15.3 How Does a Monopoly Choose Price and Output?

1) A monopoly firm’s demand curve

A) is the same as the market demand curve.

B) is perfectly inelastic.

C) is more inelastic than the demand curve for the product.

D) is inelastic at high prices and elastic at lower prices.

2) Which of the following is true for a monopolist?

A) Being the only seller in the market, the monopolist faces a perfectly inelastic demand curve.

B) Being the only seller in the market, the monopolist faces a perfectly elastic demand curve.

C) Being the only seller in the market, the monopolist faces the market demand curve.

D) Being the only seller in the market, the monopolist faces a downward sloping demand curve

that lies below the marginal revenue curve.

3) A price maker is

A) a person who actively seeks out the best price for a product that he or she wishes to buy.

B) a firm that has some control over the price of the product it sells.

C) a firm that is able to sell any quantity at the highest possible price.

D) a consumer who participates in an auction where she announces her willingness to pay for a

product.

4) Firms that face downward-sloping demand curves for their output in the product market are

called

A) price takers.

B) price dictators.

C) monopolists.

D) price makers.

5) Wendell can sell five motor homes per week at a price of $22,000. If he lowers the price of

motor homes to $20,000 per week he will sell six motor homes. What is the marginal revenue of

the sixth motor home?

A) $10,000

B) $12,000

C) $20,000

D) $22,000

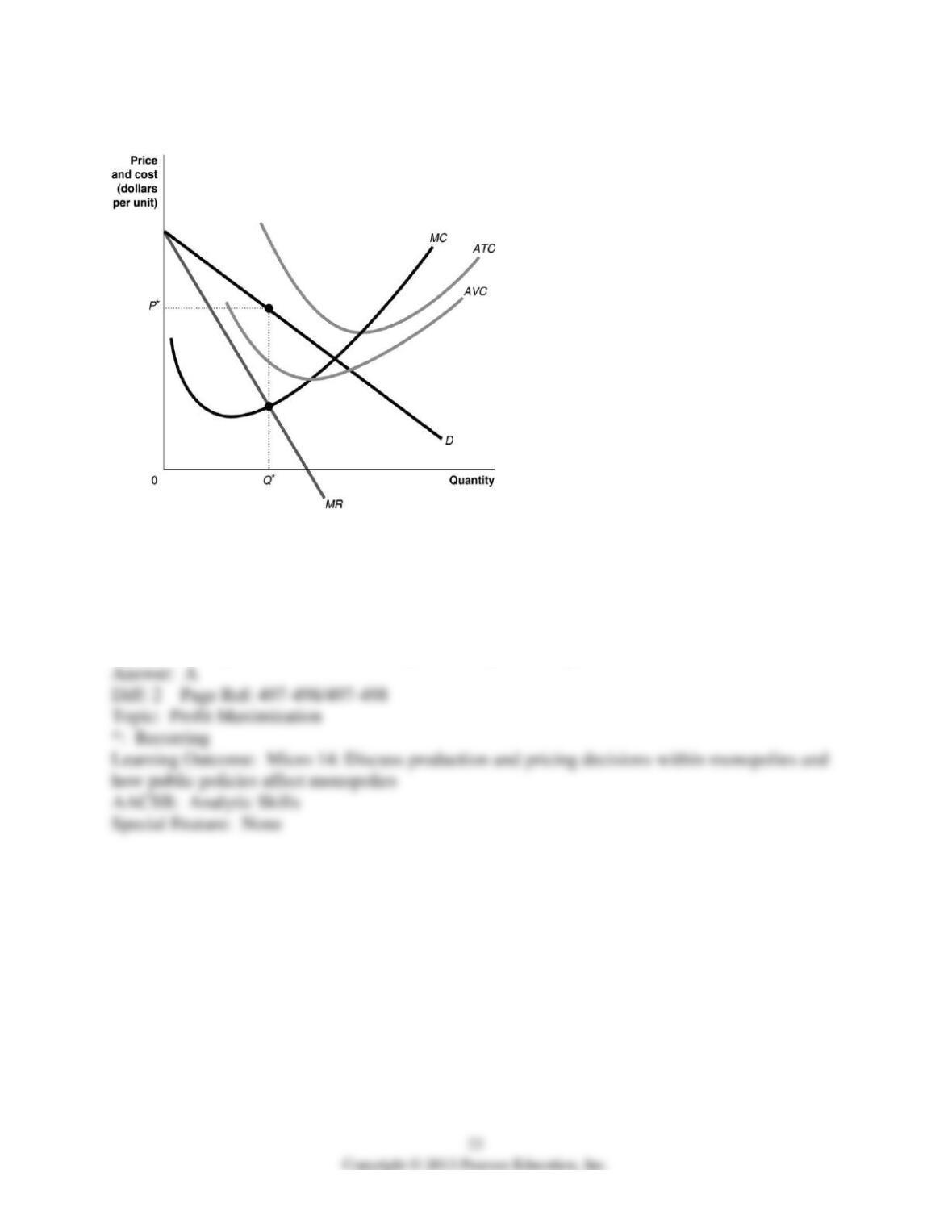

Figure 15-2

6) Refer to Figure 15-2. If the monopolist charges price P* for output Q*, in order to maximize

profit or minimize loss in the short run, it should

A) continue to produce because price is greater than average variable cost.

B) shut down because price is greater than marginal cost.

C) shut down because price is less than average total cost.

D) continue to produce because a monopolist always earns a profit.

Table 15-1

Quantity per

Day (cases)

Price per

Case

Total Cost

1

$16

$7.00

2

15

9.50

3

14

11.00

4

13

12.00

5

12

14.50

6

11

17.50

7

10

21.00

8

9

25.00

9

8

30.00

10

7

35.50

The government of a small developing country has granted exclusive rights to Linden

Enterprises for the production of plastic syringes. Table 15-1 shows the cost and demand data for

this government protected monopolist.

7) Refer to Table 15-1. What is the profit-maximizing quantity and price for the monopolist?

A) Quantity = 8 cases, Price = $9

B) Quantity = 7 cases, Price = $10

C) Quantity = 9 cases, Price = $8

D) Quantity = 10 cases, Price = $7

8) Refer to Table 15-1. What is the amount of profit that the firm earns?

A) $34.50

B) $42

C) $47

D) $49

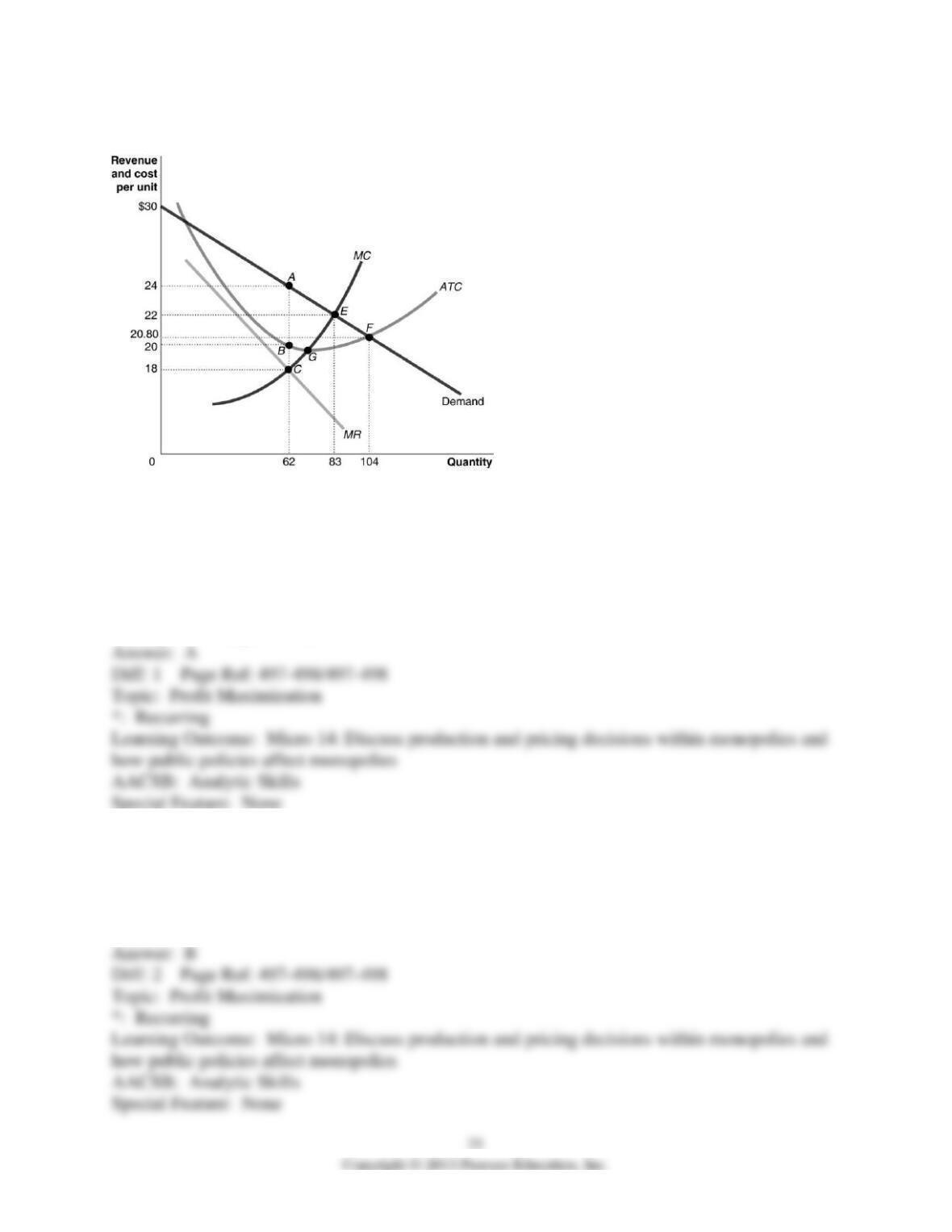

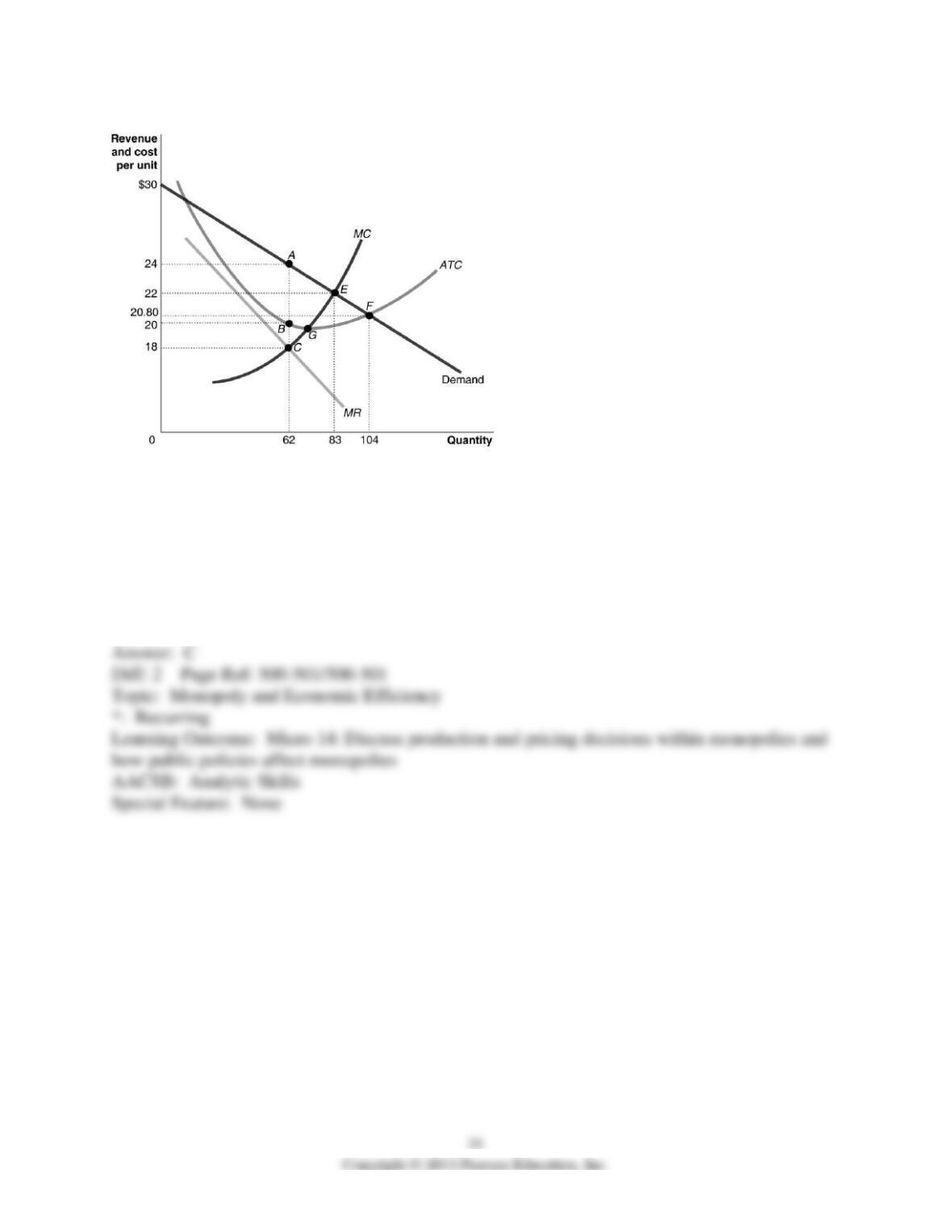

Figure 15-3

Figure 15-3 shows the cost and demand curves for a monopolist.

9) Refer to Figure 15-3. The profit-maximizing output and price for the monopolist are

A) output = 62; price = $24.

B) output = 62; price = $18.

C) output = 83; price = $22.

D) output = 104; price = $20.80.

10) Refer to Figure 15-3. The monopolist’s total revenue is

A) $1,116.

B) $1,488.

C) $1,726.40

D) $1,826.

11) Refer to Figure 15-3. The monopolist’s total cost is

A) $1,116.

B) $1,240.

C) $1,660.

D) $1,726.40.

12) Refer to Figure 15-3. The monopolist earns a profit of

A) $0.

B) $170.

C) $248.

D) $372.

Table 15-2

Price

Quantity

Total

Revenue

Marginal

Revenue

Total Cost

Marginal

Cost

$17

3

$51

—–

$56

—–

16

4

64

$13

63

$7

15

5

75

11

71

8

14

6

84

9

80

9

13

7

91

7

90

10

12

8

96

5

101

11

Assume Table 15-2 gives the monthly demand and costs for subscriptions to basic cable for

Comcast, a cable television monopoly in Philadelphia.

13) Refer to Table 15-2. If Comcast wants to maximize its profits, what price (P) should it

charge and how many cable subscriptions per month (Q) should it sell?

A) P = $12; Q = 8

B) P = $14; Q = 6

C) P = $16; Q = 4

D) P = $15: Q = 5

14) Refer to Table 15-2. If Comcast maximizes its profits how much profit will it earn?

A) $84

B) $40

C) $4

D) Comcast will break even.

15) To maximize profit a monopolist will produce where

A) marginal revenue is equal to marginal cost.

B) demand for its product is unit-elastic.

C) revenue per unit is maximized.

D) average total cost is equal to average revenue.

16) If a monopolist’s marginal revenue is $35 per unit and its marginal cost is $25, then

A) to maximize profit the firm should increase output.

B) to maximize profit the firm should decrease output.

C) to maximize profit the firm should continue to produce the output it is producing.

D) Not enough information is given to say what the firm should do to maximize profit.

17) If a monopolist’s price is $50 at 63 units of output and marginal revenue equals marginal cost

and average total cost equals $43, then the firm’s total profit is

A) $3,150.

B) $2,709.

C) $441.

D) $7.

18) Which of the following statements is true?

A) Monopolists are price makers. All other firms are price takers.

B) Unlike other industries, monopoly industries have high barriers to entry.

C) Only monopoly firms are granted patents and copyrights.

D) Unlike other firms, a monopolist’s demand curve is the same as the market demand curve.

19) The demand curve for a monopoly firm

A) is perfectly inelastic.

B) lies below its marginal revenue curve.

C) is the same as the market demand curve.

D) is horizontal.

20) A monopolist will maximize profit where marginal revenue equals marginal cost.

21) A monopolist’s demand curve is the same as the marginal revenue curve for the product.

22) If a monopolist’s price is $50 at the output where marginal revenue equals marginal cost and

average total cost is $43, then the incremental profit from the last unit sold is $7.

23) A monopolist currently sells 18 units of a good. If marginal revenue on the last unit sold is

$117, then the price of the good must be less than $117.

24) What is the difference between a monopoly’s marginal revenue curve and a perfect

competitor’s marginal revenue curve?

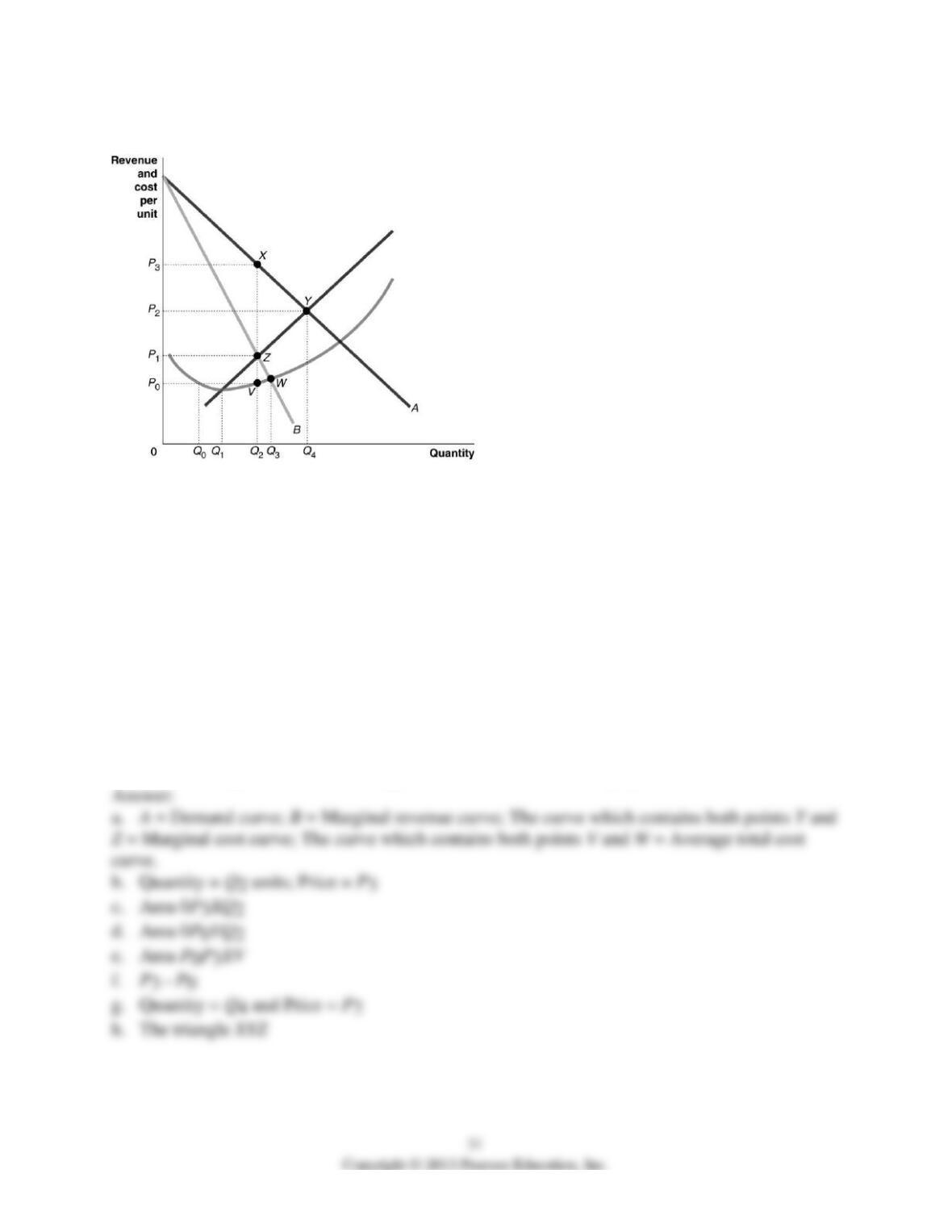

Figure 15-4

Figure 15-4 reflects the cost and revenue structure for a monopoly that has been in business for a

very long time.

25) Refer to Figure 15-4. Use the figure above to answer the following questions.

a. Identify the curves labeled A and B. Identify the curve which contains both point Y and point

Z. Identify the curve which contains both point V and point W.

b. What is the profit-maximizing quantity and what price will the monopolist charge?

c. What area represents total revenue at the profit-maximizing output level?

d. What area represents total cost at the profit-maximizing output level?

e. What area represents profit?

f. What is the profit per unit (average profit) at the profit-maximizing output level?

g. If this industry was organized as a perfectly competitive industry, what would be the profit-

maximizing price and quantity?

h. What area represents the deadweight loss as a result of a monopoly?

26) “Being the only seller in the market, the monopolist can choose any price and quantity it

desires.” Evaluate this statement: is it true or false? Explain your answer.

27) Explain whether a monopoly that maximizes profit will also be maximizing revenue and

production.

15.4 Does Monopoly Reduce Economic Efficiency?

1) Assume a hypothetical case where an industry begins as perfectly competitive and then

becomes a monopoly. Which of the following statements regarding economic surplus in each

market structure is true?

A) Under perfectly competitive conditions, economic surplus in this industry equals consumer

surplus plus producer surplus. Under monopoly conditions, some consumer surplus is transferred

to producer surplus, but economic surplus is the same as it was under perfectly competitive

conditions.

B) Under perfectly competitive conditions, economic surplus in this industry is maximized.

Under monopoly conditions economic surplus is minimized.

C) Under perfectly competitive conditions, economic surplus is equal to consumer surplus; there

is no producer surplus because firms are price-takers. Under monopoly conditions, economic

surplus is equal to producer surplus.

D) Under perfectly competitive conditions, economic surplus is maximized. Under monopoly

conditions economic surplus is less than under perfect competition and there is a deadweight

loss.

2) Assume a hypothetical case where an industry begins as perfectly competitive and then

becomes a monopoly. Which of the following statements comparing the conditions in the

industry under both market structures is true?

A) A monopoly will produce more and charge a higher price than would a perfectly competitive

industry producing the same good.

B) A monopoly will produce more and advertise more than would a perfectly competitive

industry producing the same good.

C) A monopoly will produce less and charge a higher price than would a perfectly competitive

industry producing the same good.

D) A monopoly will produce less and charge a lower price than would a perfectly competitive

industry producing the same good.

34

3) Assume a hypothetical case where an industry begins as perfectly competitive and then

becomes a monopoly. As a result of this change

A) Price will be higher, output will be lower and the deadweight loss will be eliminated.

B) Consumer surplus will be smaller, producer surplus will be greater and there will be a

reduction in economic efficiency.

C) Price will be higher, consumer surplus will be greater and output will be greater.

D) Consumer surplus will be smaller and producer surplus will be greater. There will be a net

increase in economic surplus.

4) The most profitable price for a monopolist is

A) the highest price a consumer is willing to pay for the monopolist’s product.

B) the price at which demand is unit-elastic.

C) a price that maximizes the quantity sold.

D) the price for which marginal revenue equals marginal cost.

5) Which of the following statements is true?

A) If a tax is imposed on a product sold by a monopolist, the monopolist will maximize its

profits by producing where marginal revenue equals marginal cost.

B) A monopolist will always charge the highest possible price.

C) If a tax is imposed on a product sold by a monopolist, the monopolist can increase its price to

pass along the entire tax to consumers.

D) Because a monopolist faces no competition, the demand for its product is perfectly inelastic.

Figure 15-5

Figure 15-5 shows the cost and demand curves for a monopolist.

6) Refer to Figure 15-5. Assume the firm maximizes its profits. What is the amount of consumer

surplus?

A) $21

B) $124

C) $186

D) $332

7) Refer to Figure 15-5. What is the amount of consumer surplus if, instead of monopoly, the

industry was organized as a perfectly competitive industry?

A) $21

B) $124

C) $186

D) $332

8) Refer to Figure 15-5. If this industry was organized as a perfectly competitive industry, the

market output and market price would be

A) output = 62; price = $24.

B) output = 83; price = $22.

C) output = 62; price = $18.

D) output = 104; price = $20.80.

9) Refer to Figure 15-5. If the firm maximizes its profits, the deadweight loss to society due to

this monopoly is equal to the area

A) ABF.

B) ABEG.

C) ACE.

D) EFG.

10) The ability of a firm to charge a price greater than marginal cost is called

A) monopoly power.

B) price-making power.

C) cost-plus pricing.

D) market power.

11) Whenever a firm can charge a price greater than marginal cost,

A) the firm must be a monopolist.

B) there is some loss of economic efficiency.

C) consumers have the ability to choose a close substitute.

D) the firm will earn economic profits.

12) The only firms that do not have market power are

A) firms in industries with low barriers to entry.

B) firms that do not advertise their products.

C) firms in perfectly competitive markets.

D) firms that sell identical products.

13) Arnold Harberger was the first economist to estimate the loss of economic efficiency due to

market power. Harberger found that

A) the loss of economic efficiency in the U.S. economy due to market power was less than 1

percent of the value of production.

B) because of the increase in the average size of firms since World War II, the loss of economic

efficiency has been relatively large, about 10 percent of the value of total production in the

United States.

C) although the number of monopolies was small, the large number of other non-competitive

firms in the United States resulted in a large loss of economic efficiency, about 20 percent of the

value of total production.

D) the loss of economic efficiency in the U.S. economy due to market power was small around

1973, about 1 percent of the value of production, but has since grown to about 10 percent.

14) Arnold Harberger was the first economist to estimate the loss of economic efficiency due to

market power. Since Harberger’s findings were published, other researchers have studied this

same issue. How do the results of these researchers compare to Harberger’s results?

A) The other researchers reached conclusions similar to Harberger’s; namely, the loss of

economic efficiency due to market power is about 10 percent of the value of production in the

United States.

B) The other researchers reached conclusions different from Harberger’s; namely, they found that

the loss of economic efficiency due to market power is only about 1 percent of the value of

production in the United States, much less than Harberger’s estimate.

C) The other researchers reached conclusions different from Harberger’s; namely, the loss of

economic efficiency due to market power is about 10 percent of the value of production in the

United States, significantly greater than Harberger’s estimate.

D) The other researchers reached conclusions similar to Harberger’s; namely, the loss of

economic efficiency due to market power is about 1 percent of the value of production in the

United States.

15) In evaluating the degree of economic efficiency in a market, we can state that the size of the

deadweight loss in a market will be smaller

A) the greater the difference between marginal cost and price.

B) the smaller the difference between marginal cost and average total cost.

C) the smaller the difference between marginal cost and price.

D) the greater the difference between marginal cost and average revenue.

16) The possibility that the economy may benefit from having market power, rather than being

very competitive, is closely identified with which famous economist?

A) Arnold Harberger

B) Joseph Schumpeter

C) Sergey Brin

D) Donald Turner

17) Some economists believe that the economy benefits from firms having market power. Which

of the following is an argument that has been made to support this position?

A) Large firms are better able than small firms to spend funds on research and development

required to develop new products.

B) Competition is very rare in the U.S. economy and few new products are produced by smaller,

competitive firms.

C) Research has shown that the deadweight loss from monopolies is a small percentage of the

value of production in the United States.

D) Large firms can afford to lobby the U.S. government in order to impose restrictions on

imports and reduce the outsourcing of jobs to other countries.

18) A profit-maximizing monopoly produces a lower output level than would be produced if the

industry was perfectly competitive.

19) If the market for a product begins as perfectly competitive and then becomes a monopoly,

there will be a reduction in economic efficiency and a deadweight loss.

20) Suppose a monopoly is producing its profit-maximizing output level. Now suppose the

government imposes a lump-sum tax on the monopoly, independent of its output. As a result the

monopolist will increase the price of its product to cover its higher cost.

21) Producers in perfect competition receive a smaller producer surplus than a monopoly

producer.