Chapter 16: Statement of Cash Flows

Chapter 16: Statement of Cash Flows

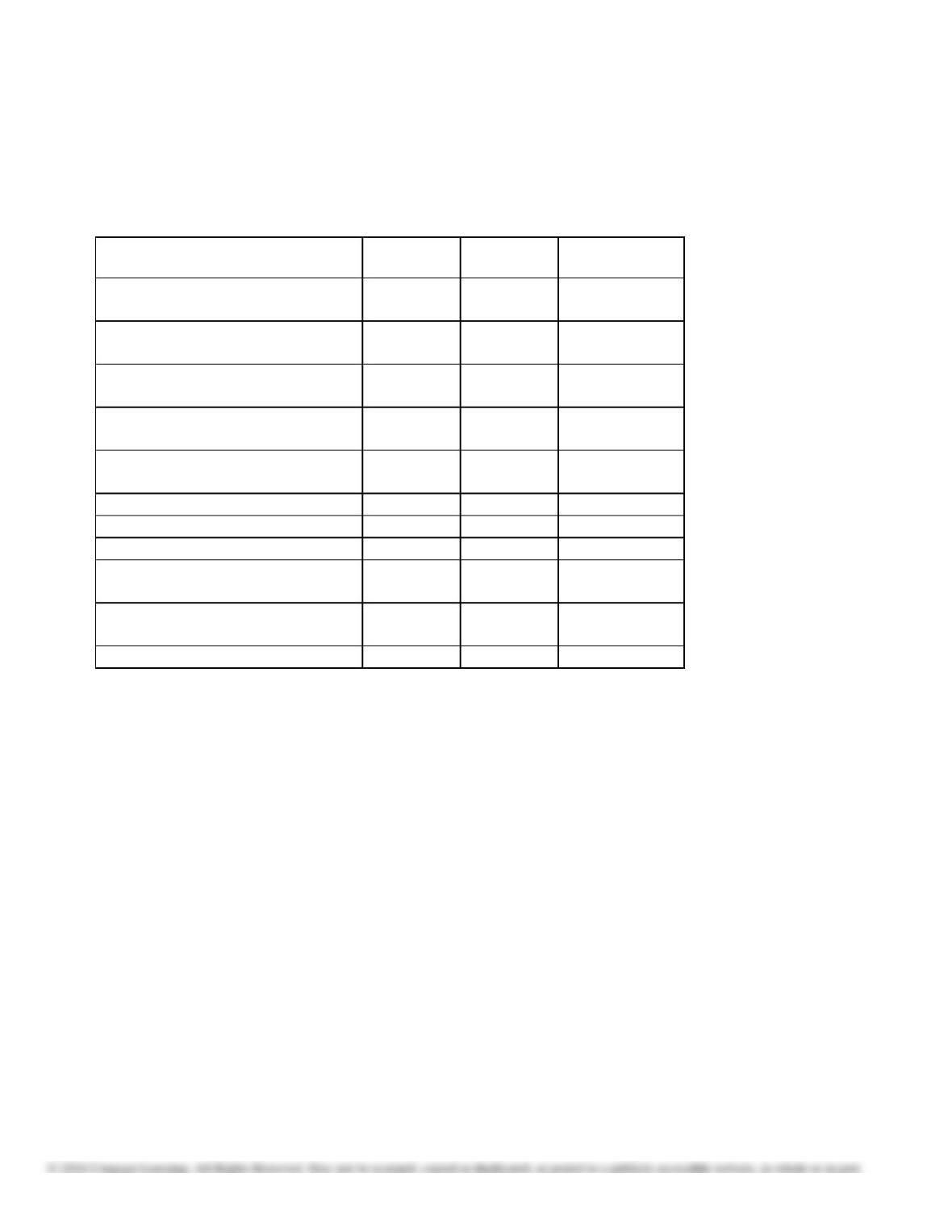

159.

Complete each of the columns on the table below, indicating in which section each item would be reported on

the

statement of cash flows (operating, investing, or financing), the amount that would be reported, and whether

the

item would create an increase or decrease in cash. For item that affect more than one section of the

statement,

indicate all affected. Assume the indirect method of reporting cash flows from operating activities.

The first item has been completed as an example.

Statement

Amount

+/– Effect

Item

Section

to Report

on Cash

Depreciation of $15,000 for the

period

Operating

$15,000

Increase

Issuance of common stock for

$35,000

Increase in accounts payable of

$7,000

Retirement of $100,000 bonds

payable

at 97

Purchase of long-term investments for

$94,500

Dividends declared and paid of $8,300

Increase in prepaid rent of $4,500

Decrease in Inventory of $5,300

Purchase of equipment for $17,600

cash

Sale of land originally costing

$134,000 for $130,000

Decrease in taxes payable of $2,100

Chapter 16: Statement of Cash Flows

Chapter 16: Statement of Cash Flows

160.

Balances of the current asset and current liability accounts at the end and beginning of the year are as follows:

End

Beginning

Cash

$ 62,000

$73,000

Accounts receivable (net)

75,000

60,000

Inventories

54,000

47,000

Accounts payable (merchandise creditors)

43,000

37,000

Salaries payable

2,800

3,800

Sales (on account)

210,000

Cost of merchandise sold

70,000

Operating expenses other than depreciation

67,000

Use the direct method to prepare the cash flows from operating activities section of a statement of cash flows.

Chapter 16: Statement of Cash Flows

161.

The comparative balance sheet of ConnieJo Company, for December 31, Years 1 and 2 ended December 31

appears below in condensed form:

Cash

Year 2

$ 45,000

Year 1

$ 53,500

Accounts receivable (net)

51,300

58,000

Inventories

147,200

135,000

Investments

0

60,000

Equipment

493,000

375,000

Accumulated depreciation—equipment

(113,700)

(128,000)

$622,800

$553,500

Accounts payable

$ 61,500

$ 42,600

Bonds payable, due Year 4

0

100,000

Common stock, $10 par

250,000

200,000

50,000

160,900

$553,500

$623,000

348,500

$274,500

100,000

$174,500

Paid-in capital in excess of par—common stock

75,000

Retained earnings

236,300

$622,800

The income statement for the current year is as follows:

Sales

Cost of merchandise sold

Gross profit

Operating expenses:

Depreciation expense

$ 24,700

Other operating expenses

75,300

Income from operations

Other income:

Gain on sale of investment

$ 5,000

Other expense:

Interest expense

12,000

(7,000)

Income before income tax

$167,500

Income tax

64,100

Net income

$103,400

Additional data for the current year are as follows:

(a)

Fully depreciated equipment costing $39,000 was scrapped, no salvage,

and

equipment was purchased for $157,000.

(b)

Bonds payable for $100,000 were retired by payment at their face amount.

(c)

5,000 shares of common stock were issued at $15 for cash.

(d)

Cash dividends declared were paid $28,000.

(e)

All sales are on account.

Prepare a statement of cash flows, using the direct method of reporting cash flows from operating activities.

Chapter 16: Statement of Cash Flows

Chapter 16: Statement of Cash Flows

162.

The cash flows from operating activities are reported by the direct method on the statement of cash

flows. Determine the following:

(a)

If sales for the current year were $375,000 and accounts receivable increased by $29,000

during the year, what was the amount of cash received from customers?

(b)

If income tax for the current year was $39,000 and income tax payable decreased by $21,000 during the year,

what was the amount of cash payments for income tax?

Chapter 16: Statement of Cash Flows

163.

Selected data for the current year ended December 31 are as follows:

Balance

Balance

December 31

January 1

Accrued expenses (operating expenses)

$29,500

$ 22,000

Accounts payable (merchandise creditors)

90,000

135,000

Inventories

42,500

68,000

Prepaid expenses

23,000

20,000

During the current year, the cost of merchandise sold was $620,000 and the operating expenses other than

depreciation were $142,000. The direct method is used for presenting the cash flows from operating activities on

the statement of cash flows.

Determine the amount reported on the statement of cash flows for (a) cash payments for merchandise and (b) cash

payments for operating expenses.

Deduct increase in accrued expenses

7,500

Add increase in prepaid expenses

3,000

Chapter 16: Statement of Cash Flows

164.

Based on the following, what is free cash flow?

Net cash flow from operating activities

$318,000

Net cash flow used for investing activities

(30,000)

Net cash flow from financing activities

30,000

Cash flows from operations include $2,000 for depreciation. Cash flows from investing include the purchase of a

replacement asset for $100,000 and the sale of the one used in production, which is now obsolete, for $70,000. Cash

flows from financing include $70,000 of borrowing.

165.

Balances of the current asset and current liability accounts at the end and beginning of the year are as follows:

End

Beginning

Cash

$ 67,000

$73,000

Accounts receivable (net)

73,000

60,000

Inventories

54,000

47,000

Accounts payable

(merchandise creditors)

43,000

37,000

Salaries payable

2,800

3,800

Sales (on account)

210,000

Cost of merchandise sold

70,000

Operating expenses other than depreciation

67,000

Use the direct method to prepare the cash flows from operating activities section of a statement of cash flows.

Cash flows from operating activities:

Cash received from customers

Deduct: Cash payments for merchandise

Cash payments for operating expenses

Net cash flow from operating activities

Chapter 16: Statement of Cash Flows

166.

Cost of merchandise sold reported on the income statement was $155,000. The accounts payable balance

increased $8,000, and the inventory balance increased by $21,000 over the year. Determine the amount of

cash

paid for merchandise.

167.

Sales reported on the income statement were $690,000. The accounts receivable balance declined $39,000

over

the year. Determine the amount of cash received from customers.

Chapter 16: Statement of Cash Flows

168.

Selected data taken from the accounting records of Laser Inc. for the current year ended December 31 are as

follows:

Balance,

December 31

Balance,

January 1

Accrued operating expenses

$ 5,590

$ 6,110

Accounts payable (merchandise creditors)

41,730

46,020

Inventories

77,350

84,110

Prepaid expenses

3,250

3,900

During the current year, the cost of merchandise sold was $448,500, and the operating expenses other than

depreciation were $78,000. The direct method is used for presenting the cash flows from operating activities on

the

statement of cash flows.

Required:

Determine the amount reported on the statement of cash flows for:

(1)

Cash payments for merchandise

(2)

Cash payments for operating expenses

Chapter 16: Statement of Cash Flows

169.

The cash flows from operating activities are reported by the direct method on the statement of cash

flows.

(1)

(2)

Determine the following:

If sales for the current year were $695,000 and accounts receivable decreased

by $43,500 during the year, what was the amount of cash received from

customers?

If income tax expense for the current year was $56,000 and income tax payable

decreased by $5,200 during the year, what was the amount of cash payments of

income tax?

170.

Connor Designs Company has cash flows for operating activities of $425,000. Cash flows used for investments in

property, plant, and equipment totaled $65,000, of which 70% of this investment was used to replace machinery

to

maintain existing capacity.

What is the free cash flow for Connor Designs?

Chapter 16: Statement of Cash Flows

For each of the following activities that may take place during the accounting period, indicate the effect (a-g) on the

statement of cash flows prepared using the indirect method. Choices may be selected as the

answer for more than

one question.

a.

increase cash from operating activities

b.

decrease cash from operating activities

c.

increase cash from investing activities

d.

decrease cash from investing activities

e.

increase cash from financing activities

f.

decrease cash from financing activities

g.

noncash investing and financing supplement

DIFFICULTY: Moderate

Bloom’s: Remembering

LEARNING OBJECTIVES: ACCT.WARD.16.16-02 – 16–02

ACCREDITING STANDARDS: ACCT.ACBSP.APC.24 – Statement of Cash Flows

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

171.

purchase of equipment

172.

repayment of long-term note payable

173.

amortization of intangible assets

174.

exchange of land for common stock

175.

payment of dividends

176.

sale of land

177.

gain on sale of investments

Chapter 16: Statement of Cash Flows

178.

acquisition of treasury stock

179.

increase in accounts receivable balance

180.

decrease in accounts payable balance

Identify the section of the statement of cash flows (a-d) where each of the following items would be

reported.

a. Operating activities

b. Financing activities

c. Investing activities

d. Schedule of noncash financing and investing

DIFFICULTY: Bloom’s:

Remembering

Easy

LEARNING OBJECTIVES: ACCT.WARD.16.16-02 – 16–02

ACCT.WARD.16.16-04 – 16–04

ACCREDITING STANDARDS: ACCT.ACBSP.APC.24 – Statement of Cash Flows

ACCT.AICPA.FN.03 – Measurement

BUSPROG: Analytic

181.

Increase in income taxes payable

182.

Dividends received on investment

183.

Sale of machinery held for use by the company

184.

Issuance of bond payable

185.

Purchase of the stock of another company as investment

Chapter 16: Statement of Cash Flows

186.

Decrease in inventory

187.

Exchange of land for note payable

188.

Payment of dividends to stockholders

189.

Increase in accounts receivable

190.

Loss on sale of equipment