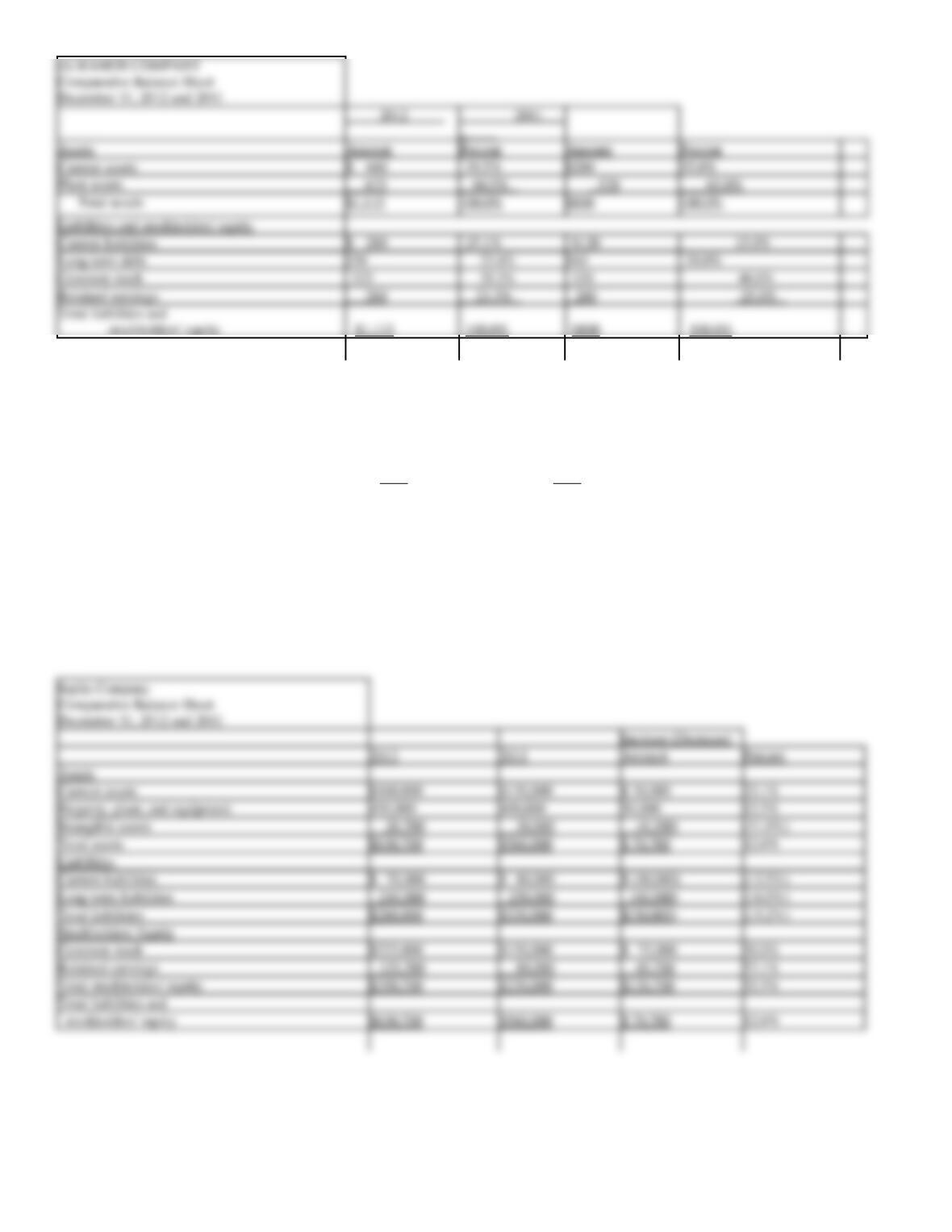

176. The comparative balance sheet of Ramos Company appears below:

(a) RAMOS COMPANY

Comparative Balance Sheet

December 31, 2012 and 2011

Assets

2012

2011

Current assets

$ 440

$280

Plant assets

675

520

Total assets

$1,115

$800

Liabilities and stockholders’ equity

Current liabilities

$ 280

$120

Long-term debt

250

160

Common stock

325

320

Retained earnings

260

200

Total liabilities and stockholders’ equity

$1,115

$800

Instructions

(a)

Using horizontal analysis, show the percentage change for each balance sheet item using 2011 as a base year.

(b)

Using vertical analysis, prepare a common size comparative balance sheet.

Round percentage to one decimal place.

Dec. 31,

Dec. 31,

Increase

(Decrease)

2012

2011

Amount

Percent

Plant assets

675

520

155

29.8%

Total assets

$1,115

$800

$315

39.4%

Current liabilities

$ 280

$120

$160

133.3%

Long-term debt

56.3%

Common stock

325

1.6%

Retained earnings

260

200

30.0%

177. Condensed data taken from the ledger of Joplin Company at December 31, 2012 and 2011, are as follows:

2012

2011

Current assets

$160,000

$130,000

Property, plant, and equipment

450,000

400,000

Intangible assets

20,700

30,000

Current liabilities

70,000

80,000

Long-term liabilities

210,000

250,000

Common stock

225,000

150,000

Retained earnings

125,700

80,000

Prepare a comparative balance sheet, with horizontal analysis, for December 31, 2012 and 2011. (Round percents to one decimal point.)

Increase (Decrease)

2012

2011

Amount

Percent

Assets

Current assets

$160,000

$130,000

$ 30,000

23.1%

Property, plant, and equipment

450,000

400,000

50,000

12.5%

Intangible assets

20,700

30,000

(9,300)

(31.0%)

Total assets

$630,700

$560,000

$ 70,700

12.6%

Liabilities

Current liabilities

$ 70,000

$ 80,000

$ (10,000)

(12.5%)

Long-term liabilities

210,000

250,000

(40,000)

(16.0%)

Total liabilities

$280,000

$330,000

$(50,000)

(15.2%)

Stockholders’ Equity

Common stock

$225,000

$150,000

$ 75,000

50.0%

Retained earnings

125,700

80,000

45,700

57.1%

Total stockholders’ equity

$350,700

$230,000

$120,700

52.5%

Total liabilities and

stockholders’ equity

$630,700

$560,000

$ 70,700

12.6%

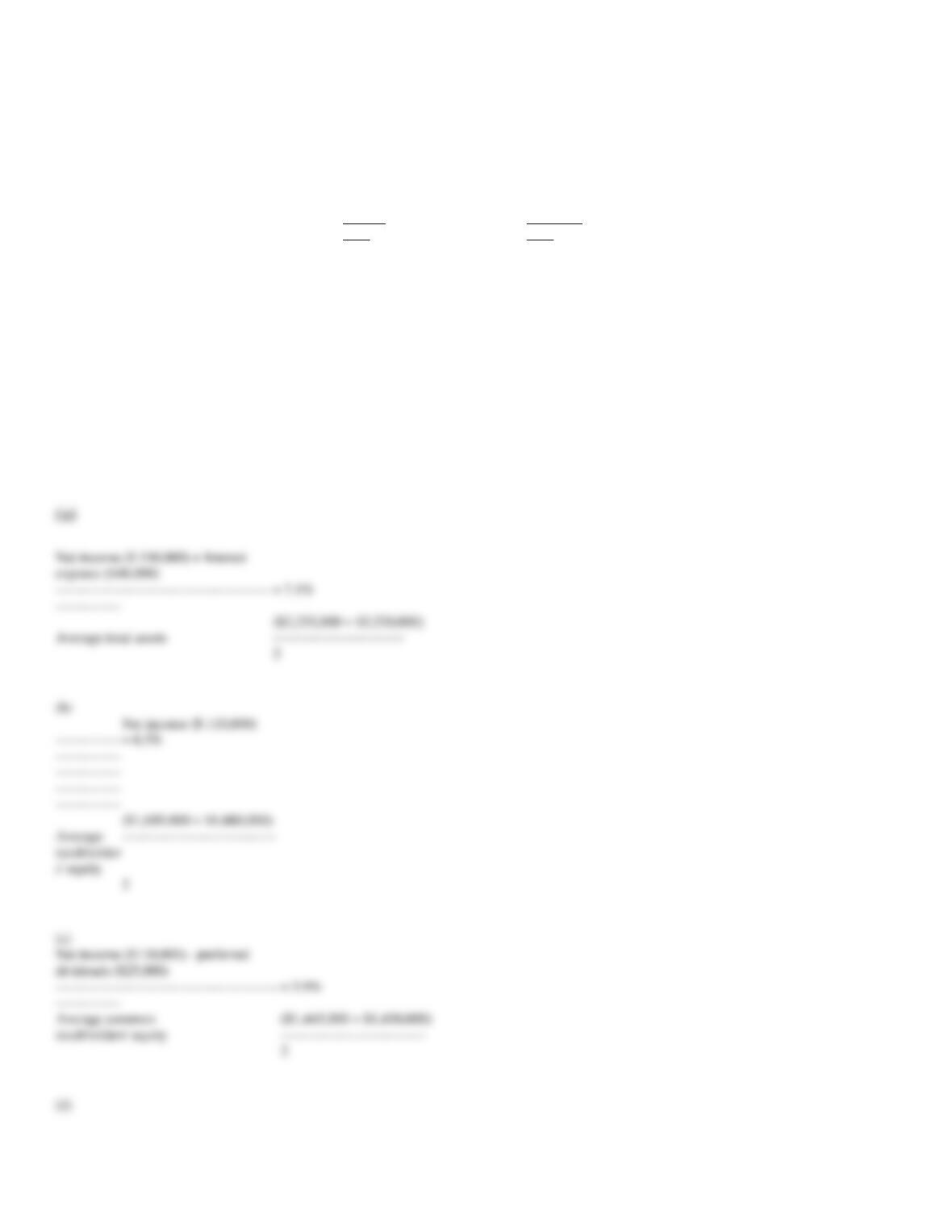

_

Assets

Amount

Percent

Amount

Percent

Current assets

$ 440

39.5%

$280

35.0%

Plant assets

675

60.5%

520

65.0%

Liabilities and stockholders’ equity

Current liabilities

$ 280

25.1%

$120

15.0%

Long-term debt

22.4%

20.0%

Common stock

29.2%

40.0%

Retained earnings

260

23.3%

200

25.0%

178. Revenue and expense data for Martinez Company are as follows:

2012

2011

Administrative expenses

$37,000

$20,000

Cost of goods sold

350,000

320,000

Income tax

40,000

32,000

Net sales

800,000

700,000

Selling expenses

150,000

110,000

(a)

Prepare a comparative income statement, with vertical analysis, stating each item for both 2012 and 2011 as a percent of sales.

(b)

Comment upon significant changes disclosed by the comparative income statement.

Round percentage to one decimal place.

Amount

Percent

Amount

Percent

Net sales

$800,000

100.0%

$700,000

100.0%

Cost of goods sold

350,000

43.8

320,000

45.7

Gross profit

$450,000

56.2%

$380,000

54.3%

Selling expenses

$150,000

18.8%

$110,000

15.7%

Administrative expenses

37,000

4.6

20,000

2.9

Total operating expenses

$187,000

23.4%

$130,000

18.6%

Income before income tax

$263,000

32.8%

$250,000

35.7%

Income tax

40,000

5.0

32,000

4.6

Net income

$223,000

27.8%

$218,000

31.1%

179. The following data are taken from the balance sheet at the end of the current year. Determine the (a)

working capital, (b) current ratio, and (c) quick ratio. Present figures used in your computations. Round ratios

to the nearest tenth.

Accounts payable

$245,000

Accounts receivable

210,000

Accrued liabilities

4,000

Cash

114,000

Income tax payable

10,000

Inventory

240,000

Temporary investments

350,000

Notes payable, short-term

85,000

Prepaid expenses

15,000

Property, plant, and equipment

375,000

180. The following data are taken from the financial statements:

Current

Preceding

Year

Year

Net sales

$3,600,000

$4,000,000

Cost of goods sold

2,000,000

2,700,000

Average inventory

332,000

328,000

Inventory, end of year

372,000

347,000

(a)

Determine for each year (1) the inventory turnover (Round answer to one decimal place) and (2) the number of days’ sales in inventory

(Round intermediate calculation to two decimal place and final answer to whole number).

(b)

Comment on the favorable and unfavorable trends revealed by the data.

Current

Preceding

Year

Year

(1)

Cost of goods sold / average inventory

6.0

8.2

(2)

Average inventory/average daily cost

of goods sold*

60.59

44.34

*Average daily cost of good sold

(Cost of goods sold 365 days)

(a)

Current assets ($929,000) – current liabilities ($344,000) = $585,000

(b)

Current assets ($929,000) / current liabilities ($344,000) = 2.7

(c)

Cash + temporary investments + accounts receivable ($674,000) / current liabilities ($344,000) = 2.0

181. The following data are taken from the financial statements:

Current

Preceding

Year

Year

Average accounts receivable (net)

$123,000

$ 95,000

Accounts receivable (net), end of year

129,012

87,516

Net sales on account

950,000

825,000

(a)

Assuming that credit terms on all sales are n/45, determine for each year (1) the accounts receivable turnover and (2) the number of

days’ sales in receivables.

Round intermediate calculation to whole number and final answer to two decimal place.

(b)

Comment on any significant trends revealed by the data.

Current

Preceding

Year

Year

(1)

Net sales on account/average

accounts receivable (net)

7.72

8.68

(2)

Average accounts receivable /

average daily sales on account **

47.25

42.04

** Current: $950,000 / 365 = $2,603

182. From the following data, determine for the current year the (a) rate earned on total assets, (b) rate earned

on stockholders’ equity, (c) rate earned on common stockholders’ equity, (d) earnings per share on common

stock, (e) price-earnings ratio on common stock, and (f) dividend yield on common stock. Assume that the

current market price per share of common stock is $25. (Present key figures used in your computations.)

Round percentage values to one decimal place, dollar values to two decimal places, and other ratios to one

decimal place.

Current

Year

Preceding

Year

Current assets

$ 745,000

$ 820,000

Property, plant, and equipment

1,510,000

1,400,000

Current liabilities

(non-interest-bearing)

160,000

140,000

Long-term liabilities, 12%

400,000

400,000

Preferred 10% stock

250,000

250,000

Common stock, $25 par

1,200,000

1,200,000

Retained earnings:

Beginning of year

230,000

160,000

Net income for year

110,000

155,000

Preferred dividends declared

(25,000)

(25,000)

Common dividends declared

(70,000)

(60,000)

= 7.1%

($2,255,000 + $2,220,000)

Average total assets

2

Net income ($ 110,000)

($1,695,000 + $1,680,000)

2

= 5.9%

Average common

($1,445,000 + $1,430,000)

stockholders’ equity

2

183. The following information has been condensed from the December 31 balance sheets of Hanson Co.:

2012

2011

Assets:

Current assets

$ 825,500

$ 674,300

Fixed assets (net)

1,473,600

1,275,300

Total assets

$2,299,100

$1,949,600

Liabilities:

Current liabilities

$ 313,500

$ 309,600

Long-term liabilities

703,000

545,000

Total liabilities

$1,016,500

$ 854,600

Stockholders’ equity

$1,282,600

$1,095,000

Total liabilities and

stockholders’ equity

$2,299,100

$1,949,600

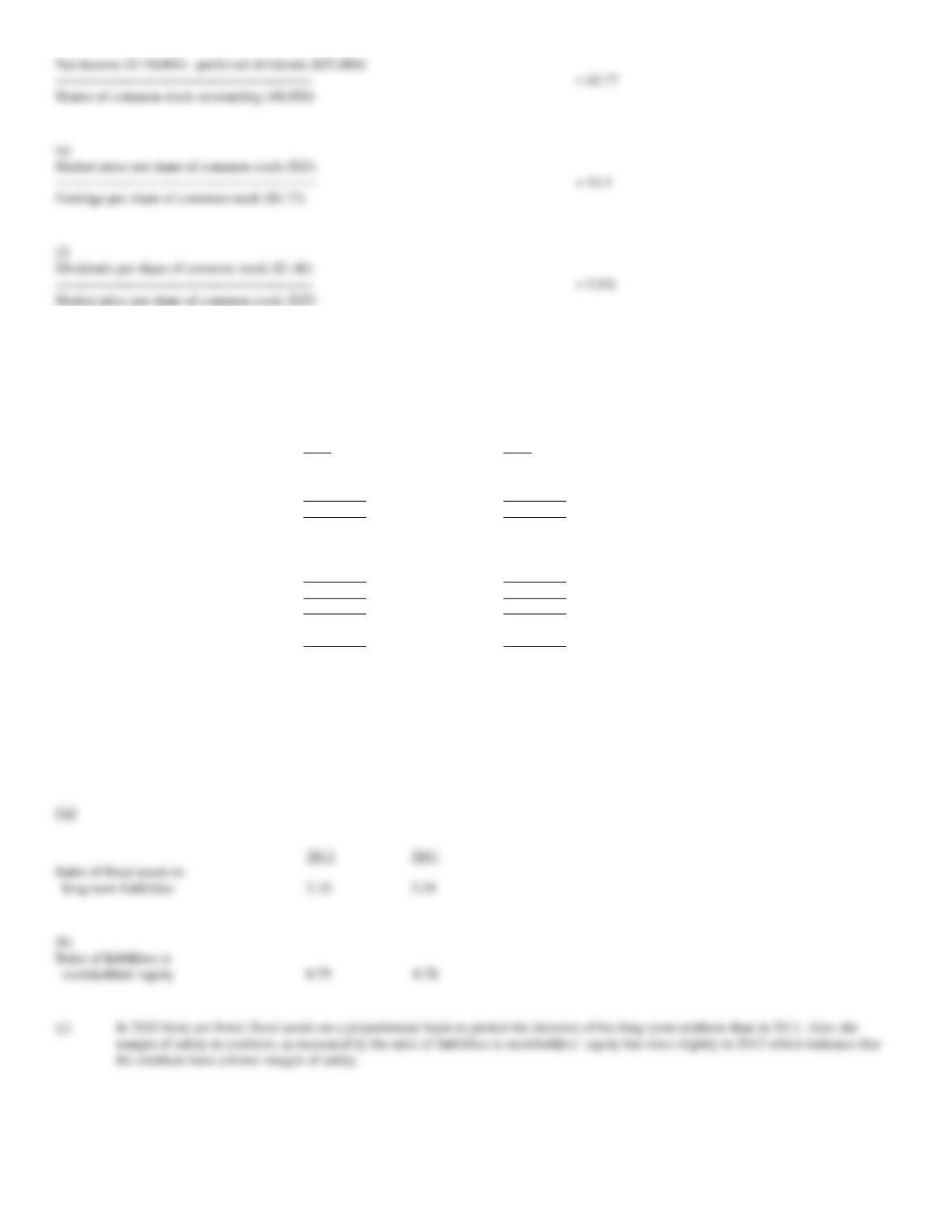

(a)

Determine the ratio of fixed assets to long-term liabilities for 2012 and 2011.

(b)

Determine the ratio of liabilities to stockholders’ equity for 2012 and 2011.

(c)

Comment on the year-to-year changes for both ratios.

Round your answers to two decimal place.

2012

2011

Ratio of fixed assets to

long-term liabilities

2.10

2.34

Ratio of liabilities to

stockholders’ equity

0.79

0.78

Net income ($110,000) – preferred dividends ($25,000)

= $1.77

Shares of common stock outstanding (48,000)

Market price per share of common stock ($25)

= 14.1

Earnings per share of common stock ($1.77)

Dividends per share of common stock ($1.46)

= 5.8%

Market price per share of common stock ($25)

184. A company reports the following:

Net income

$275,000

Preferred dividends

$30,000

Average stockholders’ equity

$1,000,000

Average common stockholders’ equity

$700,000

Determine the (a) rate earned on stockholders’ equity, and (b) rate earned on common stockholders’ equity. Round your answer to one decimal

place.

Rate earned on stockholders’ equity = Net income / Average stockholders’ equity

Rate earned on stockholders’ equity = $275,000 / $1,000,000

Rate earned on stockholders’ equity = 27.5%

Rate earned on common stockholders’ equity = (Net income – preferred dividends) /

Average common stockholders’ equity

Rate earned on common stockholders’ equity = ($275,000 – $30,000) / $700,000

Rate earned on common stockholders’ equity = 35%

185. Selected data from the Carmen Company at year end are presented below:

Total assets

$2,000,000

Average total assets

2,200,000

Net income

250,000

Net sales

1,300,000

Average common stockholders’ equity

1,000,000

Net cash provided by operating activities

275,000

Shares of common stock outstanding

10,000

Instructions

Calculate the profitability ratios that can be computed from the above information.Assume the company had no preferred stock or interest expense.

Round percentage value to one decimal place and dollar value to zero decimal place.

With the information provided, the profitability ratios that can be calculated are as follows:

Net sales Average total assets

$1,300,000 $2,200,000

=

59.1%

(Net income + Interest expense) Average total assets

$250,000 + 0 $2,200,000

=

11.4%

stockholders’ equity

=

Earnings per share on

=

$25 per share

186. Prepare an Income Statement using the following data for Young Adventures for the year ended December

31, 2012:

Net Sales

$24,500,000

Cost of Merchandise Sold

10,900,000

Operating Expenses

6,300,000

Losses from Asset Impairment

2,800,000

Income Tax Expense

500,000

Loss on Discontinued Operations

100,000

Net Loss on Extraordinary Item

125,000

Net Sales

$24,500,000

Cost of Merchandise Sold

10,900,000

Gross Profit

13,600,000

Operating Expenses

$6,300,000

Losses from Asset Impairment

2,800,000

9,100,000

Income from Continuing Operations

$4,500,000

Before Income Tax

Income Tax Expense

500,000

Income from Continuing Operations

$4,000,000

Loss on Discontinued Operations

100,000

Income before Extraordinary Expense

$3,900,000

Net Loss on Extraordinary Item

125,000

Net Income

$3,775,000

187. From the following data for Norton Company for the year ended December 31, 2012 prepare a multiple-

step income statement. Show parenthetically earnings per share for the following: income from continuing

operations, loss on discontinued operations (less applicable income tax), income before extraordinary item,

extraordinary item (less applicable income tax), and net income.

Common stock, $50 par

$200,000

Cost of merchandise sold

342,000

Administrative expenses

48,250

Income tax (applicable to continuing operations)

142,000

Interest expense

3,750

Loss on discontinued operations,

net of applicable tax of $2,700

5,400

Sales

865,000

Selling expenses

83,000

Uninsured flood loss, net of applicable

income tax of $4,500

14,000

Sales

$865,000

Cost of merchandise sold

342,000

Gross profit

$523,000

Operating expenses:

Selling expenses

$ 83,000

Administrative expenses

48,250

Total operating expenses

131,250

Income from operations

$391,750

Interest expense

3,750

Income from continuing operations

before income tax

$388,000

Income tax expense

142,000

Income from continuing operations

$246,000

Loss on discontinued operations, net of

applicable income tax of $2,700

5,400

Income before extraordinary item

$240,600

Extraordinary item:

Uninsured flood loss, net of applicable

income tax of $4,500

14,000

Net income

$226,600

Earnings per common share:

Income from continuing operations

$61.50

Loss on discontinued operations

1.35

Income before extraordinary item

$60.15

Extraordinary item:

Uninsured flood loss

3.50

Net Income

$56.65

188. Gallant Company reported net income of $2,500,000. The income statement included one extraordinary

item: a $500,000 gain from condemnation of land and a $200,000 loss on discontinued operations, both after

applicable income tax.

There were 100,000 shares of $10 par common stock and 40,000 shares 4% preferred stock of $100 par

outstanding throughout the current year.

Required: Prepare the earnings per share section of Gallant Company’s income statement.