Monopolistic Competition 4061

143. Refer to Scenario 16-3. How much profit will Peter earn each day if he chooses the price and

quantity that maximize his profit?

a. $176

b. $208

c. $225

d. $352

144. Refer to Scenario 16-3. Which of the following statements best describes the long run

adjustment in this market?

a. One or more ice cream shops in Fairfield closes, increasing the demand for Peter’s ice

cream. Peter’s profits increase and he sustains positive profits in the long run.

b. One or more ice cream shops in Fairfield closes, increasing the demand for Peter’s ice

cream. Peter’s profits increase until he earns zero profit.

c. One or more new ice cream shops in Fairfield opens and competes with Peter for customers,

reducing the demand for Peter’s ice cream. Peter’s profits decline until he incurs losses and

exits the industry.

d. One or more new ice cream shops in Fairfield opens and competes with Peter for customers,

reducing the demand for Peter’s ice cream. Peter’s profits decline until he earns zero profit.

4062 Monopolistic Competition

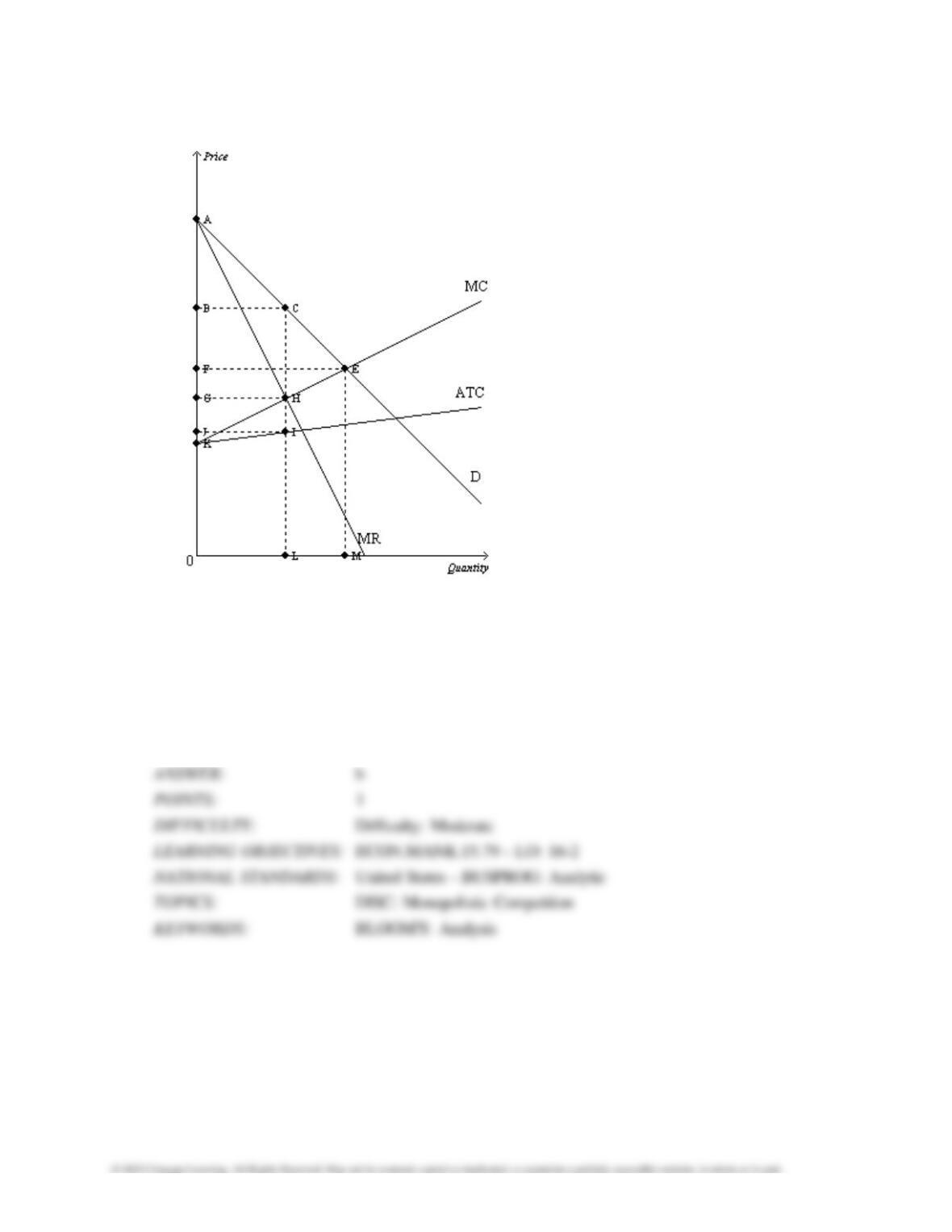

Figure 16–13

145. Refer to Figure 16-13. Which of the following areas represents the profit for this profit

maximizing monopolistically competitive firm?

a. BCHG

b. BCIJ

c. GHIJ

d. 0BCL

Monopolistic Competition 4063

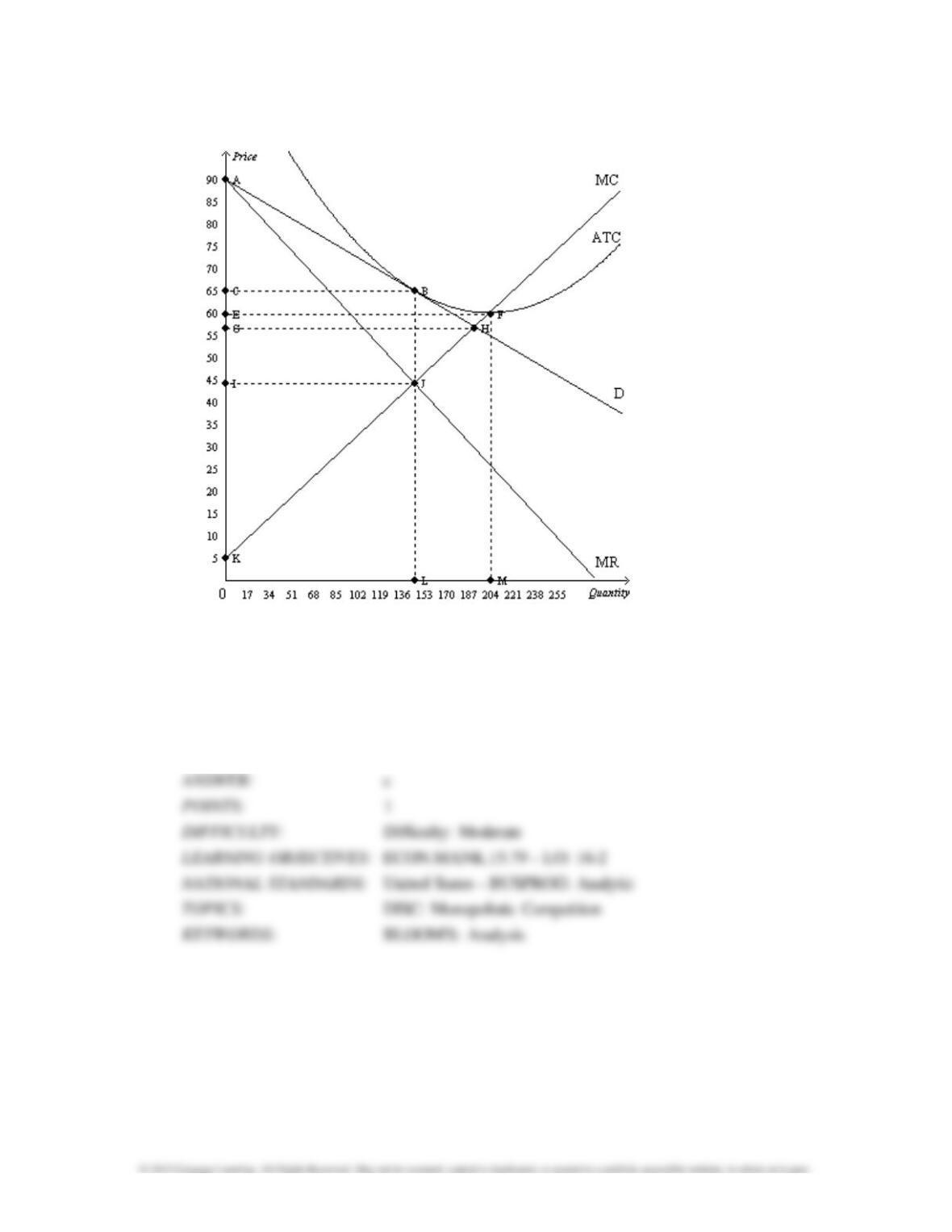

Figure 16-14

146. Refer to Figure 16-14. Which of the following represents the excess capacity of this firm?

a. BJ

b. GH

c. LM

d. There is no excess capacity.

4064 Monopolistic Competition

147. Refer to Figure 16–14. Which of the following best describes the profit-maximizing outcome

for the firm depicted here?

a. This firm is earning a short run profit, but will earn zero profit in the long run.

b. This firm is incurring a short run loss, but will earn zero profit in the long run.

c. This firm is earning zero profit in the short run, but will earn a positive profit in the long run.

d. This firm is in long run equilibrium and will continue to earn zero profit.

148. Refer to Figure 16-14. If this firm were operating in a perfectly competitive market, it would

charge a price equal to point

a. I but in a monopolistically competitive market, the profit–maximizing price is C.

b. G but in a monopolistically competitive market, the profit-maximizing price is C.

c. C but in a monopolistically competitive market, the profit-maximizing price is G.

d. G but in a monopolistically competitive market, the profit-maximizing price is J.

Monopolistic Competition 4065

149. Refer to Figure 16–14. The deadweight loss from production for this firm is represented by

which of the following areas?

a. ABC

b. IJK

c. BHJ

d. BCIJ

150. Refer to Figure 16–14. The deadweight loss from production for this firm is represented by

which of the following areas?

a. ABC

b. IJK

c. BHJ

d. BCIJ

4066 Monopolistic Competition

151. In which of the following markets is economic profit driven to zero in the long run?

a. oligopoly

b. monopoly

c. monopolistic competition

d. cartels

152. Which of the following conditions is characteristic of a monopolistically competitive firm in long-

run equilibrium?

a. P > demand and P = MR

b. ATC > demand and MR = MC

c. P > MC and demand = ATC

d. P < ATC and demand > MR

Monopolistic Competition 4067

153. Which of the following conditions is characteristic of a monopolistically competitive firm in long-

run equilibrium?

a. P > MR and P = MC

b. ATC = demand and MR = MC

c. P < MC and demand = ATC

d. P > ATC and demand > MR

154. A monopolistically competitive firm

a. charges a price that is equal to marginal cost.

b. experiences a zero profit in the long run.

c. produces at the efficient scale in the long run.

d. All of the above are correct.

4068 Monopolistic Competition

155. In a monopolistically competitive market,

a. entry by new firms is impeded by barriers to entry; thus, the number of firms in the market is

never ideal.

b. entry by new firms is impeded by barriers to entry, but the number of firms in the market is

nevertheless always ideal.

c. free entry ensures that the number of firms in the market is ideal.

d. there may be too few or too many firms in the market, despite free entry.

156. In which of the following market structures does free entry and exit play an important role in the

long-run equilibrium outcome?

(i) perfect competition

(ii) monopolistic competition

(iii) monopoly

a. (i) only

b. (i) and (ii) only

c. (ii) and (iii) only

d. (i), (ii), and (iii)

Monopolistic Competition 4069

157. If firms in a monopolistically competitive market are earning positive profits, then

a. firms will likely be subject to regulation.

b. barriers to entry will be strengthened.

c. some firms will exit the market.

d. new firms will enter the market.

158. If firms in a monopolistically competitive market are earning economic profits, which of the

following scenarios would best describe the change existing firms would face as the market

adjusts to the long-run equilibrium?

a. an increase in demand for each firm

b. a decrease in demand for each firm

c. a downward shift in the marginal cost curve for each firm

d. an upward shift in the marginal cost curve for each firm

4070 Monopolistic Competition

159. If firms in a monopolistically competitive market are incurring economic losses, which of the

following statements describes the changes that occur as the market adjusts to the long-run

equilibrium?

a. Each existing firm’s demand curve shifts to the left.

b. More firms enter the market.

c. Each firm eliminates its excess capacity.

d. Both a and b are correct.

160. In monopolistically competitive markets, positive economic profits

a. suggest that some existing firms will exit the market.

b. suggest that new firms will enter the market.

c. are sustained through government-imposed barriers to entry.

d. are never possible.

Monopolistic Competition 4071

161. In monopolistically competitive markets, economic losses

a. suggest that some existing firms will exit the market.

b. suggest that new firms will enter the market.

c. are minimized through government-imposed barriers to entry.

d. are never possible.

162. As new firms enter a monopolistically competitive market, profits of existing firms

a. rise, and product diversity in the market increases.

b. rise, and product diversity in the market decreases.

c. decline, and product diversity in the market increases.

d. decline, and product diversity in the market decreases.

163. As firms exit a monopolistically competitive market, profits of remaining firms

a. decline, and product diversity in the market decreases.

b. decline, and product diversity in the market increases.

c. rise, and product diversity in the market decreases.

d. rise, and product diversity in the market increases.

4072 Monopolistic Competition

164. The free entry and exit of firms in a monopolistically competitive market guarantees that

a. both economic profits and economic losses can persist in the long run.

b. both economic profits and economic losses disappear in the long run.

c. economic profits, but not economic losses, can persist in the long run.

d. economic losses, but not economic profits, can persist in the long run.

165. In monopolistically competitive markets, free entry and exit suggests that

a. the market structure will eventually be characterized by perfect competition in the long run.

b. all firms earn zero economic profits in the long run.

c. some firms will be able to earn economic profits in the long run.

d. some firms will be forced to incur economic losses in the long run.

Monopolistic Competition 4073

166. When a profit–maximizing firm in a monopolistically competitive market is producing the long-run

equilibrium quantity,

a. its average revenue will equal its marginal cost.

b. its marginal revenue will exceed its marginal cost.

c. it will be earning positive economic profits.

d. its demand curve will be tangent to its average total cost curve.

167. When a firm’s demand curve is tangent to its average total cost curve, the

a. firm’s economic profit is zero.

b. firm must be earning economic profits.

c. firm must be incurring economic losses.

d. firm must be operating at its efficient scale.

4074 Monopolistic Competition

168. When a profit-maximizing firm in a monopolistically competitive market is in long–run equilibrium,

a. the demand curve will be perfectly elastic.

b. price exceeds marginal cost.

c. marginal cost must be falling.

d. marginal revenue exceeds marginal cost.

169. A profit-maximizing firm operating in a monopolistically competitive market that is in a long–run

equilibrium has

a. minimized average total cost.

b. chosen to produce where demand is unitary elastic.

c. produced the efficient scale of output.

d. chosen a quantity of output where average revenue equals average total cost.

Monopolistic Competition 4075

170. In a long–run equilibrium, a firm in a monopolistically competitive market operates

a. where marginal revenue is zero.

b. where marginal revenue is negative.

c. on the rising portion of its average total cost curve.

d. on the declining portion of its average total cost curve.

171. When a new firm enters a monopolistically competitive market, the individual demand curves

faced by all existing firms in that market will

a. shift to the left.

b. shift to the right.

c. shift in a direction that is unpredictable without further information.

d. remain unchanged. It is the supply curve that will shift.

4076 Monopolistic Competition

172. When a firm exits a monopolistically competitive market, the individual demand curves faced by

all remaining firms in that market will

a. shift in a direction that is unpredictable without further information.

b. shift to the right.

c. shift to the left.

d. remain unchanged. It is the supply curve that will shift.

173. Long-run profit earned by a monopolistically competitive firm is driven to the competitive level

due to a(n)

a. change in the technology that the firm utilizes.

b. shift of its demand curve.

c. shift of its supply curve.

d. increase in the firm’s average cost of production.

Monopolistic Competition 4077

174. Because a monopolistically competitive firm has some market power, in the long-run the price of

its product exceeds its

a. average revenue.

b. average total cost.

c. marginal cost.

d. None of the above is correct.

175. New firms will likely enter a monopolistically competitive market when price exceeds

a. marginal revenue.

b. average revenue.

c. marginal cost.

d. average total cost.

4078 Monopolistic Competition

176. Which two curves are tangent to each other in a monopolistically competitive market with zero

economic profit?

a. demand and average variable cost

b. demand and average total cost

c. marginal revenue and average variable cost

d. marginal revenue and average total cost

177. In a monopolistically competitive market,

a. strategic interactions among the firms are very important.

b. the threat of entry by new firms is not an important consideration.

c. the attainment of a Nash equilibrium is an important objective.

d. firms may enter even though they will earn zero economic profit in the long run.

Monopolistic Competition 4079

178. Among the following situations, which one is least likely to apply to a monopolistically

competitive firm?

a. profit is positive in the short run

b. total cost exceeds total revenue in the short run

c. profit is positive in the long run

d. total revenue equals total cost in the long run

179. Suppose that monopolistically competitive firms in a certain market are earning positive profits.

In the transition from this initial situation to a long–run equilibrium,

a. the number of firms in the market decreases.

b. each existing firm experiences a decrease in demand for its product.

c. each existing firm experiences a rightward shift of its marginal revenue curve.

d. each existing firm experiences an upward shift in its average total cost curve.

4080 Monopolistic Competition

180. Suppose that monopolistically competitive firms in a certain market are experiencing losses. In

the transition from this initial situation to a long-run equilibrium,

a. the number of firms in the market decreases.

b. each existing firm experiences a decrease in demand for its product.

c. each firm experiences an upward shift of its marginal cost and average total cost curves.

d. each existing firm’s average total cost falls to bring economic profit back to zero.

181. When a monopolistically competitive firm is in long–run equilibrium,

a. marginal revenue is equal to marginal cost.

b. average total cost is minimized.

c. marginal revenue is tangent to average total cost.

d. All of the above are correct.