Page 1

1.

Which of the following industries is MOST likely to be monopolistically competitive?

A)

automobile production

B)

fresh bagel shops

C)

corn farming

D)

electric utility production

2.

A monopolistically competitive industry, such as corn snack chips, and a perfectly

competitive industry, like wheat farming, are alike in that:

A)

firms in both types of industries produce identical products.

B)

firms in both types of industries produce similar but not identical products.

C)

barriers to entry in both industries are large.

D)

there are many firms in each industry.

3.

Monopolistic competition is characterized by:

A)

free entry and exit in the long run.

B)

each firm producing a standardized product.

C)

few producers.

D)

barriers to entry.

4.

In monopolistic competition, each firm:

A)

is a price taker.

B)

has some ability to set the price of its differentiated good.

C)

will set price equal to marginal cost.

D)

has marginal revenue that is greater than price.

5.

The wedding dress industry is monopolistically competitive. As a result:

A)

thousands of dress suppliers all sell identical products.

B)

dresses tend to be differentiated among the many sellers serving this market.

C)

it has freedom of entry but not exit.

D)

prices tend to be lower than if the dress industry approximated perfect competition.

6.

Monopolistic competition is similar to perfect competition because firms in both market

structures:

A)

are price takers.

B)

produce goods that are perfect substitutes.

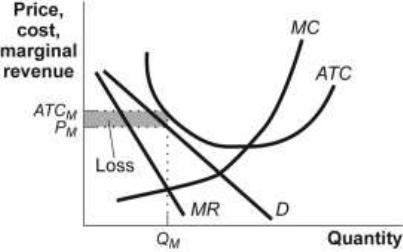

C)

find it beneficial to advertise.

D)

do not face any barriers to entry to the industry in the long run.

Page 2

7.

In monopolistic competition:

A)

firms earn zero economic profits in the long run.

B)

each firm produces a product identical to that of every other firm in the industry.

C)

firms are aware of their strategic interdependence.

D)

firms earn large economic profits in the long run.

8.

For the monopolistically competitive wild-caught seafood market, the demand curve for

any individual firm is _____, and there are _____ producers of seafood.

A)

downward-sloping; few

B)

upward-sloping; many

C)

vertical; few

D)

downward-sloping; many

9.

The downward-sloping demand curve for a monopolistically competitive firm:

A)

reflects product differentiation.

B)

eventually will become perfectly elastic as more firms enter.

C)

indicates collusion among firms in the industry.

D)

ensures that the firm will produce at minimum average cost in the long run.

10.

An industry characterized by many firms producing similar but differentiated products

in a market with easy entry and exit is called:

A)

perfectly competitive.

B)

monopolistic.

C)

monopolistically competitive.

D)

oligopolistic.

11.

An example of monopolistic competition is the _____ industry.

A)

restaurant

B)

soft-drink

C)

automobile

D)

airline

12.

A(n) _____ is a single firm with _____, whereas a(n) _____ implies an industry with

_____ firm(s) and _____.

A)

oligopoly; no barriers to entry; monopoly; many; easy entry and exit

B)

monopoly; barriers to entry; monopolistic competition; many; easy entry and exit

C)

monopoly; barriers to entry; oligopoly; few; no barriers to entry

D)

monopolistic competitor; barriers to entry; monopoly; one; barriers to entry

Page 3

13.

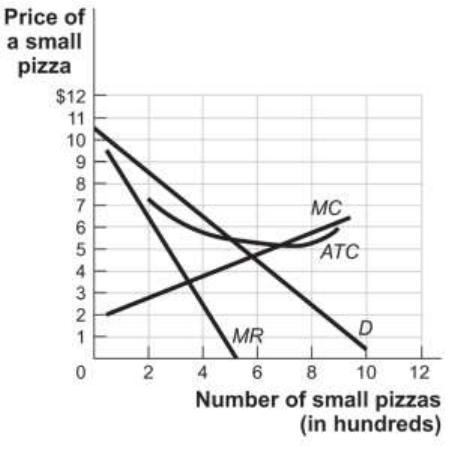

In large shopping malls, the retail clothing market is most illustrative of:

A)

monopolistic competition.

B)

monopoly.

C)

perfect competition.

D)

perfect oligopoly.

14.

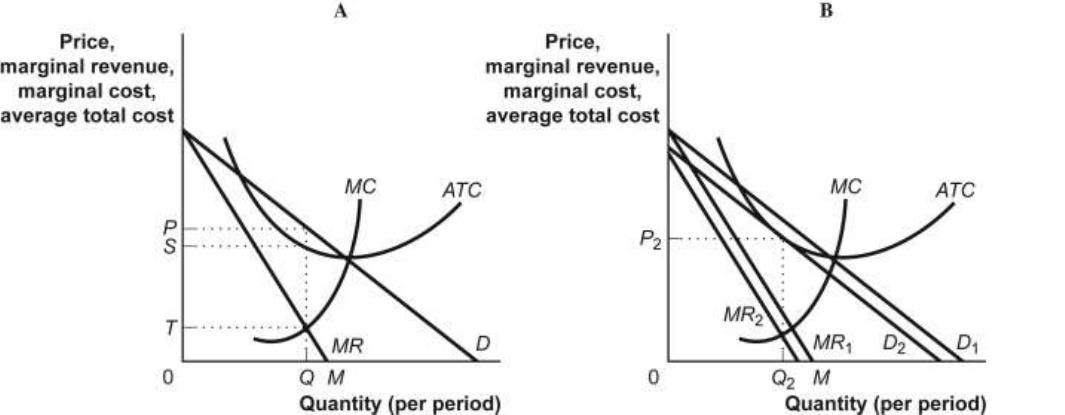

An industry with a large number of relatively small firms producing differentiated

products in a market with easy entry and exit of firms is:

A)

a monopoly.

B)

a duopoly.

C)

an oligopoly.

D)

monopolistically competitive.

15.

A monopolistically competitive industry is characterized by a _____ number of firms

producing _____ products; it has _____ entry.

A)

small; identical; barriers to

B)

small; similar; relatively easy

C)

large; similar; relatively easy

D)

large; identical; relatively easy

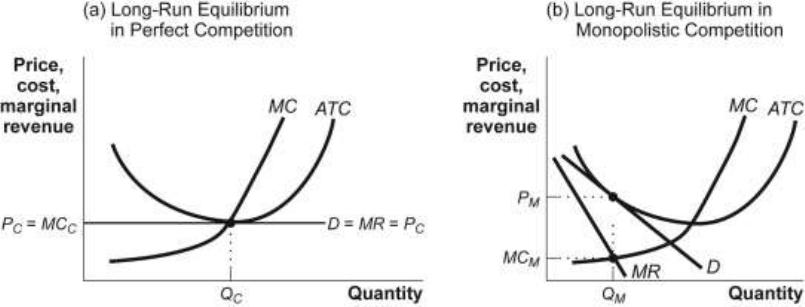

16.

Monopolistic competition is an industry structure characterized by:

A)

a product with no close substitutes.

B)

a horizontal demand curve.

C)

a large number of firms.

D)

barriers to entry and exit.

17.

Because most communities have a large number of similar but not identical substitutes,

the market for chiropractors is best considered to be:

A)

an oligopoly.

B)

perfect competition.

C)

monopolistically competitive.

D)

a monopoly.

18.

Because most communities have a large number of similar but not identical substitutes,

the market for financial planners is best considered to be:

A)

a monopoly.

B)

an oligopoly.

C)

perfect competition.

D)

monopolistically competitive.

Page 4

19.

A feature of monopolistic competition that makes it different from monopoly is the:

A)

fact that firms in monopolistically competitive industries follow the marginal

decision rule, while monopolies do not.

B)

downward-sloping demand curve.

C)

downward-sloping marginal revenue curve.

D)

number of firms in the industry.

20.

An industry characterized by many competitors, each producing identical products, with

free entry and exit, is described as:

A)

monopolistically competitive.

B)

oligopolistic.

C)

perfectly competitive.

D)

monopolistic.

21.

Which of the following is NOT a characteristic of monopolistic competition?

A)

product differentiation

B)

lack of barriers to entry and exit in the long run

C)

many competing producers

D)

tacit collusion

22.

Which of the following describes a feature shared by monopolistic competition and

perfect competition?

A)

few firms in the industry

B)

no barriers to entry or exit in the long run

C)

absolute market power

D)

standardized products

23.

A common example of monopolistic competition is the market for:

A)

oranges.

B)

1-inch nails.

C)

automobiles.

D)

gas stations.

24.

An industry with a large number of relatively small firms producing _____ in a market

with easy entry and exit is a(n) _____.

A)

similar products; monopoly

B)

identical products; monopolistic competition

C)

differentiated products; oligopoly

D)

differentiated products; monopolistic competition

Page 5

25.

Monopolistic competition describes an industry characterized by a _____ number of

firms producing _____ products with _____ entry.

A)

small; identical; barriers to

B)

small; similar; relatively easy

C)

large; similar; relatively easy

D)

large; identical; relatively easy

26.

The market for dentists in most communities can be considered _____ because the

market has a large number of similar but not identical dental services.

A)

monopolistic competition

B)

a monopoly

C)

perfect competition

D)

an oligopoly

27.

Monopolistic competition describes an industry characterized by:

A)

a product with many close substitutes.

B)

a horizontal demand curve.

C)

a small number of firms.

D)

barriers to entry and exit.

28.

Monopolistic competition is different from monopoly because firms:

A)

have some power to set prices.

B)

have a downward-sloping demand curve.

C)

face some competition.

D)

have a downward-sloping marginal revenue curve.

29.

Because most communities have a large number of similar but not identical substitutes,

the market for florists is best considered:

A)

a monopoly.

B)

an oligopoly.

C)

monopolistically competitive.

D)

perfectly competitive.

30.

Monopolistic competition describes an industry characterized by:

A)

a product with no close substitutes.

B)

many firms, each with some market power.

C)

a small number of firms.

D)

barriers to entry and exit.

Page 6

31.

An industry with easy entry and exit of a large number of small firms producing a

standardized product is:

A)

in perfect competition.

B)

in monopolistic competition.

C)

an oligopoly.

D)

a monopoly.

32.

Because of the lack of substitutes, the market for newly developed brand-name

prescription drugs is best considered to be:

A)

perfect competition.

B)

monopolistic competition.

C)

oligopoly.

D)

monopoly.

33.

An industry with a few interdependent firms is best described as an example of:

A)

perfect competition.

B)

monopolistic competition.

C)

oligopoly.

D)

monopoly.

34.

The market for grade A large eggs in California is best considered to be an example of:

A)

perfect competition.

B)

monopolistic competition.

C)

oligopoly.

D)

monopoly.

35.

An industry with a single firm producing a product for which there are no close

substitutes and which is protected by barriers to entry is an example of:

A)

perfect competition.

B)

monopolistic competition.

C)

oligopoly.

D)

monopoly.

36.

The market for soft drinks, which is dominated by Coca Cola and Pepsi, is best

considered to be an example of:

A)

perfect competition.

B)

monopolistic competition.

C)

oligopoly.

D)

monopoly.

Page 7

37.

If the toothpaste market is monopolistically competitive, product differentiation may

take the form of:

A)

production of many varieties of toothpaste, including those with whitening agents.

B)

differentiation in the locations where certain toothpastes are available.

C)

quality differences among the various brands.

D)

production of many varieties of toothpaste, including those with whitening agents;

differentiation in the locations where certain toothpastes are available; and quality

differences among the various brands.

38.

In many cities you can stay at a Holiday Inn in the downtown area, in a suburban

community, or near the airport. These Holiday Inn establishments are examples of

product differentiation by:

A)

type.

B)

location.

C)

quality.

D)

style.

39.

Many customers will walk right past a diner that serves coffee and go to Starbucks,

where they pay more for a cup of java. For these customers, coffee is differentiated by:

A)

style.

B)

location.

C)

quality.

D)

type.

40.

The sources of product differentiation do NOT include:

A)

differences in location.

B)

differences in quality.

C)

the perception by consumers that products are different, even if they are physically

identical.

D)

consumers’ value in uniformity.

41.

Which of the following is NOT a source of product differentiation?

A)

price

B)

location

C)

style

D)

quality

Page 8

42.

Firms in monopolistic competition can acquire some market power by:

A)

using price competition.

B)

engaging in tacit collusion.

C)

differentiating the product.

D)

increasing their output to the perfectly competitive level.

43.

When initially a monopolistically competitive industry earns economic profit, the result

of competition among sellers is usually that:

A)

the price of the product increases to monopoly level.

B)

the price of the product quickly reaches the perfectly competitive level.

C)

firms in the industry gain market share.

D)

firms in the industry lose market share.

44.

Since a monopolistically competitive firm faces a downward-sloping demand curve, its

price will be _____ revenue.

A)

equal to marginal

B)

less than marginal

C)

greater than marginal

D)

equal to total

45.

The demand curve for a firm operating in a monopolistically competitive industry is:

A)

U-shaped.

B)

upward-sloping.

C)

downward-sloping.

D)

vertical.

46.

The demand curve for a firm in monopolistic competition is _____ facing a perfectly

competitive firm.

A)

downward-sloping, unlike the horizontal demand curve

B)

horizontal, unlike the downward-sloping demand curve

C)

horizontal, the same as that

D)

downward-sloping, the same as that

47.

The profit-maximizing rule MC = MR is followed by firms operating in:

A)

monopolistic competition but not perfect competition.

B)

perfect competition but not monopolistic competition.

C)

either monopolistic competition or perfect competition, depending on the costs of

production.

D)

both monopolistic competition and perfect competition.

Page 9

48.

Product differentiation under monopolistic competition means that each firm:

A)

charges the same price.

B)

maximizes profit where MC = P.

C)

faces a downward-sloping demand curve.

D)

always receives economic profits.

49.

Product differentiation under monopolistic competition means that each firm:

A)

charges a slightly different price.

B)

has a pure monopoly.

C)

maximizes profit where MC = P.

D)

faces a horizontal demand curve.

50.

In a monopolistically competitive industry:

A)

a firm maximizes profits when MR = MC yet P > MC.

B)

people would be better off if output were reduced.

C)

output could be increased without an increase in total cost.

D)

to maximize profits, firms set MR = MC, and people would be better off if output

were reduced.

51.

A monopolistically competitive firm has a downward-sloping demand curve for its

product, primarily because:

A)

there are no barriers to entry or exit in the long run.

B)

there are many sellers in the industry.

C)

its product is differentiated.

D)

the price is greater than the marginal revenue.

52.

The demand curve for a firm operating in a monopolistically competitive market is best

described as:

A)

U-shaped.

B)

upward-sloping.

C)

downward-sloping.

D)

horizontal.

53.

The _____ demand curve for a firm operating in a monopolistically competitive market

_____ facing a perfectly competitive firm.

A)

downward-sloping; is the same as the demand curve

B)

downward-sloping; differs from the horizontal demand curve

C)

horizontal; differs from the downward-sloping demand curve

D)

horizontal; is the same as the demand curve

Page 10

54.

If a monopolistically competitive firm is producing the profit-maximizing level of

output and is earning an economic profit in the short run:

A)

price is less than average total costs.

B)

price is less than marginal cost.

C)

marginal revenue is less than marginal cost.

D)

marginal revenue equals marginal cost.

55.

Suppose a monopolistically competitive firm is making a profit, but it can increase its

profits by increasing output. At the current level of output:

A)

marginal revenue is greater than marginal cost.

B)

price is less than marginal cost.

C)

price is less than average total cost.

D)

marginal revenue is less than marginal cost.

56.

Suppose Susan owns a business that operates in a market characterized by monopolistic

competition. Susan’s profit-maximizing price is $12, her profit-maximizing output is

900 units per week, and her profits are $1,800 per week. Susan decides that she needs

more profits and therefore raises her price to $15. At the new price of $15:

A)

profits will increase.

B)

profits will remain at $1,800.

C)

marginal revenue will be greater than marginal cost.

D)

marginal revenue will be less than marginal cost.

57.

Suppose a monopolistically competitive firm can increase its profits by decreasing its

output. At the current output:

A)

marginal revenue is less than zero.

B)

price is less than marginal revenue.

C)

marginal revenue is less than marginal cost.

D)

price is less than average total cost.

58.

To maximize profit, a monopolistically competitive firm should produce the level of

output at which:

A)

marginal revenue equals marginal cost.

B)

price equals marginal cost.

C)

price equals total cost.

D)

marginal revenue equals price.

Page 11

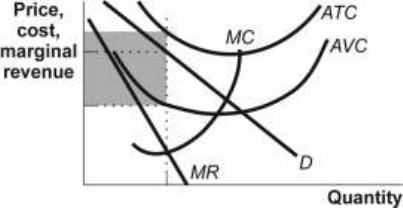

Use the following to answer question 59:

Figure: Monopolistic Competition

59.

(Figure: Monopolistic Competition) The firm in the figure Monopolistic Competition is

producing at the output level that maximizes profits (minimizes losses). The shaded

rectangle depicts the level of:

A)

profit.

B)

loss.

C)

fixed cost.

D)

variable cost.

60.

The price for a firm under monopolistic competition is _____ revenue.

A)

equal to marginal

B)

greater than marginal

C)

less than marginal

D)

greater than total

61.

A firm in monopolistic competition maximizes its profit by producing so that:

A)

MC = ATC.

B)

MC = AR.

C)

MC = MR.

D)

MC = P.

62.

If a firm operating in monopolistic competition is producing a quantity that generates

MC > MR, then the marginal decision rule tells us that profit:

A)

can be increased by increasing production.

B)

can be increased by decreasing production.

C)

can be increased by decreasing the price.

D)

is maximized only if MC = P.

Page 12

63.

If a firm operating in monopolistic competition is producing a quantity that generates

MC < MR, then the marginal decision rule tells us that profit:

A)

can be increased by increasing production.

B)

can be increased by decreasing production.

C)

can be increased by increasing the price.

D)

is maximized only if MC = P.

64.

If a firm operating in monopolistic competition is producing a quantity that generates

MC = MR, then the marginal decision rule tells us that profit:

A)

is maximized.

B)

can be increased by decreasing production.

C)

can be increased by decreasing the price.

D)

is maximized only if MC = P.

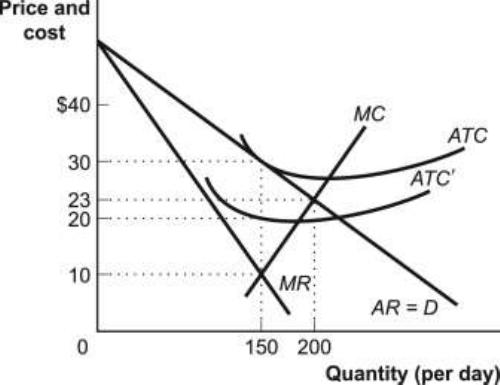

Use the following to answer questions 65-66:

Figure: Profit Maximization for a Firm in Monopolistic Competition

65.

(Figure: Profit Maximization for a Firm in Monopolistic Competition) Look at the

figure Profit Maximization for a Firm in Monopolistic Competition. Suppose that an

innovation reduces a firm’s costs from ATC to ATC. Before the innovation reduced the

cost, the firm’s maximum economic profit was:

A)

$0.

B)

$30.

C)

$750.

D)

$4,500.

Page 13

66.

(Figure: Profit Maximization for a Firm in Monopolistic Competition) Look at the

figure Profit Maximization for a Firm in Monopolistic Competition. Suppose that an

innovation reduces a firm’s costs from ATC to ATC. After the innovation reduces the

cost, the firm’s maximum economic profit is:

A)

$0.

B)

$30.

C)

$1,500.

D)

$3,000.

67.

In the short run, a monopolistically competitive firm produces at the optimal level of

output and is earning positive economic profits. Which of the following must be TRUE

for this firm?

A)

MR = MC and P = ATC.

B)

MR = MC and P > ATC.

C)

MR > MC and P = ATC.

D)

P = MR = MC > ATC.

68.

A monopolistically competitive firm is operating in the short run at the optimal level of

output and is earning negative economic profits. Which of the following must be

TRUE?

A)

ATC > P > MR = MC.

B)

ATC = P > MR = MC.

C)

ATC > P = MR = MC.

D)

ATC > P > MR > MC.

69.

A gas station operates in a monopolistically competitive market and is in short-run

equilibrium. Suppose that a fixed cost for this firm decreases. As a result, the firm’s

price will _____, the firm’s output will _____, and the firm’s economic profit will

_____.

A)

increase; increase; increase

B)

increase; increase; decrease

C)

stay the same; stay the same; increase

D)

decrease; stay the same; increase

70.

To maximize profits, a firm in monopolistic competition will likely produce so that

marginal cost:

A)

equals average total cost.

B)

is greater than marginal revenue.

C)

equals marginal revenue.

D)

equals price.

Page 14

71.

If a firm operating in monopolistic competition is producing a quantity at which _____,

then the marginal decision rule tells us that profit _____.

A)

MC > MR; can be increased by increasing production

B)

MC < MR; can be increased by decreasing production

C)

MC < MR; can be increased by increasing production

D)

MC > MR; is maximized

72.

If a firm operating in monopolistic competition is producing a quantity at which MC <

MR, then profit can be _____ by _____.

A)

increased; decreasing production

B)

increased; increasing production

C)

increased; increasing the price

D)

maximized; decreasing production

73.

A firm operating in a monopolistically competitive market is producing a quantity at

which MC = MR. Profit:

A)

can be increased by increasing production.

B)

is maximized.

C)

can be increased by decreasing the price.

D)

is maximized only if MC = P.

74.

If a monopolistically competitive firm is in long-run equilibrium, price:

A)

equals average total cost.

B)

equals marginal cost.

C)

equals marginal revenue.

D)

is greater than average total cost.

75.

In the long run, monopolistically competitive firms:

A)

produce at the level that minimizes average total cost.

B)

set marginal revenue equal to price.

C)

cannot earn an economic profit.

D)

produce so that marginal cost equals price.

76.

Monopolistically competitive firms have zero economic profits in the long run because

of:

A)

excess capacity.

B)

price wars among firms.

C)

easy entry and exit.

D)

excessive advertising.

Page 15

77.

Toby operates a small deli downtown. The deli industry is monopolistically competitive.

In the long run, Toby will produce where:

A)

marginal revenue equals marginal cost.

B)

price equals minimum average total cost.

C)

price equals marginal cost.

D)

price equals marginal revenue.

78.

Suppose the dry-cleaning market is monopolistically competitive and economically

profitable this year. In the long run, the demand for any one firm’s dry-cleaning services

will _____ as more firms enter the industry, causing economic profits to _____.

A)

decrease; become economic losses

B)

decrease; fall to zero

C)

not change; fall

D)

increase; increase

79.

If monopolistically competitive firms are earning positive economic profits in the short

run, then in the long run:

A)

firms will leave the industry.

B)

the demand curves faced by existing firms will move to the right.

C)

economic profits will increase.

D)

economic profits will be reduced to zero.

80.

When a monopolistically competitive firm is making zero economic profits, it is

producing so that the average total cost curve is tangent to the demand curve. At this

output:

A)

the firm is maximizing profits, and marginal cost must equal marginal revenue.

B)

the firm is not maximizing profits, and a slight increase or decrease in output will

lead to positive profits.

C)

since economic profits are zero, the condition that marginal revenue equals

marginal cost is irrelevant.

D)

the condition that marginal revenue equals marginal cost continues to be relevant,

but the marginal revenue and marginal cost curves need not intersect directly below

the point of tangency between the average total cost curve and the demand curve.

81.

Toby operates a small deli downtown. The deli industry is monopolistically competitive.

If some delis leave the industry, Toby’s _____ curve will shift to the _____.

A)

marginal cost; left

B)

marginal cost; right

C)

demand; left

D)

demand; right

Page 16

82.

In monopolistic competition:

A)

firms may advertise to increase demand for their product.

B)

entry of new firms shifts the demand curve for existing firms to the right.

C)

when some firms exit, the demand curve for the firms that remain in the industry

shifts to the left.

D)

firms earn large economic profits in the long run.

83.

The model of monopolistic competition characterizes the market for plumbing services

in a city. Suppose that the market is in long-run equilibrium. For a typical plumbing

firm, price:

A)

equals average total cost.

B)

exceeds average total cost.

C)

is less than average total cost.

D)

is greater than the average for all other firms in the market.

84.

The model of monopolistic competition characterizes the market for plumbing services

in a city. This market is initially in long-run equilibrium, but then there is an increase in

market demand for plumbing services. We expect that in the long run:

A)

firms will leave the plumbing market.

B)

there will be a short-run increase in the number of firms, but then the number will

return to the original level.

C)

new firms will enter the plumbing market.

D)

firms will shut down, but they will not leave the industry.

85.

In the long run, monopolistically competitive firms tend to have:

A)

high economic profits.

B)

zero economic profits.

C)

negative economic profits.

D)

substantial economic losses.

86.

In the long run, if a monopolistically competitive firm produces the optimal level of

output:

A)

P = ATC = MR = MC.

B)

P > ATC > MR = MC.

C)

P = ATC > MR > MC.

D)

P = ATC > MR = MC.

Page 17

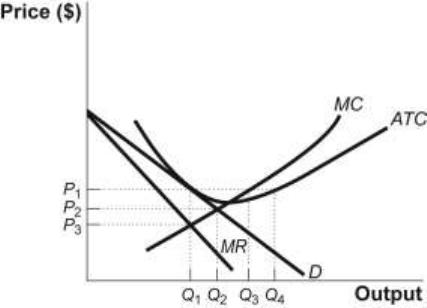

Use the following to answer question 87:

Figure: Possible Long-Run Outcome

87.

(Figure: Possible Long-Run Outcome) In the figure Possible Long-Run Outcome, which

price and quantity refer to a potential long-run profit maximizing outcome for a firm

producing in a monopolistically competitive market?

A)

P1 and Q3

B)

P1 and Q1

C)

P2 and Q2

D)

P1 and Q4

88.

In the short run, a monopolistically competitive firm produces at the optimal level of

output and is earning positive economic profits. In the long run, the _____ of firms

shifts the firm’s demand and marginal revenue curves _____ the firm’s level of output

and _____ the price it can charge until price equals average total cost.

A)

entry; leftward, decreasing; decreasing

B)

entry; leftward, decreasing; increasing

C)

entry; downward, decreasing; decreasing

D)

exit; rightward, increasing; increasing

89.

In a long-run equilibrium, firms in a monopolistically competitive industry sell at a

price:

A)

equal to marginal cost.

B)

less than marginal cost.

C)

greater than marginal cost.

D)

less than marginal revenue.

Page 18

90.

General Snacks is a typical firm in monopolistic competition. If the market is in

long-run equilibrium, then the price General Snacks charges for its snack goods:

A)

equals average total cost.

B)

exceeds average total cost.

C)

is less than average total cost.

D)

is more than the average for all other firms in the market.

91.

General Snacks is a typical firm in monopolistic competition. Initially, the market is in

long-run equilibrium, and then there is an increase in the market demand for snacks. In

the long run, the economic profits of typical firms in the industry will be:

A)

typical of those earned by monopoly firms.

B)

positive but less than the level typically earned by monopoly firms.

C)

zero.

D)

negative.

92.

In the long run, monopolistically competitive firms:

A)

always earn high economic profits.

B)

tend to earn zero economic profits.

C)

usually incur negative economic profits.

D)

usually incur substantial economic losses.

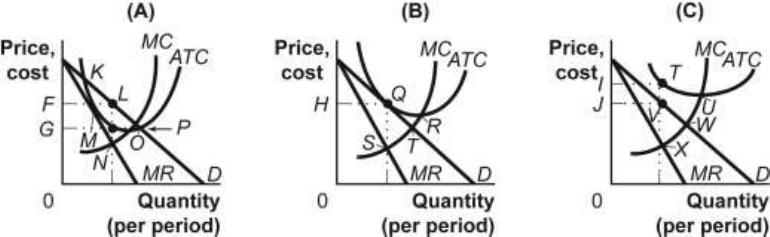

Use the following to answer questions 93-101:

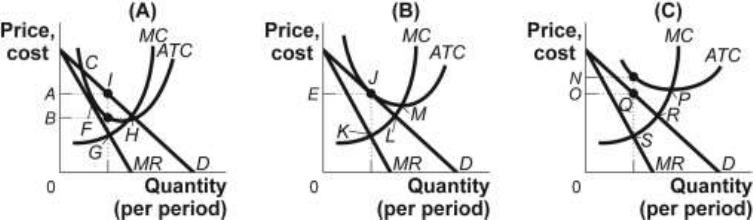

Figure: Firms in Monopolistic Competition

93.

(Figure: Firms in Monopolistic Competition) In panel (A) of the figure Firms in

Monopolistic Competition, the profit-maximizing quantity of output is determined by

the intersection at point:

A)

K.

B)

P.

C)

N.

D)

O.

Page 19

94.

(Figure: Firms in Monopolistic Competition) In panel (B) of the figure Firms in

Monopolistic Competition, the profit-maximizing quantity of output is determined by

the intersection at point:

A)

Q.

B)

R.

C)

S.

D)

T.

95.

(Figure: Firms in Monopolistic Competition) In panel (C) of the figure Firms in

Monopolistic Competition, the profit-maximizing quantity of output is determined by

the intersection at point:

A)

U.

B)

V.

C)

W.

D)

X.

96.

(Figure: Firms in Monopolistic Competition) In panel (A) of the figure Firms in

Monopolistic Competition, economic profit per unit is:

A)

KL.

B)

LO.

C)

MN.

D)

NO.

97.

(Figure: Firms in Monopolistic Competition) In panel (C) of the figure Firms in

Monopolistic Competition, economic loss per unit is:

A)

XT.

B)

UW.

C)

VW.

D)

VT.

98.

(Figure: Firms in Monopolistic Competition) Look at the figure Firms in Monopolistic

Competition. A positive economic profit will be earned if the profit-maximizing price is

_____ in panel _____.

A)

F; (A)

B)

G; (A)

C)

H; (B)

D)

I; (C)

Page 20

99.

(Figure: Firms in Monopolistic Competition) Look at the figure Firms in Monopolistic

Competition. Zero economic profit will be earned if the profit-maximizing price is

_____ in panel _____.

A)

F; (A)

B)

G; (A)

C)

H; (B)

D)

I; (C)

100.

(Figure: Firms in Monopolistic Competition) Look at the figure Firms in Monopolistic

Competition. There will be a negative economic profit (or an economic loss) earned at

the profit-maximizing price _____ in panel _____.

A)

G; (A)

B)

H; (B)

C)

I; (C)

D)

J; (C)

101.

(Figure: Firms in Monopolistic Competition) Look at the figure Firms in Monopolistic

Competition. A long-run equilibrium is illustrated at the profit-maximizing price _____

in panel _____.

A)

F; (A)

B)

G; (A)

C)

H; (B)

D)

I; (C)

Use the following to answer questions 102-108:

Figure: Profits in Monopolistic Competition

Page 21

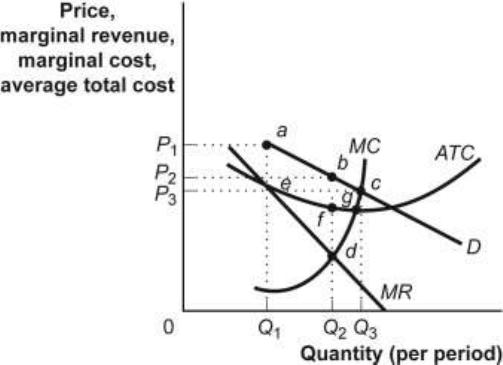

102.

(Figure: Profits in Monopolistic Competition) In panel (A) of the figure Profits in

Monopolistic Competition, the profit-maximizing quantity of output is determined by

the intersection at point:

A)

G.

B)

F.

C)

H.

D)

C.

103.

(Figure: Profits in Monopolistic Competition) In panel (B) of the figure Profits in

Monopolistic Competition, the profit-maximizing quantity of output is determined by

the intersection at point:

A)

J.

B)

K.

C)

L.

D)

M.

104.

(Figure: Profits in Monopolistic Competition) In panel (C) of the figure Profits in

Monopolistic Competition, the profit-maximizing quantity of output is determined by

the intersection at point:

A)

P.

B)

S.

C)

R.

D)

Q.

105.

(Figure: Profits in Monopolistic Competition) Look at the figure Profits in Monopolistic

Competition. A positive economic profit is earned if the profit-maximizing price is

_____ in panel _____.

A)

E; (B)

B)

B; (A)

C)

A; (A)

D)

N; (C)

106.

(Figure: Profits in Monopolistic Competition) Look at the figure Profits in Monopolistic

Competition. A zero economic profit is earned if the profit-maximizing price is _____ in

panel _____.

A)

A; (A)

B)

B; (A)

C)

N; (C)

D)

E; (B)

Page 22

107.

(Figure: Profits in Monopolistic Competition) Look at the figure Profits in Monopolistic

Competition. A negative economic profit (or economic loss) is earned if the

profit-maximizing price is _____ in panel _____.

A)

E; (B)

B)

B; (A)

C)

N; (C)

D)

O; (C)

108.

(Figure: Profits in Monopolistic Competition) Look at the figure Profits in Monopolistic

Competition. A long-run equilibrium is illustrated at the profit-maximizing price _____

in panel _____.

A)

A; (A)

B)

E; (B)

C)

B; (A)

D)

N; (C)

Use the following to answer questions 109-114:

Figure: The Restaurant Market

109.

(Figure: The Restaurant Market) The figure The Restaurant Market shows curves facing

a typical restaurant. Assume that many firms, differentiated products, and easy entry and

exit characterize the restaurant industry. The restaurant shown here will maximize

profits at quantity:

A)

Q1.

B)

Q2.

C)

Q3.

D)

Not enough information is given to answer the question.

Page 23

110.

(Figure: The Restaurant Market) The figure The Restaurant Market shows curves facing

a typical restaurant. Assume that many firms, differentiated products, and easy entry and

exit characterize the restaurant market. For the restaurant shown here, the

profit-maximizing price is:

A)

P1.

B)

P2.

C)

P3.

D)

Not enough information is given to answer the question.

111.

(Figure: The Restaurant Market) The figure The Restaurant Market shows curves facing

a typical restaurant. Assume that many firms, differentiated products, and easy entry and

exit characterize the restaurant market. For the restaurant shown here, the profit per unit

is:

A)

ae.

B)

fd.

C)

bf.

D)

bd.

112.

(Figure: The Restaurant Market) The figure The Restaurant Market shows curves facing

a typical restaurant. Assume that many firms, differentiated products, and easy entry and

exit characterize the restaurant market. If the restaurant shown here were to raise its

price above the profit-maximizing price, its total revenue would:

A)

decrease.

B)

increase.

C)

not change.

D)

Not enough information is given to answer the question.

113.

(Figure: The Restaurant Market) The figure The Restaurant Market shows curves facing

a typical restaurant. Assume that many firms, differentiated products, and easy entry and

exit characterize the market. In the long run:

A)

restaurants will leave the market.

B)

restaurants will enter the market.

C)

restaurants will neither enter nor exit the market.

D)

Not enough information is given to answer the question.

Page 24

114.

(Figure: The Restaurant Market) The figure The Restaurant Market shows curves facing

a typical restaurant. Assume that many firms, differentiated products, and easy entry and

exit characterize the restaurant market. In long-run equilibrium, the economic profit

earned by the typical restaurant in the community will be:

A)

negative.

B)

zero.

C)

equal to the level shown in the figure.

D)

Not enough information is given to answer the question.

115.

The model of monopolistic competition characterizes a city’s market for plumbing

services. Suppose that the market is initially in long-run equilibrium, and then demand

for plumbing services increases. In the short run, plumbing services’ price will _____

and output will _____.

A)

fall; fall

B)

not change; not change

C)

rise; rise

D)

rise; fall

Use the following to answer questions 116-121:

Figure: The Market for Gas Stations

Page 25

116.

(Figure: The Market for Gas Stations) Look at the figure The Market for Gas Stations.

Assume that the market for gas stations is characterized by many firms, differentiated

products, easy entry, and easy exit. The typical gas station will maximize profits at a

quantity of:

A)

Q1.

B)

Q2.

C)

Q3.

D)

Not enough information is given to answer the question.

117.

(Figure: The Market for Gas Stations) Look at the figure The Market for Gas Stations.

Assume that the market for gas stations is characterized by many firms, differentiated

products, easy entry, and easy exit. For the typical gas station the profit-maximizing

price would be:

A)

P1.

B)

P2.

C)

P3.

D)

Not enough information is given to answer the question.

118.

(Figure: The Market for Gas Stations) The figure Market for Gas Stations shows curves

facing a typical gas station in a large town. The market is characterized by many firms,

differentiated products, easy entry, and easy exit. If the gas station shown here were to

raise its price above the profit-maximizing price, the outcome would be _____ in total

revenue.

A)

a reduction

B)

an increase

C)

no change

D)

Not enough information is given to answer the question.

119.

(Figure: The Market for Gas Stations) The figure The Market for Gas Stations shows

curves facing a typical gas station in a large town. The market is characterized by many

firms, differentiated products, easy entry, and easy exit. If the gas station here is typical,

then in the long run, we would expect to observe:

A)

a few gas stations leaving the market.

B)

new gas stations entering the market.

C)

neither entry nor exit.

D)

many gas stations leaving the market.

Page 26

120.

(Figure: The Market for Gas Stations) The figure The Market for Gas Stations shows

curves facing a typical gas station in a large town. The market is characterized by many

firms, differentiated products, easy entry, and easy exit. If the gas station here is typical,

prices charged by firms in the market are likely to:

A)

fall in the long run.

B)

rise in the long run.

C)

remain unchanged.

D)

rise dramatically in the long run.

121.

(Figure: The Market for Gas Stations) Look at the figure The Market for Gas Stations.

This market is characterized by many firms, differentiated products, easy entry, and

easy exit. In long-run equilibrium, the economic profit earned by the typical gas station

will be:

A)

equal to the level shown in the figure.

B)

negative.

C)

zero.

D)

Not enough information is given to answer the question.

122.

The model of monopolistic competition characterizes the market for plumbing services.

This market is initially in long-run equilibrium, but then there is an increase in the

market demand for plumbing services. We expect that in the long run, the economic

profits of typical firms will be:

A)

typical of those earned by monopoly firms.

B)

negative.

C)

zero.

D)

positive but less than the level typically earned by monopoly firms.

123.

General Snacks is a typical firm in a market characterized by monopolistic competition.

Initially, the market is in long-run equilibrium, and then there is an increase in the

market demand for snacks. In the short run the price of snacks will _____ and the output

of snacks will _____.

A)

fall; fall

B)

remain unchanged; remain unchanged

C)

rise; fall.

D)

rise; rise

Page 27

124.

General Snacks is a typical firm in a market characterized by the model of monopolistic

competition. Initially, the market is initially in long-run equilibrium, and then there is an

increase in the market demand for snacks. We expect that:

A)

in the long run, new firms will enter the market.

B)

there will be a short-run increase in the number of firms, but in the long run the

number of firms will return to the original level.

C)

firms will leave the market in the long run.

D)

firms will shut down, but they will not leave the industry in the long run.

Use the following to answer questions 125-128:

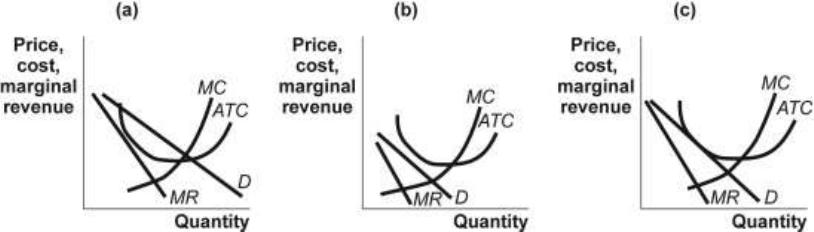

Figure: Monopolistic Competition II

125.

(Figure: Monopolistic Competition II) Panel _____ in the figure Monopolistic

Competition II shows a monopolistic competitor earning a loss in the short run.

A)

(a)

B)

(b)

C)

(c)

D)

None of the panels shows a loss in the short run.

126.

(Figure: Monopolistic Competition II) Which of the panels in the figure Monopolistic

Competition II shows a monopolistic competitor earning a profit in the short run?

A)

panel (a)

B)

panel (b)

C)

panel (c)

D)

panels (a) and (c)

Page 28

127.

(Figure: Monopolistic Competition II) Which panel(s) in the figure Monopolistic

Competition II show(s) a monopolistic competitor producing where price is greater than

marginal revenue?

A)

panel (a)

B)

panel (b)

C)

panel (c)

D)

panels (a), (b), and (c)

128.

(Figure: Monopolistic Competition II) Which panel(s) in the figure Monopolistic

Competition II show(s) a monopolistic competitor in long-run equilibrium?

A)

panel (a)

B)

panel (b)

C)

panel (c)

D)

panels (a), (b), and (c)

Use the following to answer questions 129-131:

Figure: Monopolistic Competition III

Page 29

129.

(Figure: Monopolistic Competition III) The figure Monopolistic Competition III shows

the demand, marginal revenue, marginal cost, and average total cost curves for Pat’s

Pizza Parlor, a monopolistic competitor in the food-to-go industry. The optimal level of

output for Pat’s Pizza Parlor is _____ and the profit-maximizing price is _____.

A)

350; $3.50

B)

350; $7.00

C)

590; $5.60

D)

500; $5.50

130.

(Figure: Monopolistic Competition III) The figure Monopolistic Competition III shows

the demand, marginal revenue, marginal cost, and average total cost curves for Pat’s

Pizza Parlor, a monopolistic competitor in the food-to-go industry. Pat’s Pizza Parlor’s

maximal profit will be:

A)

$0.

B)

$350.

C)

$700.

D)

$900.

131.

(Figure: Monopolistic Competition III) The figure Monopolistic Competition III shows

the demand, marginal revenue, marginal cost, and average total cost curves for Pat’s

Pizza Parlor, a monopolistic competitor in the food-to-go industry. In the long run, the

demand curve for Pat’s Pizza Parlor will shift to the _____ as competitors _____ the

market.

A)

right; enter

B)

right; leave

C)

left; enter

D)

left; leave

132.

Toby operates a small deli downtown. The deli industry is monopolistically competitive.

Toby is producing the quantity that minimizes his average total cost. Assuming that

Toby is maximizing profits, his:

A)

marginal cost is less than his average total cost.

B)

marginal cost is less than his marginal revenue.

C)

price equals his average total cost.

D)

price is more than his average total cost.

Page 30

133.

Toby operates a small deli downtown. The deli industry is monopolistically competitive.

Toby, along with every other deli in town, is producing the quantity that minimizes

average total cost. Assuming the delis are maximizing profits, the:

A)

number of delis will eventually decrease.

B)

number of delis will eventually increase.

C)

delis’ prices equal their average total costs.

D)

delis have excess capacity.

Use the following to answer question 134:

Figure: Monopolistic Competition IV

134.

(Figure: Monopolistic Competition IV) The firm in the figure Monopolistic Competition

IV is producing at the output level that maximizes profits (minimizes losses). The

shaded rectangle depicts the level of:

A)

profit.

B)

loss.

C)

fixed cost.

D)

variable cost.

Use the following to answer questions 135-136:

Figure: Monopolistic Competition V

Page 31

135.

(Figure: Monopolistic Competition V) The figure Monopolistic Competition V

illustrates a firm in the _____; in the _____, the demand and marginal revenue curves

will shift to the _____.

A)

short run; long run; right

B)

long run; short run; left

C)

short run; long run; left

D)

long run; short run; right

136.

(Figure: Monopolistic Competition V) In the figure Monopolistic Competition V, in the

long run firms will:

A)

enter this market until all firms earn zero economic profit.

B)

exit this market until all remaining firms earn zero profit.

C)

enter this market, leading to excess profit for all the firms.

D)

exit this market, leading to excess profit for all the remaining firms.

Use the following to answer questions 137-138:

Figure: Monopolistic Competition VI

137.

(Figure: Monopolistic Competition VI) The figure Monopolistic Competition VI

illustrates a firm in the _____; in the _____, the demand and marginal revenue curves

will shift to the _____.

A)

short run; long run; right

B)

long run; short run; left

C)

short run; long run; left

D)

long run; short run; right

Page 32

138.

(Figure: Monopolistic Competition VI) In the figure Monopolistic Competition VI, in

the long run firms will:

A)

enter this market until all firms earn a zero economic profit.

B)

exit this market until all remaining firms earn a zero economic profit.

C)

enter this market, leading to excess profit for all of the firms.

D)

exit this market, leading to excess profit for all of the remaining firms.

Use the following to answer questions 139-147:

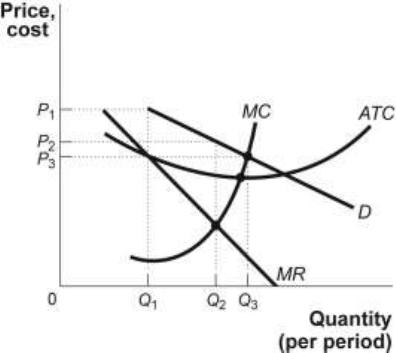

Figure: Profit Maximization in Monopolistic Competition

139.

(Figure: Profit Maximization in Monopolistic Competition) In panel (A) of the figure

Profit Maximization in Monopolistic Competition, the profit-maximizing price and

quantity are _____ and _____.

A)

S; M

B)

P; M

C)

P; Q

D)

T; Q

140.

(Figure: Profit Maximization in Monopolistic Competition) Look at the figure Profit

Maximization in Monopolistic Competition. A firm in monopolistic competition will

maximize profits by producing so that:

A)

P = MC.

B)

MR = MC.

C)

P = MR.

D)

P – ATC (i.e., economic profit per unit) is the largest.

Page 33

141.

(Figure: Profit Maximization in Monopolistic Competition) In the short run, a firm in

monopolistic competition may earn economic profits. The profits in the figure Profit

Maximization in Monopolistic Competition, panel (A), are:

A)

PS.

B)

PS × M.

C)

PS × Q.

D)

PT × Q.

142.

(Figure: Profit Maximization in Monopolistic Competition) Look at the figure Profit

Maximization in Monopolistic Competition. If other firms see economic profits in the

industry, they will enter it, and the demand curve for firms already in the industry will

shift to the _____; in the long run, this will result in an economic profit _____ and a

price _____.

A)

right; equal to zero; equal to ATC

B)

right; greater than zero; greater than ATC

C)

left; less than zero; less than ATC

D)

left; equal to zero; equal to ATC

143.

(Figure: Profit Maximization in Monopolistic Competition) Look at the figure Profit

Maximization in Monopolistic Competition. In monopolistic competition, long-run

equilibrium is characterized by:

A)

P > MR.

B)

P < MR.

C)

P = MR.

D)

profit maximization, which occurs where P = MR = MC.

144.

(Figure: Profit Maximization in Monopolistic Competition) In panel (A) of the figure

Profit Maximization in Monopolistic Competition, if the firm raises its price above P, it

will:

A)

lose all of its customers.

B)

still have some customers.

C)

not lose any customers.

D)

gain many new customers.

Page 34

145.

(Figure: Profit Maximization in Monopolistic Competition) Look at the figure Profit

Maximization in Monopolistic Competition. When the demand curve for a firm in

monopolistic competition shifts, the marginal revenue curve:

A)

must also shift.

B)

shifts in the opposite direction.

C)

will stay the same.

D)

will shift, but the profit-maximizing quantity will not change.

146.

(Figure: Profit Maximization in Monopolistic Competition) In panel (B) of the figure

Profit Maximization in Monopolistic Competition, the long-run equilibrium will result

in:

A)

no economic profits.

B)

no accounting profits.

C)

a tangency of the ATC curve with the MR curve.

D)

no economic profits and a tangency of the ATC curve with the MR curve.

147.

(Figure: Profit Maximization in Monopolistic Competition) In panel (B) of the figure

Profit Maximization in Monopolistic Competition, the profit-maximizing price is P2 and

the ATC curve is tangent to the new demand curve. The portion of the ATC that lies to

the right of the tangency and continues down to the intersection of MC with ATC

indicates:

A)

that the firm is incurring an economic loss.

B)

that the firm is earning an economic profit.

C)

overutilization.

D)

excess capacity.

148.

A monopolistically competitive industry has some of the characteristics of perfect

competition, including:

A)

many firms making economic profit in the long run.

B)

easy entry and exit.

C)

identical products.

D)

easy entry and exit and identical products.

Page 35

149.

Which of the following is TRUE?

A)

For choosing the profit-maximizing quantity, the short-run decision-making

process of a firm in perfect competition is the same as that of a firm in

monopolistic competition, since they produce so that P > MC.

B)

In the long run in perfect competition, economic profits equal zero, and in

monopolistic competition in the long run, economic profits are very large.

C)

In perfect competition, P = MC, and in monopolistic competition, MR = MC, but P

> MC and there is excess capacity.

D)

In both perfect competition and monopolistic competition, P equals minimum

average total cost in the long run.

150.

The price in long-run equilibrium for a monopolistically competitive firm is _____ and

output is _____, compared to that of a perfectly competitive firm with an identical

production function and cost curves.

A)

higher; higher

B)

higher; smaller

C)

lower; higher

D)

lower; smaller

151.

The profit-maximizing rule, expressed as _____, is adhered to by firms operating in a

market that is _____.

A)

MC > MR; monopolistically competitive but not perfectly competitive

B)

MC = MR; both monopolistically competitive and perfectly competitive

C)

MC > MR; perfectly competitive but not monopolistically competitive

D)

MC = MR; either monopolistically competitive or perfectly competitive, depending

on the costs of production

152.

The failure to produce enough to minimize average total cost is termed:

A)

economic profits.

B)

excess capacity.

C)

advertising.

D)

excess production.

153.

The main characteristic that distinguishes monopolistic competition from perfect

competition is:

A)

easy entry and exit.

B)

many firms.

C)

differentiated products.

D)

that in perfect competition, to maximize profits, a firm will produce where MR =

MC.

Page 36

154.

Monopolistic competition in an industry results in:

A)

overutilization of plants.

B)

chronic excess capacity.

C)

less advertising than in perfect competition.

D)

lower prices than in perfect competition.

155.

Long-run equilibrium in perfect competition and in monopolistic competition are similar

because in both models, firms:

A)

produce at the minimum point of the average total cost curve.

B)

set price equal to marginal cost.

C)

make zero economic profits.

D)

have excess capacity.

156.

The broccoli market is perfectly competitive. This means that the price of broccoli is

_____ than if the market were monopolistically competitive, and broccoli output is

_____ than if it were monopolistically competitive.

A)

lower; higher

B)

lower; lower

C)

higher; lower

D)

higher; higher

157.

A monopolistically competitive firm has excess capacity in the long run. This means

that it:

A)

produces less than the output at which average total costs are minimized.

B)

produces less than the output at which price and marginal cost are equal.

C)

could produce more by moving to a larger plant.

D)

doesn’t maximize profits.

158.

The restaurant industry is characterized by excess capacity. This means that:

A)

restaurants are producing more than their profit-maximizing level.

B)

the profit-maximizing level is less than the level that minimizes average total costs.

C)

restaurants are producing less than their profit-maximizing level.

D)

the quantity of restaurant meals supplied exceeds the quantity of restaurant meals

demanded.

Page 37

159.

Firms in the monopolistically competitive movie industry face excess capacity. This

means that there are _____ movies than the output at which _____ cost is minimized.

A)

fewer; marginal

B)

more; average total

C)

fewer; average total

D)

more; marginal

Use the following to answer questions 160-162:

Figure: Comparing Long-Run Equilibriums

160.

(Figure: Comparing Long-Run Equilibriums) In the figure Comparing Long-Run

Equilibriums, which of the following statements is FALSE?

A)

The firm in panel (a) produces where price equals marginal cost and average total

cost.

B)

The firm in panel (b) produces where price equals marginal cost.

C)

The firm in panel (b) produces where price equals average cost.

D)

The firm in panel (a) produces where price equals average cost.

161.

(Figure: Comparing Long-Run Equilibriums) In the figure Comparing Long-Run

Equilibriums, which of the following statements is TRUE?

A)

Firms in the market structure shown in panel (a) cannot have excess profits in the

long run, but those in panel (b) can.

B)

Both panels show markets that have few interdependent firms.

C)

Both panels show markets that produce identical products.

D)

Both panels show markets that have many firms.

Page 38

162.

(Figure: Comparing Long-Run Equilibriums) Look at the figure Comparing Long-Run

Equilibriums. Which of the following statements is FALSE?

A)

Firms in panel (A) cannot have excess profits in the long run, but those in panel (B)

can.

B)

Both panels show markets in which firms are covering all of their implicit and

explicit costs.

C)

Firms in the market shown in panel (A) produce identical products, whereas those

in panel (B) produce similar but differentiated products.

D)

Both firms show markets that have many firms.

163.

Monopolistic competition in an industry will result in _____ because firms produce

_____.

A)

overutilization of plants; the minimum-cost output

B)

less advertising than in perfect competition; the minimum-cost output

C)

lower prices than in perfect competition; more than the minimum-cost output

D)

chronic excess capacity; less than the minimum-cost output

164.

When the profit-maximizing level of output is less than the output associated with the

minimum possible average total cost of production, a firm is said to have:

A)

economic profits.

B)

excess capacity.

C)

advertising.

D)

excess production.

165.

Which of the following is TRUE?

A)

All markets should be oligopolies because that is the most efficient market

structure.

B)

Monopolistic competition results in excess capacity, since in the long run the point

where MR = MC is to the right of the minimum of the ATC curve.

C)

In monopolistic competition firms earn large economic profits in the long run.

D)

In monopolistic competition firms earn zero economic profits in the long run.

166.

In contrast to perfect competition, in monopolistic competition:

A)

entry and exit are easy.

B)

there are many firms.

C)

products are differentiated.

D)

to maximize profits, a firm will produce where MR = MC.

Page 39

167.

Firm A and firm B have identical cost curves. Firm A operates in perfect competition

and firm B operates in monopolistic competition. In the long run, firm A will charge

_____ and produce _____ than firm B.

A)

less; less

B)

more; more

C)

more; less

D)

less; more

168.

Monopolistically competitive firms produce less than the output at which average total

cost is minimized in the long run. As a result, there is:

A)

irrational capacity.

B)

excess capacity.

C)

product differentiation.

D)

zero economic profit.

169.

The excess capacity in monopolistic competition may be viewed as:

A)

the cost of product diversity.

B)

efficient.

C)

the reason P = MR = MC in monopolistic competition.

D)

the advantage of monopolistic competition over monopoly.

170.

Because monopolistically competitive firms charge a price that is greater than marginal

cost:

A)

monopolistic competition is efficient.

B)

monopolistic competition is inefficient.

C)

the marginal benefit to society of an additional unit of output is below its cost.

D)

monopolistic competition is inefficient and the marginal benefit to society of an

additional unit of output is below its cost.

171.

Which of the following is TRUE?

A)

Monopolistic competition and perfect competition are both inefficient.

B)

Monopolistic competition is efficient because of product differentiation.

C)

The inefficiency of monopolistic competition may be a small price to pay for the

wide range of product choices it offers.

D)

The inefficiency of monopolistic competition is a result of advertising expenses.

Page 40

172.

In long-run equilibrium, a firm in monopolistic competition is similar to a monopoly

because it:

A)

earns no economic profit.

B)

charges a price equal to marginal cost.

C)

charges a price greater than marginal cost.

D)

charges a price equal to average total cost.

173.

The problem of wasteful duplication in monopolistic competition is due to:

A)

excess capacity.

B)

a lack of physical and human capital.

C)

barriers to entry.

D)

the lack of close substitutes for products produced by monopolistically competitive

firms.

174.

Excess capacity is a problem in monopolistic competition because if there were fewer

firms in the industry:

A)

there would be more choices for consumers.

B)

average total costs would be higher and profits would be lower.

C)

average total costs would be lower and the prices paid by consumers could be

lower.

D)

there would be less need for government regulation.

175.

Which of the following is TRUE of firms in both perfect competition and monopolistic

competition?

A)

The long-run price is equal to marginal revenue, marginal cost, and average total

cost.

B)

Long-run economic profits are equal to zero.

C)

The long-run level of output is at the point where average total cost is minimized.

D)

Price is equal to marginal cost, ensuring that the efficient level of output is

produced.

176.

In long-run equilibrium in perfect competition, marginal cost is:

A)

greater than price.

B)

equal to price.

C)

less than price.

D)

related to price but not in a predictable way.

Page 41

177.

In long-run equilibrium in monopolistic competition, marginal cost is:

A)

greater than price.

B)

equal to price.

C)

less than price.

D)

related to price but not in a predictable way.

178.

In long-run equilibrium in perfect competition, price is:

A)

greater than average total cost.

B)

equal to average total cost at an output below the point where average total cost is

minimized.

C)

equal to average total cost at its minimum.

D)

equal to average total cost at an output above the point where average total cost is

minimized.

179.

In long-run equilibrium in monopolistic competition:

A)

price is greater than average total cost.

B)

price is equal to average total cost at an output below where average total cost is

minimized.

C)

price is equal to average total cost at its minimum.

D)

price is equal to average total cost at an output above where average total cost is

minimized.

180.

Which of the following scenarios is likely to provide the LEAST amount of economic

usefulness?

A)

NFL player Peyton Manning is shown throwing a football in a toothpaste

commercial.

B)

An online advertisement is posted at Cars.com for a 2005 Volvo S60 with 60,000

miles, a sunroof, and heated leather seats.

C)

An actor in a television commercial is describing the benefits and side effects of a

new arthritis medication.

D)

A radio commercial for a local restaurant is announcing special prices during any

college football broadcast.

181.

A monopolistic competitor is likely to advertise to:

A)

increase the perception of product differentiation in the minds of potential

consumers.

B)

shift the demand curve for its product rightward.

C)

convey information about the product it is offering for sale.

D)

increase the perception of product differentiation in the minds of potential

consumers, shift the demand curve for its product rightward, and convey

information about the product it is offering for sale.

Page 42

182.

Which of the following advertising slogans provides information to potential buyers?

A)

“Coffee Palace—Stop and smell the coffee!”

B)

“Karaoke Maker wants you to just sing it!”

C)

“Bee’s Beachside Restaurant is the only restaurant on the beach for 50 miles.”

D)

“The Happy Hotel has a happy bed for you.”

183.

Some economists think that advertising is a waste of resources because:

A)

rational consumers end up spending too little on brand names.

B)

consumers may buy things they do not need.

C)

advertising creates excess capacity.

D)

advertising leads to lower costs for goods and services.

184.

Advertising is an economically productive activity and NOT a waste of resources

because:

A)

advertisements increase profits.

B)

advertisements can convey information about the product.

C)

if consumers don’t have good information about a product, ads can serve as indirect

signals about the provider.

D)

advertisements can convey information about the product, and if consumers don’t

have good information about a product, ads can serve as indirect signals about the

provider.

185.

Monopolistic competitors often hire a celebrity spokesperson to advertise their product.

One reason such advertising works is that:

A)

celebrities are better informed about the relative merits of different products than

the rest of us.

B)

consumers assume that the celebrity has researched the product and that the claims

being made on his or her behalf are true.

C)

the fact that a firm is willing to pay the large fees associated with celebrity

advertising signals consumers that it is a major company and that it is therefore

likely to have a reliable product.

D)

celebrities encourage other firms to enter the industry.

186.

Budweiser is a widely recognized brand name. During the Super Bowl each year, this

beer company has many of the most successful ads. Which of the following is TRUE

about advertising for Budweiser?

A)

It is designed to increase the demand for Budweiser.

B)

It decreases the costs of supplying Budweiser.

C)

It guarantees customers that Budweiser tastes better than other beers.

D)

It is designed to increase excess capacity.

Page 43

187.

Which of the following is TRUE?

A)

There is no role for advertising in perfect competition.

B)

Firms in monopolistic competition and oligopoly use advertising in expectation of

increasing profit.

C)

Advertising has costs but few if any benefits.

D)

There is no role for advertising in perfect competition, and firms in monopolistic

competition and oligopoly use advertising in expectation of increasing profit.

188.

Critics of advertising argue that it:

A)

tends to make markets more perfect.

B)

leads to low-cost mass production.

C)

results in higher prices to consumers.

D)

encourages competition through new-product advertising.

189.

Those who are critical of advertising argue that it:

A)

tends to make markets behave more like perfectly competitive markets.

B)

leads to a shortage of high-cost, high-quality goods.

C)

results in higher prices to consumers.

D)

encourages competition through price comparison.

190.

Defenders of advertising argue that it:

A)

seeks to persuade rather than inform buyers.

B)

provides education and information about products.

C)

facilitates the concentration of monopoly power.

D)

encourages artificial product differentiation.

191.

Advertising is an economically productive activity and NOT a waste of resources

because it:

A)

increases sales.

B)

can convey information about the product.

C)

can signal that firms are desperate for customers.

D)

can decrease the costs of production.

Page 44

192.

Which of the following is CORRECT about celebrity spokespersons?

A)

Celebrities are better informed about the relative merits of different products than

the rest of us.

B)

Celebrity advertising signals consumers that the product is reliable, because the

firm is willing to pay the high fees associated with hiring a celebrity.

C)

Consumers assume that the celebrity has researched the product and that the claims

being made on his or her behalf are true.

D)

None of the statements is correct.

193.

Among the drawbacks of brand names is the fact that:

A)

they may encourage the consumption of expensive substitutes for generic items.

B)

they provide some assurance of consistency of quality.

C)

they convey information about the nature of the product.

D)

they indicate that the seller is engaged in repeated interaction with its customers.

Use the following to answer questions 194-199:

Page 45

194.

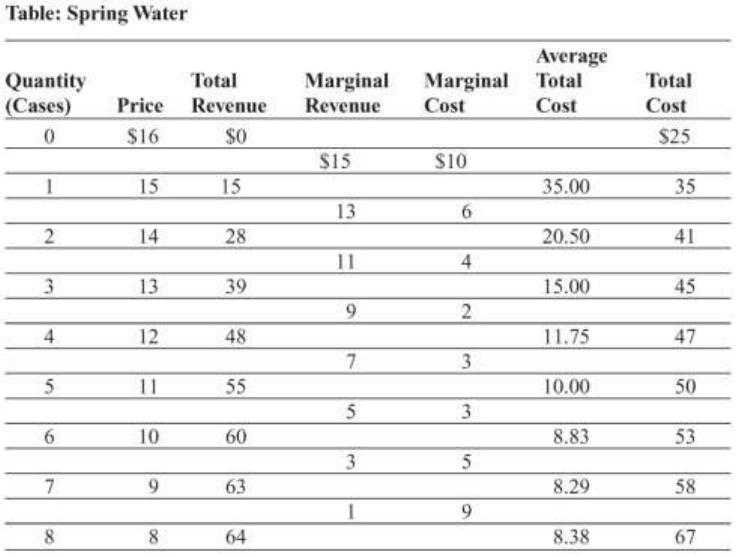

(Table: Spring Water) The table Spring Water shows the demand and cost data for a

firm in a monopolistically competitive industry producing drinking water from

underground springs. The profit-maximizing output is _____ cases.

A)

5

B)

6

C)

7

D)

8

195.

(Table: Spring Water) The table Spring Water shows the demand and cost data for a

firm in a monopolistically competitive industry producing drinking water from

underground springs. The profit-maximizing price is:

A)

$16.

B)

$3.

C)

$5.

D)

$10.

196.

(Table: Spring Water) The table Spring Water shows the demand and cost data for a

firm in a monopolistically competitive industry producing drinking water from

underground springs. At the profit-maximizing output, profit is:

A)

$9.00.

B)

$10.00.

C)

$60.00.

D)

$7.00.

197.

(Table: Spring Water) The table Spring Water shows the demand and cost data for a

firm in a monopolistically competitive industry producing drinking water from

underground springs. At the profit-maximizing output, profit per unit is:

A)

$1.17.

B)

$8.83.

C)

$10.00.

D)

$11.75.

198.

(Table: Spring Water) The table Spring Water shows the demand and cost data for a

firm in a monopolistically competitive industry producing drinking water from

underground springs. If the industry were in perfect competition, the profit-maximizing

output would be _____ cases.

A)

6

B)

5

C)

7

D)

8

Page 46

199.

(Table: Spring Water) The table Spring Water shows the demand and cost data for a

firm in a monopolistically competitive industry producing drinking water from

underground springs. If the industry were in perfect competition, the profit-maximizing

price would be:

A)

$10.00.

B)

$6.50.

C)

$8.38

D)

$8.29

200.

Shops that sell live bait to people in Alabama may be monopolistically competitive if

there is product differentiation and differentiation by location.

A)

True

B)

False

201.

The hamburger industry has some differentiation and many firms. This suggests that the

hamburger industry is more oligopolistic than monopolistically competitive.

A)

True

B)

False

202.

Gas stations are not monopolistically competitive, because everyone knows the gasoline

is the same regardless of where it is purchased.

A)

True

B)

False

203.

Tacit collusion is NOT feasible in monopolistic competition because of the large

number of competing firms.

A)

True

B)

False

204.

As product differentiation increases, the price elasticity of demand falls and the firm

increases its market power.

A)

True

B)

False

205.

Monopolistic competition is unique among the four market structures in that it is the

only one that is always characterized by product differentiation.

A)

True

B)

False

Page 47

206.

Monopolistic competition is often found in service industries.

A)

True

B)

False

207.

Competition limits the price a monopolistically competitive firm can set.

A)

True

B)

False

208.

If the Boston doughnut market is monopolistically competitive and the firms are earning

short-run profits, consumers in Boston will see less diversity in the doughnuts offered

over time.

A)

True

B)

False

209.

In monopolistic competition, the primary source of product differentiation is price

competition.

A)

True

B)

False

210.

The best way for firms in monopolistic competition to gain market power is to engage in

tacit collusion.

A)

True

B)

False

211.

Firms in monopolistic competition can gain some market power by engaging in product

differentiation.

A)

True

B)

False

212.

Economics textbooks are an example of product differentiation by type and style.

A)

True

B)

False

213.