156. The cost of materials transferred into the Bottling Department of Mountain Springs Water Company is

$32,400, with $26,000 from the Purifying Department, plus additional $6,400 from the materials storeroom.

The conversion cost for the period in the Bottling Department is $8,750 ($3,750 factory applied and $5,000

direct labor.) The total costs transferred to finished goods for the period was $31,980. The Bottling Department

had a beginning inventory of $1,860.

a.

Journalize (1) the cost of transferred-in materials (2) conversion costs, and (3) the cost of transferred out to finished goods.

b.

Determine the balance of Work in Process-Bottling at the end of the period.

157. The cost of energy consumed in producing good units in the Bottling Department of Mountain Springs

Water Company was $36,850 and $39,060 for June and July, respectively. The number of equivalent units

produced in June and July was 55,000 and 62,000 liters respectively. Evaluate the change in the cost of energy

between the two months.

Work in Process-Bottling

32,400

Work in Process-Purifying

26,000

Materials

6,400

Work in Process-Bottling

8,750

Factory Overhead-Bottling

3,750

Wages Payable

5,000

Finished Goods

31,980

Work in Process-Bottling

31,980

$11,030 ($1,860 + $32,400 + 8,750 – $31,980)

158. Amos Company’s molding department opened on October 1, 2012. During October, 35,000 units were

completed and transferred out to the next department. On October 31, 2012, the 9,000 units which remained in

inventory were 40% complete with respect to conversion costs and 100% complete with respect to materials.

Required:

How many equivalent units of work did the molding department complete during October for materials and

conversion costs?

159. Kamin Company’s mixing department had a beginning inventory of 4,000 units which had accumulated

conversion costs of $55,000. During the period, the mixing department accumulated conversion costs of

$92,000 and started 8,000 new units. Ending inventory was 2,500 units which were 40% complete with respect

to conversion costs. Kamin uses the average cost method to cost inventories.

Required:

Calculate the cost per equivalent unit for conversion costs in the mixing department.

160. Kramer Company started its production operations on August 1. During August, the printing department

completed 17,600 units. There were 4,400 units in ending inventory which were 80% complete with respect to

materials and 10% complete with respect to conversion costs. During August, the department accumulated

materials costs of $45,408 and conversion costs of $76,670.

Required:

a. Calculate the cost of the goods transferred out.

b. What is the value of the ending inventory?

Round intermediate computation to nearest cent.

161. On March 1, Upton Company’s packaging department had Work in Process inventory of

8,820 units, which had been transferred in from the finishing department. These units had accumulated costs of

$315,000 in previous departments and $16,000 for conversion costs in the packaging department.

During March, 30,000 units were transferred into the department. These units had

accumulated costs of $770,000 in the previous departments. The packaging department incurred $54,000 in

conversion costs during the month.

Seven hundred units remained in ending inventory on March 31. These units were 80% complete with respect

to conversion costs.

Required:

Calculate the cost per equivalent unit for transferred-in costs and for conversion costs for the packaging

department using the average cost method.

162. Match the following terms with their definitions.

1. Measures the quantity of output of production

2. Provides information for controlling and

cost of production

3. The portion of whole units that are complete with

just-in-time

4. Work centers for processing in a just in time

equivalent units of

5. Focuses on reducing time, cost, and poor quality

163. Match the correct term with the statement that describes it.

3. Costing system used by a company producing

direct labor and

4. Summary of the activity in a processing department

cost of production

5. Costing system used by a company producing by a

6. Costs incurred in a previous process that are carried

forward as part of the product’s cost when it moves to

direct labor and

7. A process costing method that costs each period’s

equivalent units of work with that period’s costs per

8. Measure of the work done during a production

period, expressed in terms of fully complete units of

164. The inventory at June 1 and costs charged to Work in Process – Department 60 during June are as follows:

3,800 units, 60% completed

$ 60,400

Direct materials, 32,000 units

378,000

Direct labor

274,000

Factory overhead

168,000

Total cost to be accounted for

$880,400

During June, 32,000 units were placed into production and 31,200 units were completed, including those in inventory on June 1. On June 30, the

inventory of work in process consisted of 4,600 units which were 85% completed. Inventories are costed by the first-in, first-out method and all

materials are added at the beginning of the process.

Determine the following, presenting your computations (Prepare your computations using unit cost data to four decimal places, i.e. $4.4444, to

minimize rounding differences):

(a)

equivalent units of production for conversion cost

(b)

conversion cost per equivalent unit

(c)

total and unit cost of finished goods started in prior period and completed in the current period

(d)

total and unit cost of finished goods started and completed in the current period

(e)

total cost of work in process inventory at June 30

(a)

Equivalent units of production:

To process units in inventory on June 1:

3,800 ´ 40%

1,520

To process units started and completed in June:

31,200 – 3,800

27,400

To process units in inventory on June 30:

4,600 ´ 85%

3,910

Equivalent units of production for conversion cost

32,830

(b)

Conversion cost per equivalent unit of production:

Direct labor

$274,000

Factory overhead

168,000

$442,000

Unit conversion cost, $442,000 32,830

(c)

Cost of finished goods started in the prior period and completed in current period:

Work in process inventory on June 1:

3,800 ´ 60%

$60,400

Conversion costs in current period,

3,800 ´ 40% = 1,520 units at $13.4633

20,464

Total cost

$80,864

Beginning inventory,

Unit cost, $80,864 3,800

(d)

Cost of finished goods started and completed in current period:

Direct materials, 27,400 units at $11.8125

$323,663

Conversion costs, 27,400 units at $13.4633

368,894

Total cost

$692,557

Unit cost, $692,557 27,400

(e)

Cost of work in process inventory at June 30:

Direct materials, 4,600 units at $11.8125

$ 54,338

Conversion costs, 3,910 units at $13.4633

52,642

Total cost accounted for, $80,864 + $692,557 + $106,980

$880,401*

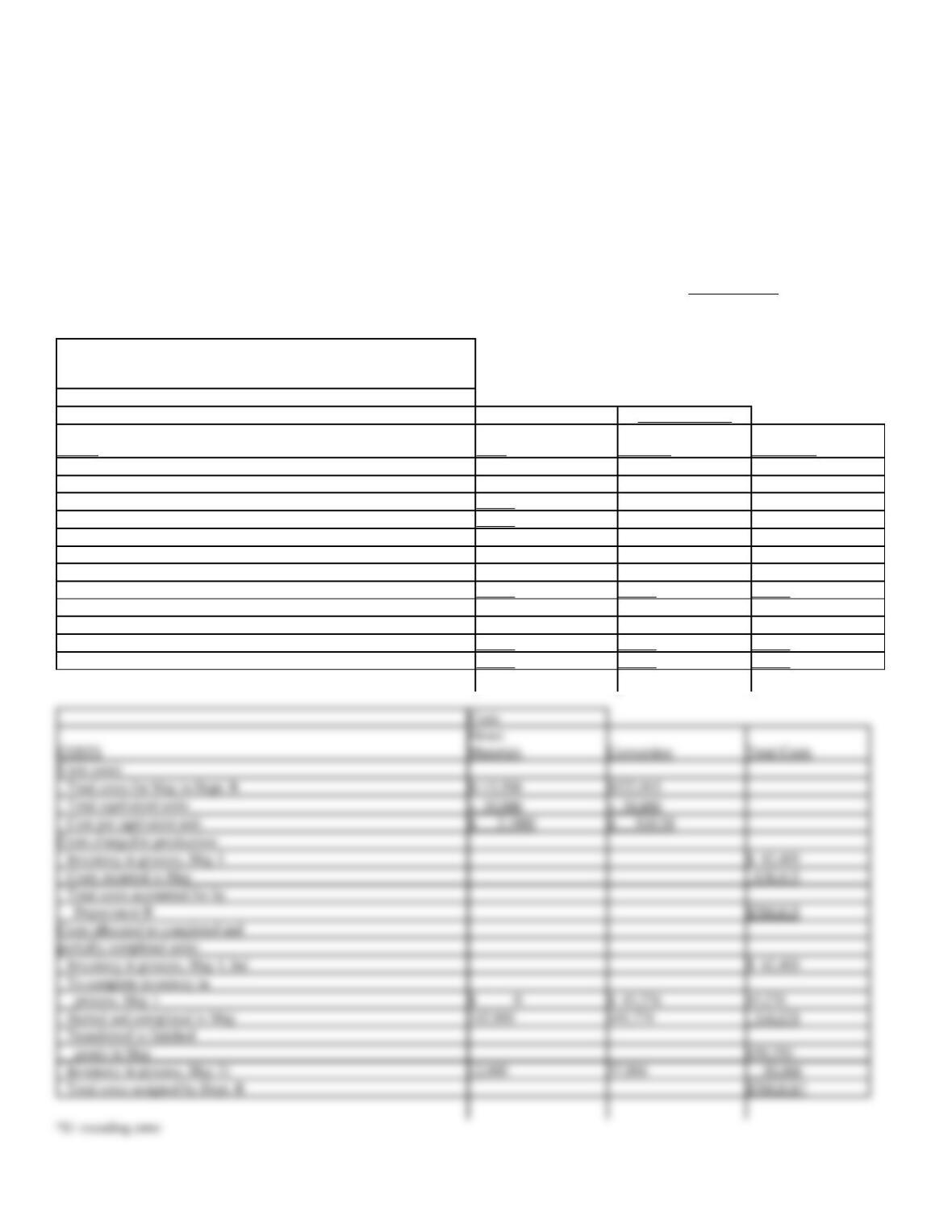

165. The inventory at May 1 and the costs charged to Work in Process—Department B during May for Stella

Company are as follows:

Beginning WIP, 12,000 units, 60% completed

$ 62,400

From Department A, 55,000 units started this period

Direct materials added

115,500

Direct labor incurred

384,915

Factory overhead incurred

138,000

During May, all direct materials are transferred from Department A, the units in process at May 1 were completed, and of the 55,000 units entering

the department, all were completed except 6,000 units which were 70% completed. Inventories are costed by the first-in, first-out method.

Prepare a cost of production report for May. Round unit cost data to four decimal places and total cost to nearest cent.

Stella Company

Cost of Production Report—Department B

For the Month Ended May 31, 20—

Equivalent Units

UNITS

Whole

Units

Direct

Materials

Conversion

Units charged to production:

Inventory in process, May 1

12,000

Received from Department A

55,000

Total units accounted for by Dept. B

67,000

Units to be assigned costs:

Inventory in process, May 1

(60% completed)

12,000

0

4,800

Started and completed in May

49,000

49,000

49,000

Transferred to finished goods in May

61,000

49,000

53,800

Inventory in process, May 31

(70% complete)

6,000

6,000

4,200

Total units to be assigned costs

67,000

55,000

58,000

Costs

Direct

Units costs:

Total costs for May in Dept. B

$115,500

$522,915

Cost per equivalent unit

$ 2.1000

$ 9.0158

Costs charged to production:

Inventory in process, May 1

$ 62,400

Costs incurred in May

638,415

Total costs accounted for by

Department B

$700,815

Costs allocated to completed and

partially completed units:

Inventory in process, May 1, bal

$ 62,400

To complete inventory in

process, May 1

$ 0

$ 43,276

43,276

Started and completed in May

102,900

441,774

544,674

Transferred to finished

goods in May

650,350

Total costs assigned by Dept. B

$700,816*

166. Zither Co. manufactures a product called Zens in a three-process series. All materials are introduced at the

beginning of the first process. Zither uses the first-in, first-out method of inventory costing. Unit and cost data

for the first process (Department A) for the month of October 2012 follow:

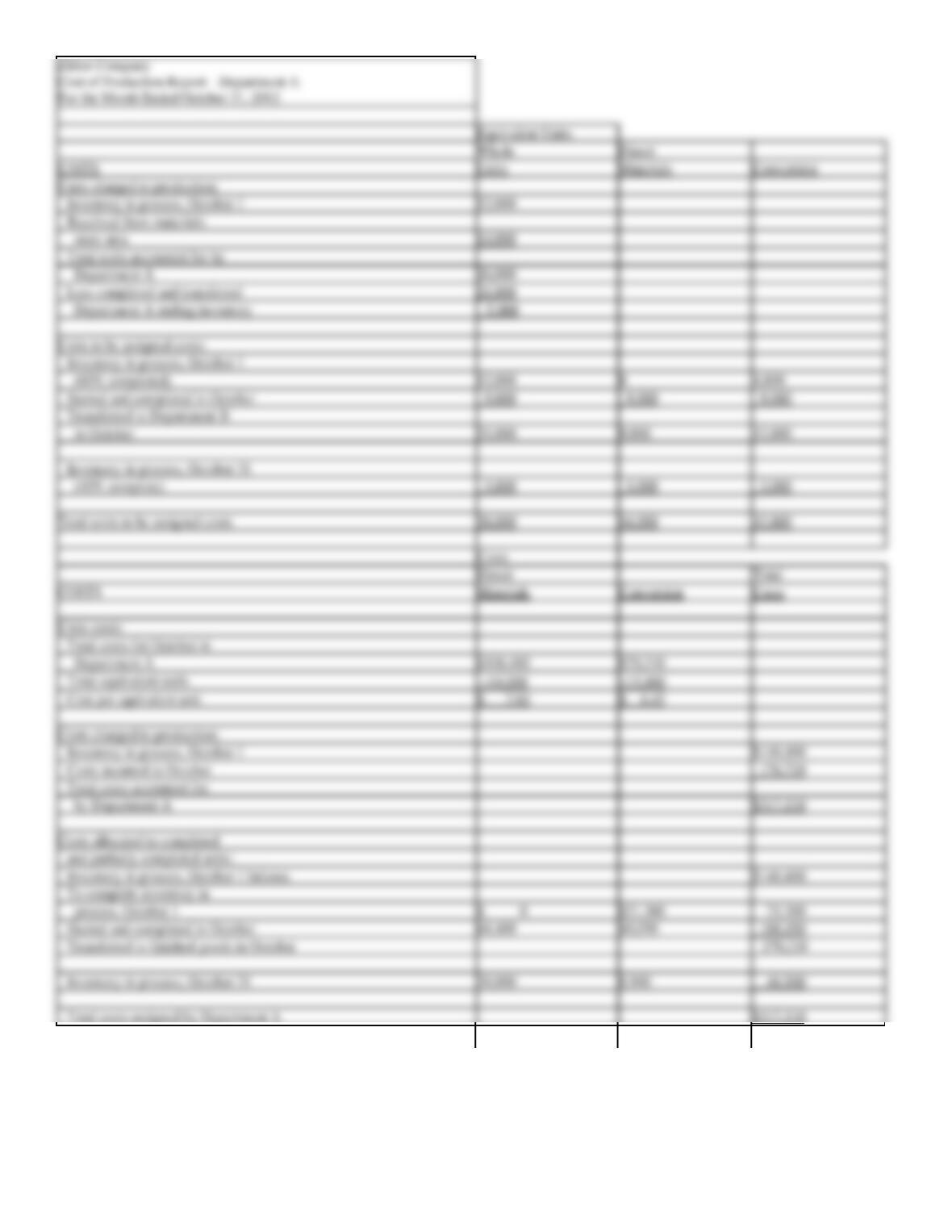

167. The inventory at April 1, 2012, and the costs charged to Work in Process—Department B during April for

Zarley Company are as follows:

1,200 units, 40% completed

$ 47,800

From Department A, 26,000 units

845,000

Direct labor

312,000

Factory overhead

176,770

During April, all direct materials are transferred from Department A, the units in process at April 1 were completed, and of the 26,000 units entering

the department, all were completed except 1,000 units which were 70% completed as to conversion costs. Inventories are costed by the first-in, first-

out method.

Equivalent Units

Units charged to production:

Inventory in process, April 1

1,200

Received from Department A

26,000

Total units accounted for by Dept. B

27,200

Units to be assigned costs:

Inventory in process, April 1

(40% completed)

1,200

0

Started and completed in April

25,000

25,000

25,000

Transferred to finished goods in April

26,200

25,000

25,720

Inventory in process, April 30

(70% complete)

1,000

1,000

700

Total units to be assigned costs

27,200

26,000

26,420

Costs

Units costs:

Total costs for April in Dept. B

$845,000

$488,770

Cost per equivalent unit

$ 32.50

$ 18.50

Costs charged to production:

Inventory in process, April 1

$ 47,800

Costs incurred in April

1,333,770

Total costs accounted for by

Department B

$1,381,570

Costs allocated to completed and

partially completed units:

Inventory in process, April 1, bal.

$ 47,800

To complete inventory in

process, April 1

$ 0

$ 13,320

13,320

Started and completed in April

812,500

462,500

1,275,000

Transferred to finished

168. The inventory at April 1, 2012, and the costs charged to Work in Process—Department B during April for

Hawk Company are as follows:

500 units, 60% completed

$ 3,460

From Department A, 10,000 units

36,300

Direct labor

7,960

Factory overhead

12,500

During April, all direct materials are transferred from Department A, the units in process at April 1 were completed, and of the 10,000 units entering

the department, all were completed except 1,200 units which were 25% completed as to conversion costs. Inventories are costed by the first-in, first-

out method.

Equivalent Units

Units charged to production:

Inventory in process, April 1

Received from Department A

10,000

Total units accounted for by Dept. B

10,500

Units to be assigned costs:

Inventory in process, April 1

(60% completed)

0

Started and completed in April

8,800

8,800

8,800

Transferred to finished goods in April

9,300

8,800

9,000

Inventory in process, April 30

(25% complete)

1,200

1,200

300

Total units to be assigned costs

10,500

10,000

9,300

Costs

Units costs:

Total costs for April in Dept. B

$36,300

$20,460

Cost per equivalent unit

$ 3.63

$ 2.20

Costs charged to production:

Inventory in process, April 1

$ 3,460

Costs incurred in April

56,760

Total costs accounted for by

Department B

$60,220

Costs allocated to completed and

partially completed units:

Inventory in process, April 1, bal.

$ 3,460

To complete inventory in

process, April 1

$ 0

$ 440

Started and completed in April

31,944

19,360

51,304

Transferred to finished

169. Information for the Sandy Manufacturing Company for the month of July 2012 is as follows:

Beginning work in process:

Cost of Inventory at process, July 1

$5,010

Units – 800

Direct materials = 100% complete

Conversion costs = 70% complete

Units started in July = 14,000

Costs charged to Work in Process during July:

Ending work in process inventory:

Direct materials costs = $57,400

Units = 1,500

Direct labor costs = 20,049

Direct materials = 100% complete

Factory overhead costs = 30,073

Conversion costs = 30% complete

Prepare a cost of production report for the month of July, using the FIFO method.

Sandy Manufacturing Company

Cost of Production Report

For the Month Ended July 31, 2012

_______________________

Units

Material

Conversion

Equivalent

Equivalent

Units

Units

Units

Beginning work in process

-0-

(70% complete)

Units started & completed

12,500

12,500

12,500

(14,000 started – 1,500 ending)

Ending work in process

(30% complete)

1,500

1,500

450

14,800

14,000

13,190

Units costs;

Total cost for July

$ 57,400

$50,122*

Total Equivalent units (from above)

¸14,000

¸13,190

Costs per equivalent unit

$ 4.10

$ 3.80

$7.90

Costs charged to production:

Inventory in process, July 1

$ 5,010

Cost incurred in July

107,522

Total costs accounted for in July

$112,532