Chapter 16—Monetary Policy

MULTIPLE CHOICE

1. Keynes called money people hold to make routine day-to-day purchases the:

a.

transactions demand for holding money.

c.

speculative demand for holding money.

b.

precautionary demand for holding money.

d.

store of value demand for holding money.

2. The stock of money people hold to pay everyday predictable expenses is the:

a.

transactions demand for holding money.

c.

speculative demand for holding money.

b.

precautionary demand for holding money.

d.

store of value demand for holding money.

3. The quantity of money demanded to satisfy transactions needs:

a.

is intended for unexpected expenditures.

b.

increases with the level of real GDP.

c.

decreases with the level of real GDP.

d.

is unrelated to either national income or the interest rate.

e.

varies inversely with the liquidity demand for money.

4. People learn to hold a specific quantity of money for the groceries, theater tickets, gasoline, clothes,

film, and other items they habitually purchase. This behavior is representative of the:

a.

precautionary demand.

b.

speculative demand.

c.

transactions demand.

d.

volatility demand.

e.

liquidity demand.

5. The transactions demand for holding money is when people hold money:

a.

instead of near money.

b.

to transact purchases they expect to make.

c.

as insurance against unexpected expenses.

d.

to speculate in the stock market.

e.

to take advantage of changes in interest rates.

6. When people hold money to transact purchases they expect to make, this is known as the:

a.

precautionary demand for money.

b.

liquidity demand for money.

c.

spending demand for money.

d.

speculative demand for money.

e.

transactions demand for money.

7. The transactions demand for money is the demand for money by households for:

a.

rainy day spending.

c.

liquidity purposes.

b.

predictable spending purposes.

d.

investing purposes.

8. One reason that people hold money is to pay for unexpected car repairs and other unpredictable

expenses. This motive for holding money is called:

a.

transactions demand.

c.

speculative demand.

b.

precautionary demand.

d.

noncyclical demand.

9. Keynes called the money people hold in order to pay unforeseen or unexpected expenses the:

a.

transactions demand for holding money.

c.

speculative demand for holding money.

b.

precautionary demand for holding money.

d.

store of value demand for holding money.

10. The precautionary demand for money:

a.

varies inversely with the income level.

b.

varies inversely with the price level.

c.

is used as an insurance agent against unexpected needs.

d.

states that nominal income must exceed real income.

e.

is a classical concept in monetary theory.

11. If you hold money in anticipation of household emergency expense, this represents the::

a.

speculative demand for holding money.

b.

transactions demand for holding money.

c.

opportunity cost motive for holding money.

d.

precautionary demand for holding money.

e.

regressive cost of holding money.

12. The precautionary demand for holding money is when people hold money:

a.

instead of near money.

b.

to transact purchases they expect to make.

c.

as insurance against unexpected needs.

d.

to speculate in the stock market.

e.

to take advantage of changes in interest rates.

13. The demand for money that households keep for emergency purposes is known as the:

a.

precautionary demand.

b.

emergency demand.

c.

speculative demand.

d.

transactions demand.

e.

temporary demand.

14. The precautionary demand for money is the demand for money:

a.

for normal transactions purposes.

b.

for normal investment purposes.

c.

for special stock purchases.

d.

to protect against inflation.

e.

to cover unexpected events.

15. When a household takes extra (unbudgeted) money on a trip, economists would classify this money as

held for a(n):

a.

speculative demand.

b.

transactions demand.

c.

emergency motive.

d.

precautionary demand.

e.

inflationary motive.

16. Keynes called the money people hold in order to buy bonds, stocks, or other nonmoney financial assets

the:

a.

transactions demand for holding money.

b.

precautionary demand for holding money.

c.

speculative demand for holding money.

d.

unit of account demand for holding money.

17. The quantity of money held in response to interest rates is the:

a.

transactions motive for holding money.

c.

speculative motive for holding money.

b.

precautionary motive for holding money.

d.

unit-of-account motive for holding money.

18. The speculative demand for money is the stock of money that people hold to:

a.

pay their predictable, everyday expenses.

b.

pay for any unexpected expenses that may occur.

c.

buy stocks, bonds, and other financial assets.

d.

buy the foreign currencies needed to purchase imports.

19. Which type of demand for money causes the demand for money curve to slope downward?

a.

Speculative demand.

c.

Transactions demand.

b.

Precautionary demand.

d.

Foreign-exchange demand.

20. The stock of money people hold to take advantage of expected future changes in the price of bonds,

stocks, or other nonmoney financial assets is the:

a.

unit-of-account motive for holding money.

c.

speculative motive for holding money.

b.

precautionary motive for holding money.

d.

transactions motive for holding money.

21. Which of the following statements is true?

a.

The speculative demand for money at possible interest rates gives the demand for money

curve its upward slope.

b.

There is an inverse relationship between the quantity of money demanded and the interest

rate.

c.

According to the quantity theory of money, any change in the money supply will have no

effect on the price level.

d.

All of these are true.

22. The speculative demand curve for money is:

a.

downward sloping.

b.

upward sloping.

c.

vertical.

d.

horizontal.

e.

spiral.

23. The speculative demand for money:

a.

varies inversely with income.

b.

is only concerned with active money.

c.

involves holding money for unexpected problems.

d.

varies directly with the transactions demand for money.

e.

varies inversely with the interest rate.

24. Speculative demand for money is a(n):

a.

positive function of prices.

b.

inverse function of prices.

c.

positive function of interest rates.

d.

inverse function of interest rates.

e.

function of unexpected needs.

25. The speculative demand for holding money is when people hold money:

a.

instead of near money.

b.

to transact purchases they expect to make.

c.

as insurance against unexpected needs.

d.

to speculate in the stock market.

e.

to take advantage of changes in interest rates.

26. The money that households might hold either as money or in interest-bearing assets, depending on the

interest rate, is called the:

a.

precautionary demand.

b.

transactions demand.

c.

speculative demand.

d.

liquidity motive.

e.

investment motive.

27. The speculative demand for money shows the relationship between money demand and:

a.

income levels.

b.

interest rates.

c.

prices

d.

investment.

e.

consumption.

28. When interest rates rise, the quantity demanded of money held for the:

a.

speculative motive rises.

b.

precautionary motive rises.

c.

transactions motive falls.

d.

precautionary motive falls.

e.

speculative motive falls.

29. The downward slope of the demand for money curve is created by the:

a.

transactions demand for money.

c.

speculative demand for money.

b.

precautionary demand for money.

d.

all of these.

30. The demand curve for money:

a.

shows the amount of money balances that individuals and businesses wish to hold at

various levels of private investment.

b.

reflects the open market operations policy of the Federal Reserve.

c.

shows the amount of money that households and businesses wish to hold at various rates

of interest.

d.

indicates the amount that consumers wish to borrow at a given interest rate.

31. The opportunity cost of holding money balances increases when:

a.

the inflation rate decreases.

c.

the interest rate decreases.

b.

the interest rate increases.

d.

GDP is far from full employment.

32. Other things being equal, the quantity of money that people wish to hold in currency and their

checking accounts can be expected to:

a.

increase as the interest rate increases.

c.

decrease as real GDP increases.

b.

decrease as the interest rate increases.

d.

none of these.

33. In a two-asset economy with money and T-bills, the quantity of money that people will want to hold,

other things being equal, can be expected to:

a.

increase as the real GDP interest rate increases.

b.

decrease as the real GDP interest rate increases.

c.

decrease as real GDP increases.

d.

none of these.

34. Keynes argued that the downward slope of the demand for money curve depends on the:

a.

equation of exchange.

c.

federal funds rate.

b.

rate of interest.

d.

discount rate.

35. A graph illustrating the relationship between the quantity of money demanded and the interest rate

would have a slope that is:

a.

positive.

c.

horizontal.

b.

negative.

d.

vertical.

36. Other things being equal, an increase in the rate of interest causes a(n):

a.

upward movement along the demand for money curve.

b.

downward movement along the demand for money curve.

c.

rightward shift of the demand for money curve.

d.

leftward shift of the demand for money curve.

37. In a two-asset economy with money and T-bills, the quantity of money that people will want to hold,

other things being equal, can be expected to:

a.

decrease as real GDP increases.

c.

increase as the interest rate increases.

b.

increase as the interest rate decreases.

d.

all of these.

38. A decrease in the interest rate, other things being equal, causes a(n):

a.

upward movement along the demand curve for money.

b.

downward movement along the demand curve for money.

c.

rightward shift of the demand curve for money.

d.

leftward shift of the demand curve for money.

39. The demand for money curve shows that there is an inverse relationship between the quantity of

money demanded and the:

a.

quantity of money supplied.

c.

price level.

b.

gross domestic product (GDP).

d.

interest rate.

40. Which of the following statements is true?

a.

The speculative demand for money at possible interest rates gives the demand for money

curve its upward slope.

b.

There is an inverse relationship between the quantity of money demanded and the interest

rate.

c.

According to the quantity theory of money, any change in the money supply will have no

effect on the price level.

d.

All of these.

41. Keynesians identify three principal motives for demanding money. They are the:

a.

transactions demand, precautionary demand, and liquidity motive.

b.

transactions demand, precautionary demand, and convertibility motive.

c.

transactions demand, speculative demand, and volatility motive.

d.

transactions demand, speculative demand, and liquidity motive.

e.

transactions demand, speculative demand, and precautionary demand.

42. As the interest rate decreases, the quantity of money people will hold:

a.

decreases.

b.

increases.

c.

stays the same.

d.

rises and then falls.

e.

falls and then rises.

43. When the interest rate falls,

a.

the opportunity cost of holding money rises.

b.

people shift out of holding interest-yielding bonds into holding money.

c.

the quantity of money people will hold decreases.

d.

investment spending decreases.

e.

real GDP will decrease.

44. People react to an excess supply of money by:

a.

selling bonds, thus driving up the interest rate.

b.

selling bonds, thus driving down the interest rate.

c.

buying bonds, thus driving up the interest rate.

d.

buying bonds, thus driving down the interest rate.

45. In Keynes’s view, an excess quantity of money demanded causes people to:

a.

sell bonds and the interest rate rises.

c.

buy bonds and the interest rate rises.

b.

buy bonds and the interest rate falls.

d.

increase speculative balances.

46. In Keynes’s view, an excess quantity of money supplied causes people to:

a.

sell bonds and the interest rate rises.

c.

buy bonds and the interest rate rises.

b.

buy bonds and the interest rate falls.

d.

increase speculative balances.

47. If people attempt to sell bonds because of excess money demand, then the interest rate will:

a.

rise.

c.

remain unchanged

b.

fall.

d.

react unpredictably.

48. Which of the following falls when bond prices rise?

a.

Stock prices.

c.

Money demand.

b.

Interest rates.

d.

Money supply.

49. Assume the Fed decreases the money supply and the demand for money curve is fixed. In response,

people will:

a.

sell bonds, thus driving up the interest rate.

b.

buy bonds, thus driving down the interest rate.

c.

buy bonds, thus driving up the interest rate.

d.

sell bonds, thus driving down the interest rate.

50. Assume a fixed demand for money curve and the Fed increases the money supply. In response, people

will:

a.

sell bonds, thus driving up the interest rate.

b.

sell bonds, thus driving down the interest rate.

c.

buy bonds, thus driving up the interest rate.

d.

buy bonds, thus driving down the interest rate.

51. Assume a fixed demand for money curve and the Fed decreases the money supply. In response, people

will:

a.

sell bonds, thus driving up the interest rate.

b.

sell bonds, thus driving down the interest rate.

c.

buy bonds, thus driving up the interest rate.

d.

buy bonds, thus driving down the interest rate.

52. Assume a fixed demand for money curve and the Fed increases the money supply. The result is a

temporary:

a.

excess quantity of money demanded.

c.

new equilibrium interest rate.

b.

excess quantity of money supplied.

d.

decrease in the demand for loans.

53. If the Fed wants to raise interest rates, then it can use its open market operations to:

a.

increase the money supply.

c.

increase money demand.

b.

decrease the money supply.

d.

decrease money demand.

54. Which of the following policies could the Fed use to lower the interest rate?

a.

A tax cut.

c.

Raising the discount rate.

b.

Selling government securities.

d.

Reducing the required reserve ratio.

55. An increase in the money supply is represented by a(n):

a.

rightward shift of the downward-sloping money supply curve.

b.

upward shift of the money supply curve.

c.

rightward shift of the money supply curve.

d.

increase in the rate of interest.

56. When the Fed increases the money supply, interest rates:

a.

rise.

b.

fall.

c.

are unaffected.

d.

rise and then fall.

e.

fall and then rise.

57. If the Federal Reserve increases the money supply, ceteris paribus, the:

a.

rate of interest decreases.

c.

rate of interest is unaffected.

b.

rate of interest increases.

d.

Fed sells bonds.

58. When the Fed decreases the money supply, interest rates:

a.

rise.

b.

fall.

c.

are unaffected.

d.

rise and then fall.

e.

fall and then rise.

59. Assume the demand for money curve is stationary and the Fed increases the money supply. The result

is that people:

a.

increase the supply of bonds, thus driving up the interest rate.

b.

increase the supply of bonds, thus driving down the interest rate.

c.

increase the demand for bonds, thus driving up the interest rate.

d.

increase the demand for bonds, thus driving down the interest rate.

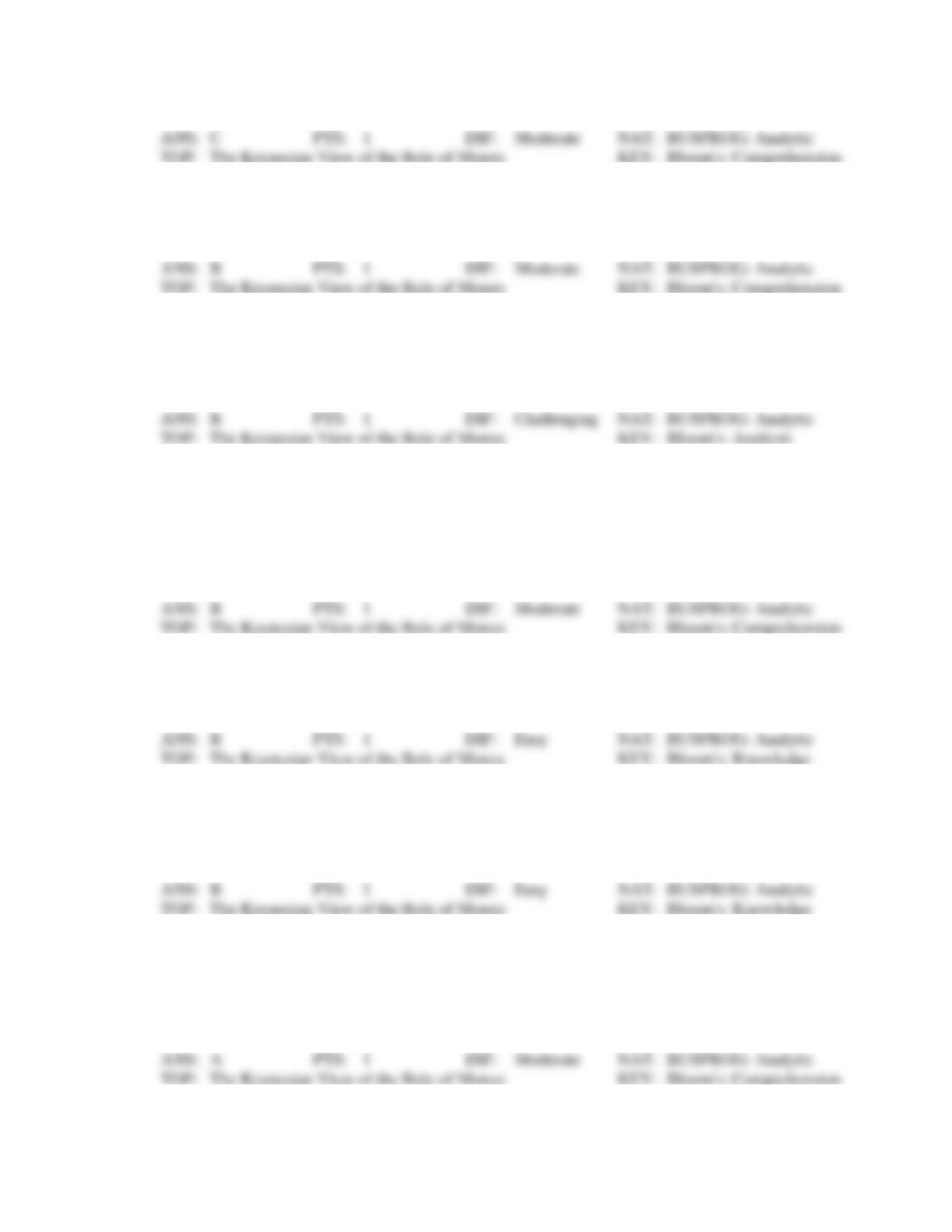

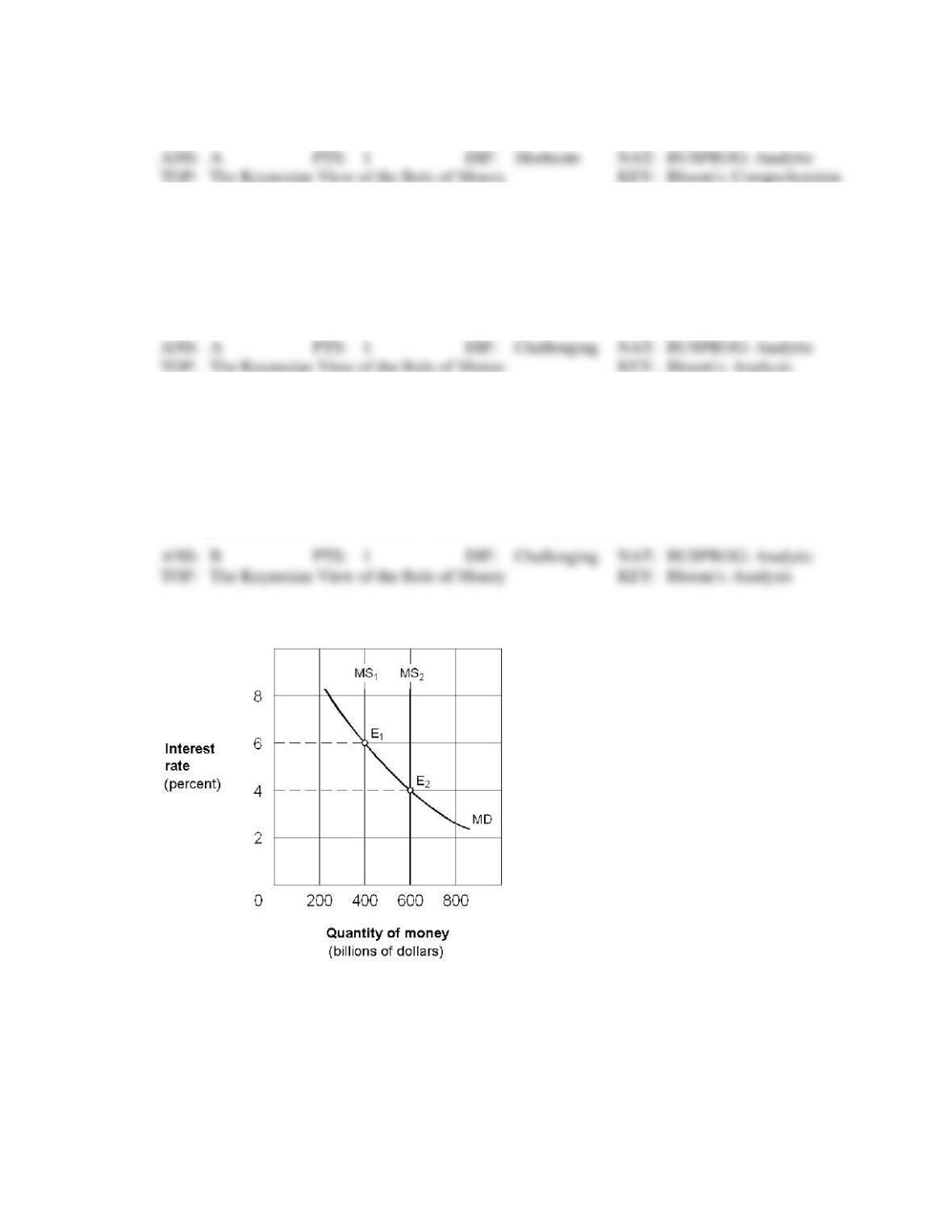

Exhibit 16-1 Money market demand and supply curves

60. Starting from an equilibrium at E1 in Exhibit 16-1, a leftward shift of the money supply curve from

MS1 to MS2 would cause an excess:

a.

demand for money, leading people to sell bonds.

b.

demand for money, leading people to buy bonds.

c.

supply of money, leading people to sell bonds.

d.

supply of money, leading people to buy bonds.

61. Beginning from an equilibrium at E1 in Exhibit 16-1, a decrease in the money supply from $150 billion

to $100 billion causes people to:

a.

sell bonds and drive the price of bonds down.

b.

sell bonds and drive the price of bonds up.

c.

buy bonds and drive the price of bonds down.

d.

buy bonds and drive the price of bonds up.

62. As shown in Exhibit 16-1, assume the money supply curve shifts leftward from MS1 to MS2 and the

economy is operating along the intermediate segment of the aggregate supply curve. The result will be

a:

a.

higher investment, lower real GDP, and lower price level.

b.

lower investment, lower real GDP, and lower price level.

c.

higher investment, higher real GDP, and higher price level.

d.

higher interest rate and no effect on real GDP or the price level.

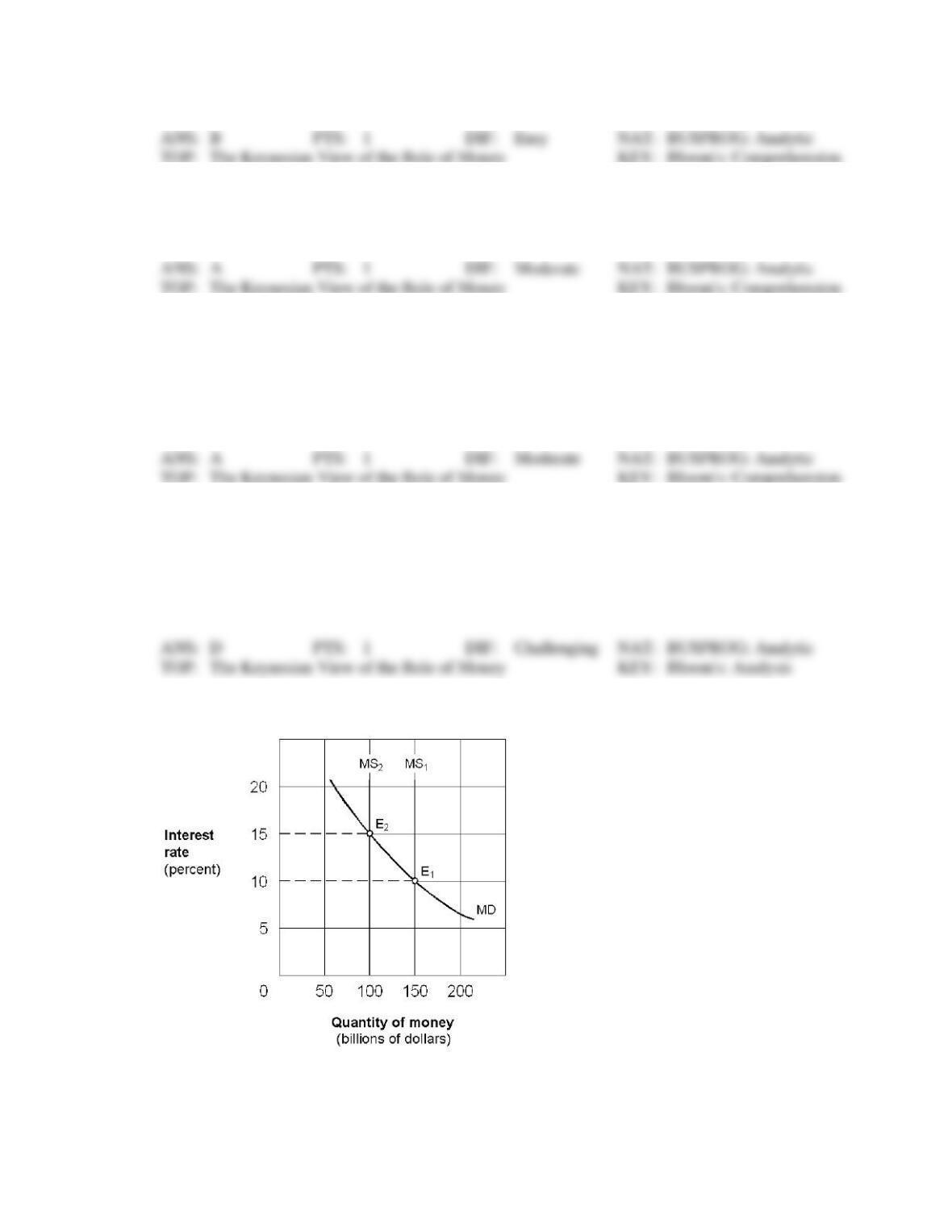

Exhibit 16-2 Money market demand and supply curves

63. Starting from an equilibrium at E1 in Exhibit 16-2, a rightward shift of the money supply curve from

MS1 to MS2 would cause an excess:

a.

demand for money, leading people to sell bonds.

b.

supply of money, leading people to buy bonds.

c.

supply of money, leading people to sell bonds.

d.

demand for money, leading people to buy bonds.

64. Beginning from an equilibrium at E1 in Exhibit 16-2, an increase in the money supply from $400

billion to $600 billion causes people to:

a.

sell bonds and drive the price of bonds down.

b.

buy bonds and drive the price of bonds up.

c.

buy bonds and drive the price of bonds down.

d.

sell bonds and drive the price of bonds up.

65. As shown in Exhibit 16-2, assume the money supply curve shifts rightward from MS1 to MS2 and the

economy is operating along the intermediate segment of the aggregate supply curve. The result will be

a:

a.

higher interest rate and no effect on real GDP or the price level.

b.

lower investment, lower real GDP, and lower price level.

c.

higher investment, higher real GDP, and higher price level.

d.

higher investment, lower real GDP, and lower price level.

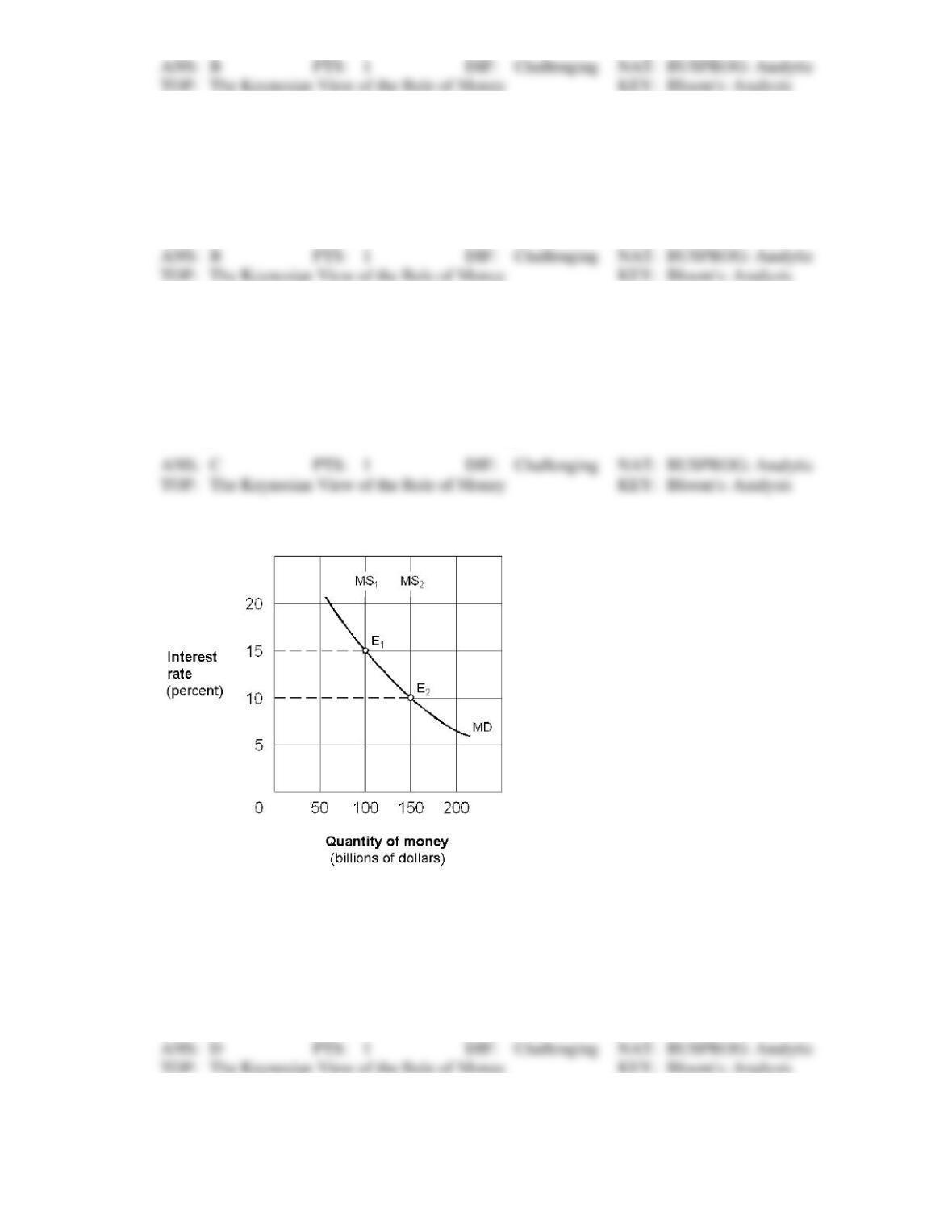

Exhibit 16-3 Money market demand and supply curves

66. In Exhibit 16-3, assume an equilibrium with an interest rate of 15 percent and the money supply at

$100 billion. The Fed uses its policy tools to move the economy to a new equilibrium at E2 with money

supply of $150 billion and an interest rate of 10 percent. This change could be the result of a(n):

a.

open market sale of securities by the Fed.

b.

higher discount rate set by the Fed.

c.

higher required-reserve ratio set by the Fed.

d.

open market purchase of securities by the Fed.

67. In Exhibit 16-3, assume an equilibrium at E2 with the money supply at $100 billion and the interest

rate at 15 percent. The Fed uses its policy tools to move the economy to a new equilibrium at E1 with a

money supply of 150 billion and an interest rate of 10 percent. As part of the adjustment to the new

equilibrium, we would expect the:

a.

price of bonds to rise.

c.

price of bonds to fall.

b.

price of bonds to remain unchanged.

d.

none of these.

68. As shown in Exhibit 16-3, assume the money supply curve shifts rightward from MS1 to MS2 and the

economy is operating along the intermediate segment of the aggregate supply curve. The result will be

a:

a.

higher investment, lower real GDP, and lower price level.

b.

lower investment, lower real GDP, and lower price level.

c.

higher investment, higher real GDP, and higher price level.

d.

higher interest rate and no effect on real GDP or the price level.

69. Starting from a position of macroeconomic equilibrium at below the full-employment level of real

GDP, an increase in the money supply will:

a.

raise interest rates, prices, and reduce real GDP.

b.

raise interest rates, lower prices, and leave real GDP unchanged.

c.

raise interest rates, lower prices, and leave real GDP unchanged.

d.

lower interest rates, raise prices, and increase real GDP.

70. An increase in the supply of money will:

a.

reduce the rate of interest and, thereby, trigger an increase in current spending by

households and businesses.

b.

reduce aggregate demand and real output.

c.

increase only the general level of prices.

d.

lead to a higher rate of unemployment.

71. The impact of an increase in the money supply is a(n):

a.

increase in the interest rate, which in turn stimulates investment and GDP.

b.

decrease in the interest rate, which in turn stimulates investment and GDP.

c.

reduction in the general level of prices, which will increase the disposable income of

households.

d.

improvement in technology, which will stimulate both output and employment.

72. Which of the following is the objective of expansionary monetary policy?

a.

An increase in employment.

b.

A decrease in employment.

c.

An increase in the velocity of money.

d.

An increase in prices proportional to the rise in the money supply.

73. When the Fed reduces the money supply, it will cause a decrease in aggregate demand because:

a.

real rates will rise, lowering business investment and consumer spending.

b.

the dollar will depreciate on the foreign exchange market, leading to an increase in net

exports.

c.

lower interest rates will cause the value of assets (for example, stocks) to rise.

d.

the national debt will increase, causing consumers to reduce their spending.

74. Which of the following policies would be most likely to reduce the rate of inflation?

a.

sale of government bonds by the Federal Reserve

b.

a reduction in the discount rate

c.

an increase in the size of the federal budget deficit

d.

a reduction in the required reserves imposed on the banking system

75. Using the aggregate supply and demand model, assume the economy is operating along the

intermediate portion of the aggregate supply curve. An increase in the money supply will increase the

price level and:

a.

lower both the interest rate and real GDP.

b.

raise both the interest rate and real GDP.

c.

lower the interest rate and raise GDP.

d.

raise the interest rate and lower real GDP.

76. An increase in the money supply:

a.

lowers the interest rate, causing a decrease in investment and an increase in GDP.

b.

lowers the interest rate, causing an increase in investment and a decrease in GDP.

c.

lowers the interest rate, causing an increase in investment and an increase in GDP.

d.

raises the interest rate, causing an increase in investment and an increase in GDP.

e.

raises the interest rate, causing a decrease in investment and a decrease in GDP.

77. A decrease in the money supply:

a.

lowers the interest rate, causing a decrease in investment and a decrease in GDP.

b.

lowers the interest rate, causing a decrease in investment and an increase in GDP.

c.

raises the interest rate, causing an increase in investment and a decrease in GDP.

d.

raises the interest rate, causing an increase in investment and an increase in GDP.

e.

raises the interest rate, causing a decrease in investment and a decrease in GDP.

78. An increase in the money supply:

a.

raises the interest rate, causing an increase in investment and an increase in GDP.

b.

lowers the interest rate, causing an increase in investment and an increase in GDP.

c.

raises the interest rate, causing a decrease in investment and an increase in GDP.

d.

lowers the interest rate, causing a decrease in investment and an increase in GDP.

e.

lowers the interest rate, causing a decrease in investment and a decrease in GDP.

79. A decrease in the money supply:

a.

raises the interest rate, causing an increase in investment and an increase in GDP.

b.

lowers the interest rate, causing an increase in investment and an increase in GDP.

c.

raises the interest rate, causing a decrease in investment and a decrease in GDP.

d.

lowers the interest rate, causing a decrease in investment and an increase in GDP.

e.

lowers the interest rate, causing a decrease in investment and a decrease in GDP.

80. The Keynesian mechanism through which monetary policy affects the price level, real GDP, and

employment depends on the impact of the:

a.

interest rate on savings.

c.

interest rate on investment.

b.

inflation on investment.

d.

interest rate on bond prices.

81. If the economy is inflationary, the Fed would most likely:

a.

encourage banks to provide loans by buying government securities.

b.

encourage banks to provide loans by raising the discount rate.

c.

encourage banks to provide loans by selling government securities.

d.

restrict bank lending by selling government securities.

e.

restrict bank lending by lowering the federal funds rate.

82. According to Keynesian economists, which of the following is not a consequence of increasing the

money supply?

a.

A lower interest rate.

c.

Lower real GDP.

b.

Greater investment.

d.

Higher real GDP.

83. Keynesian economists argue that monetary policy works through its effects on:

a.

interest rates and investment.

c.

budget deficits and trade deficits.

b.

price- and wage-flexibility.

d.

the spending and money multipliers.

84. According to Keynesians, an increase in the money supply will:

a.

decrease the interest rate, and increase investment, aggregate demand, prices, real GDP,

and employment.

b.

decrease the interest rate, and decrease investment, aggregate demand, prices, real GDP,

and employment.

c.

increase the interest rate, and decrease investment, aggregate demand, prices, real GDP,

and employment.

d.

only increases prices.

85. Keynesians believe that an increase in the money supply will lead to:

a.

both c and d.

b.

all of the following.

c.

an increase in the price level.

d.

a decrease in nominal GDP.

e.

an increase in real GDP.

86. The Keynesian cause-and-effect sequence predicts that an increase in the money supply will cause

interest rates to:

a.

fall, boosting investment and shifting the AD curve rightward, leading to an increase in

real GDP.

b.

fall, boosting investment and shifting the AD curve rightward, leading to a decrease in real

GDP.

c.

rise, cutting investment and shifting the AD curve rightward, leading to an increase in real

GDP.

d.

rise, boosting investment and shifting the AD curve rightward, leading to an increase in

real GDP.

e.

fall, cutting investment and shifting the AD curve leftward, leading to a decrease in real

GDP.

87. The Keynesian cause-and-effect sequence predicts that a decrease in the money supply will cause

interest rates to:

a.

fall, boosting investment and shifting the AD curve rightward, leading to an increase in

real GDP.

b.

fall, boosting investment and shifting the AD curve rightward, leading to a decrease in real

GDP.

c.

rise, cutting investment and shifting the AD curve rightward, leading to an increase in real

GDP.

d.

rise, boosting investment and shifting the AD curve rightward, leading to an increase in

real GDP.

e.

rise, cutting investment and shifting the AD curve leftward, leading to a decrease in real

GDP.

88. While the classicists believed that both velocity and output are stable, Keynesians believe:

a.

velocity is stable and output is variable.

b.

velocity and output are both variable.

c.

output is stable and velocity is variable

d.

the same as the classical economists that both output and velocity are stable

e.

at low levels of income both velocity and output are stable, but at high levels of income

velocity becomes variable.

89. An increase in the supply of money will lead to ____ in equilibrium real GDP and ____ in equilibrium

price level.

a.

an increase; an increase

c.

a decreases; an increase

b.

an increase; a decrease

d.

a decrease; a decrease

90. According to Keynesians, an increase in the money supply will have its greatest impact on GDP when

the aggregate demand curve intersects:

a.

the vertical portion of the aggregate supply curve.

b.

the upward sloping portion of the aggregate supply curve.

c.

the horizontal portion of the aggregate supply curve.

d.

either the upward sloping or the vertical portions of the aggregate supply curve.

e.

either the horizontal or vertical portions of the aggregate supply curve.

91. According to Keynesians, an increase in the money supply will have its least impact on GDP when the

aggregate demand curve intersects:

a.

the horizontal portion of the aggregate supply curve.

b.

the vertical portion of the aggregate supply curve.

c.

the upward sloping portion of the aggregate supply curve.

d.

either the horizontal or upward sloping portion of the aggregate supply curve.

e.

either the horizontal or upward sloping portion of the aggregate supply curve.

92. According to Keynesians, for monetary policy to have a stimulative effect on GDP, a(n):

a.

increase in the money supply lowers the interest rate in order to stimulate higher levels of

investment.

b.

increase in the money supply lowers the interest rate in order to lower levels of

investment.

c.

decrease in the money supply lowers interest rate in order to stimulate higher levels of

investment

d.

decrease in the money supply causes the interest rate to rise in order to stimulate higher

levels of investment.

e.

increase in the money supply causes the interest rate to rise in order to stimulate higher

levels of investment.

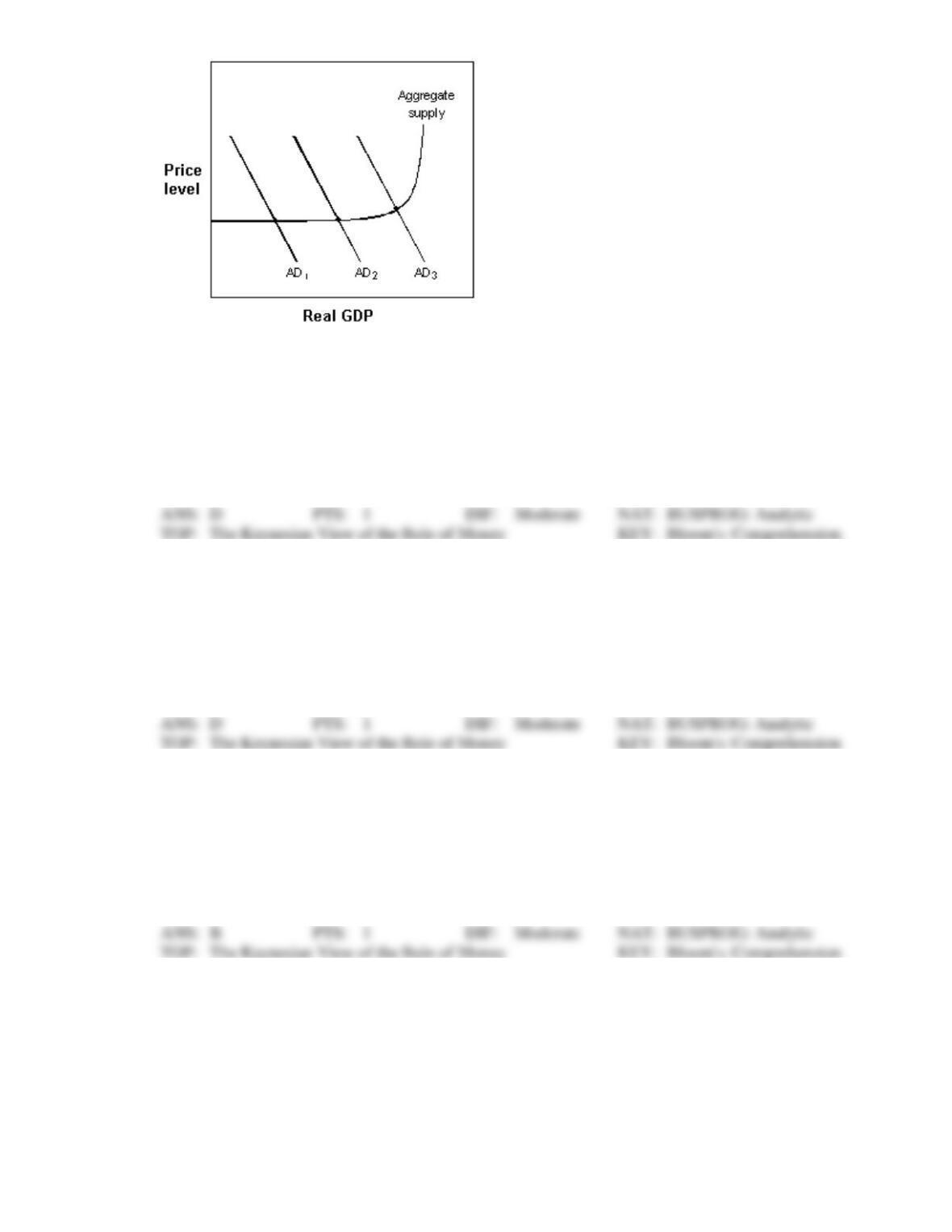

Exhibit 16-4 Aggregate demand and supply model

93. In Exhibit 16-4, which one of the following actions could the Fed use to shift the AD curve from AD1

to AD2?

a.

Raise the legal reserve requirement.

b.

Raise the discount rate.

c.

Lower the federal funds rate.

d.

Buy government securities.

e.

Print currency.

94. In Exhibit 16-4, which one of the following actions could the Fed use to shift the AD curve from AD3

to AD2?

a.

Lower the legal reserve requirement.

b.

Lower the discount rate.

c.

Lower the federal funds rate.

d.

Sell government securities.

e.

Print currency.

95. In Exhibit 16-4, which one of the following actions could the Fed use to shift the AD curve from AD1

to AD2?

a.

Raise the legal reserve requirement.

b.

Lower the discount rate.

c.

Lower the federal funds rate.

d.

Sell government securities.

e.

Raise the federal funds rate.

96. In Exhibit 16-4, which one of the following actions could the Fed use to shift the AD curve from AD3

to AD2?

a.

Lower the legal reserve requirement.

b.

Lower the discount rate.

c.

Lower the federal funds rate.

d.

Raise the discount rate.

e.

Buy government securities.