14. The difference between the costs at the high and low levels of activity represents the fixed

cost element of a mixed cost.

15. When applying the high-low method, the variable cost element of a mixed cost is

calculated before the fixed cost element.

16. An assumption of CVP analysis is that all costs can be classified as either variable or

fixed.

17. In CVP analysis, the term “cost” includes manufacturing costs, and selling and

administrative expenses.

18. Contribution margin is the amount of revenues remaining after deducting cost of goods

sold.

19. Unit contribution margin is the amount that each unit sold contributes towards the

recovery of fixed costs and to income.

20. The contribution margin ratio is calculated by multiplying the unit contribution margin by

the unit sales price.

21. Both variable and fixed costs are included in calculating the contribution margin.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 6

22. A CVP income statement shows contribution margin instead of gross profit.

23. The break-even point is where total sales equal total variable costs.

24. The break-even point is where total sales equal total variable costs.

25. The break-even point is equal to the fixed costs plus net income.

26. If the unit contribution margin is $1 and unit sales are 10,000 units above the break-even

volume, then net income will be $10,000.

27. A target net income is calculated by taking actual sales minus the margin of safety.

28. Target net income is the income objective for an individual product line.

29. The margin of safety is the difference between sales at breakeven and sales at a

determined activity level.

30. The margin of safety is the difference between contribution margin and fixed costs.

31. The activity level is represented by an activity index such as direct labor hours, units of

output, or sales dollars.

32. The trend in most companies is to have more variable costs and fewer fixed costs.

33. For purposes of CVP analysis, mixed costs must be classified into their fixed and variable

elements.

34. The contribution margin ratio of 40% means that 60 cents of each sales dollar is available

to cover fixed costs and to produce a profit.

Cost-Volume-Profit

18 – 7

35. A cost-volume-profit graph shows the amount of net income or loss at each level of sales.

36. If variable costs per unit are 70% of sales, fixed costs are $290,000 and target net income

is $70,000, required sales are $1,200,000.

37. The margin of safety ratio is equal to the margin of safety in dollars divided by the actual

or (expected) sales.

Answers to True-False Statements

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

1.

T

7.

T

13.

F

19.

T

25.

F

31.

T

37.

T

2.

T

8.

F

14.

F

20.

F

26.

T

32.

F

3.

F

9.

F

15.

T

21.

F

27.

F

33.

T

4.

F

10.

T

16.

T

22.

T

28.

T

34.

F

5.

T

11.

F

17.

T

23.

F

29.

T

35.

T

6.

F

12.

T

18.

F

24.

F

30.

F

36.

T

MULTIPLE CHOICE QUESTIONS

38. For an activity base to be useful in cost behavior analysis,

a. the activity should always be stated in dollars.

b. there should be a correlation between changes in the level of activity and changes in

costs.

c. the activity should always be stated in terms of units.

d. the activity level should be constant over a period of time.

39. A variable cost is a cost that

a. varies per unit at every level of activity.

b. occurs at various times during the year.

c. varies in total in proportion to changes in the level of activity.

d. may or may not be incurred, depending on management’s discretion.

40. A cost which remains constant per unit at various levels of activity is a

a. variable cost.

b. fixed cost.

c. mixed cost.

d. manufacturing cost.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 8

41. Two costs at Bradshaw Company appear below for specific months of operation.

Month Amount Units Produced

Delivery costs September $ 40,000 40,000

October 55,000 60,000

Utilities September $ 84,000 40,000

October 126,000 60,000

Which type of costs are these?

a. Delivery costs and utilities are both variable.

b. Delivery costs and utilities are both mixed.

c. Utilities are mixed and delivery costs are variable.

d. Delivery costs are mixed and utilities are variable.

42. An increase in the level of activity will have the following effects on unit costs for variable

and fixed costs:

Unit Variable Cost Unit Fixed Cost

a. Increases Decreases

b. Remains constant Remains constant

c. Decreases Remains constant

d. Remains constant Decreases

43. A fixed cost is a cost which

a. varies in total with changes in the level of activity.

b. remains constant per unit with changes in the level of activity.

c. varies inversely in total with changes in the level of activity.

d. remains constant in total with changes in the level of activity.

44. Fixed costs normally will not include

a. property taxes.

b. direct labor.

c. supervisory salaries.

d. depreciation on buildings and equipment.

45. The increased use of automation and less use of the work force in companies has caused

a trend towards an increase in

a. both variable and fixed costs.

b. fixed costs and a decrease in variable costs.

c. variable costs and a decrease in fixed costs.

d. variable costs and no change in fixed costs.

Cost-Volume-Profit

18 – 9

46. Cost behavior analysis is a study of how a firm’s costs

a. relate to competitors’ costs.

b. relate to general price level changes.

c. respond to changes in the level of business activity.

d. respond to changes in the gross national product.

47. Cost behavior analysis applies to

a. retailers.

b. wholesalers.

c. manufacturers.

d. all entities.

48. If a firm increases its activity level,

a. costs should remain the same.

b. most costs will rise.

c. no costs will remain the same.

d. some costs will change, others will remain the same.

49. An activity index might be referred to as a cost

a. driver.

b. multiplier.

c. element.

d. correlation.

50. Cost activity indexes might help classify costs as

a. temporary.

b. permanent.

c. variable.

d. transient.

51. Which of the following is not a cost classification?

a. Mixed

b. Multiple

c. Variable

d. Fixed

52. If the activity level increases 10%, total variable costs will

a. remain the same.

b. increase by more than 10%.

c. decrease by less than 10%.

d. increase 10%.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 10

53. Which of the following costs are variable?

Cost 10,000 Units 30,000 Units

1. $100,000 $300,000

2. 40,000 240,000

3. 90,000 90,000

4. 50,000 150,000

a. 1 and 2

b. 1 and 4

c. only 1

d. only 2

54. Changes in activity have a(n) _________ effect on fixed costs per unit.

a. positive

b. negative

c. inverse

d. neutral

55. Which of the following is not a fixed cost?

a. Direct materials

b. Depreciation

c. Lease charge

d. Property taxes

56. Why is identification of a relevant range important?

a. It is required under GAAP.

b. Cost behavior outside of the relevant range is not linear, which distorts CVP analysis.

c. It directly impacts the number of units of product a customer buys.

d. It is a cost that is incurred by a company that must be accounted for.

57. The relevant range of activity refers to the

a. geographical areas where the company plans to operate.

b. activity level where all costs are curvilinear.

c. levels of activity over which the company expects to operate.

d. level of activity where all costs are constant.

58. Which of the following is not a plausible explanation of why variable costs often behave in

a curvilinear fashion?

a. Labor specialization

b. Overtime wages

c. Total variable costs are constant within the relevant range

d. Availability of quantity discounts

Cost-Volume-Profit

18 – 11

59. Firms operating at 100% capacity

a. are common.

b. are the exception rather than the rule.

c. have no fixed costs.

d. have no variable costs.

60. Which of the following would be the least controllable fixed costs?

a. Property taxes

b. Rent

c. Research and development

d. Management training programs

61. Which one of the following is a name for the range over which a company expects to

operate?

a. Mixed range

b. Fixed range

c. Variable range

d. Relevant range

62. If graphed, fixed costs that behave in a curvilinear fashion resemble a(n)

a. S-curve.

b. inverted S-curve.

c. straight line.

d. stair-step pattern.

63. The graph of variable costs that behave in a curvilinear fashion will

a. approximate a straight line within the relevant range.

b. be sharply kinked on both sides of the relevant range.

c. be downward sloping.

d. be a stair-step pattern.

64. Frazier Manufacturing Company collected the following production data for the past

month:

Units Produced Total Cost

1,600 $44,000

1,300 38,000

1,500 45,000

1,100 33,000

If the high-low method is used, what is the monthly total cost equation?

a. Total cost = $8,800 + $22/unit

b. Total cost = $11,000 + $20/unit

c. Total cost = $0 + $30/unit

d. Total cost = $6,600 + $24/unit

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 12

65. A mixed cost contains

a. a variable element and a fixed element.

b. both selling and administrative costs.

c. both retailing and manufacturing costs.

d. both operating and nonoperating costs.

66. At the high level of activity in November, 7,000 machine hours were run and power costs

were $16,000. In April, a month of low activity, 2,000 machine hours were run and power

costs amounted to $8,000. Using the high-low method, the estimated fixed cost element of

power costs is

a. $16,000.

b. $8,000.

c. $4,800.

d. $11,200.

67. Gribble Company’s high and low level of activity last year was 60,000 units of product

produced in May and 20,000 units produced in November. Machine maintenance costs

were $104,000 in May and $40,000 in November. Using the high-low method, determine

an estimate of total maintenance cost for a month in which production is expected to be

45,000 units.

a. $90,000

b. $96,000

c. $78,000

d. $80,000

68. Which of the following is not true about the graph of a mixed cost?

a. It is possible to determine the amount of the fixed cost from the graph.

b. There is a total cost line on the graph.

c. The fixed cost portion of the graph is the same amount at all levels of activity.

d. The variable cost portion of the graph is rectangular in shape.

69. Which of the following is not a mixed cost?

a. Car rental fee

b. Electricity

c. Depreciation

d. Telephone Expense

Cost-Volume-Profit

18 – 13

70. In using the high-low method, the fixed cost

a. is determined by subtracting the total cost at the high level of activity from the total

cost at the low activity level.

b. is determined by adding the total variable cost to the total cost at the low activity level.

c. is determined before the total variable cost.

d. may be determined by subtracting the total variable cost from either the total cost at

the low or high activity level.

71. If Qualls Quality Airline cuts its domestic fares by 30%,

a. its fixed costs will decrease.

b. profit will increase by 30%.

c. a profit can only be earned by decreasing the number of flights.

d. a profit can be earned either by increasing the number of passengers or by decreasing

variable costs.

72. In applying the high-low method, which months are relevant?

Month Miles Total Cost

January 80,000 $144,000

February 50,000 120,000

March 70,000 141,000

April 90,000 195,000

a. January and February

b. January and April

c. February and April

d. February and March

73. In applying the high-low method, what is the unit variable cost?

Month Miles Total Cost

January 80,000 $144,000

February 50,000 120,000

March 70,000 141,000

April 90,000 195,000

a. $2.16

b. $1.88

c. $2.40

d. Cannot be determined from the information given.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 14

74. In applying the high-low method, what is the fixed cost?

Month Miles Total Cost

January 80,000 $144,000

February 50,000 120,000

March 70,000 141,000

April 90,000 195,000

a. $26,250

b. $54,000

c. $21,000

d. $75,000

75. For analysis purposes, the high-low method usually produces a (n)

a. reasonable estimate.

b. precise estimate.

c. overstated estimate.

d. understated estimate.

76. The high-low method is criticized because it

a. is not a graphical method.

b. is a mathematical method.

c. ignores much of the available data by concentrating on only the extreme points.

d. doesn’t provide reasonable estimates.

77. The high-low method is often employed in analyzing

a. fixed costs.

b. mixed costs.

c. variable costs.

d. conversion costs.

78. Portman Company’s activity for the first three months of 2013 are as follows:

Machine Hours Electrical Cost

January 2,100 $3,600

February 2,600 $4,350

March 2,900 $4,800

Using the high-low method, how much is the cost per machine hour?

a. $1.50

b. $2.25

c. $1.69

d. $1.34

Cost-Volume-Profit

18 – 15

79. Ponszko Nursery used high-low data from June and July to determine its variable cost of

$18 per unit. Additional information follows:

Month Units produced Total costs

June 2,000 $48,000

July 1,000 30,000

If Ponszko’s produces 2,300 units in August, how much is its total cost expected to be?

a. $12,000

b. $59,400

c. $41,400

d. $53,400

80. In CVP analysis, the term “cost”

a. includes only manufacturing costs.

b. means cost of goods sold.

c. includes manufacturing costs plus selling and administrative expenses.

d. excludes all fixed manufacturing costs.

81. Which one of the following is not an assumption of CVP analysis?

a. All units produced are sold.

b. All costs are variable costs.

c. Sales mix remains constant.

d. The behavior of costs and revenues are linear within the relevant range.

82. CVP analysis does not consider

a. level of activity.

b. fixed cost per unit.

c. variable cost per unit.

d. sales mix.

83. Which of the following is not an underlying assumption of CVP analysis?

a. Changes in activity are the only factors that affect costs.

b. Cost classifications are reasonably accurate.

c. Beginning inventory is larger than ending inventory.

d. Sales mix is constant.

84. CVP analysis is not important in

a. calculating depreciation expense.

b. setting selling prices.

c. determining the product mix.

d. utilizing production facilities.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 16

85. To which function of management is CVP analysis most applicable?

a. Planning

b. Motivating

c. Directing

d. Controlling

86. Hollis Industries produces flash drives for computers, which it sells for $20 each. Each

flash drive costs $12 of variable costs to make. During April, 1,000 drives were sold. Fixed

costs for March were $2 per unit for a total of $1,000 for the month. How much is the

contribution margin ratio?

a. 30%

b. 40%

c. 60%

d. 70%

87. Contribution margin

a. is always the same as gross profit margin.

b. excludes variable selling costs from its calculation.

c. is calculated by subtracting total manufacturing costs per unit from sales revenue per

unit.

d. equals sales revenue minus variable costs.

88. If a company had a contribution margin of $750,000 and a contribution margin ratio of

40%, total variable costs must have been

a. $1,125,000.

b. $450,000.

c. $1,875,000.

d. $300,000.

89. Which of the following would not be an acceptable way to express contribution margin?

a. Sales minus variable costs

b. Sales minus unit costs

c. Unit selling price minus unit variable costs

d. Contribution margin per unit divided by unit selling price

Cost-Volume-Profit

18 – 17

90. A company has contribution margin per unit of $90 and a contribution margin ratio of 40%.

What is the unit selling price?

a. $150

b. $225

c. $36

d. Cannot be determined.

91. Sales are $500,000 and variable costs are $350,000. What is the contribution margin ratio?

a. 43%

b. 30%

c. 70%

d. Cannot be determined because amounts are not expressed per unit.

92. Dunbar Manufacturing’s variable costs are 30% of sales. The company is contemplating

an advertising campaign that will cost $44,000. If sales are expected to increase $80,000,

by how much will the company’s net income increase?

a. $36,000

b. $56,000

c. $24,000

d. $12,000

93. Weatherspoon Company has a product with a selling price per unit of $200, the unit

variable cost is $90, and the total monthly fixed costs are $300,000. How much is

Weatherspoon’s contribution margin ratio?

a. 55%

b. 45%

c. 150%

d. 222%

94. Armstrong Industries has a contribution margin of $300,000 and a contribution margin

ratio of 30%. How much are total variable costs?

a. $90,000

b. $700,000

c. $210,000

d. $1,000,000

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 18

95. Zehms, Inc. has a contribution margin per unit of $21 and a contribution margin ratio of

60%. How much is the selling price of each unit?

a. $35.00

b. $52.50

c. $12.60

d. Cannot be determined without more information.

96. A division sold 100,000 calculators during 2013:

Sales $2,000,000

Variable costs:

Materials $380,000

Order processing 150,000

Billing labor 110,000

Selling expenses 60,000

Total variable costs 700,000

Fixed costs 1,000,000

How much is the contribution margin per unit?

a. $2

b. $7

c. $17

d. $13

97. At the break-even point of 2,000 units, variable costs are $110,000, and fixed costs are

$64,000. How much is the selling price per unit?

a. $87

b. $23

c. $32

d. Not enough information

98. The following information is available for Wade Corp.:

Sales $550,000 Total fixed expenses $150,000

Cost of goods sold 390,000 Total variable expenses 360,000

A CVP income statement would report

a. gross profit of $160,000.

b. contribution margin of $400,000.

c. gross profit of $190,000.

d. contribution margin of $190,000.

Cost-Volume-Profit

18 – 19

99. Which is the true statement?

a. In a CVP income statement, costs and expenses are classified only by function.

b. The CVP income statement is prepared for both internal and external use.

c. The CVP income statement shows contribution margin instead of gross profit.

d. In a traditional income statement, costs and expenses are classified as either variable

or fixed.

100. The equation which reflects a CVP income statement is

a. Sales = Cost of goods sold + Operating expenses + Net income.

b. Sales + Fixed costs = Variable costs + Net income.

c. Sales – Variable costs + Fixed costs = Net income.

d. Sales – Variable costs – Fixed costs = Net income.

101. The CVP income statement

a. is distributed internally and externally.

b. classifies costs by functions.

c. discloses contribution margin in the body of the statement.

d. will reflect a different net income than the traditional income statement.

102. O’Malley Company sells 100,000 units for $13 a unit. Fixed costs are $350,000 and net

income is $250,000. What should be reported as variable expenses in the CVP income

statement?

a. $600,000.

b. $700,000.

c. $950,000.

d. $1,050,000.

103. A company has total fixed costs of $200,000 and a contribution margin ratio of 20%. The

total sales necessary to break even are

a. $800,000.

b. $1,000,000.

c. $250,000.

d. $240,000.

104. A company sells a product which has a unit sales price of $5, unit variable cost of $3 and

total fixed costs of $180,000. The number of units the company must sell to break even is

a. 90,000 units.

b. 36,000 units.

c. 360,000 units.

d. 60,000 units.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 20

105. The break-even point is where

a. total sales equal total variable costs.

b. contribution margin equals total fixed costs.

c. total variable costs equal total fixed costs.

d. total sales equal total fixed costs.

106. The break-even point cannot be determined by

a. computing it from a mathematical equation.

b. computing it using contribution margin.

c. reading the prior year’s financial statements.

d. deriving it from a CVP graph.

107. Select the correct statement concerning the

cost-volume-profit graph at right:

a. The point identified by “B” is the break-

even point.

b. Line F is the variable cost line.

c. At point B, profits equal total costs.

d. Line E is the total cost line.

108. Fixed costs are $600,000 and the variable costs are 75% of the unit selling price. What is

the break-even point in dollars?

a. $1,400,000

b. $1,800,000

c. $2,400,000

d. $800,000

109. Fixed costs are $2,400,000 and the contribution margin per unit is $150. What is the

break-even point?

a. $6,000,000

b. $16,000,000

c. 6,000 units

d. 16,000 units

Cost-Volume-Profit

18 – 21

110. Nelson Manufacturing has the following data:

Variable costs are 60% of the unit selling price.

The contribution margin ratio is 40%.

The contribution margin per unit is $500.

The fixed costs are $300,000.

Which of the following does not express the break-even point?

a. $300,000 + .60X = X

b. $300,000 + .40X = X

c. $300,000 ÷ $500 = X

d. $300,000 ÷ .40 = X

111. A CVP graph does not include a

a. variable cost line.

b. fixed cost line.

c. sales line.

d. total cost line.

112. Boswell company reported the following information for the current year: Sales (50,000

units) $1,000,000, direct materials and direct labor $500,000, other variable costs

$50,000, and fixed costs $270,000. What is Boswell’s contribution margin ratio?

a. 68%.

b. 45%.

c. 32%.

d. 55%.

113. Boswell company reported the following information for the current year: Sales (50,000

units) $1,000,000, direct materials and direct labor $500,000, other variable costs

$50,000, and fixed costs $270,000. What is Boswell’s break–even point in units?

a. 24,546.

b. 30,000.

c. 38,334.

d. 42,188.

114. Walters Corporation sells radios for $50 per unit. The fixed costs are $420,000 and the

variable costs are 60% of the selling price. As a result of new automated equipment, it is

anticipated that fixed costs will increase by $100,000 and variable costs will be 50% of the

selling price. The new break-even point in units is:

a. 21,000

b. 20,800

c. 20,600

d. 16,800

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 22

115. Cunningham, Inc. sells MP3 players for $60 each. Variable costs are $40 per unit, and

fixed costs total $90,000. What sales are needed by Cunningham to break even?

a. $120,000.

b. $225,000.

c. $270,000.

d. $360,000.

116. Cunningham, Inc. sells MP3 players for $60 each. Variable costs are $40 per unit, and

fixed costs total $90,000. How many MP3 players must Cunningham sell to earn net

income of $210,000?

a. 15,000.

b. 5,250.

c. 3,750.

d. 4,500.

117. Gall Manufacturing sells a product for $50 per unit. The fixed costs are $735,000 and the

variable costs are 60% of the selling price. As a result of new automated equipment, it is

anticipated that fixed costs will increase by $175,000 and variable costs will be 50% of the

selling price. The new break-even point in units is:

a. 36,750.

b. 36,400.

c. 36,050.

d. 29,400.

118. Pascal, Inc. is planning to sell 800,000 units for $1.50 per unit. The contribution margin

ratio is 20%. If Pascal will break even at this level of sales, what are the fixed costs?

a. $240,000.

b. $560,000.

c. $800,000.

d. $960,000.

119. April Industries sells a product with a contribution margin of $12 per unit, fixed costs of

$148,800, and sales for the current year of $200,000. How much is April’s break-even

point?

a. 9,200 units

b. $51,200

c. 12,400 units

d. 4,267 units

Cost-Volume-Profit

18 – 23

120. Kaplan, Inc. produces flash drives for computers, which it sells for $20 each. The variable

cost to make each flash drive is $13. During April, 700 drives were sold. Fixed costs for

April were $2 per unit for a total of $1,400 for the month. How much is the monthly break-

even level of sales in dollars for Kaplan?

a. $200

b. $4,000

c. $14,000

d. $8,400

121. Vintage Wines has fixed costs of $15,000 per year. Its warehouse sells wine with variable

costs of 80% of its unit selling price. How much in sales does Vintage need to break even

per year?

a. $12,000

b. $3,000

c. $18,750

d. $75,000

122. Bruno & Court is a nonprofit organization that captures stray deer bewildered within

residential communities. Fixed costs are $15,000. The variable cost of capturing each

deer is $10 each. Bruno & Court is funded by a local philanthropy in the amount of

$48,000 for 2013. How many deer can Bruno & Court capture during 2013?

a. 3,300

b. 4,800

c. 6,300

d. 3,000

123. At the break-even point of 2,000 units, variable costs are $55,000, and fixed costs are

$32,000. How much is the selling price per unit?

a. $43.50

b. $11.50

c. $16.00

d. $27.50

124. Variable costs for Abbey, Inc. are 25% of sales. Its selling price is $80 per unit. If Abbey

sells one unit more than break-even units, how much will profit increase?

a. $60

b. $20

c. $25

d. $320

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 24

125. A company requires $1,360,000 in sales to meet its net income target. Its contribution

margin is 30%, and fixed costs are $240,000. What is the target net income?

a. $408,000

b. $312,000

c. $560,000

d. $168,000

126. Montoya Manufacturing has fixed costs of $2,500,000 and variable costs are 40% of

sales. What are the required sales if Montoya desires net income of $250,000?

a. $4,583,333

b. $4,166,667

c. $6,875,000

d. $6,250,000

127. Aero, Inc. requires sales of $2,000,000 to cover its fixed costs of $400,000 and to earn net

income of $500,000. What percent are variable costs of sales?

a. 25%

b. 55%

c. 20%

d. 45%

128. Lansbury Manufacturing produces hair brushes. The selling price is $20 per unit and the

variable costs are $8 per brush. Fixed costs per month are $4,800. If Lansbury sells 25

more units beyond breakeven, how much does profit increase as a result?

a. $300

b. $500

c. $200

d. $1,000

129. Hayduke Corporation reported the following results from the sale of 6,000 units in May:

sales $300,000, variable costs $180,000, fixed costs $90,000, and net income $30,000.

Assume that Hayduke increases the selling price by 10% on June 1. How many units will

have to be sold in June to maintain the same level of net income?

a. 4,800.

b. 5,160.

c. 5,400.

d. 6,000.

Cost-Volume-Profit

18 – 25

130. Keene, Inc. produces flash drives for computers, which it sells for $20 each. Each flash

drive costs $6 of variable costs to make. During March, 1,000 drives were sold. Fixed costs

for March were $4.90 per unit for a total of $4,900 for the month. If variable costs decrease

by 10%, what happens to the break-even level of units per month for Keene?

a. It is 10% higher than the original break-even point.

b. It decreases about 14 units.

c. It decreases about 35 units.

d. It depends on the number of units the company expects to produce and sell.

131. Reliable Manufacturing wants to sell a sufficient quantity of products to earn a profit of

$80,000. If the unit sales price is $10, unit variable cost is $8, and total fixed costs are

$160,000, how many units must be sold to earn income of $80,000?

a. 120,000 units

b. 80,000 units

c. 30,000 units

d. 1,200,000 units

132. How much sales are required to earn a target income of $160,000 if total fixed costs are

$200,000 and the contribution margin ratio is 40%?

a. $600,000

b. $400,000

c. $900,000

d. $660,000

133. Farmers’ Industries has fixed costs of $400,000 and variable costs are 60% of sales. How

much will Farmers report as sales when its net income equals $40,000?

a. $1,100,000

b. $733,333

c. $1,040,000

d. $264,000

134. Murphy Company produces flash drives for computers, which it sells for $20 each. Each

flash drive costs $8 of variable costs to make. During April, 700 drives were sold. Fixed

costs for April were $4 per unit for a total of $2,800 for the month. How much does

Murphy’s operating income increase for each $1,000 increase in revenue per month?

a. $600

b. $400

c. $14,000

d. Not enough information to determine the answer.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 26

135. Greg’s Golf Carts produces two models: Model 24 has sales of 500 units with a

contribution margin of $40 each; Model 26 has sales of 350 units with a contribution

margin of $50 each. If sales of Model 26 increase by 100 units, how much will profit

change?

a. $5,000 increase

b. $17,500 increase

c. $22,500 increase

d. $35,000 increase

136. Wendy Industries produces only one product. Monthly fixed expenses are $12,000,

monthly unit sales are 2,500, and the unit contribution margin is $10. How much is

monthly net income?

a. $25,000

b. $37,000

c. $0

d. $13,000

137. A company desires to sell a sufficient quantity of products to earn a profit of $300,000. If

the unit sales price is $20, unit variable cost is $12, and total fixed costs are $600,000,

how many units must be sold to earn net income of $300,000?

a. 168,750 units

b. 112,500 units

c. 90,000 units

d. 67,500 units

138. Stephanie, Inc. sells its product for $40. The variable costs are $18 per unit. Fixed costs

are $16,000. The company is considering the purchase of an automated machine that will

result in a $2 reduction in unit variable costs and an increase of $5,000 in fixed costs.

Which of the following is true about the break-even point in units?

a. It will remain unchanged.

b. It will decrease.

c. It will increase.

d. It cannot be determined from the information provided.

Cost-Volume-Profit

18 – 27

139. How much sales are required to earn a target net income of $160,000 if total fixed costs

are $200,000 and the contribution margin ratio is 40%?

a. $500,000

b. $810,000

c. $900,000

d. $400,000

140. The following monthly data are available for Lumberyard Company. which produces only

one product: Selling price per unit, $42; Unit variable expenses, $14; Total fixed expenses,

$84,000; Actual sales for the month of June, 4,000 units. How much is the margin of

safety for the company for June?

a. $84,000

b. $42,000

c. $126,000

d. $1,000

141. Danny’s Lawn Equipment has actual sales of $800,000 and a break-even point of

$600,000. How much is its margin of safety ratio?

a. 25%

b. 33%

c. 67%

d. 75%

142. The following monthly data are available for Seasons Company which produces only one

product: Selling price per unit, $42; Unit variable expenses, $14; Total fixed expenses,

$84,000; Actual sales for the month of June, 5,000 units. How much is the margin of

safety for the company for June?

a. $56,000

b. $84,000

c. $126,000

d. $2,000

143. The amount by which actual or expected sales exceeds break-even sales is referred to as

a. contribution margin.

b. unanticipated profit.

c. margin of safety.

d. target net income.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 28

144. In evaluating the margin of safety, the

a. break-even point is not relevant.

b. higher the margin of safety ratio, the greater the margin of safety.

c. higher the dollar amount, the lower the margin of safety.

d. higher the margin of safety ratio, the lower the fixed costs.

145. Within the relevant range, the variable cost per unit

a. differs at each activity level.

b. remains constant at each activity level.

c. increases as production increases.

d. decreases as production increases.

146. An example of a mixed cost is

a. direct materials.

b. supervisory salaries.

c. utility costs.

d. property taxes.

147. In the Restin Company, maintenance costs are a mixed cost. At the low level of activity

(160 direct labor hours), maintenance costs are $600. At the high level of activity (400

direct labor hours), maintenance costs are $1,100. Using the high-low method, what is the

variable maintenance cost per unit and the total fixed maintenance cost?

Variable Cost Per Unit Total Fixed Cost

a. $2.08 $268

b. $2.08 $500

c. $2.75 $220

d. $2.75 $400

148. Cost-volume-profit analysis includes all of the following assumptions except

a. the behavior of costs is curvilinear throughout the relevant range.

b. costs can be classified accurately as either variable or fixed.

c. changes in activity are the only factors that affect costs.

d. all units produced are sold.

149. The contribution margin ratio increases when

a. fixed costs increase.

b. fixed costs decrease.

c. variable costs as a percentage of sales decrease.

d. variable costs as a percentage of sales increase.

Cost-Volume-Profit

18 – 29

150. Contribution margin is

a. the amount of revenue remaining after deducting fixed costs.

b. available to cover fixed costs and contribute to income for the company.

c. sales less fixed costs.

d. unit selling price less unit fixed costs.

151. Chung, Inc. sells 100,000 wrenches for $18 per unit. Fixed costs are $525,000 and net

income is $375,000. What should be reported as variable expenses in the CVP income

statement?

a. $810,000

b. $900,000

c. $1,425,000

d. $1,275,000

152. Sweet Manufacturing is planning to sell 400,000 hammers for $3 per unit. The contribution

margin ratio is 20%. If Sweet will break even at this level of sales, what are the fixed

costs?

a. $240,000

b. $560,000

c. $800,000

d. $960,000

153. At the break-even point,

a. sales equal total variable costs.

b. contribution margin equals total variable costs.

c. contribution margin equals total fixed costs.

d. sales equal total fixed costs.

154. Wilton Co. reported the following results from the sale of 5,000 hammers in May: sales

$200,000, variable costs $120,000, fixed costs $60,000, and net income $20,000. Assume

that Wilton increases the selling price of hammers by 10% on June 1. How many

hammers will have to be sold in June to maintain the same level of net income?

a. 4,000

b. 4,300

c. 4,500

d. 5,000

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 30

155. Required sales in dollars to meet a target net income is computed by dividing

a. fixed costs plus target net income by contribution margin per unit.

b. variable costs plus target net income by contribution margin per unit.

c. fixed costs plus target net income by contribution margin ratio.

d. total costs plus target net income by contribution margin ratio.

156. Bolton Industries had actual sales of $750,000 when break-even sales were $600,000.

What is the margin of safety ratio?

a. 20%

b. 25%

c. 75%

d. 80%

Answers to Multiple Choice Questions

Cost-Volume-Profit

18 – 31

BRIEF EXERCISES

BE 157

Dollywood Corporation accumulates the following data concerning a mixed cost, using miles as

the activity level.

Miles Driven

Total Cost

Miles Driven

Total Cost

January

10,000

$15,000

March

9,000

$12,500

February

8,000

$14,500

April

7,500

$12,000

Instructions

Compute the variable and fixed cost elements using the high-low method.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 32

BE 158

Sandel Company makes 2 products, footballs and baseballs. Additional information follows:

Footballs Baseballs

Units 4,000 2,500

Sales $60,000 $25,000

Variable costs 36,000 7,000

Fixed costs 9,000 9,000

Net income $15,000 $ 9,000

Profit per unit $3.75 $3.60

Instructions

Sandel has unlimited demand for both products. Therefore, which product should Sandel tell his

sales people to emphasize?

BE 159

Determine the missing amounts.

Unit Selling Price

Unit Variable Costs

Contribution Margin

per Unit

Contribution

Margin Ratio

1.

$300

$195

A.

B.

2.

$600

C.

$150

D.

3.

E.

F.

$480

40%

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 33

BE 160

Kipling Company has sales of $1,500,000 for the first quarter of 2013. In making the sales, the

company incurred the following costs and expenses.

Variable

Fixed

Product costs

$500,000

$550,000

Selling expenses

100,000

75,000

Administrative expenses

80,000

67,000

Instructions

Calculate net income under CVP for 2013.

BE 161

Hurly Co. has fixed costs totaling $132,000. Its contribution margin per unit is $1.50, and the

selling price is $5.50 per unit.

Instructions

Compute the break-even point in units.

BE 162

Salem Bakery sells boxes of donuts each with a variable cost percentage of 35%. Its fixed costs

are $54,600 per year.

Instructions

Determine the sales dollars Salem needs to break even per year.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 34

BE 163

Cannon Co. has a unit selling price of $500, variable cost per unit $300, and fixed costs of

$210,000.

Instructions

Compute the break-even point in units and in sales dollars.

BE 164

Oakbrook, Inc. reported actual sales of $2,000,000, and fixed costs of $350,000. The contribution

margin ratio is 25%.

Instructions

Compute the margin of safety in dollars and the margin of safety ratio.

BE 165

The following monthly data are available for Fortner Industries which produces only one product

which it sells for $18 each. Its unit variable costs are $8, and its total fixed expenses are $16,000.

Actual sales for the month of May totaled 2,000 units.

Instructions

Compute the margin of safety in dollars for the company for May.

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 35

BE 166

At break-even point, a company sells 1,200 widgets. Its selling price is $6 per widget, variable

cost is $2 per widget, and its fixed cost is $4 per widget.

Instructions

If it sells 200 additional widgets, determine the company’s incremental profit.

EXERCISES

Ex. 167

Sandburg Manufacturing manufactures a single product. Annual production costs incurred in the

manufacturing process are shown below for the production of 2,000 units. The Utilities and

Maintenance are mixed costs. The fixed portions of these costs are $300 and $200, respectively.

Costs Incurred

Production in Units 2,000 4,000

Production Costs

a. Direct Materials $ 4,000 ?

b. Direct Labor 16,000 ?

c. Utilities 1,000 ?

d. Rent 3,000 ?

e. Indirect Labor 4,200 ?

f. Supervisory Salaries 1,500 ?

g. Maintenance 900 ?

h. Depreciation 2,500 ?

Instructions

Calculate the expected costs to be incurred when production is 4,000 units. Use your knowledge

of cost behavior to determine which of the other costs are fixed or variable.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 36

Ex. 168

Bill Braddock is considering opening a Fast ‘n Clean Car Service Center. He estimates that the

following costs will be incurred during his first year of operations: Rent $9,200, Depreciation on

equipment $7,000, Wages $16,400, Motor oil $2.00 per quart. He estimates that each oil change

will require 5 quarts of oil. Oil filters will cost $3.00 each. He must also pay The Fast ‘n Clean

Corporation a franchise fee of $1.10 per oil change, since he will operate the business as a

franchise. In addition, utility costs are expected to behave in relation to the number of oil changes

as follows:

Number of Oil Changes Utility Costs

4,000 $ 6,000

6,000 $ 7,300

9,000 $ 9,600

12,000 $12,600

14,000 $15,000

Bill Braddock anticipates that he can provide the oil change service with a filter at $25 each.

Instructions

(a) Using the high-low method, determine variable costs per unit and total fixed costs.

(b) Determine the break-even point in number of oil changes and sales dollars.

(c) Without regard to your answers in parts (a) and (b), determine the oil changes required to

earn net income of $20,000, assuming fixed costs are $32,000 and the contribution margin

per unit is $8.

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 37

Ex. 169

Jane Botosan operates a bed and breakfast hotel in a resort area near Lake Michigan.

Depreciation on the hotel is $60,000 per year. Jane employs a maintenance person at an annual

salary of $32,000 and a cleaning person at an annual salary of $24,000. Real estate taxes are

$10,000 per year. The rooms rent at an average price of $60 per person per night including

breakfast. Other costs are laundry and cleaning service at a cost of $10 per person per night and

the cost of food which is $5 per person per night.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 38

Ex. 169 (Cont.)

Instructions

(a) Determine the number of rentals and the sales revenue Jane needs to break even using the

contribution margin technique.

(b) If the current level of rentals is 3,500, by what percentage can rentals decrease before Jane

has to worry about having a net loss?

(c) Jane is considering upgrading the breakfast service to attract more business and increase

prices. This will cost an additional $3 for food costs per person per night. Jane feels she can

increase the room rate to $66 per person per night. Determine the number of rentals and the

sales revenue Jane needs to break even if the changes are made.

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 39

Solution 169 (Cont.)

Ex. 170

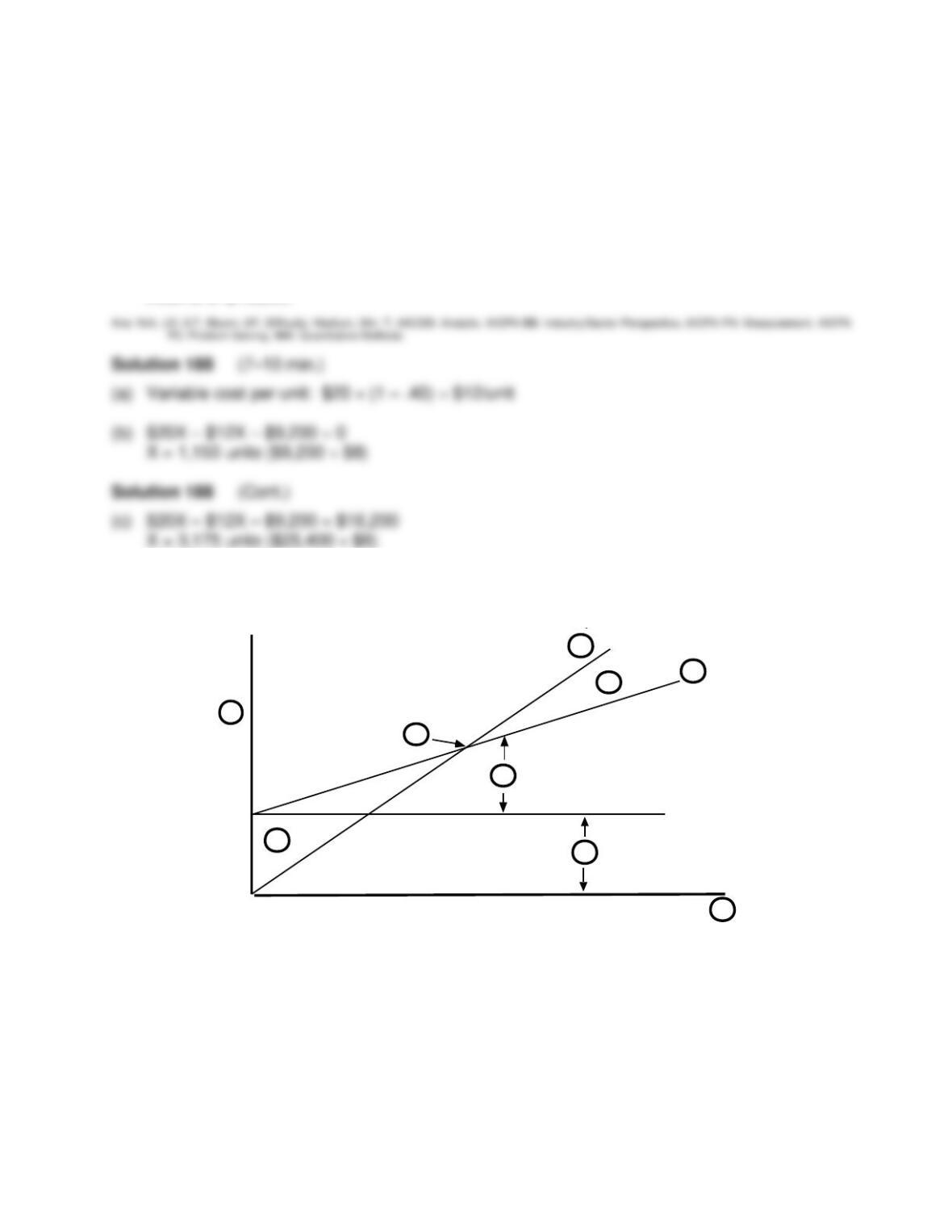

Corris Co. accumulates the following data concerning a mixed cost, using miles as the activity

level. Miles Driven Total Cost

January 10,000 $17,000

February 8,000 13,500

March 9,000 14,400

April 7,000 12,500

Instructions

Compute the variable and fixed cost elements using the high-low method.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 40

Ex. 171

Moresan Co. gathered the following information on power costs and factory machine usage for

the last six months:

Month Power Cost Factory Machine Hours

January $24,400 13,900

February 29,200 17,600

March 29,000 16,800

April 22,340 13,200

May 19,900 11,600

June 14,900 6,600

Instructions

Using the high-low method of analyzing costs, answer the following questions and show

computations to support your answers.

(a) What is the estimated variable portion of power costs per factory machine hour?

(b) What is the estimated fixed power cost each month?

(c) If it is estimated that 10,000 factory machine hours will be run in July, what is the expected

total power cost for July?

Cost-Volume-Profit

18 – 41

Ex. 172

The Bradshaw Law Office has the following monthly telephone records and costs:

Calls Costs

2,000 $2,400

1,500 2,000

2,200 2,600

2,500 2,800

2,300 2,700

1,700 2,200

Instructions

Identify the fixed and variable cost elements using the high-low method.

Ex. 173

Determine the missing amounts.

Contribution Contribution

Unit Selling Price Unit Variable Costs Margin Per Unit Margin Ratio

1. $300 $180 A B

2. $600 C $210 D

3. E F $300 30%

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 42

Ex. 174

Henderson Farms reports the following results for the month of November:

Sales (10,000 units) $600,000

Variable costs 420,000

Contribution margin 180,000

Fixed costs 110,000

Net income $ 70,000

Management is considering the following independent courses of action to increase net income.

1. Increase selling price by 5% with no change in total variable costs.

2. Reduce variable costs to 66

23

% of sales.

3. Reduce fixed costs by $10,000.

Instructions

If maximizing net income is the objective, which is the best course of action?

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 43

Ex. 175

Marvin Co. had a net loss of $150,000 in 2012 when the selling price per unit was $20, the

variable costs per unit were $14, and the fixed costs were $600,000. Management expects per

unit data and total fixed costs to be the same in 2013. Management has set a goal of earning net

income of $150,000 in 2013.

Instructions

(a) Compute the units sold in 2012.

(b) Compute the number of units that would have to be sold in 2013 to reach management’s

desired net income level.

(c) Assume that Marvin Co. sells the same number of units in 2013 as it did in 2012. What would

the selling price have to be in order to reach the target net income? Use the mathematical

equation.

Ex. 176

In the month of September, Matlock Industries sold 800 units of product. The average sales price

was $30. During the month, fixed costs were $6,300 and variable costs were 70% of sales.

Instructions

(a) Determine the contribution margin in dollars, per unit, and as a ratio.

(b) Using the contribution margin technique, compute the break-even point in dollars and in

units.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 44

Ex. 177

In 2012, Stallman Co. had a break-even point of $800,000 based on a selling price of $10 per unit

and fixed costs of $240,000. In 2013, the selling price and variable costs per unit did not change,

but the break-even point increased to $850,000.

Instructions

(a) Compute the variable cost per unit and the contribution margin ratio for 2012.

(b) Using the contribution margin ratio, compute the increase in fixed costs for 2013.

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 45

Ex. 178

The income statement for Bradford Machine Company for 2012 appears below.

BRADFORD MACHINE COMPANY

Income Statement

For the Year Ended December 31, 2012

——————————————————————————————————————————

Sales (40,000 units) ……………………………………………………………………….. $1,000,000

Variable expenses …………………………………………………………………………. 700,000

Contribution margin ………………………………………………………………………… 300,000

Fixed expenses ……………………………………………………………………………… 360,000

Net income (loss) …………………………………………………………………………… $ (60,000)

Instructions

Answer the following independent questions and show computations using the contribution

margin technique to support your answers:

1. What was the company’s break-even point in sales dollars in 2012?

2. How many additional units would the company have had to sell in 2013 in order to earn net

income of $45,000?

3. If the company is able to reduce variable costs by $2.50 per unit in 2013 and other costs and

unit revenues remain unchanged, how many units will the company have to sell in order to

earn a net income of $45,000?

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 46

Ex. 179

Webber, Inc. developed the following information for its product:

Per Unit

Sales price $90

Variable cost 63

Contribution margin $27

Total fixed costs $1,080,000

Instructions

Answer the following independent questions and show computations using the contribution

margin technique to support your answers.

1. How many units must be sold to break even?

2. What is the total sales that must be generated for the company to earn a profit of $60,000?

3. If the company is presently selling 45,000 units, but plans to spend an additional $108,000 on

an advertising program, how many additional units must the company sell to earn the same

net income it is now making?

4. Using the original data in the problem, compute a new break-even point in units if the unit

sales price is increased 20%, unit variable cost is increased by 10%, and total fixed costs are

increased by $210,000.

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 47

Ex. 180

Werth & Garza Manufacturing’s sales slumped badly in 2013 due to so many people purchasing

gifts online. The company’s income statement showed the following results from selling 500,000

units of product: net sales $2,125,000; total costs and expenses $2,500,000; and net loss

$375,000. Costs and expenses consisted of the following:

Total Variable Fixed

Cost of goods sold $2,000,000 $1,300,000 $700,000

Selling expenses 200,000 50,000 150,000

Administrative expenses 300,000 150,000 150,000

$2,500,000 $1,500,000 $1,000,000

Management is considering the following alternative for 2013:

Purchase new automated equipment that will change the proportion between variable and

fixed expenses sold to 45% variable and 55% fixed.

Instructions

(a) Compute the break-even point in dollars for 2013.

(b) Compute the break-even point in dollars under the alternative course of action.

Ex. 181

Henning Co. estimates that variable costs will be 60% of sales and fixed costs will total

$2,160,000. The selling price of the product is $10, and 600,000 units will be sold.

Instructions

Using the mathematical equation,

(a) Compute the break-even point in units and dollars.

(b) Compute the margin of safety in dollars and as a ratio.

(c) Compute net income.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 48

Ex. 182

Norton, Inc. has the following information available for September 2013.

Unit selling price of video game consoles $ 400

Unit variable costs $ 280

Total fixed costs $48,000

Units sold 500

Instructions

(a) Prepare a CVP income statement that shows both total and per unit amounts.

(b) Compute Norton’s breakeven in units.

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 49

Ex. 183

In the month of April, Avante Salon gave 2,500 haircuts, shampoos, and permanents at an

average price of $40. During the month, fixed costs were $21,000 and variable costs were 70% of

sales.

Instructions

(a) Determine the contribution margin in dollars, per unit, and as a ratio.

(b) Using the contribution margin technique, compute the break-even point in dollars and in

units.

(c) Compute the margin of safety dollars and as a ratio.

Ex. 184

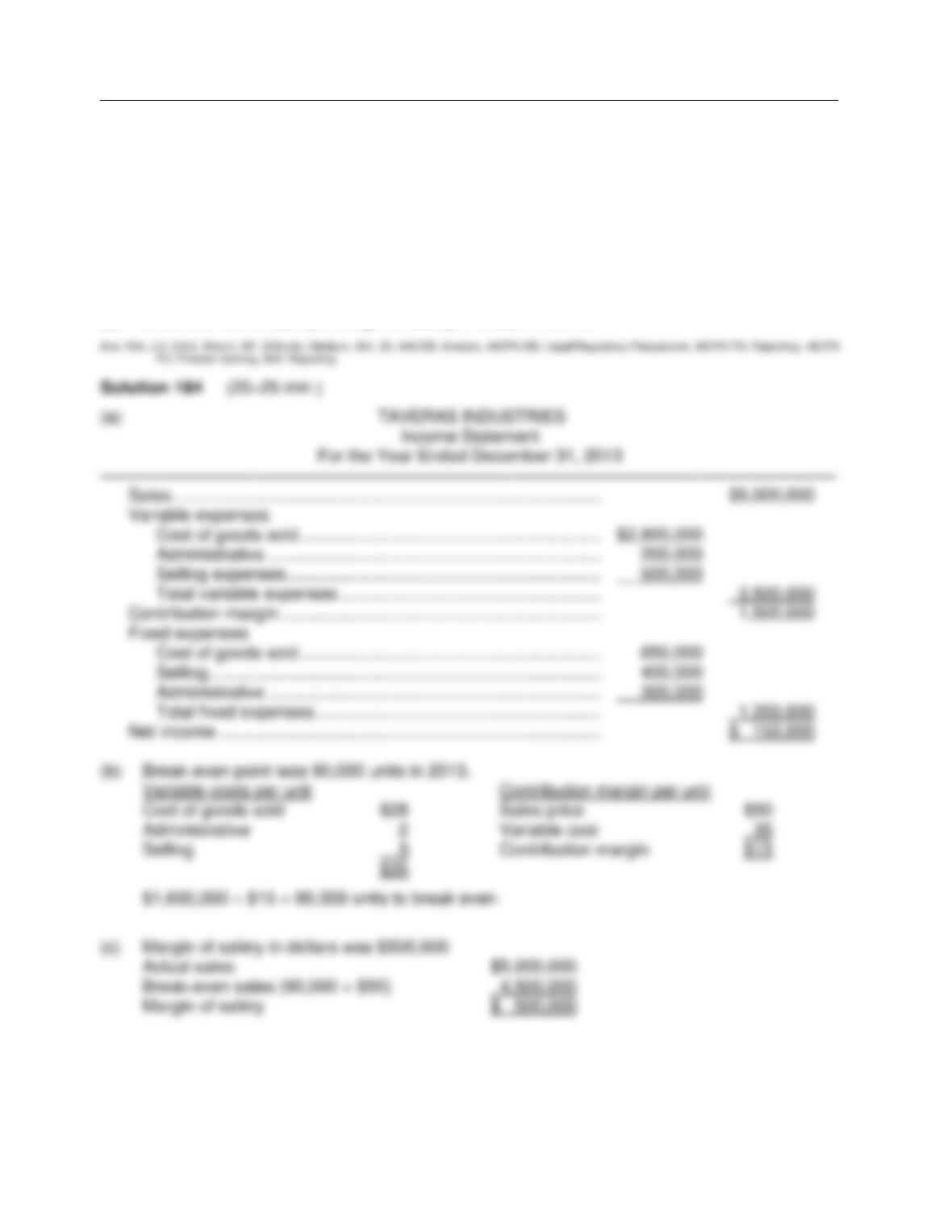

Taveras Industries developed the following information for the product it sells:

Sales price $50 per unit

Variable cost of goods sold $28 per unit

Fixed cost of goods sold $650,000

Variable selling expense 10% of sales price

Variable administrative expense $2.00 per unit

Fixed selling expense $400,000

Fixed administrative expense $300,000

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 50

Ex. 184 (cont.)

For the year ended December 31, 2013, Taveras produced and sold 100,000 units of product.

Instructions

(a) Prepare a CVP income statement using the contribution margin format for Taveras

Industries for 2013.

(b) What was the company’s break-even point in units in 2013? Use the contribution margin

technique.

(c) What was the company’s margin of safety in dollars in 2013?

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 51

Ex. 185

Gordon Manufacturing earned net income of $100,000 during 2012. The company wants to earn

net income of $40,000 more during 2013. The company’s fixed costs are expected to be

$126,000, and variable costs are expected to be 30% of sales.

Instructions

(a) Determine the required sales to meet the target net income during 2013.

(b) Fill in the dollar amounts for the summary income statement for 2013 below, based on your

answer to part (a).

Sales revenue

$

Variable costs

Contribution margin

Fixed costs

Net income

$

Ex. 186

Ferris, Inc. has a unit selling price of $500, variable cost per unit of $300, and fixed costs of

$260,000.

Instructions

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 52

Ex. 187

Erickson, Inc. makes student book bags that sell for $20 each. For the coming year, management

expects fixed costs to be $225,000. Variable costs are $15 per unit.

Instructions

(a) Compute break-even sales in dollars using the mathematical equation.

(b) Compute break-even sales using the contribution margin ratio.

(c) Compute margin of safety ratio assuming actual sales are $1,200,000.

(d) Compute the sales required to earn net income of $150,000, using the mathematical

equation.

Cost-Volume-Profit

FOR INSTRUCTOR USE ONLY

18 – 53

Ex. 188

Melody Manufacturing produces a hip-hop CD that is sold for $20. The contribution margin ratio is

40%. Fixed expenses total $9,200.

Instructions

(a) Compute the variable cost per unit.

(b) Compute how many CDs Melody Manufacturing will have to sell in order to break even.

(c) Compute how many CDs Melody Manufacturing will have to sell in order to make a target net

income of $16,200.

Ex. 189

Usher, Inc. has prepared the following cost-volume-profit graph:

Instructions

For the items listed below, enter to the left of the item, the letter in the graph which best

corresponds to the item.

____ 1. Activity base

____ 2. Break-even point

____ 3. Dollars

____ 4. Fixed costs

____ 5. Loss

I

BH

D

G

EA

F

C

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

18 – 54

Ex. 189 (cont.)

____ 6. Profit

____ 7. Revenues

____ 8. Total costs

____ 9. Variable costs

Ex. 190

Holder Manufacturing had $125,000 of net income in 2012 when the selling price per unit was

$100, the variable costs per unit were $70, and the fixed costs were $475,000. Management

expects per unit data and total fixed costs to remain the same in 2013. The president of Holder

Manufacturing is under pressure from stockholders to increase net income by $60,000 in 2013.

Instructions

(a) Compute the number of units sold in 2012.

(b) Compute the number of units that would have to be sold in 2013 to reach the stockholders‘

desired profit level.

(c) Assume that Holder Manufacturing sells the same number of units in 2013 as it did in 2012.

What would the selling price have to be in order to reach the stockholders’ desired profit

level.

Cost-Volume-Profit

18 – 55

Ex. 191

Englehart, Inc. reports the following operating results for the month of August: Sales $400,000

(units 5,000); variable costs $280,000; and fixed costs $95,000. Management is considering the

following independent courses of action to increase net income.

1. Increase selling price by 10% with no change in total variable costs.

2. Reduce variable costs to 65% of sales.

3. Reduce fixed costs by $15,000.

Instructions

Compute the net income to be earned under each alternative. Which course of action will produce

the highest net income?

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

18 – 56

Ex. 192

Kreter, Inc. earned net income of $300,000 last year. This year it wants to earn net income of

$450,000. The company’s fixed costs are expected to be $300,000, and variable costs are

expected to be 70% of sales.

Instructions

(a) Determine the required sales to meet the target net income of $450,000 using the

mathematical equation.

(b) Using a CVP income statement format, prove your answer.

Ex. 193